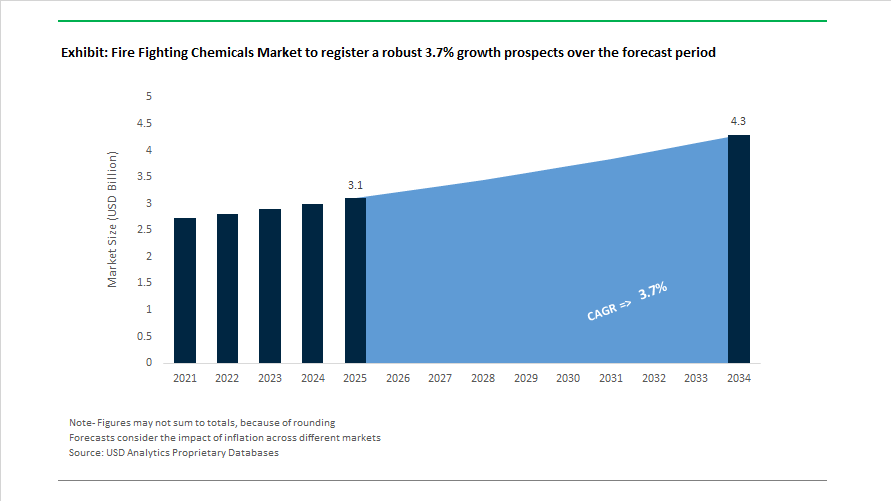

Fire Fighting Chemicals Market Size 2025–2034: $3.1 Billion to $4.3 Billion at 3.7% CAGR Driven by PFAS Phase-Out and Halon Replacement Mandates

The Fire Fighting Chemicals Market is projected to grow from $3.1 billion in 2025 to $4.3 billion by 2034, registering a CAGR of 3.7%. Market expansion is being shaped by regulatory elimination of fluorinated compounds, halon phase-outs in aviation, and structural investment in wildland and industrial fire suppression infrastructure. Firefighting chemical demand spans fluorine-free foam concentrates (F3), dry chemical powders, clean agent suppressants, retardants for aerial firefighting, and specialty stabilizers. Regulatory mandates across maritime, aviation, and municipal fire services are accelerating reformulation cycles and capital expenditure in compliant suppression chemistries.

In January 2026, amendments to the SOLAS Convention and High-Speed Craft Codes entered into force globally, prohibiting the use or storage of firefighting media containing PFOS on ships. Vessel operators are now required to provide manufacturer declarations or laboratory verification confirming PFOS-free foam systems. The maritime enforcement follows the September 2024 update to EU REACH targeting PFHxA and related C6 fluorochemicals, mandating that public fire services phase out C6 foams by April 10, 2026 unless full containment measures are implemented. These regulatory actions are driving rapid conversion to fluorine-free foam concentrates across Europe and international shipping fleets. In January 2026, Perimeter Solutions completed the acquisition of MMT, expanding its fire suppression portfolio and strengthening its position in wildland and industrial chemical retardants.

During 2025, aviation and federal wildfire mandates intensified chemical substitution cycles. The European Union Aviation Safety Agency set a December 31, 2025 deadline requiring EU-registered aircraft to replace Halon 1211 extinguishers, triggering strong procurement of halon-free alternatives such as 2-BTP-based clean agents with near-zero ozone depletion potential. In September 2025, the USDA signed a five-year master agreement with Perimeter Solutions mandating full conversion to domestically manufactured powder retardants for federal aerial firefighting. In November 2025, Amerex achieved FM 5970 compliance for its vehicle fire suppression systems, enhancing dry chemical distribution performance for heavy-duty mining and forestry equipment. In April 2025, Johnson Controls launched specialized chemical suppression packages for non-acute healthcare and correctional facilities, emphasizing low-toxicity and rapid-response systems.

Earlier structural developments in 2024 reinforced the transition toward sustainable foam chemistry and integrated fire safety infrastructure. In March 2024, Honeywell entered a strategic partnership with the Adani Group to deploy advanced fire suppression chemicals across airports, data centers, and refinery assets in India. Throughout 2024, Wacker Chemie expanded silicone-based antifoam emulsion capacity, supporting the production stability of high-performance firefighting foam concentrates. The January 2024 formation of Novonesis following the merger of Novozymes and Chr. Hansen initiated collaboration with foam manufacturers to develop bio-based and enzymatic stabilizers aimed at improving fluorine-free foam shelf life and drain time performance, aligning with global PFAS reduction strategies.

Fire Fighting Chemicals Market Share and Segmentation Insights

Dry Chemical Fire Suppression Agents Lead Global Fire Protection Systems Due to Versatility and Cost Efficiency

Dry Chemicals accounted for 32.80% of the Fire Fighting Chemicals Market share in 2025, making them the most widely deployed fire suppression chemical category globally. These chemicals—primarily monoammonium phosphate and sodium bicarbonate formulations—are extensively used in portable fire extinguishers and fixed fire suppression systems designed to combat Class A (combustible solids), Class B (flammable liquids), and Class C (electrical) fires. Their strong adoption is largely due to their broad fire suppression capability, rapid flame knockdown, long shelf life, and relatively low production cost, which makes them suitable for large-scale deployment across residential, commercial, and industrial facilities. Additionally, the massive installed base of portable multipurpose fire extinguishers worldwide continues to drive steady demand for dry chemical refill materials and system maintenance chemicals. In 2025, however, the fire protection industry is experiencing growing transition pressure toward environmentally safer “clean agent” fire suppression systems, particularly in sensitive facilities such as data centers, telecommunications infrastructure, museums, and archival facilities, where residue-free suppression is essential. Despite this shift, dry chemical agents maintain market leadership due to their cost efficiency, proven reliability, and broad compatibility with general-purpose fire safety equipment.

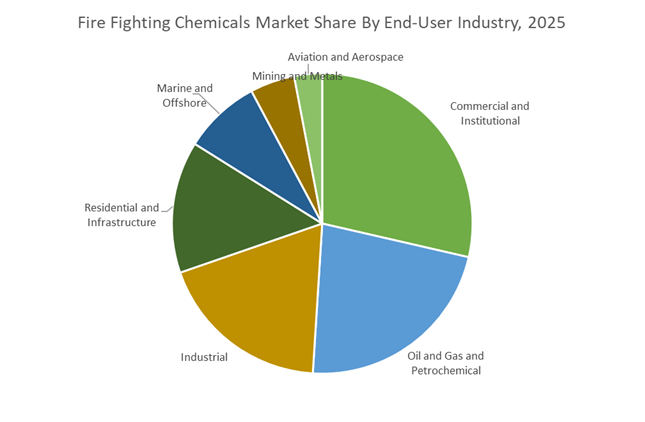

Commercial and Institutional Buildings Drive Largest Demand for Fire Suppression Chemicals

Commercial and Institutional facilities represented 28.60% of the Fire Fighting Chemicals Market share in 2025, reflecting the extensive fire protection requirements across office buildings, hospitals, educational institutions, hotels, retail complexes, and public infrastructure. These facilities are subject to strict building safety codes, fire protection regulations, and insurance compliance requirements, mandating the installation and regular maintenance of portable fire extinguishers, fire suppression systems, and chemical fire control equipment. The high density of occupied buildings within urban environments generates continuous demand for initial chemical system filling, periodic extinguisher refilling, and suppression system upgrades, making the commercial sector a stable and recurring revenue base for fire protection chemical manufacturers. In 2025, the sector has experienced adjustments driven by post-pandemic building occupancy shifts, as organizations reassess facility utilization and safety infrastructure requirements. Many facility managers have conducted comprehensive fire risk assessments based on revised occupancy patterns, resulting in targeted upgrades of fire suppression systems in high-traffic spaces such as healthcare facilities, hospitality environments, and educational campuses. At the same time, some buildings have optimized the number and placement of fire extinguishers to better align with current safety codes and operational layouts, reinforcing the commercial and institutional sector’s central role in driving global fire fighting chemicals demand.

Competitive Landscape in Fire Fighting Chemicals Market

Perimeter Solutions Leads Global Wildfire Retardant and Fluorine Free Foam Innovation

Perimeter Solutions maintains clear dominance in wildfire retardants through its PHOS-CHEK® portfolio, which includes long term retardants, Class A and Class B foams, and specialized fire extinguisher additives. In 2025 and 2026, the company introduced SOLBERG SPARTAN™, a 1% fluorine free Class A and B foam concentrate engineered to address municipal, structural, and running gasoline fires, marking a major milestone in PFAS free fire suppression chemicals. The commissioning of a 110,000 square foot retardant manufacturing facility in Sacramento in 2025 strengthened North American supply chain resilience during peak wildfire seasons. A core differentiator is its Resilient Response logistics model, enabling rapid deployment of operational air tanker bases at small airports during emergency events. Through advanced retardant chemistry, scalable production capacity, and field deployable infrastructure, Perimeter Solutions remains the benchmark in wildfire chemical suppression technologies.

Johnson Controls Integrates Chemical Suppression with Smart Building Automation

Johnson Controls operates as a system level leader by combining chemical fire suppression agents with digital building automation platforms. Its portfolio includes established brands such as ANSUL and Tyco, alongside clean agent solutions like SAPPHIRE®, designed to protect mission critical facilities with zero residue gaseous suppression. The company’s Five Ss framework focuses on safety, space efficiency, discharge speed, lifecycle cost control, and sustainability, particularly in hyperscale data centers and semiconductor facilities. In early 2026, Johnson Controls expanded its OpenBlue platform to incorporate AI driven detection and localized chemical discharge, reducing suppressant waste by up to 30% in controlled environments. Its unified digital architecture links fire detection sensors directly with chemical actuators across large campuses, offering a foundational control layer unmatched by most competitors. This integration of fire fighting chemicals with intelligent building systems strengthens its competitive advantage in high value infrastructure protection.

Angus Fire Advances Biodegradable Aviation Firefighting Foam Solutions

Angus Fire has repositioned itself as a leader in fluorine free foam technology, particularly within the aviation rescue and firefighting segment. Its Respondol ATF and JetFoam product lines are recognized for biodegradable performance and high film forming efficiency without persistent halogens. In 2025, the company launched JetFoam ICAO-C, the first fully biodegradable fluorine free foam to achieve ICAO Level C certification for airport rescue and firefighting applications. At INTERSCHUTZ 2026, Angus Fire introduced its F3 Transition Service, offering structured consulting programs to assist oil and gas operators in safely flushing legacy PFAS based systems. By mid 2026, the company maintained one of the highest counts of GreenScreen Silver certified fluorine free formulations in the industry. Its technical depth in foam stabilization chemistry positions Angus Fire as a global authority in sustainable aviation and industrial fire suppression chemicals.

Amerex Corporation Strengthens Industrial and Lithium Ion Battery Fire Suppression

Amerex Corporation is a dominant player in portable and vehicle mounted fire suppression systems, particularly across mining, heavy construction, and transit sectors. The company is widely recognized for high capacity dry chemical extinguishers using monoammonium phosphate and specialized Class D agents tailored for lithium ion battery fire risks. In late 2025, Amerex introduced a new vehicle suppression system featuring a 20% higher thermal resistance agent designed for electric vehicle fleet warehouses and logistics hubs. Its strategy emphasizes digitalization of the cylinder through integration of smart pressure sensors that transmit real time readiness data to centralized dashboards. Ruggedized chemical canisters engineered for extreme environments reinforce its reputation across industrial applications. As electrification expands across transportation and warehousing, Amerex strengthens its position in high risk fire fighting chemical deployment.

Solvay Supplies Advanced Flame Retardant Chemistry to the Global Market

Solvay plays a strategic upstream role in the fire fighting chemicals market by supplying phosphorus based flame retardants and high purity intermediates used in fluorine free foam stabilizers and fire resistant polymers. In 2026, the company ramped up specialty polymer production to support rising demand for fire retardant bulkhead materials in aerospace and marine industries. Through a Circular Bio Economy initiative, Solvay increased sourcing of renewable feedstocks for industrial fire suppression powders, lowering lifecycle carbon intensity. As a foundational chemical supplier, Solvay provides the advanced surfactant and polymer chemistry required by downstream foam manufacturers seeking PFAS alternatives. Its integrated production network and focus on low emission chemical manufacturing enhance its relevance as regulatory scrutiny on halogenated fire retardants intensifies globally.

United States Fire Fighting Chemicals Market: $5B PFAS Cleanup Funding, EPA Superfund Rules, and Fluorine-Free Foam Transition

The United States Fire Fighting Chemicals Market is undergoing a structural shift as the industry moves away from legacy PFAS-based aqueous film-forming foams (AFFF) toward fluorine-free firefighting chemicals and environmentally compliant suppression agents. In Apr 2024, the U.S. Environmental Protection Agency designated PFOA and PFOS as hazardous substances under the Comprehensive Environmental Response Compensation and Liability Act, dramatically increasing liability and remediation costs for manufacturers and industrial users of PFAS-based firefighting chemicals. Parallel infrastructure reforms by the U.S. General Services Administration now require PFAS-free fire suppression chemicals in federal building safety contracts, accelerating nationwide adoption of fluorine-free firefighting foams.

Aviation safety policies are also reshaping the market. The Federal Aviation Administration issued updated guidance in 2024 enabling civilian airports to transition to Fluorine-Free Foam (F3) technologies following earlier defense-sector mandates. Technology innovation is advancing rapidly, with Honeywell and Carrier Global launching AI-driven fire detection and suppression systems in June 2024 that optimize chemical deployment in industrial HVAC environments. Additionally, the EPA’s 2024 National Primary Drinking Water Regulation established strict PFAS limits, prompting utilities to invest in advanced chemical filtration technologies. More than $5B allocated through the Bipartisan Infrastructure Law for contamination remediation is further driving R&D in chemical sequestration and destruction technologies, strengthening innovation across the U.S. firefighting chemicals industry.

Saudi Arabia Fire Fighting Chemicals Market: Vision 2030 Infrastructure Boom and $500M NEOM Fire Protection Demand

Saudi Arabia’s Fire Fighting Chemicals Market is expanding rapidly as the country invests heavily in large-scale urban infrastructure and industrial fire suppression systems under Vision 2030. Mega-projects such as NEOM and The Line are driving massive demand for advanced firefighting foams, dry chemical agents, and gaseous suppression technologies. Fire protection engineering investments for NEOM alone exceed $500M, creating significant opportunities for specialty firefighting chemical manufacturers and safety engineering firms.

Regulatory modernization is accelerating adoption of global fire safety standards. The Saudi Civil Defense partnered with international fire protection specialists to implement SBC 801 and SBC 802 codes across high-density industrial zones and oil and gas infrastructure. Investments in IoT-enabled fire monitoring systems are projected to surpass SAR 500M by 2027 as the Kingdom integrates smart suppression technologies into industrial facilities. In parallel, Saudi Aramco has deployed advanced dry chemical agents and specialized foams across offshore platforms and refineries. With more than 1,000 fire safety audits planned by 2026 and rapid urbanization underway, the Saudi government is also encouraging domestic manufacturing of firefighting foams to reduce import dependency and support local chemical supply chains.

Germany Fire Fighting Chemicals Market: Green Flame Retardants, €2B BASF R&D, and EU REACH Compliance Leadership

Germany represents Europe’s innovation hub for sustainable firefighting chemicals, flame retardants, and environmentally compliant suppression technologies. In late 2025, LANXESS introduced Levagard 2100, a next-generation reactive phosphonate flame retardant that chemically bonds with polymer matrices to reduce volatile organic compound emissions and enhance long-term fire resistance performance.

Germany’s leadership in sustainable chemical innovation is reinforced by significant R&D investment. BASF invested approximately €2B in research and development during 2024, with a substantial share dedicated to green transformation initiatives for fire safety polymers and eco-friendly suppression agents. In early 2025, BASF inaugurated the first commercial Loopamid facility focused on circular chemical recycling of materials used in fire-resistant textiles. German chemical manufacturers are also aligning with strict EU REACH restrictions on halogenated flame retardants, accelerating the shift toward phosphorus-based and polymeric brominated alternatives. Government funding for low-viscosity reactive phosphonates and fire-resistant construction materials further strengthens Germany’s leadership in advanced fire protection chemicals and sustainable building safety technologies.

China Fire Fighting Chemicals Market: Smart Chemical Parks, Indigenous Foam Production, and Industrial Safety Upgrades

China’s Fire Fighting Chemicals Market is expanding rapidly under the country’s 14th Five-Year Plan as industrial safety upgrades and urbanization drive demand for advanced suppression technologies. Government work reports for 2025 emphasize indigenous innovation in chemical manufacturing, including localization of high-performance fluorine-free synthetic firefighting foams. The National Development and Reform Commission launched an industrial modernization action plan in 2024 to upgrade safety equipment across municipal and chemical facilities.

China is also advancing smart manufacturing and sustainable chemical processing. In early 2025, BASF initiated commercial recycling operations in Shanghai, supporting the transition toward circular chemical production. With urbanization projected to reach 75% by 2035, the Ministry of Emergency Management introduced stricter fire safety codes for high-rise residential developments. The country’s Smart Chemical Park initiatives require real-time automated suppression systems in new industrial clusters, integrating AI and robotics to optimize chemical discharge timing during fire events. These developments position China as a major market for advanced fire suppression chemicals and intelligent firefighting systems.

Australia Fire Fighting Chemicals Market: Nationwide PFAS Ban, Ultra-Trace Detection Technology, and Eco-Friendly Foam Adoption

Australia has emerged as a global regulatory leader in the Fire Fighting Chemicals Market through comprehensive legislation banning persistent PFAS firefighting chemicals. Effective Jul 1, 2025, the Australian government prohibited the import, manufacture, and use of PFOS, PFOA, and PFHxS under the Industrial Chemicals Environmental Management Standard. These compounds are now classified as Schedule 7 substances, the highest hazard category, severely restricting their use outside controlled research environments.

Water safety regulations are reinforcing the transition toward eco-friendly firefighting chemicals. New drinking water guideline limits established in 2025 set PFOS concentrations as low as 8 ng/L, forcing industrial facilities to redesign chemical containment and fire suppression strategies. Major companies across mining and aviation sectors, including Maersk and Qantas, have already transitioned to fluorine-free firefighting foams. The Australian Department of Defence has also allocated significant funding for site remediation and procurement of environmentally compliant suppression chemicals. Supporting this regulatory shift, analytical laboratories such as Leeder Analytical have deployed Orbitrap LC-MS technology capable of detecting more than 500 PFAS compounds at ultra-trace levels, reinforcing Australia’s position as a global leader in PFAS-free fire safety chemical innovation.

Fire Fighting Chemicals Market Report Scope

Fire Fighting Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.1 Billion

|

|

Market Size (2034)

|

$4.3 Billion

|

|

Market Growth Rate

|

3.7%

|

|

Segments

|

By Product Type (Dry Chemicals, Wet Chemicals, Dry Powder, Foam-Based Agents, Gaseous Agents), By Application (Portable Fire Extinguishers, Automatic Fire Sprinklers and Fixed Systems, Fire Retardant Materials, Fire Dampers, Industrial Suppression Systems), By End-User Industry (Oil and Gas and Petrochemical, Aviation and Aerospace, Marine and Offshore, Mining and Metals, Commercial and Institutional, Residential and Infrastructure), By Fire Class Compatibility (Class A, Class B, Class C, Class D, Class K)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Johnson Controls International plc, Perimeter Solutions, Carrier Global Corporation, Solvay S.A., 3M Company, DIC Corporation, Linde plc, Honeywell International Inc., Angus Fire, Minimax Viking Group, Ceasefire Industries Private Limited, Foamtech Antifire Company, Amerex Corporation, Orchidee Europe BV, Hiller Companies

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fire Fighting Chemicals Market Segmentation

By Product Type

- Dry Chemicals

- Wet Chemicals

- Dry Powder

- Foam-Based Agents

- Gaseous Agents

By Application

- Portable Fire Extinguishers

- Automatic Fire Sprinklers and Fixed Systems

- Fire Retardant Materials

- Fire Dampers

- Industrial Suppression Systems

By End-User Industry

- Oil and Gas and Petrochemical

- Aviation and Aerospace

- Marine and Offshore

- Mining and Metals

- Commercial and Institutional

- Residential and Infrastructure

By Fire Class Compatibility

- Class A

- Class B

- Class C

- Class D

- Class K

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Fire Fighting Chemicals Industry

- Johnson Controls International plc

- Perimeter Solutions

- Carrier Global Corporation

- Solvay S.A.

- 3M Company

- DIC Corporation

- Linde plc

- Honeywell International Inc.

- Angus Fire

- Minimax Viking Group

- Ceasefire Industries Private Limited

- Foamtech Antifire Company

- Amerex Corporation

- Orchidee Europe BV

- Hiller Companies

*- List not Exhaustive