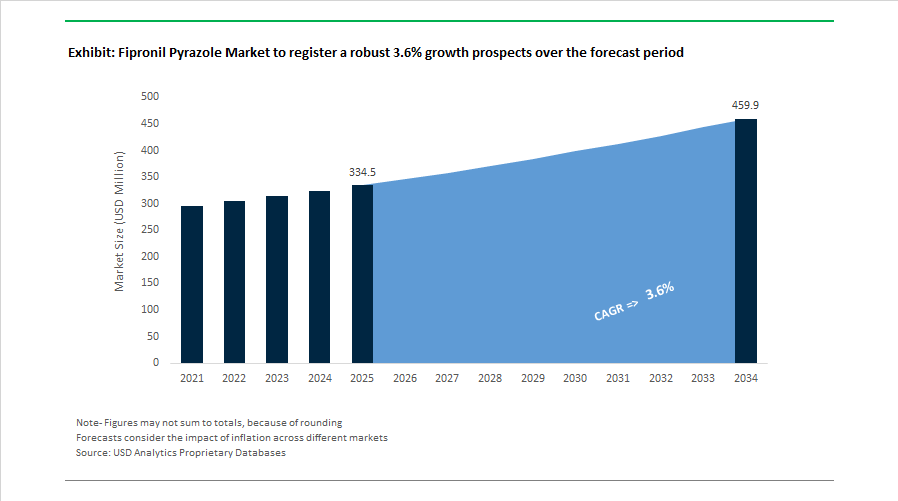

Fipronil Pyrazole Market Size 2025–2034: $334.5 Million to $459.9 Million at 3.6% CAGR Amid Regulatory Tightening and Export Realignment

The Fipronil Pyrazole Market is projected to expand from $334.5 Million in 2025 to $459.9 Million by 2034, registering a CAGR of 3.6%. Market performance reflects a complex interplay between tightening residue regulations in developed economies and sustained demand in emerging agricultural and veterinary applications. Fipronil, a broad-spectrum phenylpyrazole insecticide, remains critical in rice, sugarcane, corn, soybean, and plantation crop protection, as well as in companion animal flea and tick control. However, regulatory realignment, trade policy scrutiny, and resistance management strategies are reshaping production geographies and formulation innovation.

In early 2026, ag-tech platforms such as Farmonaut introduced AI-driven digital traceability tools enabling exporters to document Fipronil application intervals and residue compliance, particularly for shipments destined for the European Union and North America. The same year, BASF’s production facility in France faced renewed scrutiny over continued export manufacturing of Fipronil for markets such as Brazil and Indonesia despite the substance being banned for domestic EU agricultural use. The debate intensified around residue tolerance asymmetries, especially after the European Commission’s Regulation (EU) 2024/347, enacted in January 2024, tightened Maximum Residue Limits to 0.005 mg/kg for products including milk, honey, and select fruits, effectively restricting imports exceeding near-zero detection thresholds.

Supply chain normalization in late 2025 marked a structural shift after prolonged volatility. BASF and other precursor manufacturers lifted Force Majeure declarations on key pyrazole intermediates, stabilizing technical-grade Fipronil pricing after two years of elevated input costs. Throughout 2025, multinational agrochemical leaders including Bayer and Syngenta pivoted toward Fipronil-based seed treatment formulations, targeting precision delivery for corn and rice stem borer protection in Southeast Asia and Latin America. In March 2025, Albaugh Brazil launched Sultan®, based on etiprole, providing soybean growers with a phenylpyrazole alternative in regions facing resistance pressure and regulatory scrutiny. During 2024 and 2025, GSP Crop Science expanded its pyrazole blend R&D following favorable patent litigation outcomes, intensifying competition in India’s combo-insecticide segment.

In January 2024, India’s Registration Committee approved Gharda Chemicals for indigenous manufacture of a Fipronil 15% plus Chlorantraniliprole 5% suspension concentrate, targeting rice and sugarcane pest complexes through dual-mode action. Across 2024 and 2025, China’s Ministry of Agriculture and Rural Affairs authorized new export-only technical registrations under Policy No. 269, enabling production of Fipronil for high-demand markets such as Brazil, Indonesia, and Australia despite domestic restrictions. Parallel to agricultural shifts, the veterinary segment strengthened in 2023 and 2024 as companies including Boehringer Ingelheim expanded Fipronil-based spot-on flea and tick treatments, supported by rising urban pet ownership and premium pet care expenditure in Asia-Pacific and Latin America.

Trends and Opportunities in the Fipronil Pyrazole Market

Geographic Market Divergence and Regulatory Fragmentation

A pronounced bifurcation has emerged between prohibitionist markets and productivity-focused agricultural regions, fundamentally reshaping global demand flows for fipronil pyrazole. The European Union and the United Kingdom have reinforced bans on agricultural fipronil use due to pollinator toxicity concerns. In contrast, South America and Asia-Pacific continue to rely on fipronil as a critical insecticide under more controlled and technology-driven application frameworks.

In South America, fipronil remains deeply embedded in large-scale crop protection systems. As of September 2025, Brazil continues to treat an estimated 1.1 billion hectares annually with insecticide programs where fipronil plays a role, particularly in seed treatment and soil application. While Bill No. 4592/23 proposed restrictions on foliar spraying, enforcement agencies such as Ibama and state regulators have focused on tightening stewardship rather than eliminating usage. Recent penalties related to the improper distribution of Fipronil Nortox without agronomic prescriptions illustrate a shift toward compliance-driven optimization rather than outright prohibition.

Asia-Pacific has emerged as the dominant consumption hub, accounting for nearly 49.4% of global fipronil pyrazole demand in mid-2025, with market value estimated at approximately USD 142.2 million. This dominance is driven by staple crop protection in rice and cereals across India and China, where fipronil remains one of the few molecules capable of effectively controlling brown planthopper infestations at scale. In these markets, food security imperatives outweigh regulatory pressure, reinforcing fipronil’s role within integrated pest management systems.

A parallel export-driven dynamic has also intensified. Investigative findings from 2024–2025 show that EU member states approved exports of nearly 122,000 tonnes of banned pesticides, including fipronil-related products, to low- and middle-income countries, representing a 50% increase since 2018. This underscores a structural paradox where production capacity is retained in banned regions primarily to serve external markets, sustaining global supply even as domestic use declines.

Strategic Consolidation Toward High-Value Animal Health and Public Health Sectors

To offset regulatory volatility in agriculture, manufacturers are deliberately rebalancing portfolios toward animal health and urban pest control, segments characterized by higher margins, longer product lifecycles, and more predictable regulatory pathways.

By late 2025, pet care has emerged as the fastest-growing end-use segment for fipronil pyrazole. Despite competition from newer isoxazoline-class molecules, fipronil remains the benchmark for cost-effective, broad-spectrum ectoparasite control. Veterinary spot-on treatments, sprays, and impregnated collars continue to see strong uptake in emerging and mid-income markets, where affordability and proven efficacy are decisive purchasing criteria. Importantly, these formulations exhibit lower environmental dispersion compared to agricultural sprays, aligning better with evolving regulatory expectations.

Urban and structural pest control represents the largest application segment, accounting for approximately 58.4% of global fipronil pyrazole usage. Termite and ant control in residential and commercial buildings remains a core demand pillar, particularly in North America, which held a dominant 49.3% revenue share in 2024. Rapid urban expansion, aging building stock, and increased reliance on professional pest management services are sustaining demand in this segment.

At the same time, portfolio diversification is underway. In March 2025, Albaugh Brazil launched Sultan®, an etiprole-based insecticide positioned as a residue-compliant, high-value alternative for soybean cultivation. Such moves signal a broader industry strategy to hedge fipronil exposure by commercializing adjacent pyrazole chemistries that retain efficacy while offering improved regulatory acceptance.

R&D into Eco-Selective Pyrazole Derivatives and Novel Modes of Action

Restrictions on fipronil have created a significant innovation gap, accelerating research into eco-selective pyrazole derivatives with enhanced target specificity and reduced non-target toxicity. The opportunity lies not in extending legacy molecules but in redefining the pyrazole class itself.

Research published in the Journal of Agricultural and Food Chemistry in November 2025 introduced 4-sulfur-substituted pyrazol-5-yl-benzamide derivatives that achieved 93.4% protective efficacy against Valsa mali in apple orchards. These compounds outperformed established fungicides such as fluxapyroxad while demonstrating no observable toxicity to Apis mellifera. Such performance profiles directly address the pollinator safety concerns that underpin fipronil bans.

Further innovation is emerging through entirely new modes of action. In September 2025, ACS Publications highlighted pyrazole-based Transketolase inhibitors that disrupt plant carbon metabolism rather than neural pathways. With IC50 values as low as 0.47 mg/L, these candidates match the potency of leading synthetic herbicides while offering faster environmental degradation, positioning them as potential “green chemistry” successors within the pyrazole family.

Global regulatory recognition is reinforcing this opportunity. In November 2025, the ISO provisionally approved the common name “dimpyrargyl” for a new pyrazolecarboxamide insecticide developed by Qingdao KingAgroot. ISO naming is a critical milestone, signaling readiness for international commercialization and validating market appetite for safer, next-generation pyrazole molecules.

Formulation Innovation Through Microencapsulation and Controlled-Release Systems

Formulation technology represents a near-term growth lever for both legacy fipronil and next-generation pyrazole actives. The focus is shifting toward delivery systems that reduce active ingredient loading while maximizing field efficacy and environmental containment.

Seed treatment applications illustrate this trend clearly. By 2024, seed-applied insecticides accounted for approximately 18% of all agricultural insecticide sales, with fipronil-based formulations playing a central role. Compared with broadcast spraying, seed coatings deliver precise, localized protection using significantly lower active ingredient volumes per hectare, aligning with integrated pest management and sustainability objectives.

Patent activity underscores momentum in this area. Between 2024 and 2025, patent filings related to microencapsulated and controlled-release fipronil formulations increased by around 10%. These technologies are designed to shield the active ingredient from rapid photolysis and soil degradation, extending residual activity while reducing runoff and leaching into aquatic systems.

Veterinary applications are also benefiting from formulation advances. In 2025, the European Medicines Agency proposed stricter environmental risk assessment requirements for pet parasiticides, intensifying demand for low-shedding delivery systems. Controlled-release formulations that sequester fipronil within hair follicles and sebaceous glands are gaining traction, as they minimize wash-off during grooming and bathing while maintaining prolonged ectoparasite control.

Fipronil Pyrazole Market Share and Segmentation Insights

Liquid Formulations Dominate Fipronil Pyrazole Market Due to Application Flexibility and Advanced Suspension Concentrate Technologies

Liquid formulations accounted for 48.20% of the Fipronil Pyrazole Market share in 2025, making them the most widely used product form across global crop protection applications. Liquid fipronil products are preferred because they provide maximum versatility for agricultural deployment, including foliar spraying, soil drenching, seed treatment applications, and integrated pest management programs across a wide range of crops. Their compatibility with modern agricultural spraying equipment and tank-mixing practices enables farmers to combine fipronil with other insecticides, fungicides, and micronutrient formulations, improving operational efficiency during crop protection cycles. In 2025, the market has witnessed significant advancements in suspension concentrate (SC) formulation technologies, replacing older emulsifiable concentrate (EC) products that relied heavily on organic solvents. These next-generation SC formulations feature optimized particle size distribution, enhanced suspension stability, and improved adhesion on plant surfaces, allowing more uniform leaf coverage and greater insecticidal performance. Additionally, reduced solvent content helps manufacturers comply with tightening environmental and safety regulations in major agricultural markets, while simultaneously improving formulation safety and storage stability. These technological improvements reinforce the dominance of liquid formulations in the global fipronil pyrazole insecticide market.

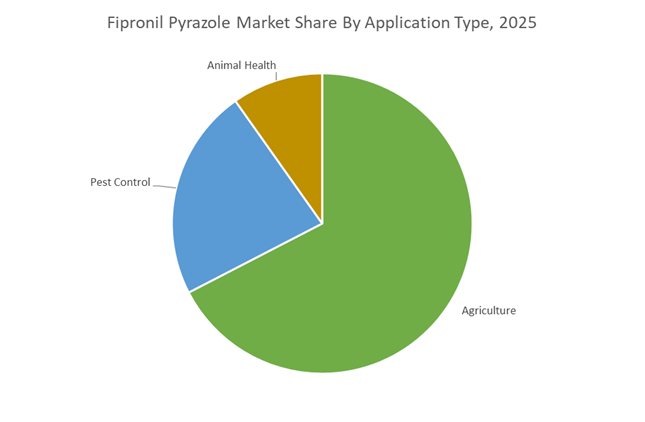

Agricultural Crop Protection Drives the Majority of Global Fipronil Pyrazole Demand

Agriculture represented 67.40% of the Fipronil Pyrazole Market share in 2025, reflecting the compound’s strong effectiveness as a broad-spectrum phenylpyrazole insecticide used in crop protection programs worldwide. Fipronil plays a crucial role in controlling soil-dwelling and foliar insect pests, making it particularly valuable in high-value crop production systems such as rice, corn, sugarcane, and vegetable cultivation. In rice farming, fipronil is widely used to control stem borers, leafhoppers, and planthoppers, pests that can significantly reduce crop yields if left unmanaged. Similarly, in corn production it helps manage rootworms and soil insect infestations, while vegetable growers rely on fipronil for protection against multiple chewing and sucking insects. The global market landscape in 2025 is shaped by regulatory divergence across agricultural regions. The European Union has imposed restrictions on fipronil use in agriculture due to concerns about pollinator safety, particularly impacts on bee populations. However, many Asian and Latin American agricultural markets continue to rely heavily on fipronil-based insecticides, particularly in rice and sugarcane production where pest pressure remains high. In these regions, modern integrated pest management (IPM) strategies emphasize controlled and targeted application methods to maintain insect control efficacy while reducing environmental exposure.

Competitive Landscape in Fipronil Pyrazole Market

BASF SE Maintains Global Leadership Through Advanced Fipronil Formulations

BASF SE remains the dominant player in the global fipronil insecticide market, supported by flagship brands such as Regent® and Termidor®. The company strengthened its competitive position during 2024 and 2025 with the launch of microencapsulated fipronil formulations that improved residual pest control performance by 18%, particularly in structural termite management and large-scale row crops. BASF allocates more than 10% of annual revenue to research and development, emphasizing Blue Chemistry principles aimed at reducing toxicity to non-target organisms including pollinators. In early 2026, BASF expanded its Axalion insecticide platform to complement its phenylpyrazole portfolio and mitigate resistance development in high-pressure pest environments. The company maintains strong penetration in maize, rice, and cotton applications, while also holding premium positioning in structural pest control and termiticides. Its advanced delivery technologies and regulatory alignment reinforce leadership in high-purity fipronil formulations.

Gharda Chemicals Strengthens Cost-Competitive Technical Fipronil Production

Gharda Chemicals Ltd. is a major global supplier of technical-grade fipronil, particularly within the 93% to 95% purity segment that commands roughly 68% of global market demand. The company produces fipronil technical with minimum 95% purity alongside branded formulations such as Zolt, Yamakazi, and X Factor, with specialization in suspension concentrate formats. Gharda exports to more than 50 countries, leveraging a fully integrated production chain in India to maintain cost competitiveness across emerging markets. Recent innovation includes synergistic dual-chemistry formulations combining fipronil with complementary active ingredients to inhibit pest feeding behavior immediately upon contact, particularly targeting Diamondback moth infestations. Expansion of its Blue Chemistry initiative aligns product safety profiles with European standards for vegetable crops. This integrated manufacturing and formulation capability positions Gharda as a critical supplier in both agricultural insecticides and export-driven markets.

Bayer CropScience Focuses on Seed Treatment and Veterinary Applications

Bayer CropScience maintains strong positioning in premium fipronil applications, particularly in seed treatment technologies and veterinary pest control products. The company is shifting application emphasis from foliar spraying toward seed coating, significantly reducing active ingredient volumes per hectare while maintaining pest protection efficacy. In 2025, Bayer collaborated with drone technology manufacturers to optimize aerial precision dosing, lowering runoff risk and labor intensity in large-scale farming operations. The company dominates the pet care segment with flea and tick treatments while maintaining strong presence in corn and sunflower seed treatments. Strategic partnerships in Brazil and India aim to address localized pest challenges such as Brown Planthopper infestations through tailored fipronil-based integrated pest management programs. Bayer’s precision agriculture strategy strengthens its competitive edge in sustainable pesticide deployment.

Tagros Chemicals Expands High-Purity Fipronil Capacity in Asia-Pacific

Tagros Chemicals has emerged as a fast-growing manufacturer in the phenylpyrazole insecticide segment, supplying fipronil technical with minimum 97% purity for premium agricultural and veterinary applications. The company increased production capacity in South India in 2025 to serve rising demand from Asia-Pacific, which accounts for nearly 59% of global fipronil pyrazole consumption. Tagros differentiates through development of low-VOC liquid carriers that enable uniform active ingredient dispersion in broad-acre crop protection. Its expertise in substitution and condensation reactions required for synthesizing complex pyrazole frameworks enhances technical manufacturing reliability. By focusing on high-purity active ingredients and advanced formulation chemistry, Tagros strengthens its supply position in regulated and high-value crop protection markets.

Jiangsu Changqing Agrochemical Drives High-Volume Global Supply

Jiangsu Changqing Agrochemical Co. operates within China, the world’s largest fipronil producer with annual output near 5,800 metric tons. The company manufactures technical fipronil alongside broad-spectrum insecticides such as thiamethoxam and lambda-cyhalothrin, supporting diversified export portfolios. In its 2025 filings, Changqing reported net revenue of approximately 3.8 billion RMB, reflecting strong demand from Southeast Asia and Russia. The company invests heavily in smart manufacturing systems, deploying automated and closed-loop synthesis lines to comply with increasingly stringent Chinese environmental and safety regulations. Its high-capacity infrastructure supports leadership in liquid formulations, which account for roughly 48% of global fipronil pyrazole market revenue. Through scale, export orientation, and regulatory alignment, Jiangsu Changqing remains a critical supplier in the global agrochemical value chain.

India: Export-Led Manufacturing Discipline and Safety-Centric Scale-Up

India’s Fipronil pyrazole ecosystem in 2025–2026 is being shaped by export-driven growth combined with heightened safety, environmental, and compliance benchmarks. A central pillar is Gharda Chemicals, the originator of indigenous Fipronil production. In January 2025, the company announced a major technological upgrade at its Lote, Maharashtra facility to scale high-purity pyrazole intermediates aligned with regulated global markets. This site, recognized with the FICCI Outstanding Contribution to Society Award 2024, is integrating Zero Harm safety protocols to meet the tightening audit expectations of North American, Latin American, and EU buyers ahead of the 2026 export cycle. Parallel recognition came in January 2025 when Gharda’s Dombivli unit received the Prashansa Patra from the National Safety Council of India, reinforcing India’s positioning as a reliable source of compliance-ready pyrazole chemistry.

Downstream excellence is equally visible. Gujarat Insecticides Limited, a Gharda subsidiary, received the Fame National Award 2024 Platinum Category for environmental excellence, highlighting its transition toward waste-to-wealth recovery systems in pyrazole insecticide synthesis. From a trade perspective, Ministry of Commerce data released in December 2025 shows Indian agrochemical exports, including Fipronil derivatives, reaching a record first-half high for FY 2025–26. This momentum is supported by a 6.46% expansion in the Drugs and Pharmaceuticals sector, which increasingly leverages pyrazole-ring chemistry for advanced veterinary formulations. Collectively, these developments underscore India’s evolution from cost-competitive producer to a high-standard export platform for regulated Fipronil pyrazole products.

China: Export-Only Reform and Carbon-Aware Formulation Mandates

China’s Fipronil pyrazole market is undergoing a structural reset driven by export-only registration reform, residue compliance tightening, and low-carbon manufacturing mandates. In November 2025, the Ministry of Agriculture and Rural Affairs released a draft framework streamlining export-only pesticide registration. This reform allows Chinese manufacturers to produce new pyrazole molecules not approved for domestic use, explicitly targeting South American and Southeast Asian markets where demand for cost-effective insecticide actives remains strong. This policy significantly improves time-to-market for export-focused Fipronil derivatives while decoupling domestic food safety sensitivities from overseas growth strategies.

Regulatory scrutiny is simultaneously intensifying. On December 9, 2025, China notified the WTO of 209 new Maximum Residue Limits for 93 pesticides, including stricter monitoring of pyrazole residues across multiple food categories. This aligns Chinese exports more closely with global food safety benchmarks. On the formulation side, BASF commissioned a new high-performance dispersants line in Nanjing in November 2025. These dispersants are critical for suspension concentrate Fipronil formulations, improving stability and biological efficacy in liquid delivery systems. Looking ahead, the MIIT 2026 Work Plan mandates the adoption of Controlled Free Radical Polymerization technology to reduce the product carbon footprint of insecticide formulations, forcing pyrazole producers to integrate sustainability metrics directly into formulation design.

Brazil: Resistance Management and Seed-Treatment Pull

Brazil’s Fipronil pyrazole dynamics are closely tied to resistance management in row crops and the scale of its soybean economy. In March 2025, Albaugh launched Sultan®, an Etiprole-based insecticide, for Brazilian soybean growers. As a pyrazole-class analog of Fipronil, the product is positioned to address resistance challenges while maintaining efficacy against key pests. This launch highlights Brazil’s openness to differentiated pyrazole chemistry as part of integrated pest management strategies rather than reliance on a single active.

Feedstock availability is reinforcing demand visibility. Record soy and corn harvests in the 2024–2025 season have increased the use of seed-treatment Fipronil ahead of the 2026 planting cycle. To secure volumes, Brazilian formulators have entered new supply agreements with Indian and Chinese technical-grade manufacturers. This reinforces Brazil’s role as a demand anchor market that shapes export production planning across Asia, particularly for high-volume, cost-sensitive Fipronil pyrazole actives.

Australia: Environmental Scrutiny and Veterinary Reassessment

Australia represents a regulatory bellwether market where environmental risk assessment is increasingly influencing Fipronil usage patterns. The Australian Pesticides and Veterinary Medicines Authority is in the assessment phase of a comprehensive Fipronil review spanning 2025–2026, with a proposed decision for veterinary products expected in March 2026. Outcomes from this review could materially alter application practices in livestock and companion animal segments, especially for spot-on treatments.

Environmental protection is an additional pressure point. In October 2025, Australia and New Zealand jointly released draft default guideline values for Fipronil in marine water to mitigate ecological risks from urban and agricultural runoff. These guidelines elevate the compliance threshold for pyrazole residues, signaling that future market access will depend not only on efficacy but also on demonstrable environmental stewardship across the product lifecycle.

United States: Environmental Persistence and Financial Enablement

In the United States, Fipronil pyrazole developments are increasingly shaped by environmental persistence concerns and commercial facilitation mechanisms. During 2025, U.S. regulators began aligning with EMA concept papers following studies on Fipronil persistence in wastewater. This has led to the integration of Fipronil-based flea and tick treatments into veterinary watch lists, prompting reassessment of usage patterns to reduce secondary environmental exposure while preserving animal health outcomes.

On the commercial front, BASF Agricultural Solutions introduced the Grower Finance Program in December 2025, offering 0 percent APR financing on seed treatments that include high-performance Fipronil coatings. This initiative improves planning certainty for growers ahead of the 2026 season and underscores how financial instruments are being deployed alongside chemistry innovation to sustain adoption in a more regulated environment.

Strategic Snapshot: Fipronil Pyrazole Market by Country (2025–2026)

Fipronil Pyrazole Market County Level Snapshot

|

Country

|

Primary Policy or Market Driver

|

Strategic Focus Area

|

Competitive Implication

|

|

India

|

Export growth and safety recognition

|

High-purity pyrazole intermediates

|

Trusted supplier for regulated markets

|

|

China

|

Export-only reform and PCF reduction

|

Low-carbon formulations and SC stability

|

Faster export launches with compliance

|

|

Brazil

|

Pest resistance and seed treatment demand

|

Pyrazole analog diversification

|

Volume pull shaping global supply

|

|

Australia

|

Environmental and veterinary review

|

Marine toxicity and usage controls

|

Higher compliance barriers

|

|

United States

|

Environmental persistence scrutiny

|

Financing-enabled adoption

|

Balanced regulation and grower support

|

Fipronil Pyrazole Market Report Scope

Fipronil Pyrazole Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$334.5 Million

|

|

Market Size (2034)

|

$459.9 Million

|

|

Market Growth Rate

|

3.6%

|

|

Segments

|

By Form (Liquid, Gel, Granular, Powder), By Application Type (Agriculture, Animal Health, Pest Control), By Crop Type (Rice, Corn, Cotton, Soybeans, Fruits and Vegetables), By Synthesis Route (Technical Grade, Formulated Grade), By Sales Channel (Direct B2B, Retail and Veterinary)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Gharda Chemicals Limited, Bayer AG, Syngenta AG, Tagros Chemicals India Private Limited, GSP Crop Science Private Limited, HPM Chemicals & Fertilizers Limited, Jiangsu Tuoqiu Agrochemical Co., Ltd., Zhejiang Yongnong Bio-Sciences, Albaugh, LLC, Bharat Group, Rotam CropSciences, Nanjing Red Sun Co., Ltd., UPL Limited, Meghmani Organics Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fipronil Pyrazole Market Segmentation

By Form

- Liquid

- Gel

- Granular

- Powder

By Application Type

- Agriculture

- Animal Health

- Pest Control

By Crop Type

- Rice

- Corn

- Cotton

- Soybeans

- Fruits and Vegetables

By Synthesis Route

- Technical Grade

- Formulated Grade

By Sales Channel

- Direct B2B

- Retail and Veterinary

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Fipronil Pyrazole Industry

- BASF SE

- Gharda Chemicals Limited

- Bayer AG

- Syngenta AG

- Tagros Chemicals India Private Limited

- GSP Crop Science Private Limited

- HPM Chemicals & Fertilizers Limited

- Jiangsu Tuoqiu Agrochemical Co., Ltd.

- Zhejiang Yongnong Bio-Sciences

- Albaugh, LLC

- Bharat Group

- Rotam CropSciences

- Nanjing Red Sun Co., Ltd.

- UPL Limited

- Meghmani Organics Limited

*- List not Exhaustive