Fitness Tracker for Sleep Monitoring Market Overview: Growth Outlook and Strategic Insights

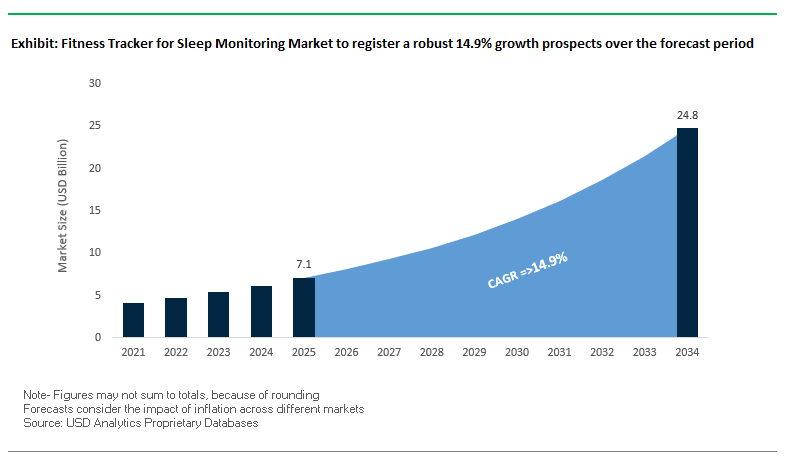

The global fitness tracker for sleep monitoring market is projected to expand from USD 7.1 billion in 2025 to USD 24.8 billion by 2034, achieving a robust CAGR of 14.9%. Situated at the convergence of wearable tech, preventive health, and digital wellness, this market is driven by increased public awareness of sleep's critical importance in both physical and mental health. Contemporary sleep tracking devices have transformed into multipurpose health platforms with sophisticated sensors, AI-driven analytics, and effortless ecosystem connectivity to provide actionable insights. The industry is being fueled by the growing use of health wearables, growth in preventative care models, and consumer demand for personalized health data.

Key Insights for Industry Professionals

- Advanced Sensor Technology – Use of PPG, accelerometers, temperature sensors, and SpO₂ monitoring to capture granular sleep data.

- Personalized Recommendations – Devices now focus on providing actionable sleep hygiene tips and “Sleep Scores” rather than just raw metrics.

- Non-Intrusive Alternatives – Demand is rising for under-mattress sensors, smart rings, and headbands to replace traditional wrist-worn devices.

- Health Platform Integration – Sleep data is increasingly linked to overall wellness metrics such as HRV, readiness scores, and sleep apnea screening.

- Product Diversification – Growing variety in form factors, from wearables to smart home–connected devices.

Fitness Tracker for Sleep Monitoring Market Analysis: Strategic Developments and Industry Momentum

The Competitive Landscape of sleep-centric wearables is characterized by ongoing innovation, algorithmic improvements, and growth into preventative health use cases. In July 2025, Apple widened availability of its sleep apnea detection capability to Australian Apple Watch users, using accelerometer-based micro-movement monitoring to spot breathing anomalies. This follows Apple's further expansion into diagnostic healthcare through its platform. Fitbit, in August 2025, refined its sleep algorithm to more accurately detect short awakenings as the first step in a series of planned improvements to accuracy.

Hardware innovations are more and more combined with scientific collaborations. Samsung, in August 2025, launched the Galaxy Watch8 with KAIST-designed sensors to monitor vascular load and antioxidant status during sleep, consistent with its health prevention positioning. Oura's Ring 4, released in October 2024, brought "Smart Sensing" to adjust readings to personal physiology, improving data accuracy for stress, activity, and cycle tracking.

Market innovation goes beyond form factor. Non-wearable solutions like Withings' under-mattress trackers are becoming popular with users who want to see as little disruption as possible during sleep. The sector is also subject to cross-sector consumer trends sustainability, for example, is informing material selection, with brands introducing environmentally friendly housing and packaging for wearables, following similar changes in other lifestyle and personal care products.

Advanced Technology Trends and Emerging Opportunities in the Fitness Tracker for Sleep Monitoring Market

Medical-Grade Sleep Staging Transforming Consumer Sleep Analytics

The market is moving strongly away from crude sleep/wake detection towards medical-grade sleep staging, enabled by advanced sensor arrays and AI-driven algorithms. Modern wearables now integrate accelerometers, photoplethysmography (PPG), and in some cases EEG-like electrodes to monitor light, deep, and REM sleep stages with accuracy nearing that of a clinical polysomnography (PSG). A systematic review in Sleep confirmed that earlier wrist-based devices were suboptimal, but newer multi-sensor monitors have almost-90% accuracy in sleep stage classification. This is spurred by a growing health-literate consumer demanding actionable, clinically relevant data to inform long-term sleep health. Mainstream brands are pursuing regulatory clearances and validation studies of device performance directly against PSG, paving the way for possible use in clinical screening and remote patient monitoring.

Circadian Light Exposure Monitoring for Overall Sleep Health

Next-gen fitness trackers are incorporating blue and UV light exposure sensors to further increase circadian rhythm entrainment an underappreciated yet valuable aspect of sleep health. As outlined in Chronobiology in Medicine, wearables offer a time-saving alternative to the labor-intensive DLMO method, with the ability to continuously monitor environmental light signals alongside movement, temperature, and heart rate information. With research demonstrating that evening exposure to short-wavelength blue light disrupts melatonin release, devices now provide real-time "light exposure scores" and tailored recommendations, for example, when to engage in natural daylighting to increase energy or restrict screen time in the evenings. This capability takes the utility of trackers from passive sleep monitors to active circadian regulators.

Incorporating Corporate Wellness to Improve Employee Sleep Health

Corporate wellness programs are becoming a top driver of sleep-tracking device adoption as companies link employee sleep quality with productivity and healthcare cost savings. Workplace stress is a top precipitant of sleep disturbance, according to American Psychological Association, and employers are including sleep in more comprehensive wellness programs. Facts show that companies with successful wellness programs are 40% more likely to have superior financial performance, and health options are considered by 87% of employees in their decision-making when choosing an employer. By partnering with corporations, tracker vendors can offer stand-alone programs with workshops, one-on-one coaching, and sleep goal incentives, making sleep monitoring a value-added benefit in talent attraction and retention.

Non-Invasive Disorder Detection through Pediatric Sleep Monitoring

Child-friendly sleep wearables offer a promising alternative to PSG in-lab assessment for pediatric sleep disorders like obstructive sleep apnea. ClinicalTrials.gov cites ongoing trials affirming wearable EEG bands, motion detectors, and ring oximeters for precise home-based sleep staging in children and adolescents. Wearables overcome the comfort and expense barriers of standard diagnostics through the convenience of long-term home monitoring. Firms are responding with tiny, lightweight sensors for comfort and accompanied parent-facing mobile apps that make data interpretation easier and allow pediatrician review. With the tide of unundiagnosed pediatric sleep problems swelling, this market is set to grow.

Fitness Tracker for Sleep Monitoring Market Share and Segmentation Insights

By Technology: Accelerometers and Optical Heart Rate Sensors Lead, Multi-Sensor Systems Rise

Accelerometers hold 35% market share, still the standard technology enjoyed for detecting movement and differentiating wake from all sleep stages. Optical heart rate sensors hold 28% and are now standard in all mid- to high-end trackers for enabling better REM detection accuracy via heart rate variability analysis. Pulse oximetry and respiration sensors are quickly gaining popularity, driven by consumer demand for sleep apnea detection and other disorder screening. Temperature sensors, though still niche, are becoming increasingly important for circadian rhythm tracking and women's health monitoring. Competitive positioning is shifting towards multi-sensor platforms that bring these technologies together into comprehensive, high-accuracy sleep profiling systems.

.png)

By Application: Sleep Quality Monitoring Dominates, Sleep Disorder Diagnosis Accelerates

Sleep quality monitoring has the largest portion at 52% because consumers want to track sleep duration, efficiency, and stage distribution to maximize rest and recovery. Sleep disorder diagnosis takes 30% and is growing fast with new sensors that enable early detection of sleep disorders like sleep apnea, which triggers medical follow-up. Sleep coaching is a new category, employing AI to interpret raw data into individualized, actionable guidance. The use case is also enabled by smart home integration, permitting automated environmental adjustment such as lighting or temperature to maximize sleep conditions. Employer-sponsored wellness adoption is also propelling occupational sleep health monitoring as a benefit differentiator in business plans.

Competitive Landscape – Leading Players in the Fitness Tracker for Sleep Monitoring Sector

The market is dominated by a combination of tech giants with extensive device systems and specialized wellness companies with specialized sleep monitoring experience. Apple Inc., Google LLC (Fitbit), Oura Health Oy, Garmin Ltd., Whoop, Samsung Electronics Co., Ltd., Withings SA, Xiaomi Corporation, Huawei Technologies Co., Ltd., Polar Electro Oy, ResMed Inc., Dreem, Amazfit, Eight Sleep, Eko Health, Others are some of the notable players mentioned.

Garmin Ltd. – Athlete-Focused, Total Health Integration

Garmin incorporates sleep monitoring into its "Body Battery" feature, bringing together sleep, tension, and activity data for an overall recovery perspective. Its sophisticated metrics feature HRV, breathing rate, and Pulse Ox monitoring. Sport enthusiasts' favorite, Garmin has now included nap monitoring to further improve recovery analytics, solidifying its role as a performance-based health platform.

Fitbit (Google LLC) – Gamified Coaching with Accessible Tracking

Fitbit's easy-to-use interface and "Sleep Profile" capability make tracking a form of gamification by giving users a "sleep animal" designation based on patterns. Integration with Google's Pixel Watch enhances its presence in ecosystems, and its August 2025 algorithm update enhanced detection of awake periods more accurately to report.

Samsung Electronics Co., Ltd. – Sensor-Driven Preventative Care Leader

Samsung Galaxy Watch8 has improved BioActive Sensors that are able to monitor vascular load and antioxidant index in rest mode. It also has a sleep coaching feature with snore detection and pet assignment based on patterns, and smart home compatibility allows for automatic environment adjustment for quality sleep.

Apple Inc. – Clinical Ambition within Health Ecosystem

Apple's sleep tracking is firmly based in the iOS Health app, combining stage analysis with well-being metrics. Its machine learning-based detection of sleep apnea is also a reflection of greater focus on preventive health. The addition of "Wind Down" and "Sleep Focus" also puts Apple ahead of habit-forming sleep improvement products.

Ōura Health Oy – Unobtrusive, Evidence-Based Smart Ring

Oura's ultralight smart ring tracks real-time sleep stage monitoring, HRV, temperature rhythms, and SpO₂. The subscription service enhances user engagement with tailored insights, and polysomnography verification ensures clinical-grade accuracy.

United States: Regulatory Evolution and AI-Driven Sleep Health Innovation

The United States fitness tracker for sleep monitoring market is being shaped by a shifting regulatory landscape under the oversight of the FDA’s Digital Health Center of Excellence. While most sleep trackers are still marketed as wellness devices, the push toward classifying certain products as medical devices especially those claiming to detect sleep disorders like sleep apnea is driving brands to pursue greater clinical validation. This trend is raising product standards and pushing the industry toward more medically relevant applications.

Technological innovation is advancing quickly, with companies developing multi-sensor platforms that monitor SpO₂, body temperature, and heart rate variability (HRV) while leveraging AI algorithms to deliver actionable sleep insights. Non-wearable technology is an emerging subsegment, featuring radar-based smart mattresses and under-mattress infrared sensors for contact-free monitoring. Corporate wellness programs are becoming a major adoption driver, with employers integrating sleep trackers into benefits packages to improve employee health and productivity. Strategic partnerships such as Apple’s sleep enhancements in watchOS and Google’s Fitbit-led advancements are mainstreaming high-quality sleep monitoring across the consumer electronics sector.

China: Manufacturing Leadership and Smart Wearable Diversification

China continues to dominate global wearable manufacturing while increasingly investing in R&D for advanced sleep monitoring devices. Domestic brands and ODM/OEM suppliers produce a full spectrum of products, from budget-friendly fitness bands to premium smart rings with multi-sensor capabilities. Government policies promoting digital health and smart technology provide infrastructure and funding for both innovation and scale.

Academic research institutions are exploring the integration of consumer sleep trackers into healthcare workflows, enabling personalized sleep health programs. E-commerce remains the primary distribution channel, with platforms and livestream selling offering both broad reach and fast consumer adoption. The market is diversifying into non-wrist categories, such as discreet smart rings and clip-on sensors, to cater to comfort-focused consumers who prefer non-intrusive devices.

European Union: Regulatory Compliance and Privacy-First Product Design

The EU market is heavily influenced by stringent medical device regulations (MDR, IVDR), forcing brands to differentiate clearly between wellness-oriented trackers and medically validated devices. Compliance requires robust clinical evidence for any diagnostic claims, which is pushing European companies to invest in precision sensor technologies and extensive validation trials.

Data privacy is a defining factor, with the GDPR requiring transparency and consumer control over personal health data. This is leading to product designs that emphasize local data storage, encryption, and consent-based sharing. The EU’s eco-design policies are also steering brands toward sustainable materials, repairable hardware, and long-lifespan devices. R&D priorities include EEG-based headbands and neurotechnology-driven wearables capable of mapping brainwave activity during various sleep stages, elevating data accuracy and clinical relevance.

Japan: Aging Demographics and Non-Invasive Sleep Solutions

Japan’s rapidly aging population and rising awareness of sleep-related health issues including insomnia and sleep apnea are generating strong demand for sleep monitoring solutions. The country is positioning itself as a leader in integrated sleep health ecosystems, combining hardware, data analytics, and consumer lifestyle services. Unique initiatives, such as NTT Data Japan’s capsule hotel sleep labs, collect large-scale sleep datasets to inform product development across food, wellness, and medical device industries.

Consumer preference leans toward non-invasive and user-friendly products, with strong adoption of smart mattresses, bed sensors, and ambient monitoring devices that avoid the need for continuous wearable use. Government healthcare R&D funding and its emphasis on preventive health are accelerating innovation and adoption. This, coupled with Japan’s expertise in precision electronics, is reinforcing its competitive edge in the high-tech sleep monitoring space.

Fitness Tracker for Sleep Monitoring Market Report Scope

Fitness Tracker for Sleep Monitoring Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.1 Billion

|

|

Market Size (2034)

|

$24.8 Billion

|

|

Market Growth Rate

|

14.9%

|

|

Segments

|

By Product (Wearables (Smartwatches, Fitness Bands, Smart Rings), Non-Wearables (Smart Mattresses, Under-Mattress Sensors)), By Technology (Accelerometers, Optical Heart Rate Sensors, Pulse Oximeters, Respiration Sensors, Temperature Sensors), By Application (Sleep Quality Monitoring, Sleep Disorder Diagnosis, Sleep Coaching), By Distribution Channel (Online Retail, Specialty Stores, Pharmacies, Sleep Centers), By End User (Adults, Children, Athletes)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Apple Inc., Google LLC (Fitbit), Oura Health Oy, Garmin Ltd., Whoop, Samsung Electronics Co., Ltd., Withings SA, Xiaomi Corporation, Huawei Technologies Co., Ltd., Polar Electro Oy, ResMed Inc., Dreem, Amazfit, Eight Sleep, Eko Health, Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fitness Tracker for Sleep Monitoring Market Segmentation

By Product

- Wearables

- Smartwatches

- Fitness Bands

- Smart Rings

- Non-Wearables

- Smart Mattresses

- Under-Mattress Sensors

By Technology

- Accelerometers

- Optical Heart Rate Sensors

- Pulse Oximeters

- Respiration Sensors

- Temperature Sensors

By Application

- Sleep Quality Monitoring

- Sleep Disorder Diagnosis

- Sleep Coaching

By Distribution Channel

- Online Retail

- Specialty Stores

- Pharmacies

- Sleep Centers

By End User

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Fitness Tracker for Sleep Monitoring Market

- Apple Inc.

- Google LLC (Fitbit)

- Oura Health Oy

- Garmin Ltd.

- Whoop

- Samsung Electronics Co. Ltd.

- Withings SA

- Xiaomi Corporation

- Huawei Technologies Co. Ltd.

- Polar Electro Oy

- ResMed Inc.

- Dreem

- Amazfit

- Eight Sleep

- Eko Health

* List Not Exhaustive

Research Coverage

This report investigates the Fitness Tracker for Sleep Monitoring Market end-to-end, delivering strategic breakthroughs, analysis reviews, and highlights on how multi-sensor wearables, AI analytics, and ecosystem integrations are redefining consumer sleep health. Built by USDAnalytics, the study benchmarks platform strategies of leading device makers, quantifies mix shifts across product types and use cases, and surfaces commercialization plays spanning wellness, employer benefits, and pre-clinical screening. By connecting technology roadmaps with regulatory and privacy trends, this report is an essential resource for executives, product leaders, investors, and clinicians who need decision-grade evidence on where revenue, margins, and adoption will concentrate through 2034. Scope includes-

- Segmentation covered:

- By Product: Wearables; Non-Wearables

- By Technology: Accelerometers; Optical Heart Rate Sensors; Pulse Oximeters; Respiration Sensors; Temperature Sensors

- By Application: Sleep Quality Monitoring; Sleep Disorder Diagnosis; Sleep Coaching

- By Distribution Channel: Online Retail; Specialty Stores; Pharmacies; Sleep Centers

- By End User: Adults; Children; Athletes

- Geographic scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Time horizon: Historical 2021–2024; Forecast 2025–2034.

- Company coverage: Strategy and profile reviews of 15+ companies.

Methodology

USDAnalytics applies a triangulated approach that blends primary interviews (device OEMs, sensor suppliers, clinicians, sleep-lab directors, corporate wellness buyers, regulators) with secondary intelligence (clinical validation papers, patent filings, import/export and channel sell-through data, financial disclosures, and app store telemetry). We size the market bottom-up from country-level device volumes by product and channel, and reconcile top-down to macro health-wearable baselines. Forecasts employ diffusion curves for new sensors, pricing/mix elasticity, and scenario analysis for regulatory clearances and reimbursement. Competitive benchmarking evaluates accuracy (vs. PSG studies), battery life, firmware cadence, privacy posture, and ecosystem lock-in. All results undergo multi-source triangulation and sensitivity checks to ensure reliability.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.