Fitness Ball Market: Growth Fueled by Home Fitness Trends, Functional Training, and Rehabilitation Demand

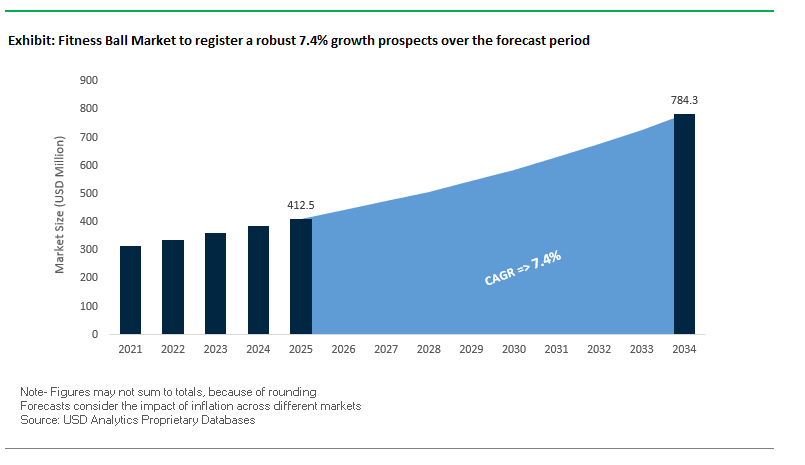

The global fitness ball industry is expected to increase from $412.5 million in 2025 to $784.3 million in 2034, with a CAGR of 7.4%, to emerge as a robust segment among total fitness equipment and wellness. Its success stems from versatility, affordability, and extensive usage, in commercial gyms, home fitness installations, and rehabilitation centers. For industry professionals, the category growth is fueled by exponential demand for functional training equipment, rising enrollment in home-based fitness programs, and the increasing usage of physiotherapy in wellness programs.

The value proposition of the fitness ball is achieved through its applicability across a broad spectrum of exercise types from core stability and strengthening through to Pilates, yoga, and injury rehabilitation. Increasing global health awareness combined with the trend towards digital and on-demand fitness programs is driving adoption of the product. Furthermore, emerging smart fitness ball technology to track posture and reps is creating the foundation for technology-enabled fitness accessories, which could redefine consumer expectations.

Key Insights for Industry Professionals:

- Home Fitness Expansion: Online workout classes and hybrid fitness models are directly boosting at-home fitness ball purchases.

- Functional Training Demand: Core stability and balance exercises are now central to modern training programs.

- Rehabilitation Integration: Physical therapy adoption of fitness balls for spine health and muscular correction is growing.

- Sustainability Shift: Eco-friendly materials, such as PVC-free designs, are gaining traction among conscious consumers.

- Tech Influence: Early innovations in connected and feedback-enabled fitness balls indicate future premium segment growth.

Product Innovation and Evolving Use Cases in Fitness Ball Market

Trends in the global fitness ball market have seen recent developments in product technology, fitness event integration, and sustainability-led innovation. In August 2025, the growing popularity of HYROX functional fitness races in India saw over 2,600 people participating in its Delhi edition, which reflects the key position of equipment like wall balls in competitive and recreationally derived fitness programs. This new functional training trend has a direct influence on product demand for retail markets and commercial gyms.

In July 2025, Gaiam expanded its product line with the Total Body Balance Ball Kit, available in multiple sizes, an air pump, and access to full-length digital workouts positioning itself at the intersection of equipment and digital content markets. This bundling is reflective of an emerging competitive strategy where brands aim to sell not a product but a complete user experience.

January 2025 was a milestone for sustainability with Progressing Ballet Technique's ProBall, which features grip technology, burst resistance level of 1000 kgs, and sustainable PVC. This is in line with the consumer trend towards products that offer durability, performance, and sustainability. In the meantime, the overall M&A trends for fitness operators during June 2025 showed strategic refocusing, whereby some operators shifted focus towards high-value, low-cost gyms and boutique models a trend that will influence procurement behavior for add-ons like fitness balls.

The effect of technology is still evident. Even though mobile ordering technology from a different industry (July and August 2024) is not necessarily transferable to fitness balls, they exhibit the use of convenience technology across industries, a use more and more prevalent in fitness retailing in the guise of virtual fitting technology, equipment subscription models, and AI-trained workouts.

Trends and Opportunities Driving the Global Fitness Ball Market

Anti-Burst Technology Redefining Safety Standards in Fitness Equipment

Anti-burst technology use has become a signature trend in the fitness ball market, addressing one of the most common safety concerns sudden bursting under intensive use. Engineered to dissipate extreme loads of more than 1000kg, premium anti-burst fitness balls feature a slow-deflation mechanism that prevents sudden collapse and minimizes injury risks. Constructed of high-density premium PVC or proprietary materials, anti-burst fitness balls remain elastic at full inflation, enhancing product durability and providing consistent performance. The increased weight capacity has made their application extend beyond Pilates and yoga to strength training, enabling exercises such as weighted squats, chest presses, and stability tests heretofore the exclusive province of larger, more expensive gym equipment. For commercial fitness clubs, physical therapy centers, and home fitness enthusiasts, anti-burst design is becoming a quality and performance standard, driving purchasing decisions in consumer and commercial markets.

Smart Fitness Balls with EMG Feedback for Precision Training

Technological integration is pushing the boundaries of fitness balls, with smart balls featuring Electromyography (EMG) feedback being a high-end innovation. By integrating muscle-activation sensors into the surface of the ball, individuals can monitor real-time electrical activity for key muscle groups, enabling fine-tuned adjustments in form and intensity. With smartphone apps, these systems offer data-driven feedback on workout efficacy, beneficial for elite athletes and rehab patients. Physical therapists can use EMG feedback to monitor progress, detect muscle imbalances, and verify proper activation during rehab exercises. The technology also facilitates gamification-based training experiences, transforming workouts into interactive sessions that enhance compliance. As connected fitness environments grow, EMG-powered fitness balls stand as high-value, multi-function training tools for pro sports centers, medical rehab centers, and luxury home gyms.

Integrating Fitness Balls into Corporate Ergonomics and Active Seating Programs

The movement towards hybrid/flexible offices has fueled the demand for active sitting solutions to counter the ill effects of prolonged sedentary behavior. Fitness balls are being integrated into corporate wellness initiatives to improve core engagement, posture, and micro-movements at the workplace. Compared to static seating, sitting on a stability ball quietly activates stabilizing muscles, enhancing spinal alignment and reducing stiffness. Cost-effectiveness compared to high-end ergonomic chairs makes them a compelling choice for corporations seeking scalable wellness initiatives. With office optimization in hybrid configurations, fitness balls also offer a space-efficient solution, particularly in rotation for short-duration use during the workday. Corporations can also induce participation by introducing short fitness breaks or seated exercise challenges, presenting the ball as a functional health investment and not merely a substitute chair.

Pediatric Physical Therapy as a High-Growth Specialized Segment

The clinical uses of fitness balls in rehabilitation for pediatric patients are well established, offering a solid expansion opportunity. Used to improve motor skills, balance, and coordination, fitness balls are standard equipment in therapies for cerebral palsy, developmental delay, and neuromuscular disorder. Their game-like, fun nature increases compliance in pediatric patients, and their versatility treats a range of therapy targets from core strengthening to sensory integration exercises. By developing a relationship with healthcare professionals, manufacturers can connect fitness balls with medical necessity and increase their chances of insurance coverage. Marketing messages boasting their dual use as both therapeutic tool and recreational device could spur adoption by hospitals, clinics, and home rehabilitation programs, positioning them in child wellness and recovery markets.

Market Share Insights of the Fitness Ball Industry

Market Share by Material: PVC Dominates, TPE and Anti-Burst Materials Accelerate Growth

PVC is the market leader with 50% share due to its durability, elasticity, and cost-effectiveness, though environmental pressures are driving a shift towards more sustainable variants. PVC variants are being produced in recycled and non-toxic formats to address sustainability trends. TPE (Thermoplastic Elastomers) is the growth leader with its hypoallergenic, soft-touch, and recyclable characteristics, appealing to the green consumer. Anti-burst materials have 15% market share, with high usage in commercial fitness centers and rehabilitation facilities for their higher safety factor. Rubber is a specialist material, prized for uses involving high-intensity and outdoor training where best grip and elasticity are a top priority. This diversified material base is a trade-off between performance-driven durability and innovation driven by sustainability.

Market Share by End-User: Individual Consumers Lead, Professional and Institutional Use Expands

Individuals account for 45% of the market, with the post-pandemic surge in home fitness adoption and online fitness platforms leading the way. Fitness balls are valued for their affordability, versatility, and ability to augment other home training equipment. Fitness professionals account for 25%, integrating balls into group fitness classes, personal training, and functional training programs. Physical therapists are a major segment, utilizing fitness balls extensively in rehabilitation for balance training, posture correction, and reconditioning of muscles. Schools are increasingly incorporating them into youth fitness programs and as alternate seating in the classroom to facilitate active learning. This broad base of users underscores the diversity of the market, as fitness balls assume roles ranging from home wellness essentials to professional-grade rehabilitation tools.

.png)

Leading Brands Shaping Innovation, Quality, and Market Reach in Fitness Ball Industry

The Competitive Landscape of the fitness ball market is defined by a blend of fitness specialists, wellness brands, and global sportswear leaders, each leveraging their unique strengths in design, material science, and consumer engagement. Key players included are GAIAM, Inc., Reebok International, SPRI Products, Dynapro, Live Infinitely, Black Mountain Products, Valor Industries, SIVA Health, Real Pilates, Cando, Inc., Tone Fitness, Theraband, Body-Solid, Inc., Champion Barbell, Power Systems, Inc., Others.

Gaiam – Wellness-Centric Home Fitness Solutions

Gaiam dominates the yoga and wellness segment with its anti-slip grip surface exercise balls and complete home exercise sets. Its Total Body Balance Ball has user-adjustable height and digital access to exercises, following the brand's emphasis on delivering complete-package solutions to fitness-conscious consumers.

Technogym S.p.A. – Premium Wellness Integration

Technogym's Wellness Ball is marketed as upscale, recyclable vinyl with professional-grade durability. Phthalate- and latex-free, it meets standards for sustainability as well as fitting within the corporate wellness system that runs from commercial fitness clubs to luxury home installations.

TheraBand – Clinical-Grade Rehabilitation Equipment

TheraBand leverages its medical authority to sell Pro Series SCP Exercise Balls with anti-burst and slow deflation technology that is critical in clinical and rehabilitation settings. Its size- and color-coded product line simplifies product selection for physical therapists, further establishing credibility in the healthcare-professional channel.

Trideer – E-Commerce Value Leader

Trideer dominates online retailers with affordable, extra-thick exercise balls with superior weight-bearing capacity and slow deflation technology. By adding pumps and offering varying sizes, it appeals to affordable home gym consumers who desire convenience without sacrificing quality.

Reebok – Athletic Brand Diversification

Reebok's Stability Gym Ball combines dual-textured styling with resistance to bursting, making it suitable for a variety of exercises. By adding it to its broader fitness equipment offerings, Reebok remains relevant in training and lifestyle markets both, blending performance reliability with brand prestige.

United States: Home Fitness Adoption and Innovation in Ergonomics

The United States fitness ball market is thriving on the back of the at-home fitness revolution and a growing focus on holistic wellness. Consumers are increasingly investing in versatile, affordable, and space-efficient workout tools that fit seamlessly into home gyms. Fitness balls have become a staple due to their ability to support strength training, balance improvement, posture correction, and rehabilitation exercises. Their popularity extends beyond personal use, as corporate wellness programs now actively incorporate gym balls for active sitting, helping to counteract the health risks associated with prolonged desk work. The U.S. fitness culture, driven by a blend of performance goals and preventive health measures, ensures consistent demand across diverse consumer segments, from professional athletes to casual users.

Technological integration is emerging as the next frontier in the American market. Although still in early adoption stages, smart fitness balls with embedded sensors are being developed to track movement, measure posture accuracy, and provide real-time feedback via mobile apps. Manufacturers are also focusing on anti-burst safety designs, textured surfaces for grip, and eco-friendly materials to align with sustainability goals. With online retail dominating distribution, brands are leveraging influencer-led marketing campaigns and virtual fitness classes to position fitness balls as an essential, multi-purpose training accessory. This blend of innovation, consumer convenience, and lifestyle integration continues to set the U.S. market apart.

Germany: Health Policy Support and Medical-Grade Applications

Germany’s fitness ball market benefits from a strong public health infrastructure and policies that actively encourage physical activity. National health initiatives like IN FORM and the Präventionsgesetz (Preventive Health Care Act) promote fitness equipment usage in schools, workplaces, and rehabilitation centers. Gym balls, often referred to locally as “Swiss Balls,” have a long-standing reputation in Germany for physical therapy and medical rehabilitation, particularly in addressing back pain and improving core stability. This established healthcare application creates a steady demand for certified, medical-grade products that meet the country’s strict safety and quality standards.

German consumers are known for their preference for durable, precisely engineered fitness equipment. Manufacturers cater to this demand by producing high-quality fitness balls with advanced anti-burst materials, ergonomic designs, and optimal weight capacities for various training needs. Backed by scientific research from German universities and sports medicine institutions, these products carry a high degree of credibility in the market. The combination of government advocacy, scientifically validated benefits, and a strong domestic manufacturing base positions Germany as a leader in both consumer and therapeutic segments of the fitness ball market.

China: E-commerce Dominance and Scalable Manufacturing Power

China’s fitness ball market is fueled by the country’s rapidly expanding fitness population, especially among millennials and Gen Z. The surge in health awareness, coupled with the influence of digital fitness classes and live-streamed workout sessions, has made gym balls a regular feature in home and studio workouts. Their affordability, ease of use, and versatility make them particularly appealing to first-time fitness equipment buyers. Demand is further supported by corporate and educational wellness programs that integrate gym balls for posture correction and ergonomic seating.

As a global manufacturing powerhouse, China’s robust supply chain and advanced production technologies allow for high-volume, cost-efficient manufacturing. Domestic brands and OEM producers supply both local and international markets, offering products in diverse sizes, colors, and material specifications. Innovation is evident in the development of anti-slip coatings, advanced PVC formulations, and eco-conscious materials that meet global safety standards. With e-commerce platforms like Tmall, JD.com, and Taobao dominating retail, brands leverage digital marketing, influencer partnerships, and livestream selling to capture massive online audiences, cementing China’s role as both a producer and a fast-growing consumer market.

Japan: Compact Design Leadership and Aging Population Focus

In Japan, the fitness ball market is shaped by space-efficient product design and the country’s unique demographic profile. Urban living spaces often require compact and multi-functional fitness equipment, making gym balls an ideal choice for home workouts. Japanese manufacturers and distributors prioritize lightweight, portable, and aesthetically pleasing designs without compromising durability or safety. Additionally, Japan’s emphasis on precision engineering ensures that fitness balls are ergonomically optimized for both exercise and rehabilitation.

The country’s aging population plays a significant role in market demand, with fitness balls widely used in low-impact exercise routines and fall-prevention programs for seniors. Rehabilitation clinics and wellness centers integrate gym balls into physiotherapy regimens for improving balance, flexibility, and muscle tone. Local brands focus on high-quality craftsmanship, anti-burst materials, and easy-to-clean surfaces to meet hygiene and safety requirements. By combining compact design innovation with solutions tailored to elderly wellness, Japan has carved out a specialized niche in the global fitness ball market.

United Kingdom: Home Workout Culture and Office Wellness Integration

The United Kingdom’s fitness ball market is sustained by a robust home workout culture and growing interest in ergonomics for both personal and professional environments. The post-pandemic emphasis on at-home fitness continues to fuel demand for affordable, versatile workout tools like gym balls, which are widely used for yoga, Pilates, and strength training. Consumers value their portability, adaptability, and the ability to incorporate them into a variety of training programs.

Beyond home fitness, the UK has embraced the use of gym balls in office wellness programs to encourage active sitting and improve posture. While opinions vary on replacing office chairs entirely, short-duration usage to engage core muscles and prevent slouching is a recognized trend. Online retail plays a dominant role, with specialty sports retailers and major e-commerce platforms driving sales. To stand out, brands are focusing on vivid color ranges, textured designs, and high-grip surfaces while promoting the postural and rehabilitative benefits of their products through influencer collaborations and online fitness communities.

Fitness Ball Market Report Scope

Fitness Ball Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$412.5 Million

|

|

Market Size (2034)

|

$784.3 Million

|

|

Market Growth Rate

|

7.4%

|

|

Segments

|

By Size (45cm, 55cm, 65cm, 75cm, 85cm), By Material (PVC, TPE (Thermoplastic Elastomers), Rubber, Anti-burst materials), By Application (Home Use, Commercial Gyms, Physical Therapy & Rehabilitation, Corporate Wellness Programs), By End-User (Individuals, Fitness Professionals, Physical Therapists, Educational Institutions), By Distribution Channel (Online Retail, Specialty Stores, Department Stores, Direct-to-Consumer)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

GAIAM, Inc., Reebok International, SPRI Products, Dynapro, Live Infinitely, Black Mountain Products, Valor Industries, SIVA Health, Real Pilates, Cando, Inc., Tone Fitness, Theraband, Body-Solid, Inc., Champion Barbell, Power Systems, Inc., Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fitness Ball Market Segmentation

By Size

By Material

- PVC

- TPE (Thermoplastic Elastomers)

- Rubber

- Anti-burst materials

By Application

- Home Use

- Commercial Gyms

- Physical Therapy & Rehabilitation

- Corporate Wellness Programs

By End-User

- Individuals

- Fitness Professionals

- Physical Therapists

- Educational Institutions

By Distribution Channel

- Online Retail

- Specialty Stores

- Department Stores

- Direct-to-Consumer

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Fitness Ball Market

- GAIAM Inc.

- Reebok International

- SPRI Products

- Dynapro

- Live Infinitely

- Black Mountain Products

- Valor Industries

- SIVA Health

- Real Pilates

- Cando Inc.

- Tone Fitness

- Theraband

- Body-Solid Inc.

- Champion Barbell

- Power Systems Inc.

* List Not Exhaustive

Research Coverage

Published by USDAnalytics, this report investigates the global fitness ball ecosystem in depth—tracking market size and revenue pools, technology breakthroughs (e.g., anti-burst and sensor-enabled balls), supply–demand balances, pricing, channel shifts, and competitor playbooks. The analysis reviews regulatory and procurement influences across gyms, healthcare, and corporate wellness; maps customer adoption curves from home fitness to rehabilitation; and highlights country-level white spaces and risks. With granular forecasts to 2034, benchmarking dashboards, and deal pipelines, this report is an essential resource for manufacturers, brands, distributors, investors, and strategy leaders seeking defensible growth in the fitness accessories category. Scope includes-

- Segmentation:

- By Size – 45cm, 55cm, 65cm, 75cm, 85cm

- By Material – PVC, TPE (Thermoplastic Elastomers), Rubber, Anti-burst materials

- By Application – Home Use, Commercial Gyms, Physical Therapy & Rehabilitation, Corporate Wellness Programs

- By End-User – Individuals, Fitness Professionals, Physical Therapists, Educational Institutions

- By Distribution Channel – Online Retail, Specialty Stores, Department Stores, Direct-to-Consumer

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Timeframe: Historic data from 2021–2024 and forecasts from 2025–2034.

- Companies: Competitive analysis/profiles of 15+ players including GAIAM, Reebok International, SPRI Products, Dynapro, Live Infinitely, Black Mountain Products, Valor Industries, SIVA Health, Real Pilates, Cando, Tone Fitness, Theraband, Body-Solid, Champion Barbell, and Power Systems.

Methodology

USDAnalytics applies a blended top-down and bottom-up approach. Market sizing is triangulated from brand revenues, channel sell-out, trade statistics, and procurement in healthcare/education, normalized to constant USD. Primary research includes interviews with OEMs, retailers, gym chains, physiotherapists, distributors, and corporate wellness buyers; secondary inputs span company filings, customs data, association reports, patents, and pricing trackers. Forecasts employ ARIMA and diffusion models for category penetration, with scenario analysis for material shifts (PVC→TPE), technology adoption (smart/EMG balls), and channel mix (e-commerce vs. stores). Quality control includes cohort back-testing, outlier capping, and region-wise sensitivity checks.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.