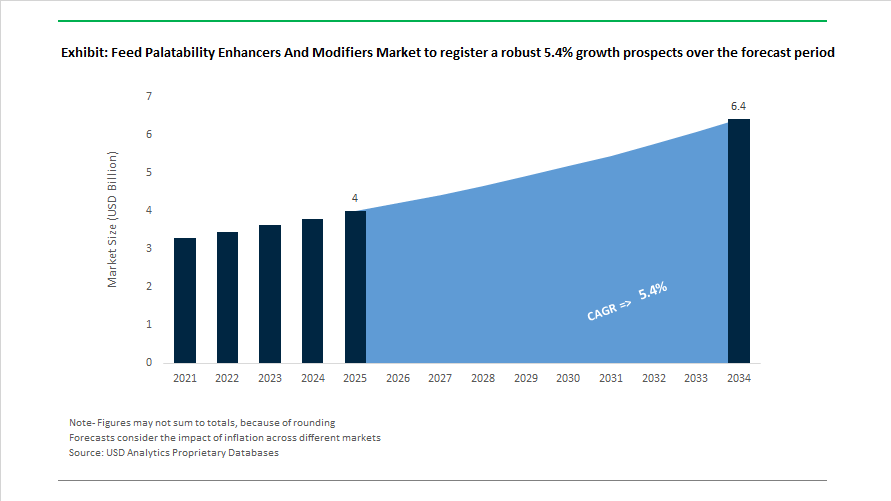

Feed Palatability Enhancers and Modifiers Market Size 2025–2034: $4 Billion to $6.4 Billion at 5.4% CAGR Driven by Natural and Enzyme-Based Innovations

The Feed Palatability Enhancers and Modifiers Market is projected to expand from $4 billion in 2025 to $6.4 billion by 2034, registering a CAGR of 5.4%. Growth is anchored in the structural shift toward antibiotic-free livestock production, precision nutrition, and premiumization in pet food. Palatability enhancers have evolved from simple flavor additives to multifunctional feed solutions that optimize feed intake, improve feed conversion ratios, and stabilize consumption in variable raw material environments. Rising inclusion of alternative proteins, high-protein concentrates, and mineral-rich premixes has increased the need for advanced taste-masking agents, aroma modifiers, buffered organic acids, and enzyme-enhanced palatants.

In February 2023, Adisseo Group completed the acquisition of Nor-Feed Holding, strengthening its botanical extract portfolio and expanding its presence in natural feed additives. The transaction positioned Adisseo to capture demand for plant-based palatability enhancers aligned with sustainable livestock nutrition. During 2023, Glanbia Nutritionals expanded its flavor solutions portfolio, incorporating taste-masking technologies that address bitterness in high-protein and mineral-fortified animal feed formulations. In 2023, Ajinomoto entered into a strategic alliance with Solar Foods to improve the sensory characteristics of microbial protein sources such as Solein, targeting aquaculture and livestock feed applications where palatability remains a barrier to adoption.

Product innovation accelerated in 2024 and 2025. In early 2024, Kerry Group acquired the lactase enzyme business of Chr. Hansen and Novozymes, integrating advanced biotechnology into dairy-based feed and pet treat applications to refine taste profiles and address lactose sensitivity. In late 2024, Cargill and Novozymes announced a collaboration to develop enzyme-enhanced palatants designed to improve poultry feed intake while stimulating digestive enzyme activity. In 2024, Symrise AG launched its ONE CARE initiative, integrating human-grade flavor and aroma technologies into the pet food palatability segment. In March 2025, Kemin introduced PROSIDIUM at VIV Asia, followed by continued expansion of its PALIVATE line for wet, dry, and liquid pet food formats. At IPPE 2025, Selko, part of Trouw Nutrition, debuted the Selko AlpHa acidification strategy designed to preserve intake even at higher organic acid inclusion levels. According to the 2025 Alltech Agri-Food Outlook, nearly 55% of global livestock producers now deploy palatability enhancers, with notable adoption in poultry during 2024 to offset raw material variability in emerging markets.

Trends and Opportunities in the Feed Palatability Enhancers and Modifiers Market

Integration of Flavor-Masking and Bitter Blockers for Alternative Proteins

The global shift toward circular and sustainable feed formulations has introduced insect meal, single-cell proteins, algae, and oilseed by-products into mainstream livestock diets. While nutritionally attractive, these ingredients often carry metallic, earthy, or bitter off-notes that negatively impact voluntary feed intake.

In late 2024, ADM, through its Pancosma division, reported a sharp increase in R&D investment focused on bitter-blocking chemistry. These systems combine high-intensity sweeteners, nucleotides, and yeast-derived compounds to suppress bitterness from alkaloids in rapeseed meal and mitigate the fishy odor associated with algae-based proteins. Rather than simply masking flavors, these solutions actively modulate gustatory receptors by dampening bitter signals while amplifying umami perception, improving acceptance across monogastric species.

Yeast extracts have emerged as a cornerstone of this strategy. Industry publications in late 2024 highlighted their role as multifunctional palatants, delivering roasted and meaty notes that appeal strongly to carnivorous fish species and companion animals. Their naturally high amino acid content also helps mask the taste of vitamins and trace minerals, which are increasingly added at higher inclusion rates in functional feeds.

From a formulation standpoint, the importance of flavors has structurally increased. By 2025, flavors accounted for roughly 38% of the sensory additive segment, driven by the need to maintain average daily gain when alternative proteins are included at levels approaching 15%. This trend underscores palatability enhancers as enablers of sustainable feed economics rather than cosmetic additives.

Precision Application via Microencapsulation and Post-Pelleting Liquid Systems

Modern feed processing environments place severe thermal and mechanical stress on sensory additives. To preserve efficacy, manufacturers are rapidly adopting microencapsulation and post-processing application technologies that protect volatile aromatics and heat-sensitive sweeteners.

Scientific reviews published in 2025 demonstrated that microencapsulation using lipid or polymer matrices significantly improves additive stability during pelleting, where temperatures routinely exceed 85°C. By shielding active compounds until they reach the lower gastrointestinal tract, encapsulation enhances bioavailability and ensures consistent flavor release, even in high-density diets.

Post-Pelleting Liquid Application has moved from a premium feature to an industry standard in high-value feeds. Applying palatability enhancers after pellet cooling, typically at 40 to 250 grams per ton, eliminates thermal degradation and preserves nearly all aroma potency. In contrast, additives introduced before pelleting can lose up to 40% of their sensory impact.

Precision dosing is also becoming data-driven. In 2024, Cargill expanded the deployment of its FeedWatch platform across hundreds of broiler operations. By dynamically adjusting flavor intensity during heat-stress periods, the system stabilized intake and improved feed conversion ratios by measurable margins, demonstrating that palatability optimization can be responsive rather than static.

Supporting Antibiotic-Free and Zinc-Free Swine Production Systems

Regulatory bans on therapeutic Zinc Oxide in Europe and rising global pressure to reduce in-feed antibiotics have created a structural need for non-pharmaceutical solutions that maintain feed intake during critical growth phases. Palatability enhancers have become essential components of post-weaning nutrition strategies.

A November 2025 study confirmed that formulations containing glutamate and sucrose analogs stimulate key taste receptors in piglets, promoting early feed intake and supporting gut integrity. This intake stability is crucial in preventing post-weaning diarrhea, particularly in systems where ZnO is no longer permitted.

Field data from research institutions show that in antibiotic-free systems, average daily feed intake can drop by up to 20% during the first post-weaning week. Flavor-enhanced diets have consistently reduced this decline, preserving growth trajectories and shortening time to market. As producers in Southeast Asia and South America begin aligning with European regulatory models, demand for palatability-driven gut health solutions is accelerating.

Acceptance and Compliance in Specialty and Therapeutic Pet Nutrition

Pet food is one of the fastest-evolving end-use segments for palatability enhancers, driven by the medicalization and humanization of companion animals. Veterinary therapeutic diets often restrict salt, fat, or protein sources, making sensory acceptance a primary barrier to compliance.

In 2024, Purina and Royal Canin expanded their veterinary portfolios with a sensory-first approach. For chronic kidney disease and metabolic disorders, these diets rely on fermented fish proteins and hydrolyzed liver extracts to deliver high palatability without compromising clinical objectives. Ensuring consistent intake is directly linked to treatment success and medication adherence.

Consumer research reinforces this dynamic. Surveys conducted in 2024 showed that 85% of pet owners rank palatability as the most important factor when selecting a therapeutic diet. This preference has fueled double-digit growth in super-premium wet foods, which command substantial price premiums due to advanced flavor-delivery systems.

As hypoallergenic and novel-protein diets gain traction for pets with food sensitivities, species-specific palatants are becoming indispensable. These additives help overcome unfamiliar aroma profiles from insect or hydrolyzed proteins, ensuring caloric intake is maintained even among selective animals.

Feed Palatability Enhancers and Modifiers Market Share and Segmentation Insights

Precision Animal Nutrition Drives Flavor Systems to Lead Palatability Enhancer Demand

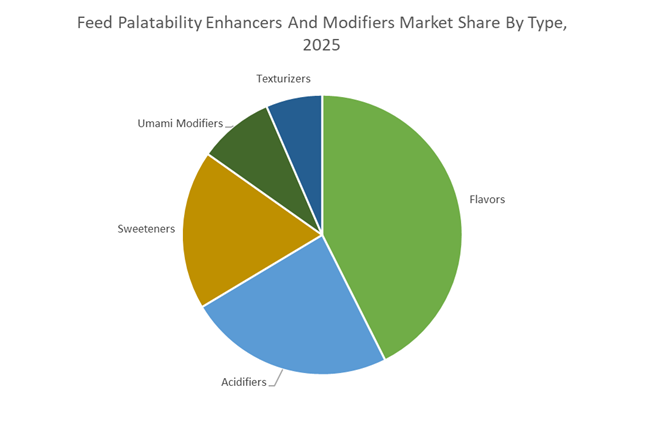

Flavors accounted for 42.60% of the Feed Palatability Enhancers and Modifiers Market share in 2025, making them the most widely used ingredient category in modern animal feed formulation. Their dominance stems from the ability to directly improve feed palatability, aroma, and taste acceptance, which are critical factors influencing feed intake across livestock species including swine, poultry, ruminants, and aquaculture. Feed manufacturers increasingly rely on advanced flavor systems to overcome common palatability barriers created by high-protein diets, alternative feed ingredients, antibiotics replacement programs, and plant-based protein formulations. In 2025, the feed additives industry has moved toward species-specific precision flavor engineering, representing a major evolution in palatability technology. Flavor developers are designing formulations aligned with animal taste receptor biology, enabling targeted stimulation of taste perception. For example, umami-rich flavor compounds are used to enhance swine feed acceptance, anise-based aromatic systems improve ruminant feed intake, while marine-based attractants are optimized for aquaculture feeds. These specialized flavor technologies significantly improve first-feed acceptance, feed conversion efficiency, and early-stage growth performance, reinforcing flavors as the most critical component within the global feed palatability enhancers and modifiers market.

Appetite Stimulation Functions Lead Feed Palatability Technologies Supporting Livestock Growth Efficiency

Appetite stimulation represented 38.70% of the Feed Palatability Enhancers and Modifiers Market share in 2025, highlighting its central role in optimizing livestock productivity, feed conversion ratios, and growth performance. In commercial animal production systems, even small reductions in feed intake can significantly impact weight gain, feed efficiency, and overall farm profitability, making appetite stimulation technologies a critical component of modern feed formulation strategies. Palatability enhancers designed for appetite stimulation help animals maintain consistent feeding behavior during diet changes, early-life feeding stages, transportation stress, or environmental challenges. A notable innovation shaping the market in 2025 is the emergence of early-life flavor programming strategies in animal nutrition. Scientific studies show that exposing animals to specific flavor compounds during gestation, lactation, or early hatch stages can influence taste familiarity and feed acceptance later in life. This insight has led to the development of integrated flavor continuity programs, such as “sow-to-piglet” and “hen-to-chick” feeding systems, where identical flavor profiles are incorporated into maternal diets and later into starter feeds. These programs reduce post-weaning stress, improve feed transition efficiency, and stabilize feed intake, reinforcing appetite stimulation as the leading functional application in the feed palatability enhancers and modifiers market.

Competitive Landscape in Feed Palatability Enhancers And Modifiers Market

Symrise Pet Food Dominates the Global Pet Food Palatability Segment

Symrise Pet Food operates 31 sites globally with more than 1,500 experts, positioning it as the global leader in pet food palatability enhancers. Under the SPF brand, the company supplies a broad portfolio of liquid and dry palatants, including the Nutri and Sense lines that address both premium and economy pet food formulations. In early 2026, the appointment of Fernando Bocabello as President marked a new phase of global expansion, reinforced by the inauguration of a major production facility in Latin America to serve Brazil and Argentina, two high-growth pet food markets. Its Panelis centers utilize expert cat panels to decode feline umami preferences, enabling the launch of fermented protein hydrolysates tailored to species-specific taste receptors. Through full side-stream valorization, Symrise converts poultry and fish by-products into high-value savory palatants, strengthening its circular economy credentials while ensuring supply stability in the global feed palatability enhancers market.

Kemin Industries Strengthens Heat-Stable Palatant Technology for Livestock and Pet Feed

Kemin Industries maintains a strong presence across both livestock feed additives and pet food palatability solutions, supported by advanced molecular science capabilities. Its PALASURANCE® portfolio addresses companion animal applications, while AMPLIVITA™ and EnerFAT™ PLUS target livestock flavor and energy enhancement requirements. In late 2025, Kemin released research on PALIVATE™ WP, a palatant engineered to withstand retort processing temperatures of 130°C in wet pet food, ensuring post-processing flavor retention and feed acceptance. The company integrates antioxidant technologies to prevent lipid oxidation in fat-based flavor carriers, a critical factor in reducing feed refusal rates. Strategic expansion in Asia Pacific, particularly India and China, focuses on dairy cattle palatants designed to mask off-flavors associated with high-yield bypass fats. This combination of heat stability, oxidative control, and regional market penetration reinforces Kemin’s leadership in feed palatability modifiers and taste optimization solutions.

Adisseo Expands Natural Smart Flavor Solutions for Poultry and Swine

Adisseo, backed by Bluestar under ChemChina ownership, holds a strong position in poultry and swine palatability enhancers within the livestock nutrition market. The acquisition of Nor-Feed accelerated its transition toward natural botanical extracts, addressing growing demand for plant-based feed additives and clean-label livestock solutions. Its Delistee and Krave brands apply Smart Flavor technology, delivering species-specific aromas that maintain stability during pelleting and extrusion processes common in compound feed manufacturing. Adisseo differentiates by integrating palatability with its Digestive Performance platform, ensuring enhancers work synergistically with enzymes to improve feed conversion ratios and nutrient absorption. The company is expanding its Palatability Solutions service model, providing on-site technical assistance to feed mills for optimized liquid enhancer application. This technical integration approach strengthens Adisseo’s position in performance-driven livestock feed palatability enhancement.

Kerry Group Advances Clean-Label Umami Solutions in Animal Nutrition

Kerry Group leverages its human food flavor R&D infrastructure to deliver advanced taste modulation technologies to the animal feed additives market. Its portfolio includes high-nucleotide yeast extracts and fermented fish proteins that serve as natural umami enhancers, reducing reliance on synthetic monosodium glutamate in animal diets. In 2025, Kerry’s Taste and Nutrition segment generated more than €3 billion in sales, supported by rising demand for sustainable and plant-based feed flavorings across Europe and North America. The company is actively transitioning from synthetic sweeteners such as saccharin toward botanical-derived modifiers including stevia-based compounds, aligning with tightening regulatory frameworks. A key application focus is swine nutrition, particularly weaning piglets where masking bitter medicinal additives directly impacts feed intake and survival rates. Kerry’s clean-label strategy reinforces its competitive standing in natural feed palatability enhancers and flavor modifier technologies.

ADM Animal Nutrition Integrates Precision Feeding with Botanical Palatants

ADM Animal Nutrition benefits from extensive vertical integration across global oilseed processing and agricultural supply chains, providing cost control and raw material security for botanical-based feed palatants. Its portfolio includes organic sweeteners and botanical flavoring agents, recently expanded with palatants designed for ruminant digestion and organic dairy farming systems. The 2025 to 2026 Sales Enablement platform emphasizes demedication strategies, using palatability enhancers to maintain nutrient absorption in antibiotic-free livestock production. ADM shields itself from protein hydrolysate price volatility by leveraging internal oilseed processing capabilities for consistent input supply. A distinguishing capability lies in its Precision Feeding Platforms, which integrate digital intake monitoring systems that adjust flavor intensity in real time within poultry and swine production facilities. This data-driven feed optimization model positions ADM strongly in advanced feed palatability enhancers and smart livestock nutrition systems.

China: Hygiene Mandates and Regulatory Filtering Reshape Palatant Supply Chains

China’s feed palatability enhancers and modifiers market is entering a structurally stricter phase driven by regulatory enforcement and quality normalization. In August 2025, the Ministry of Agriculture and Rural Affairs introduced China’s first mandatory national hygienic standard dedicated to pet food. This regulation places explicit limits on microbial load and contaminant thresholds, compelling palatability enhancer producers to upgrade sterilization, filtration, and closed-loop blending systems. As a result, the market is tilting away from low-cost flavoring premixes toward traceable, high-purity palatants that can demonstrate batch-level compliance across pet and premium livestock feed applications.

Capacity expansion aligned with compliance is reinforcing this shift. Adisseo completed mechanical construction of its 37KT specialty blending facility in Nanjing in December 2024, with operational ramp-up extending through 2025. The site is positioned as a strategic hub for liquid and powder palatability enhancers designed for China’s integrated livestock and pet food systems. Parallel regulatory developments are tightening formulation boundaries. The China Feed Industry Association’s November 2025 standard discouraging calcitriol impurities in 25OHD3 has increased demand for palatability modifiers that remain chemically inert to sensitive vitamin systems. Further, the May 2025 rollout of a food and feed additive “positive list” with a circuit-breaker mechanism is actively removing non-compliant producers, consolidating demand around transparent, well-capitalized suppliers.

United States: Onshoring Momentum and Clean-Label Innovation Accelerate Adoption

The United States market is being reshaped by investment in traceable manufacturing and by shifts in trade policy that favor domestic sourcing. In April 2025, DSM-Firmenich inaugurated a state-of-the-art premix facility in the Kansas Animal Health Corridor. Designed around precision automation and containerized logistics, the site enhances biosecurity, traceability, and batch consistency for pet food palatants, aligning with rising retailer and regulatory scrutiny on ingredient provenance.

Trade measures are reinforcing this localization trend. Reciprocal tariffs implemented in April 2025 on specialty acids and flavor precursors imported from the EU and India have increased input cost volatility, prompting U.S. producers to accelerate domestic synthesis of feed sweeteners and acidifiers. On the innovation front, Nestlé Purina introduced botanical-based flavoring systems in late 2024 that leverage natural aromatic compounds to stimulate voluntary intake while supporting gut microbiome health. These solutions are gaining traction across both pet and ruminant feeds. The demand signal is amplified by growth in organic dairy. According to USDA organic surveys, a 4.3% rise in organic milk output has driven a 12% increase in adoption of clean-label botanical palatability enhancers in ruminant nutrition.

Brazil: Volume Expansion Meets Premiumization in Pet and Aquaculture Feeds

Brazil’s feed palatability enhancers market is benefiting from simultaneous growth in volume-intensive livestock feed and premium pet nutrition. The country has consolidated its position as the world’s third-largest pet market, with sector value projected to reach R$77 billion in 2025. This scale is catalyzing consolidation among palatant and flavor suppliers as global players seek exposure to Brazil’s fast-growing premium pet food segment, where meat-based attractants and functional flavor systems command higher margins.

At the same time, industrial feed output continues to expand. Sindirações projects total feed, concentrate, and supplement production to reach 94 million tonnes in 2025, up about 3% year on year. This volume growth underpins strong demand for bulk liquid palatants in broiler and swine diets. Brazil’s export-oriented aquaculture sector adds another demand layer. Record corn and soybean harvests in the 2024–2025 season have enabled feed producers to incorporate specialized fish and shrimp attractants to enhance feed intake efficiency and maintain competitiveness in global seafood markets.

European Union: Authorization Simplification and Technology-Led Differentiation

The European Union is advancing a more innovation-friendly yet tightly controlled framework for feed palatability enhancers. In December 2025, the European Commission proposed a Feed Safety Simplification Package aimed at accelerating additive approvals through digital labeling and streamlined authorization pathways. This reform is particularly beneficial for fermentation-derived palatants and next-generation flavor systems, reducing time to market while maintaining high safety thresholds.

Regulatory openness to natural solutions is expanding the palette of legal options. In July 2025, the Commission issued implementing regulations authorizing peppermint, clary sage, and Spanish sage essential oils for use across all animal species. These approvals significantly broaden opportunities for botanical palatability modifiers in both pet and livestock feeds. Concurrently, EU manufacturers are investing in precision nutrition technologies such as microencapsulation and controlled-release matrices. These systems protect volatile aromatic esters during high-temperature pelleting and ensure targeted flavor release upon ingestion, improving efficacy while reducing dosage requirements.

Strategic Snapshot: Feed Palatability Enhancers and Modifiers by Region (2025–2026)

Feed Palatability Enhancers And Modifiers Market County Level Snapshot

|

Region

|

Primary Policy or Market Driver

|

Technology Focus

|

Strategic Outcome

|

|

China

|

Mandatory hygiene standards and positive list enforcement

|

Sterilization, high-purity blending

|

Supplier consolidation and quality-led growth

|

|

United States

|

Onshoring and clean-label demand

|

Automated premix, botanical flavors

|

Higher traceability and domestic sourcing

|

|

Brazil

|

Pet market premiumization and feed volume growth

|

Meat-based attractants, liquid palatants

|

Dual-track growth in pet and livestock feeds

|

|

European Union

|

Authorization simplification and botanical approvals

|

Microencapsulation, controlled release

|

Faster innovation with regulatory certainty

|

Feed Palatability Enhancers And Modifiers Market Report Scope

Feed Palatability Enhancers And Modifiers Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4 Billion

|

|

Market Size (2034)

|

$6.4 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Type (Flavors, Sweeteners, Acidifiers, Texturizers, Umami Modifiers), By Form (Powder, Liquid, Pellets), By Animal Species (Poultry, Swine, Ruminants, Aquaculture, Companion Animals), By Function (Appetite Stimulation, Off-Note Masking, Feed Intake Stabilization, Stress Mitigation)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Kemin Industries, Inc., Adisseo, Kerry Group plc, DSM-Firmenich, Alltech, Inc., Associated British Foods plc, Cargill, Incorporated, Symrise AG, Diana Pet Food, Lucta S.A., Nutreco N.V., Palital Feed Additives B.V., Elanco Animal Health, Phytosynthese, Tanke International Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Feed Palatability Enhancers and Modifiers Market Segmentation

By Type

- Flavors

- Sweeteners

- Acidifiers

- Texturizers

- Umami Modifiers

By Form

By Animal Species

- Poultry

- Swine

- Ruminants

- Aquaculture

- Companion Animals

By Function

- Appetite Stimulation

- Off-Note Masking

- Feed Intake Stabilization

- Stress Mitigation

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Feed Palatability Enhancers and Modifiers Industry

- Kemin Industries, Inc.

- Adisseo

- Kerry Group plc

- DSM-Firmenich

- Alltech, Inc.

- Associated British Foods plc

- Cargill, Incorporated

- Symrise AG

- Diana Pet Food

- Lucta S.A.

- Nutreco N.V.

- Palital Feed Additives B.V.

- Elanco Animal Health

- Phytosynthese

- Tanke International Group

*- List not Exhaustive