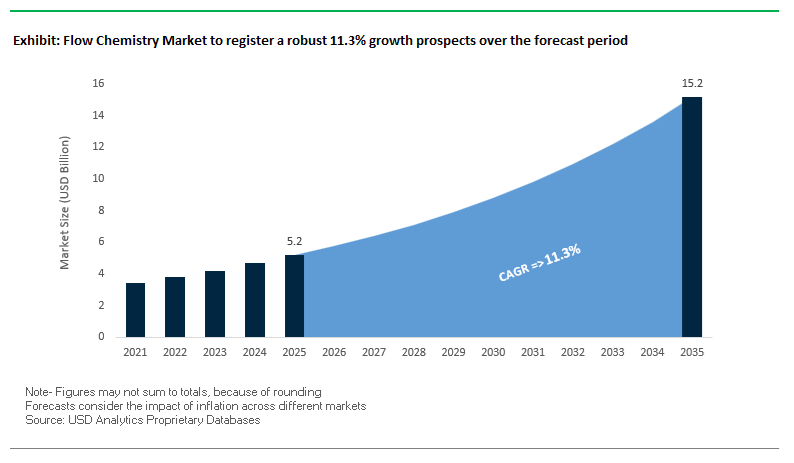

The Flow Chemistry Market, valued at USD 5.2 billion in 2025, is projected to reach USD 15.2 billion by 2035, expanding at a robust CAGR of 11.3%. The growth is supported by the technology’s ability to address some of the most critical challenges in chemical manufacturing—namely safety, sustainability, cost efficiency, scalability, and regulatory compliance. Flow chemistry is increasingly central to continuous pharmaceutical manufacturing, fine and specialty chemicals production, catalysis innovation, and green chemistry initiatives.

The global Flow Chemistry Market is undergoing a rapid transformation driven by advancements in modular reactor design, AI-enabled optimization, enhanced hardware components, and large-scale adoption by pharmaceutical manufacturers. A key demonstration of the technology’s expanding application base occurred in September 2025, when Vapourtec’s R-Series reactor was installed at ANSTO to support the synthesis of specialized deuterated molecules. The milestone illustrates the increasing role of flow systems in advanced materials science, nuclear chemistry, and high-value specialty molecule synthesis—segments traditionally dominated by batch processes due to their complexity. Earlier innovations including Vapourtec’s April 2025 launch of its enhanced ‘BLACK’ peristaltic pump tube highlight the sector’s ongoing focus on improving compatibility with aggressive reagents, thereby strengthening reliability and extending use cases in challenging continuous reactions.

R&D breakthroughs continue to address long-standing challenges in flow chemistry implementation. In June 2025, KHIMOD and the University of Liège announced a breakthrough in integrating ultrasound technology into monolithic exchanger-reactors, enabling in-situ control of solid precipitation—one of the biggest pain points in scaling flow reactions for APIs. The innovation targets clogging issues that affect roughly 60% of flow-capable chemistry, unlocking broader commercial viability for multi-step, high-solid pharmaceutical reactions. Similarly, in January 2025, Asahi Glassplant (Syrris) highlighted the use of its Asia Flow Chemistry System by Gedeon Richter for synthesizing novel heterocyclic scaffolds, strengthening validation of microreactor platforms in modern drug discovery workflows.

Industrial-scale adoption remains a major catalyst for market expansion. A pivotal event occurred in July 2024, when Corning and Laurus Labs inaugurated a G4 Advanced-Flow™ Reactor system for high-volume API production in India—one of the world’s largest pharmaceutical manufacturing hubs. The demonstrates the movement of flow chemistry from R&D to full production environments. Meanwhile, Corning’s June 2024 introduction of its Lab Reactor System 2 reflects strong momentum in flow photochemistry, a domain experiencing surging interest due to LED-driven catalytic innovations in pharma and fine chemicals. Together, these developments signify a market shifting rapidly toward continuous, scalable, and digitally optimized chemical synthesis.

Buyers and R&D teams evaluating flow technology are primarily concerned with how continuous processing reduces hazardous inventories, enhances heat and mass transfer, improves reaction reproducibility, and shortens development timelines.

Buyers also examine whether microreactor systems and modular continuous platforms can handle multistep transformations, solid-forming reactions, and photochemical or electrochemical conditions with greater control than batch systems. Equally important is the role of AI-driven optimization and process analytical technologies (PAT), which allow fast reaction tuning with lower reagent consumption. As global pressure mounts for greener, safer, and more flexible production models, flow chemistry is becoming a foundational approach for next-generation chemical synthesis.

- E-factor reductions of up to 87% make continuous flow essential for green chemistry and sustainable manufacturing goals.

- Process time compression from days to hours dramatically accelerates API development cycles and speeds time-to-market.

- Safety improves by more than 100× due to low reaction inventory, enabling safer nitration, hydrogenation, and other high-hazard processes.

- AI-driven synthesis optimization improves yields (e.g., achieving 79% yield) while reducing experimental rounds by nearly 28%, cutting development costs.

- CO₂ emissions reductions of up to 79% align with global decarbonization initiatives and regulatory pressures on chemical manufacturers.

Acceleration of Continuous Pharmaceutical Production and Digitally Driven Innovation Shaping the Flow Chemistry Market

Trend 1 - Flow Chemistry Becomes Foundational to Continuous Manufacturing (CM) of APIs Across the Pharmaceutical Sector

Flow chemistry has emerged as the central technology enabling the pharmaceutical industry's transition from batch processing to Continuous Manufacturing (CM). Regulatory agencies are explicitly supporting CM adoption due to its reliability, traceability, and significant reductions in drug development timelines.

A self-audit by the FDA Office of Pharmaceutical Quality (OPQ) revealed that CM applications were approved nine months faster on average compared with batch applications. Moreover, CM-based products entered the market twelve months earlier, illustrating clear regulatory incentives for manufacturers adopting flow chemistry for API synthesis.

Industrial validation further underscores its transformative potential. The well-cited Novartis–MIT CM collaboration demonstrated a fully integrated pilot plant converting raw materials into finished tablets in under 48 hours-a dramatic improvement over traditional multi-step batch processes that typically require up to 200 days, largely due to intermediate storage and cleaning cycles.

CM also simplifies lifecycle management. An FDA review comparing CM and batch manufacturing found zero major post-approval changes in equipment or batch size among CM submissions, highlighting flow chemistry’s inherent process flexibility and lower regulatory burden.

Across the broader CM ecosystem, continuous synthesis-powered by flow chemistry-holds the largest revenue share and is forecast to grow fastest due to its irreplaceable role in high-throughput API and intermediate production.

Trend 2 - Flow Chemistry Enables On-Demand, Point-of-Use Synthesis of Hazardous and Energetic Compounds

Flow reactors provide unmatched thermal control and mixing efficiency, making them ideal for the safe production of highly exothermic, toxic, or shock-sensitive chemicals that pose severe risks under batch conditions.

A defining advantage is flow chemistry’s high surface-area-to-volume ratio, which enables rapid heat removal. Reactions such as nitrations-traditionally requiring 4–6 hours in batch-can be executed safely in under 30 minutes in a flow system, dramatically reducing the risk of thermal runaway.

Flow chemistry also eliminates reliance on cryogenic conditions. Hazardous reagents such as n-butyllithium, which require temperatures below −50°C in batch to prevent uncontrolled side reactions, can be handled near +20°C in flow, reducing utility costs by approximately 70% and improving operational safety.

Equally important is the elimination of intermediate storage for unstable materials. Compounds like hydrazoic acid, used in tetrazole synthesis, can be generated in situ and consumed immediately downstream. This avoids accumulation of shock-sensitive intermediates that historically contributed to fatal industrial accidents.

Pharmaceutical manufacturers also report up to 50% reductions in solvent use when using flow systems for hazardous reactions, aligning with corporate sustainability targets while lowering operational costs.

Opportunity 1 - Modular Automated Flow Systems Enable Distributed, Rapidly Deployable Pharmaceutical Manufacturing

Flow chemistry’s compactness and modularity position it as the cornerstone of a new generation of distributed, localized, and rapidly deployable pharmaceutical production infrastructure.

Modular systems built around Module Type Package (MTP) concepts allow manufacturers to purchase standardized, pre-validated skids integrating synthesis, purification, and inline analytics. This dramatically reduces engineering complexity and allows rapid scaling from laboratory to tens-of-kilograms-per-day pilot production, compressing time-to-market for essential therapeutics.

Vendor-agnostic interoperability further enhances manufacturing agility. Facilities can assemble skids from multiple suppliers without “vendor lock-in,” simplifying technology updates and lowering CAPEX over the plant lifecycle.

The smaller reactor volumes inherent to flow chemistry enable entire CM production lines to fit within compact enclosures, making it feasible to build distributed manufacturing hubs in hospitals, remote regions, or regions lacking pharma infrastructure. This distributed strategy enhances supply chain resilience, reduces reliance on centralized mega-plants, and supports on-site production of short-shelf-life APIs.

As global regulators and governments prioritize decentralized pharmaceutical manufacturing for pandemic preparedness, modular flow chemistry systems represent one of the most scalable and strategically significant opportunities in the sector.

Opportunity 2 - AI/ML-Integrated Autonomous Flow Chemistry Unlocks Accelerated Reaction Discovery and Optimization

The deterministic, high-fidelity data produced by flow reactors makes them ideal for integration with AI/ML-driven autonomous reaction discovery platforms, transforming the pace and scope of chemical innovation.

Academic breakthroughs such as RoboChem demonstrate that autonomous flow synthesis robots can optimize 10–20 molecules per week, a rate that would require months of manual labor from skilled chemists. Notably, RoboChem improved reaction yields in ~80% of previously published cases, validating AI’s ability to systematically outperform human-guided optimization.

Platforms such as Fast-Cat autonomously map multidimensional reaction spaces-temperature, residence time, reagent ratios, ligand identity-often more than doubling the number of viable selectivity and yield outcomes compared with conventional experimentation.

The reliability of the data generated is the key enabler. Flow reactors provide uniform temperature control, defined residence times, and consistent mixing conditions, producing clean datasets ideal for machine-learning algorithms. These high-quality data streams allow AI systems to learn underlying chemical patterns with greater clarity than batch-derived data permit.

In one landmark case, an autonomous flow system identified previously non-intuitive reaction conditions, including extremely low light exposures that human chemists would not have predicted. This demonstrates the ability of AI-driven flow chemistry to discover entirely new chemical space, accelerating innovation in pharmaceuticals, catalysts, advanced materials, and specialty chemicals.

Flow Chemistry Market Share Analysis

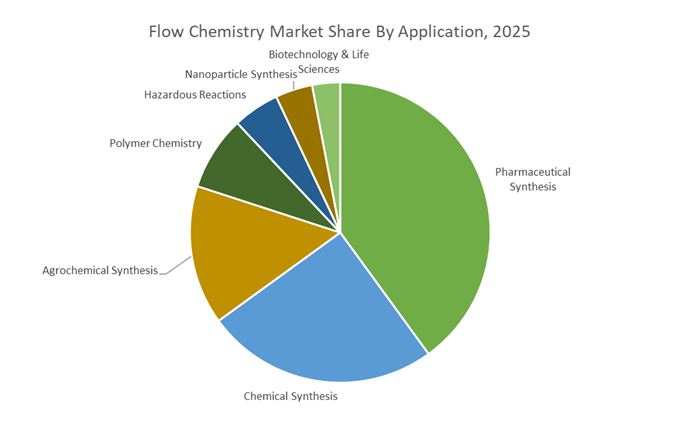

Market Share by Application / Reaction Type: Pharmaceutical Synthesis Leads Through Safety, Scalability, and High-Precision Reaction Control

Pharmaceutical Synthesis accounts for the leading 40% share of the Flow Chemistry Market, driven by the transformative advantages continuous flow systems offer in API development and complex reaction handling. Flow chemistry—particularly via microreactors—addresses the long-standing safety, efficiency, and quality challenges that batch reactors struggle to overcome, especially when dealing with hazardous, thermally unstable, or highly energetic intermediates. Because microreactors typically operate with internal volumes measured in milliliters, they significantly reduce the risk associated with explosive reagents such as diazomethane and organolithium compounds, enabling pharmaceutical manufacturers to run high-risk chemistries that would otherwise be impractical or prohibited. This enhanced safety profile is matched by substantial process efficiency gains: the high surface-area-to-volume ratio in flow systems enables superior heat and mass transfer, allowing reactions to run safely at elevated temperatures and pressures—often above solvent boiling points—that dramatically accelerate kinetics and reduce reaction times from hours to mere minutes or seconds. Moreover, the precise control over residence time, temperature gradients, and reagent mixing results in higher yields, improved selectivity, and fewer side-products, making flow chemistry ideal for producing high-purity APIs and intermediates. These performance, safety, and quality advantages establish pharmaceutical synthesis as the dominant application driving the adoption of flow chemistry globally.

Market Share by End-Use Industry: Pharmaceuticals & Biotechnology Dominate Through Regulatory Momentum and Economic Efficiency

The Pharmaceuticals & Biotechnology sector holds the largest 55% share, reflecting strong regulatory support and compelling economic incentives that make flow chemistry integral to modern drug manufacturing. Global regulatory agencies—particularly the U.S. FDA—actively promote the transition to Continuous Manufacturing (CM), with industry analyses showing that CM applications often reach approval faster than comparable batch submissions. This acceleration translates into substantial economic gains, estimated at $171 million to $537 million in early revenue benefits for CM adopters. Beyond regulatory momentum, flow chemistry supports process intensification, enabling manufacturers to replace large, multi-step batch reactors with compact, modular continuous systems that can reduce facility footprints by up to 90%, significantly lowering capital expenditure and operational costs. For companies operating in clinical and early commercial stages, flow-based API production also reduces material waste, with reported API savings exceeding 60% due to minimized start-up and shutdown losses. As biopharmaceutical innovation accelerates—driven by complex molecules, high-potency APIs, and personalized medicine—flow chemistry provides the precision, scalability, and safety needed to meet evolving production requirements, reinforcing Pharmaceuticals & Biotechnology as the dominant end-use industry in the flow chemistry market.

Country Analysis: Global Flow Chemistry Development Hubs

United States: FDA-Driven Acceleration of Continuous Manufacturing and Industrial Flow Chemistry Integration

The United States remains the global epicenter for flow chemistry adoption, propelled largely by the U.S. FDA’s strong regulatory preference for Continuous Manufacturing (CM) across pharmaceutical production. The FDA continues to publish new CM guidance documents and host educational workshops endorsing the transition from batch to continuous processing, positioning flow chemistry as a key enabler of improved drug quality, real-time process control, and resilient supply chains. This regulatory commitment is one of the strongest catalysts in the U.S. market, encouraging pharmaceutical innovators and CDMOs to adopt continuous flow reactors for Active Pharmaceutical Ingredient (API) synthesis and high-value intermediate production. Companies like Corning Incorporated are central to this ecosystem, supplying advanced flow reactor systems specifically engineered for Process Intensification, superior heat transfer, and enhanced reaction safety.

Academic and industrial collaboration is another defining feature of the U.S. landscape. Institutions such as the University of Michigan, supported by major pharmaceutical firms and NSF funding, are advancing complex multi-step reaction sequences using continuous flow platforms—pushing boundaries in photochemistry, organometallic transformations, and telescoped synthesis. Beyond pharmaceuticals, the U.S. petrochemical sector is integrating flow chemistry for high-pressure and high-temperature reactions, particularly catalytic hydrogenation, nitration, and oxidation processes where thermal control, safety, and scalability are critical. With significant investment in automation, integrated control systems, and advanced reactor technologies, the U.S. stands as a global leader in industrial-scale continuous flow adoption across pharmaceuticals, fine chemicals, and petrochemicals.

European Union / Germany: Green Chemistry Regulation and Microreactor Innovation Driving Industrial Flow Adoption

Europe—led by Germany—represents one of the most advanced regions for sustainable flow chemistry adoption, shaped heavily by strict environmental regulations and the EU’s sustainability-driven industrial policy framework. Under the EU Chemicals Strategy for Sustainability (CSS) and the broader European Green Deal, manufacturers are increasingly required to minimize hazardous substances, reduce solvent use, and lower waste (E-factor), making flow chemistry uniquely aligned with compliance requirements. European Contract Development and Manufacturing Organizations (CDMOs) have accelerated investment in continuous flow systems for API manufacturing, improving yield, reducing process steps, and removing inefficient or hazardous intermediates. In 2024, a notable collaboration between a pharmaceutical firm and a reactor vendor reduced a seven-step batch synthesis to three steps using flow chemistry, demonstrating Europe’s strong commercial appetite for continuous processing.

R&D leadership remains strong in the region. BASF and Imperial College London’s SOLVE spinout, launched in July 2024, exemplifies the rising integration of AI, automation, and flow reactor technology to optimize chemical production, especially for pharmaceuticals, fertilizers, and high-value intermediates. German firms such as Ehrfeld Mikrotechnik BTS, a Bayer subsidiary, continue to be world leaders in microreactor systems, offering high-precision small-channel reactors suitable for highly exothermic reactions, gas-liquid transformations, and hazardous chemistries that are unsafe in batch mode. Europe’s focus on process safety, waste reduction, and decarbonization ensures that flow chemistry remains central to its long-term industrial manufacturing strategy.

China: Large-Scale Continuous Processing Expansion in Fine Chemicals and Agrochemical Intermediates

China is rapidly scaling up its adoption of flow chemistry as its fine chemical, pharmaceutical, and agrochemical sectors modernize toward high-volume, high-consistency continuous production. Driven by national environmental reforms and global customer expectations, Chinese manufacturers are shifting away from traditional batch reactors toward continuous synthesis facilities designed for higher throughput, reduced waste, and improved reaction safety. Large state-owned and private chemical firms are rapidly building infrastructure for continuous flow processing to service both domestic and international contracts—particularly in segments where reliability, purity control, and scalability are non-negotiable.

Flow chemistry adoption is also accelerating within the agrochemical sector, where China is a dominant global supplier of intermediates and active ingredients. Continuous flow systems provide precise temperature control and enhanced safety for highly reactive intermediates used in pesticide and herbicide synthesis, enabling better process stability and improved yields. Additionally, Chinese universities and technology providers are investing heavily in the development of proprietary photochemical and electrochemical flow reactor technologies, supporting the synthesis of complex organic molecules used in specialty materials, pharmaceuticals, OLED precursors, and high-value chemicals. As environmental regulations tighten, flow chemistry offers China a pathway to cleaner, safer, and more internationally competitive manufacturing.

India: Government-Backed Flow Chemistry Expansion to Strengthen API Manufacturing and CDMO Competitiveness

India’s growing prominence in global API and pharmaceutical manufacturing is driving strong adoption of flow chemistry, supported by government initiatives and increasing demand from multinational pharmaceutical clients. A major milestone came in August 2024 when the Telangana government signed an MoU with Corning Incorporated to deepen the state’s role in the Flow Chemistry Technology (FCT) hub, developed in collaboration with leading pharmaceutical companies Dr. Reddy’s Laboratories and Laurus Labs, along with the University of Hyderabad. This initiative underscores India’s strategic ambition to integrate continuous manufacturing into its pharmaceutical sector, improving product quality, reducing dependency on batch processing, and bolstering global competitiveness.

Indian Contract Development and Manufacturing Organizations (CDMOs) are investing significantly in commercial-scale continuous flow reactors to secure long-term supply contracts from global pharmaceutical companies that increasingly require CM readiness. At the research level, Indian universities and institutes are actively publishing novel continuous flow routes for widely used drugs such as Olanzapine and Tamoxifen, demonstrating superior yields, enhanced safety, and improved impurity control compared to batch processes. These scientific advances—combined with government-backed infrastructure development—position India as an emerging global hub for industrial flow chemistry adoption across the pharmaceutical and fine chemical value chain.

Competitive Landscape: Global Leaders Advance Continuous Reactor Technologies, Microreactor Design, and Industrial-Scale Flow Processing

The competitive landscape of the Flow Chemistry Market is defined by companies specializing in microreactor engineering, continuous manufacturing platforms, modular flow systems, and advanced reactor materials including borosilicate glass, silicon carbide (SiC), and additive-manufactured components. These companies are shaping the industry through innovations in process intensification, photochemical integration, scale-up reliability, automation, and advanced safety features.

Corning is a global leader in microreactor and flow reactor technology through its Advanced-Flow™ Reactor (AFR) portfolio, spanning G1 lab systems to G4 production units. Its proprietary heart-cell glass modules deliver precise mixing and heat transfer, enabling seamless scale-up from milligrams to tonnes. A major validation occurred in July 2024, when Laurus Labs installed a G4 unit for high-volume API manufacturing, demonstrating AFR’s reliability for industrial continuous production. Corning also expanded its presence in R&D workflows with the June 2024 launch of the Corning Lab Reactor System 2, supporting the rapidly growing field of flow photochemistry.

Vapourtec remains one of the most versatile players in the market with its modular R-Series and E-Series platforms, widely used in academia, pharma, and specialty chemical R&D. Its systems support photochemistry, electrochemistry, and high-pressure reactions. A key milestone was its September 2025 installation at ANSTO, enabling high-value deuterated molecule production. Its April 2025 release of the enhanced ‘BLACK’ pump tube improved solvent compatibility and durability, strengthening reliability for demanding continuous workflows.

Syrris, backed by Asahi Glassplant (AGI), provides the widely adopted Asia Flow Chemistry System, used extensively in research institutions and pharma labs worldwide. The system’s modularity enables seamless transitions between batch and flow for complex synthesis tasks. In January 2025, its use by Gedeon Richter for novel heterocyclic scaffolds underscored its utility in drug discovery and complex reaction development. Syrris maintains a strong academic footprint with over 600 supporting publications.

Chemtrix, supported by Dürr Group, is a pioneer in SiC microreactor technology, offering exceptional thermal conductivity, chemical resistance, and pressure stability. Their Labtrix and Plantrix platforms enable precise temperature control essential for hazardous reactions including strong exotherms and corrosive reagent handling. SiC’s performance advantage—100× higher thermal conductivity than stainless steel—positions Chemtrix as a preferred supplier for demanding industrial flow processes.

ThalesNano is globally recognized for its H-Cube hydrogenation systems, providing safer and faster catalytic reactions under controlled conditions. Its plug-and-play systems eliminate the need for hydrogen cylinders, reducing on-site hazards while enabling rapid parameter exploration. These systems are widely adopted in pharma R&D for API intermediate hydrogenations and reduction chemistry.

V-Squared leverages additive manufacturing to create custom reactors with complex internal geometries—including helical or herringbone channels—that are unachievable through conventional machining. These designs dramatically improve mixing, heat transfer, and reaction uniformity, making them vital for process intensification in niche or highly specialized chemistry applications. Their work supports novel reaction pathways that require tailored reactor design for optimal performance.

Flow Chemistry Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.2 Billion

|

|

Market Size (2035)

|

$15.2 Billion

|

|

Market Growth Rate

|

11.3%

|

|

Segments

|

By Reactor Type (Continuous Stirred Tank Reactor, Plug Flow Reactor, Microreactor, Photochemical Reactor, Electrochemical Reactor, Packed-Bed Reactor), By Application/Reaction Type (Pharmaceutical Synthesis, Chemical Synthesis, Agrochemical Synthesis, Polymer Chemistry, Biotechnology & Life Sciences, Nanoparticle Synthesis, Hazardous Reactions), By End-Use Industry (Pharmaceuticals & Biotechnology, Chemical Industry, Petrochemicals, Academic & Research Institutions, Food & Beverages), By Component/System (Equipment/Hardware, Software & Automation, Process Analytical Technology), By Material Type (Glass/Borosilicate Reactors, Stainless Steel Reactors, Silicon Carbide Reactors, PTFE/PFA/FEP-Coated Reactors)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Corning Incorporated, Biotage AB, AM Technology, Vapourtec Ltd., Syrris Ltd., ThalesNano Inc., Mettler-Toledo International Inc., Chemtrix B.V. (AGI Group), Lonza Group Ltd., CEM Corporation, Uniqsis Ltd., H.E.L Group, Ehrfeld Mikrotechnik BTS

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Flow Chemistry Market Segmentation

By Reactor Type

- Continuous Stirred Tank Reactor (CSTR)

- Plug Flow Reactor (PFR)

- Microreactor

- Photochemical Reactor

- Electrochemical Reactor

- Packed-Bed Reactor

By Application / Reaction Type

- Pharmaceutical Synthesis

- Chemical Synthesis (Fine & Specialty Chemicals)

- Agrochemical Synthesis

- Polymer Chemistry

- Biotechnology & Life Sciences

- Nanoparticle Synthesis

- Hazardous Reactions

By End-Use Industry

- Pharmaceuticals & Biotechnology

- Chemical Industry

- Petrochemicals

- Academic & Research Institutions

- Food & Beverages

By Component / System

- Equipment / Hardware

- Software & Automation

- Process Analytical Technology (PAT)

By Material Type

- Glass / Borosilicate Reactors

- Stainless Steel Reactors

- Silicon Carbide (SiC) Reactors

- PTFE / PFA / FEP Coated Reactors

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies: Key Flow Chemistry Market Players

- Corning Incorporated

- Biotage AB

- AM Technology

- Vapourtec Ltd.

- Syrris Ltd.

- ThalesNano Inc.

- Mettler-Toledo International Inc.

- Chemtrix B.V. (AGI Group)

- Lonza Group Ltd.

- CEM Corporation

- Uniqsis Ltd.

- H.E.L Group

- Ehrfeld Mikrotechnik BTS

*- List not Exhaustive