Fashion Maternity Clothing Market Overview: Growth Outlook and Strategic Insights

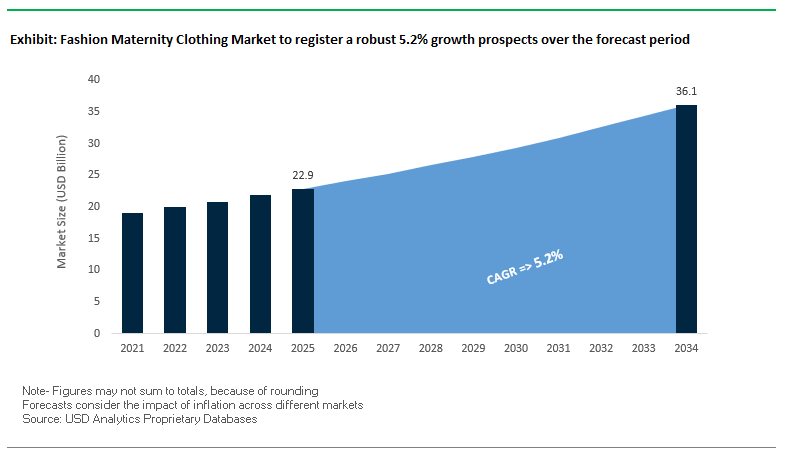

The global maternity fashion wear market is anticipated to increase from USD 22.9 billion in 2025 to USD 36.1 billion in 2034 with a CAGR of 5.2%. This segment is where comfort, fashion, and functionality meet, serving pregnant women who require practicality alongside beauty. As consumer attitude shifts, maternity fashion companies are expanding their offerings beyond conventional silhouettes to adaptive, transitional pieces that can be used pre-pregnancy, in pregnancy, and even after pregnancy. It is also fueled by e-commerce penetration, innovation in fabrics, and sustainability-driven product innovation.

Key Insights for Industry Professionals

- Premium Fabric Focus – Soft, breathable, and stretchable fabrics like cotton dominate, ensuring comfort without compromising style.

- Modernized Aesthetics – A clear shift from oversized, shapeless maternity wear toward contemporary, trend-aligned designs.

- Smart Apparel Integration – Innovative lines now include antimicrobial and moisture-wicking materials, and in some cases, wearable tech for health monitoring.

- E-commerce Leadership – Online platforms are the primary growth channel, offering convenience and a wider assortment for customers with mobility limitations.

- Transitional Wear Boom – Adjustable waistbands, nursing access, and flexible fabrics are increasing the lifecycle value of maternity apparel.

Fashion Maternity Clothing Market Analysis: Strategic Developments and Industry Momentum

The maternity fashion industry is changing fast, spurred by sustainability, diversity, and retail technology. In March 2025, H&M Group accelerated its sustainability ambitions through its venture Syre, aiming at expanding textile-to-textile recycled polyester production. This is just one component of an industry-wide shift toward circular fashion systems, a priority as conscious consumption trends continue to gain momentum.

Seraphine's May 2025 opening of its New York flagship is a major U.S. expansion effort targeting urban, fashion-conscious business professionals. Strategic investment enables the brand to provide a personalized in-store experience and build out its U.S. e-commerce platform. In August 2025, Shein's Sustainability Report detailed improvements to supplier standards and the use of renewable energy, reaffirming sustainability as a competitive differentiator.

Product category extension is also having an impact. Uniqlo's March 2025 launch of specialized maternity and newborn "LifeWear" lines is an extension of its comfort-and-function-over-style philosophy, further broadening its mass-market appeal. Isabella Oliver's August 2024 rental service, on the other hand, offers a new model for sustainable maternity fashion, enabling short-term rental of luxury garments. HATCH's August 2025 new collection furthered its focus on postpartum-friendly fashion, reinforcing its "4th Trimester" positioning and enabling long-term wardrobe longevity.

Innovative Trends and Growth Opportunities in the Fashion Maternity Clothing Market

Wearable Postpartum Tech Redefining Maternity Clothing Beyond Pregnancy

The maternity apparel market is expanding to address postpartum recovery, integrating wearable smart technology into garments to support maternal health. A 2024 JMIR mHealth and uHealth study verified that consumer-level wearables such as smartwatches and fitness trackers supplemented by machine learning algorithms accurately detected risk for postpartum depression through monitoring of heart rate, sleep, and activity. This scientific proof is driving postpartum-ready wear innovation, wherein sensors and AI-powered monitoring platforms in apparel provide new mothers with personal recovery feedback. Increasing awareness of postpartum health issues and widespread adoption of wearable health technology make specialized postpartum wear a natural progression. Companies such as Trellis Health are pioneering this intersection with AI-powered platforms that combine health monitoring, in-home lab testing, and telehealth care, a new market wherein fashion, medical science, and technology converge.

Office-to-Maternity Transition Wear Meeting the Needs of the Modern Working Woman

Since over 60% of working pregnant women in industrialized countries continue to work throughout pregnancy, professional maternity fashion is on the rise. The trend is driving the adoption of corporate-chic, stretch, and flexible designs that transform from boardroom to casual wear without the need for a change of clothes. While casual wear is the most common in the maternity fashion marketplace, the most rapidly expanding segment is formal wear, driven by more fashion-forward working mothers who are willing to spend money for high-quality, transitional garments. Maternity consumer research confirms that working pregnant women are concerned with fashion and comfort but seek clothing that adapts to changing body shapes without sacrificing a professional look.

Plug the Plus-Size Maternity Fashion Gap

The plus-size maternity wear segment is still under-developed despite the plus-size women's wear market worldwide being worth billions. The body positivity phenomenon and increased media coverage of diverse body types are pushing consumers to ask for inclusive sizing. Brands that are starting to make the change are stocking maternity ranges in US sizes 10–28 but the segment is still a comparatively under-developed growth space. The research shows plus-size demand is extremely strong in occasion wear and outerwear, so the category is a high-value opportunity for brands to offer fashionable, well-fitting designs for every body type.

Subscription Rental Models for Short-Term Maternity Needs

With the temporary use of maternity clothing, rental and subscription models are emerging as affordable, sustainable solutions. Studies of apparel rental identify maternity apparel as one of the most appropriate product lines for the model, with environmental advantages including lower greenhouse gas emissions. Rental models are appealing to price-sensitive, urban, style-oriented consumers who enjoy variety at a lower cost than storage or ownership. Trimester-specific, curated boxes are now available in maternity rental subscription companies to enable women to experience high-quality, seasonally appropriate wardrobes at every stage of pregnancy.

Fashion Maternity Clothing Market Share Insights

Fashion Maternity Apparel Market Share by Material: Cotton Dominates with Green Options Increasing

Cotton is the market leader at 38%, favored for its comfort, breathability, and hypoallergenic nature suitable for sensitive skin and ideal for changing climatic conditions. Organic cotton is increasingly popular as sustainability becomes the buying criterion. Polyester at 22% is budget-friendly but is under environmental attack; recycled polyester is increasingly a greener choice that is gaining traction. Spandex and Lycra have seen demand increase by 25% since 2020 because of the need for stretchy fits in leggings, nursing bras, and active maternity. Viscose and rayon are valued for their drape and softness, especially in dresses and tunics, while wool maintains its stable position in high-end winter maternity coats. Other sustainable alternatives like bamboo, Tencel, and modal are increasingly popular among eco-aware millennial and Gen Z shoppers seeking fashionable yet responsible maternity wear.

.png)

Maternity Fashion Apparel Market Share by Price Segment: Economical and Mid Segments Are Dominant, Luxury Experiences Niche Growth

Low-cost maternity wear holds 40% market share, led by fast fashion shops like H&M Mama and ASOS Maternity targeting price-conscious consumers. The mid-level segment holds 35%, with mass merchants like Gap and Motherhood Maternity offering style, quality, and affordability in one package targeting working women who need practical wardrobe solutions. High-end and luxury maternity wear holds smaller but increasing percentages led by celebrity endorsement, designer endorsement, and increased social media exposure of high-end maternity fashion. Luxury brands like Seraphine and Tiffany Rose are entering this niche market with custom and high-end maternity solutions for upscale occasions.

Competitive Landscape – Key Players Shaping the Fashion Maternity Clothing Industry

The market is led by a blend of dedicated maternity fashion specialists and mainstream apparel giants with specialized maternity lines, each leveraging distinct competitive strengths. Key players included are H&M, Gap Inc., Seraphine, Isabella Oliver, Motherhood Maternity, ASOS, Hatch, Thyme Maternity, PinkBlush Maternity, Ingrid+Isabel, JoJo Maman Bébé, Beyond Yoga, Zara, Mango, Storq, Old Navy, Boob, Others.

Seraphine – Premium, Endorsed, and Expanding Globally

Seraphine is renowned for blending high fashion aesthetics with functionality, winning endorsements from high-profile figures such as the Duchess of Cambridge. Its product portfolio spans everyday essentials to luxury occasion wear, often with discreet nursing access. The brand’s May 2025 New York store launch expands its global retail footprint and positions it strategically in a key luxury fashion market.

H&M MAMA – Affordable, Trend-Led Maternity Wear

H&M’s maternity line delivers trend-conscious, accessible fashion to a mass audience. Offering denim, basics, occasion wear, and activewear, its designs feature adjustable fits and sustainable materials. Integrated into H&M’s broader sustainability goals, H&M MAMA aligns fashion-forward maternity wear with environmental responsibility.

HATCH Collection – Luxury Maternity for All Stages

HATCH stands out for its “Before, During, and After” philosophy, ensuring product relevance across motherhood stages. Known for its elevated fabrics and timeless silhouettes, the brand also extends into maternity-safe beauty products, creating a complete lifestyle ecosystem. Its marketing challenges traditional maternity aesthetics, appealing to the modern, style-conscious mother.

United States: Policy-Driven Growth, Multifunctional Designs, and Digital Transformation

The United States fashion maternity clothing market is evolving under the influence of government policies and tech-driven innovation. The Family and Medical Leave Act (FMLA) is anticipated to boost maternity apparel usage by supporting extended maternity periods, while federal technology development grants are helping brands integrate virtual fitting rooms and augmented reality try-on tools. These technologies are especially impactful for e-commerce maternity brands, reducing sizing concerns and enhancing customer confidence in online purchases.

Product innovation is a core market driver, with brands developing multifunctional apparel that transitions from pregnancy to postpartum, offering higher cost-per-wear value. Examples include maternity activewear with antimicrobial and moisture-wicking fabrics, adjustable waistbands, and discreet nursing access. Social media platforms are amplifying consumer demand for body-positive designs that reflect pre-pregnancy fashion trends, blurring the line between maternity wear and mainstream style. Sustainability is another emerging focus, with organic cotton, recycled fabrics, and government-backed textile recycling initiatives shaping brand strategies. This combination of policy support, style-conscious innovation, and sustainable production is positioning the U.S. market as a leader in premium and eco-conscious maternity fashion.

China: E-Commerce Dominance, Premiumization, and Technological Integration

China’s fashion maternity clothing market is deeply influenced by the nation’s e-commerce ecosystem, supported by high smartphone penetration and AI-powered personalization. Platforms offer tailored product recommendations, targeted ads, and nationwide delivery networks, making maternity apparel accessible to both urban and rural consumers. Premiumization is a growing trend, with rising disposable incomes fueling demand for luxury-quality maternity wear that blends functionality with safety-certified materials.

Sustainability is also gaining traction, with brands using organic, biodegradable, and non-toxic fabrics to appeal to younger, environmentally conscious buyers. Technological integration is advancing quickly brands are using data analytics for demand forecasting and exploring thermal comfort innovations such as insulating maternity garments for hospital use. Coupled with China’s robust manufacturing infrastructure and government investment in high-tech industries, the sector is well-positioned for both domestic dominance and global export growth.

France: Regulatory Sustainability and High-End Functional Design

France is shaping its maternity fashion market through stringent textile regulations and eco-conscious legislation. The upcoming ban on PFAS “forever chemicals” in textiles by 2030, likely to be adopted EU-wide, will directly influence material sourcing. The country’s proposed eco-score labeling system and anti-fast fashion measures are encouraging brands to prioritize durability and sustainability in maternity wear.

French maternity clothing maintains a strong emphasis on quality and style, often targeting professional women with elegant workwear and formalwear. Innovation is evident in the use of smart textiles, seamless construction, and breathable fabrics, alongside niche offerings such as radiation protection apparel for expectant mothers. This blend of legislative pressure, high-fashion influence, and advanced material technology ensures France remains a key hub for stylish, safe, and sustainable maternity fashion.

Germany: Sustainability Leadership and Advanced Material Development

Germany’s maternity fashion market benefits from a strong national framework for sustainable textile production. The “Grüner Knopf” (Green Button) certification guides consumers toward verified eco-friendly clothing, while the Supply Chain Due Diligence Act enforces transparency and accountability. Public-private initiatives like the Partnership for Sustainable Textiles are further embedding sustainability into manufacturing practices.

Material innovation is a hallmark of the German market, with growing adoption of hemp, flax, nettle fibers, and bio-based polyesters, reducing water use and environmental impact. Maternity brands are leveraging these materials for comfort-focused, eco-friendly garments that meet stringent EU quality standards. This regulatory and innovation-driven environment is making Germany a leader in both sustainable production and consumer trust in maternity clothing.

Brazil: Rising Domestic Demand, Product Innovation, and Ethical Oversight

Brazil’s maternity clothing sector is expanding rapidly, driven by the rising middle class, greater awareness of maternal health, and a shift toward sustainable consumption. While technology adoption is gradual, wearable health monitors and pregnancy-related mobile apps are entering the market, offering integrated wellness solutions for expectant mothers.

Product innovation is increasingly visible in postpartum shapewear collections featuring seamless technology and premium fabrics, catering to both functionality and style. Ethical oversight is also improving, supported by initiatives like Moda Livre, which monitors labor conditions in the apparel sector. As sustainability and ethical manufacturing gain ground, Brazil’s maternity fashion industry is transitioning from purely price-driven to quality and values-driven, strengthening its appeal to modern consumers.

Fashion Maternity Clothing Market Report Scope

Fashion Maternity Clothing Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$22.9 Billion

|

|

Market Size (2034)

|

$36.1 Billion

|

|

Market Growth Rate

|

5.2%

|

|

Segments

|

By Product (Apparel (Loungewear, Formalwear, Swimwear, Lingerie, Others), Footwear), By Material (Cotton, Polyester, Spandex & Lycra, Viscose, Rayon, Wool, Others), By Distribution Channel (Online (E-commerce Websites, Company-Owned Websites), Offline (Hypermarkets & Supermarkets, Specialty Stores, Mono-brand Stores, Others)), By Application (Pregnancy, Postnatal), By Pricing (Economical, Medium, Fine, Luxury)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

H&M, Gap Inc., Seraphine, Isabella Oliver, Motherhood Maternity, ASOS, Hatch, Thyme Maternity, PinkBlush Maternity, Ingrid+Isabel, JoJo Maman Bébé, Beyond Yoga, Zara, Mango, Storq, Old Navy, Boob, Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fashion Maternity Clothing Market Segmentation

By Product

- Apparel

- Loungewear

- Formalwear

- Swimwear

- Lingerie

- Others

- Footwear

By Material

- Cotton

- Polyester

- Spandex & Lycra

- Viscose

- Rayon

- Wool

- Others

By Distribution Channel

- Online

- E-commerce Websites

- Company-Owned Websites

- Offline

- Hypermarkets & Supermarkets

- Specialty Stores

- Mono-brand Stores

- Others

By Application

By Pricing

- Economical

- Medium

- Fine

- Luxury

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Fashion Maternity Clothing Market

- H&M

- Gap Inc.

- Seraphine

- Isabella Oliver

- Motherhood Maternity

- ASOS

- Hatch

- Thyme Maternity

- PinkBlush Maternity

- Ingrid+Isabel

- JoJo Maman Bébé

- Beyond Yoga

- Zara

- Mango

- Storq

- Old Navy

- Boob

* List Not Exhaustive

Research Coverage

This report investigates the global Fashion Maternity Clothing Market with a boardroom-ready lens—delivering breakthroughs, analysis reviews, and highlights that decode how product innovation, inclusive sizing, premium materials, and omnichannel execution are reshaping demand across maturity stages. Produced by USDAnalytics, the study benchmarks competitive moves of specialty and mass brands, quantifies pricing-tier dynamics, and maps regulatory and sustainability influences that will steer sourcing and merchandising through 2034. This report is an essential resource for executives, investors, product leads, and retail operators who need granular, decision-grade evidence on where value will be created—from postpartum tech-enabled apparel to office-to-maternity transition wear and rental-led circular models. Scope includes-

- Segmentation covered:

- By Product: Apparel; Footwear

- By Material: Cotton; Polyester; Spandex & Lycra; Viscose; Rayon; Wool; Others

- By Distribution Channel: Online; Offline

- By Application: Pregnancy; Postnatal

- By Pricing: Economical; Medium; Fine; Luxury

- Geographic scope: 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Time horizon: Historical 2021–2024; Forecast 2025–2034.

- Company coverage: Strategic analyses/profiles of 15+ leading players.

Methodology

USDAnalytics applies a triangulated research design blending primary and secondary evidence. Primary inputs include structured interviews and surveys with maternity brand executives, retail buyers, fabric technologists, e-commerce leaders, and healthcare-adjacent innovators (wearables/telehealth). Secondary inputs span customs/trade datasets, ESG disclosures, patent and certification databases, retailer sell-through indicators, and public financials. We deploy market-sizing from the bottom up (channel × pricing tier × material) validated by a top-down reconciliation to national apparel baselines. Forecasts use cohort-driven demand modeling, price/mix elasticity, and regulatory scenario stress tests. Competitive positioning is assessed via value-chain mapping, assortment benchmarking, and a capability heat map across design agility, inclusivity, and sustainability. All outputs undergo consistency checks and sensitivity analysis to deliver reliable, decision-ready insights.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.