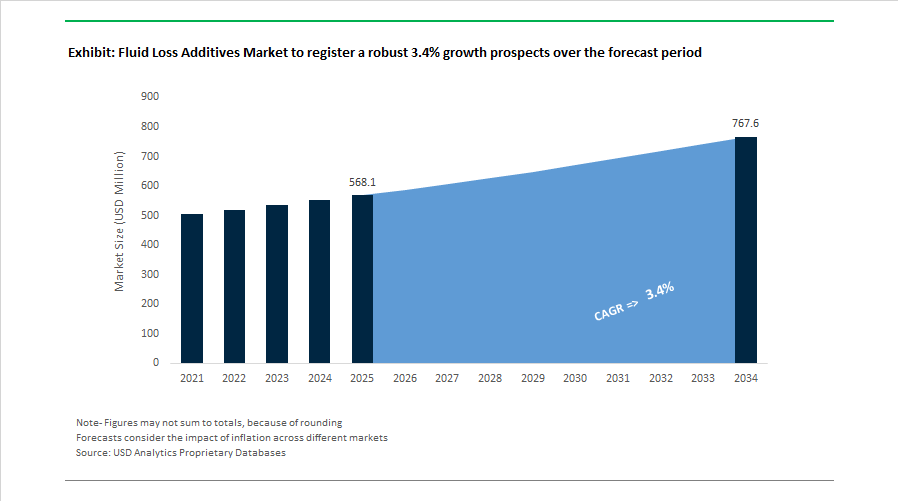

Fluid Loss Additives Market Size 2025–2034: $568.1 Million to $767.6 Million at 3.4% CAGR Supported by HPHT Drilling and Oilfield Chemical Consolidation

The Fluid Loss Additives Market is projected to increase from $568.1 Million in 2025 to $767.6 Million by 2034, registering a CAGR of 3.4%. Market demand is closely linked to global drilling activity, high-pressure high-temperature well development, enhanced oil recovery programs, and the need to minimize filtrate invasion during drilling, completion, and cementing operations. Polyacrylamide-based polymers, crosslinked synthetic additives, nanotechnology-enabled filtrate reducers, and cement slurry fluid loss control agents remain central to wellbore stability, zonal isolation, and formation damage prevention. Investment momentum in the Middle East, Latin America, and offshore deep-water basins continues to sustain additive consumption despite volatility in North American land markets.

In November 2025, Clariant Oil Services received the Petrobras Best Supplier Award in the Chemical Products category, recognizing its performance in supplying specialized fluid loss modifiers for Brazil’s pre-salt deep-water drilling projects. In October 2025, SNF Group entered into a definitive agreement to acquire Syensqo’s Oil & Gas business for €135 million, with closing expected in early 2026. This acquisition strengthens SNF’s global portfolio of polyacrylamide-based fluid loss additives, friction reducers, and stimulation chemicals. During 2025, SNF also announced expansion of its Oman manufacturing hub to increase regional production of water-soluble polymers for enhanced oil recovery and drilling fluid systems. In September 2025, SLB announced the acquisition of RESMAN Energy Technology, integrating wireless tracer diagnostics with chemical fluid loss control systems to enable real-time monitoring of filtrate invasion during completion operations. Throughout 2025, Baker Hughes emphasized its TEKPLUG™ XL and XL HD fluid loss control pills, designed as solids-free crosslinked polymer systems that provide temporary formation sealing while reducing completion costs.

Operational deployment expanded in 2024 and early 2025. Halliburton reported increased utilization of fluid loss control and cementing technologies in the Middle East and Argentina’s Vaca Muerta shale during its year-end 2024 and early 2025 disclosures, offsetting weaker North American land demand. Solenis finalized its merger with NCH Corporation during 2024, integrating synthetic polymer-based fluid loss agents with broader industrial and oilfield water treatment technologies. In early 2024, Kemira completed the divestment of its Oil & Gas portfolio, including fluid loss control products, to Sterling Specialty Chemicals, marking its transition toward a water-focused chemical strategy.

Product innovation momentum dates back to 2023. In August 2023, Italmatch Chemicals introduced Aubin CFL-600, a high-performance cement slurry fluid loss additive designed to enhance zonal isolation and reduce fluid migration in complex wellbore geometries. In late 2022 and early 2023, NanoMalaysia launched Synergy 10AS Nano, a nanoparticle-based additive engineered for HPHT drilling environments, forming thinner and more resilient filter cakes compared to conventional starch or cellulose-based systems.

Trends and Opportunities in the Fluid Loss Additives Market

Proliferation of HTHP-Stable Synthetic Terpolymers for Ultra Deepwater Drilling

Ultra deepwater projects are redefining performance benchmarks for drilling fluid systems, particularly fluid loss control under extreme pressure and temperature. The commissioning of the Anchor project in the U.S. Gulf of Mexico by Chevron and TotalEnergies in August 2024 marked a turning point for the industry. With reservoir conditions approaching 20,000 psi and temperatures above 175°C, conventional cellulose and PAC-based additives exhibit thermal thinning and filtration failure.

This operating envelope has accelerated adoption of AMPS-based synthetic terpolymers, which retain molecular stability and fluid loss control under prolonged thermal aging. These polymers are now being specified as baseline components in deepwater synthetic-based fluids rather than optional enhancements. Their higher cost is offset by reduced non-productive time and lower risks of differential sticking and wellbore instability.

Nanotechnology is further reinforcing this trend. Research published in ACS Omega in April 2024 showed that incorporating SiO₂ and g-C₃N₄ nanoparticles at concentrations as low as 0.5 lb/bbl reduced HTHP fluid loss by over 87% after thermal aging. These hybrid systems form ultra thin, mechanically resilient filter cakes that outperform polymer-only systems, particularly in high-angle and extended reach wells.

The strategic importance of this segment is underscored by developments in Asia. CNOOC commenced production at China’s first deepwater HTHP gas field in September 2024, utilizing advanced synthetic-based fluids and specialized fluid loss additives to support a peak facility capacity of 162 MMcfgd. This confirms that deepwater HTHP drilling is no longer regionally isolated and represents a global growth engine for premium additives.

Regulatory-Driven Shift Toward OSPAR-Compliant and Biodegradable Polymers

Environmental regulation is reshaping the offshore fluid loss additives landscape, particularly in the North Sea and North Atlantic. Under OSPAR Recommendation 2019/02, which entered a critical enforcement and monitoring phase in 2025, operators are required to substitute chemicals with persistence or bioaccumulation concerns. This has directly impacted the use of traditional synthetic polymers in offshore drilling fluids.

As a result, adoption of biopolymers such as scleroglucan and diutan gum has increased by approximately 20% year over year. These materials provide strong fluid loss control and suspension properties in high salinity environments while delivering near zero aquatic toxicity. Their ability to function in weighted fluids has made them viable replacements rather than niche alternatives.

In the United Kingdom, updated offshore chemical discharge guidance issued in December 2025 reinforced the requirement for Best Available Technology compliance. This has shifted R&D investment toward modified starches and carboxymethyl cellulose derivatives that achieve over 90% biodegradability within 28 days without sacrificing filtration performance.

Service majors including Baker Hughes and SLB have integrated low carbon drilling fluid strategies into their 2025 sustainability roadmaps. Biomass balanced polymers are now being deployed to reduce Scope 3 emissions associated with well construction by up to 30%, making environmental compliance a commercial differentiator rather than a cost burden.

Specialized Additives for Geopolymer and Low-CO₂ Cement Systems

The transition toward low carbon well construction is creating a new demand profile for fluid loss additives compatible with alternative cement chemistries. Geopolymer, alkali activated slag, and other supplementary cementitious material systems exhibit radically different rheology and pH conditions compared to traditional Class G cement, rendering many legacy additives ineffective.

In April 2025, Oil States introduced GeoLok technology for high temperature geothermal wells. These applications require fluid loss additives that can withstand corrosive fluids and elevated temperatures while supporting rapid setting times. Zirconium crosslinked and latex-based FLAs are emerging as preferred solutions in these systems, as they provide filtration control without interfering with geopolymer hydration kinetics.

Carbon capture and storage projects are reinforcing this opportunity. As ExxonMobil and ADNOC scale CCS developments with multi million tonne annual capacity targets announced in 2025, long term zonal isolation has become a critical risk variable. Fluid loss additives used in CO₂-resistant cement systems must remain stable in acidic environments to prevent microannulus formation over decades of storage.

The rise of alkali activated slag cements has also opened demand for FLAs capable of operating in pH environments above 12, where standard cellulose-based products rapidly degrade. Suppliers that can deliver chemical stability across these extreme conditions are positioned to capture early mover advantage in sustainable well construction.

Ultra-Low-Molecular-Weight FLAs for Unconventional and Fracturing Operations

In unconventional reservoirs, fluid loss control requirements differ fundamentally from those in drilling and cementing. Operators increasingly require additives that reduce leak-off without impairing fracture conductivity or proppant pack permeability.

Slickwater fracturing remains dominant in shale basins due to its low cost and high pump rates, but it is inherently prone to excessive fluid loss. Technical reviews in late 2025 show that nanoparticle-based and ultra-low-molecular-weight FLAs can reduce leak-off by 45 to 60%, improving fracture extension efficiency and proppant placement without increasing fluid viscosity.

These systems are gaining traction in enhanced oil recovery applications as well. In the Permian Basin, use of polyacrylamide-based fluid loss control agents in EOR projects increased sharply in 2025. By sealing thief zones and improving sweep efficiency, these additives are contributing to incremental recovery factor gains of 3 to 5%, a material uplift in mature unconventional assets.

Operator specifications are also tightening around damage mitigation. Major shale producers such as EOG Resources and Occidental are now standardizing the use of enzyme-triggered breakers in conjunction with fluid loss additives. This ensures that polymers degrade cleanly after stimulation, eliminating residual films that could compromise long term well productivity.

Fluid Loss Additives Market Share and Segmentation Insights

Synthetic Polymer-Based Fluid Loss Additives Lead High-Temperature Drilling Fluid Technologies

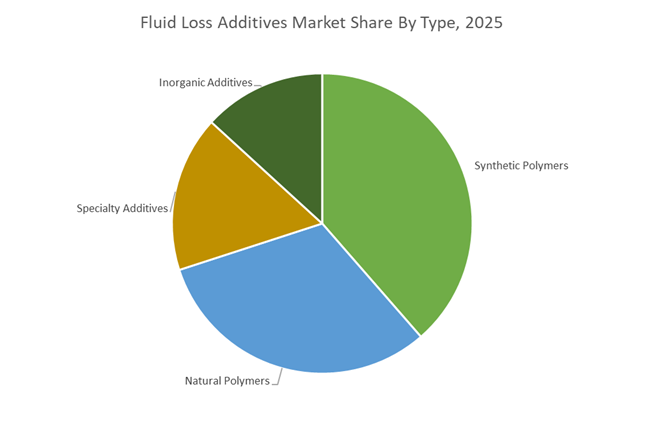

Synthetic Polymers accounted for 38.60% of the Fluid Loss Additives Market share in 2025, making them the dominant additive type used in advanced drilling fluid systems. These polymers—including polyacrylamides, polyacrylates, and vinyl-based copolymers—are widely used in drilling mud formulations to control filtration loss and maintain wellbore stability during drilling operations. Compared with natural polymer alternatives, synthetic polymers provide superior thermal stability, controlled molecular weight architecture, and resistance to bacterial degradation, enabling reliable performance in challenging drilling environments such as deepwater wells, extended-reach drilling projects, and high-temperature formations. In 2025, technological development within the sector is centered on thermoviscosifying polymer systems, which represent a major innovation in drilling fluid chemistry. These next-generation polymers exhibit the ability to increase viscosity at elevated temperatures, improving filtration control and maintaining fluid stability in high-temperature, high-pressure (HTHP) drilling conditions where conventional additives typically degrade. This advancement has significantly expanded the operational envelope for drilling fluids, enabling exploration and well construction in ultra-deep hydrocarbon reservoirs and emerging geothermal energy resources. As drilling projects increasingly move into deeper and hotter geological formations, synthetic polymer additives continue to strengthen their leadership position in the global fluid loss additives market.

Oil and Gas Extraction Drives the Majority of Global Fluid Loss Additive Consumption

Oil and Gas Extraction represented 76.80% of the Fluid Loss Additives Market share in 2025, reflecting the sector’s dominant role in global drilling and well construction activities. Fluid loss additives are essential components of drilling mud systems, where they prevent excessive filtration of drilling fluids into permeable rock formations while maintaining wellbore pressure stability and minimizing formation damage. The extensive scale of onshore, offshore, and deepwater drilling operations across major hydrocarbon-producing regions ensures consistent demand for high-performance fluid loss control chemicals. In 2025, the oil and gas industry is increasingly focused on high-temperature, high-pressure (HTHP) reservoir development, driven by the gradual depletion of easily accessible conventional resources. Modern exploration programs are targeting ultra-deep reservoirs where temperatures exceed 200°C and formation pressures are extremely high, conditions that quickly degrade conventional drilling fluid additives. To maintain drilling efficiency under these extreme environments, operators are adopting advanced synthetic polymer systems and specialty fluid loss additives designed specifically for HTHP wells. These applications require higher additive concentrations and more complex drilling fluid formulations, resulting in disproportionately strong demand growth within this segment and reinforcing oil and gas extraction as the primary end-user industry in the global fluid loss additives market.

Competitive Landscape in Fluid Loss Additives Market

SLB Integrates Digital Oilfield Platforms with Low-Carbon Fluid Loss Technologies

SLB has repositioned itself as a global energy technology company, integrating fluid loss additives with digital drilling ecosystems and carbon-neutral well construction strategies. Its EcoShield™ geopolymer cement-free system delivers advanced fluid loss control while reducing embodied carbon by up to 85% compared to traditional Portland cement systems. In 2026, SLB introduced Drilling Mud Virtualization, an AI-driven real-time monitoring system that predicts and mitigates fluid loss events before they occur, reducing chemical overuse by an estimated 22%. Through the DELFI cognitive E&P ecosystem, fluid chemistry data is integrated with autonomous drilling systems to optimize rate of penetration and minimize formation damage. Between 2024 and 2025, SLB reported a ten-fold increase in volumes of sustainable chemical technologies pumped, establishing a benchmark in low-water-usage drilling operations. This convergence of digital analytics and low-carbon fluid loss additives reinforces SLB’s leadership in advanced well construction solutions.

Halliburton Leads Completion Fluid Loss Control and Reversible Crosslinking Systems

Halliburton maintains a dominant position in completions and cementing services where zonal isolation and formation protection depend on effective fluid loss control. Its LO-Gard® service portfolio includes solids-free, low-viscosity additives engineered to minimize completion fluid losses during overbalanced workover and intervention operations. The company reported $22.9 billion in total revenue for the 2024 to 2025 fiscal year, reflecting its global deployment capacity in specialty chemical systems. Halliburton differentiates through reversible crosslinking technologies that provide temporary high-efficiency fluid loss control and can be fully reversed to prevent formation damage during production. Its Custom Chemistry teams collaborate directly with operators to design tailored fluid loss pills that address mineralogical challenges in unconventional shale reservoirs. This integration of bespoke chemical formulation with large-scale field execution strengthens Halliburton’s competitive position in high-performance fluid loss additives.

BASF Expands Biomass-Balanced Polymer Feedstocks for Drilling Fluid Additives

BASF serves as a critical upstream supplier of synthetic polymers, including polyacrylates and AMPS-based copolymers used in fluid loss control systems. For 2026, BASF forecasts EBITDA between €6.2 billion and €7.0 billion, with its Chemicals and Nutrition and Care segments contributing to earnings growth. In early 2026, the company introduced biomass-balanced polymer systems in North America that reduce drilling fluid carbon footprint by up to 30% without sacrificing performance stability. The commissioning of the Zhanjiang Verbund site in late 2025 significantly expanded production capacity for specialty surfactants and polymers serving the Asian oil and gas market. Under its Winning Ways strategy, BASF is accelerating the adoption of circular feedstocks to replace fossil-based inputs within the fluid loss additive value chain. This upstream integration and sustainability focus enhance supply security and environmental compliance for global drilling fluid manufacturers.

Clariant Focuses on Thermally Stable Additives for Geothermal and HTHP Wells

Clariant has strengthened its specialty chemical positioning, achieving an EBITDA margin improvement of 180 basis points to 17.8% as of early 2026. Its Hostadrill® and Tylose® product lines provide thermally stable fluid loss additives for water-based drilling muds operating in geothermal and high temperature high pressure environments exceeding 200°C. In 2025, Clariant reported CHF 4.152 billion in sales, with innovation-driven products accounting for nearly 19% of revenue. The company’s portfolio pruning strategy has shifted focus toward natural and bio-based additives, including glucamide-derived modifiers that enhance environmental compatibility. Clariant’s dominance in offshore and geothermal drilling markets stems from its ability to maintain stable rheology and fluid integrity under extreme thermal stress. This specialization in high-performance fluid loss control chemistry reinforces its niche leadership in demanding well conditions.

Baker Hughes Integrates Wellbore Strengthening with Digital Monitoring Platforms

Baker Hughes positions itself as an integrated energy technology provider, combining chemical fluid loss additives with subsea engineering and digital diagnostics. Its CHEK-LOSS™ and BRIDGEFORM™ systems address lost circulation and structural integrity challenges in depleted or fractured formations. The AQUA-DRILL water-based system delivers oil-based mud performance while complying with strict offshore discharge regulations through eco-friendly fluid loss controllers. Baker Hughes is expanding its Net-Zero Future portfolio into carbon capture and storage applications, where maintaining CO2 injection well integrity requires advanced fluid loss management. Through the Bently Nevada digital monitoring platform, operators gain real-time fluid health diagnostics to prevent costly lost circulation events. This convergence of chemical systems and digital monitoring enhances operational reliability in complex offshore and CCUS projects.

Newpark Resources Strengthens Pure-Play Leadership in Wellbore Strengthening

Newpark Resources operates as a pure-play drilling fluids specialist, concentrating exclusively on fluid chemistry and wellbore performance. Its FIX™ Series, including PreFIX™, ProppFIX™, and FracFIX™, is designed to prevent and remediate lost circulation in naturally fractured and induced fracture reservoirs. The company demonstrated field performance by restoring full fluid returns in the Nordeste Tupi Field in Brazil and in deepwater wells near Lake Washington. Newpark’s Kronos™ non-aqueous system is widely regarded as a benchmark flat-rheology synthetic-based fluid for deepwater operations. Its strategic approach centers on reducing non-productive time by up to 50% in complex intervals, directly improving well economics in high-cost offshore and unconventional projects. By aligning sustainability with operational efficiency, Newpark reinforces its specialization in advanced fluid loss additive technologies.

Saudi Arabia: Unconventional Gas Expansion Driving High-Temperature Fluid Loss Additives

Saudi Arabia is emerging as one of the most structurally important markets for fluid loss additives, underpinned by the Kingdom’s accelerated upstream expansion and deep commitment to unconventional gas. Saudi Aramco is executing a USD 90 billion project pipeline across 2025–2026, comprising 99 active developments, with a dominant concentration in oil, gas, and petrochemicals. This scale of activity is directly translating into sustained procurement of high-temperature stable fluid loss additives, particularly for deep and extended-reach wells where filtrate control under extreme pressure differentials is operationally critical. The emphasis on sour gas and tight formations has increased reliance on synthetic polymers that retain rheological stability beyond conventional temperature thresholds.

The Jafurah gas field marks a structural inflection point. The USD 11 billion agreement finalized in late 2025 and the commencement of Phase One production have elevated demand for acrylamide-based and hybrid synthetic fluid loss additives engineered for complex non-associated gas reservoirs. In parallel, the long-term unconventional gas services contract awarded to SLB has embedded digital diagnostics and high-fidelity drilling fluid systems into Saudi shale operations. This integration is shifting the local market away from commodity-grade additives toward performance-certified systems optimized for real-time fluid loss management, reinforcing Saudi Arabia’s position as a premium-demand market rather than a volume-driven one.

United States: Sustainability, Nanotechnology, and Specialty Fluids Redefining Additive Demand

The United States fluid loss additives landscape is increasingly shaped by sustainability-driven supply chain restructuring and technology-led differentiation. The modernization of Solvay’s Green River facility in Wyoming, following the phase-out of coal and continued upgrades through 2025, has strategic implications for drilling fluid chemistry. As soda ash remains a key precursor in water treatment and mud conditioning systems, cleaner production routes are aligning fluid loss additive sourcing with ESG-compliant drilling programs, particularly in regulated shale basins.

Technological differentiation is accelerating through nanotechnology. In 2025, Halliburton expanded deployment of its BaraHib Nano water-based fluid systems, enabling operators to achieve fluid loss control comparable to non-aqueous systems while maintaining environmental compliance. This is particularly relevant in environmentally sensitive shale regions where regulators and operators are jointly prioritizing reduced formation damage and improved wellbore stability. Additionally, the integration of HydroLite Operating LLC into AES Drilling Fluids has strengthened the U.S. market for specialty fluid loss additives designed for low-pressure and high-porosity reservoirs, especially across the Permian Basin. Collectively, these developments are shifting demand toward application-specific, high-margin additive formulations rather than standardized products.

China: Policy-Driven Shift Toward High-End and Digitally Integrated Fluid Loss Solutions

China’s fluid loss additives market is undergoing a policy-led transformation aligned with national petrochemical upgrading objectives. The Ministry of Industry and Information Technology has set a clear mandate for 2025–2026 to drive over 5% annual growth in petrochemical value addition, prioritizing high-end supply and fine chemical innovation. This policy environment is accelerating domestic development of advanced polyolefin-based and synthetic polymer fluid loss additives tailored for offshore and complex onshore drilling conditions, reducing dependence on imported formulations.

Structural capacity expansion further reinforces this trajectory. The Huajin Aramco Petrochemical Company mega-complex in Panjin, scheduled for commissioning in 2026, will localize production of ethylene and paraxylene, both critical feedstocks for synthetic fluid loss additive manufacturing. Beyond materials, Chinese producers are being guided to transition from standalone chemical sales to integrated solutions. Under the MIIT work plan, the integration of AI-driven monitoring platforms with drilling fluid systems is gaining traction, enabling real-time fluid loss diagnostics in offshore drilling environments. This convergence of policy, capacity, and digitalization positions China as a future exporter of engineered fluid loss solutions rather than a purely domestic consumer.

India: Regulatory Reform and Bio-Based Innovation Reshaping Demand Patterns

India’s fluid loss additives market is being reshaped by regulatory reform and targeted policy incentives rather than pure drilling volume expansion. The Oilfields (Regulation and Development) Amendment Act, 2025 has streamlined upstream licensing under the Hydrocarbon Exploration Licensing Policy, resulting in the award of 172 blocks and committed investments exceeding USD 4.36 billion. This regulatory clarity has accelerated demand for localized cementing and drilling fluid additives, particularly fluid loss control agents adapted to India’s diverse geological profiles.

Exploration intensity has further increased under Mission Anveshan, with government-funded seismic and deep-drilling programs extending through 2025. These programs are favoring specialized non-ionic surfactants and fluid loss additives optimized for enhanced oil recovery applications. In parallel, India’s BioE3 Policy has introduced a structural shift by incentivizing non-grain bio-based materials. This has catalyzed early-stage development of biodegradable, starch-based fluid loss additives for municipal water-well drilling and environmentally sensitive applications, positioning India as a testbed for sustainable alternatives rather than a follower market.

Brazil: Offshore Complexity Driving Premium Fluid Loss Additive Adoption

Brazil represents one of the most technically demanding environments for fluid loss additives, driven by offshore and ultra-deepwater exploration. In January 2025, Halliburton secured a three-year integrated drilling contract covering multiple offshore fields, requiring solids-free and low-viscosity fluid systems designed to minimize completion-stage fluid losses. These requirements are reinforcing demand for advanced additive chemistries capable of maintaining filtrate control under dynamic pressure and temperature conditions.

Supplier differentiation is becoming increasingly visible. Clariant Oil Services received the 2025 Petrobras Best Suppliers Award, recognizing its performance in high-pressure, high-temperature environments and validating the commercial value of innovation-led fluid loss additives. Looking ahead, pending licenses for Brazil’s Equatorial Margin are prompting service providers to pre-position advanced cementing additives and next-generation systems capable of handling ultra-deepwater challenges. This forward deployment underscores Brazil’s role as a premium market where operational complexity directly translates into higher specification and value per unit of fluid loss additives.

Summary of Country-Level Strategic Drivers in the Fluid Loss Additives Market

Fluid Loss Additives Market County Level Snapshot

|

Country

|

Key Strategic Driver

|

Implication for Fluid Loss Additives

|

|

Saudi Arabia

|

Unconventional gas and deep-well expansion

|

High-temperature stable and synthetic polymer demand

|

|

United States

|

Sustainability upgrades and nanotechnology

|

Shift toward water-based, nano-enabled additives

|

|

China

|

Policy-led petrochemical upgrading

|

Growth of high-end, AI-integrated additive solutions

|

|

India

|

Licensing reform and bio-based policies

|

Rising demand for localized and biodegradable additives

|

|

Brazil

|

Offshore and ultra-deepwater exploration

|

Premium-grade, HPHT fluid loss control systems

|

Fluid Loss Additives Market Report Scope

Fluid Loss Additives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$568.1 Million

|

|

Market Size (2034)

|

$767.6 Million

|

|

Market Growth Rate

|

3.4%

|

|

Segments

|

By Type (Natural Polymers, Synthetic Polymers, Inorganic Additives, Specialty Additives), By Application (Drilling Fluids, Well Cementing, Completion and Workover Fluids, Fracturing Fluids), By End-User Industry (Oil and Gas Extraction, Geothermal Drilling, Mining and Mineral Exploration, Construction, Water Well Drilling)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Halliburton Company, SLB, Baker Hughes Company, BASF SE, Clariant AG, Solvay S.A., Solenis, Newpark Resources Inc., Chevron Phillips Chemical Company, Global Drilling Fluids and Chemicals Limited, SNF Group, Kemira Oyj, Tetra Technologies, Inc., Innospec Inc., Auburn Manufacturing, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fluid Loss Additives Market Segmentation

By Type

- Natural Polymers

- Synthetic Polymers

- Inorganic Additives

- Specialty Additives

By Application

- Drilling Fluids

- Well Cementing

- Completion and Workover Fluids

- Fracturing Fluids

By End-User Industry

- Oil and Gas Extraction

- Geothermal Drilling

- Mining and Mineral Exploration

- Construction

- Water Well Drilling

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Fluid Loss Additives Industry

- Halliburton Company

- SLB

- Baker Hughes Company

- BASF SE

- Clariant AG

- Solvay S.A.

- Solenis

- Newpark Resources Inc.

- Chevron Phillips Chemical Company

- Global Drilling Fluids and Chemicals Limited

- SNF Group

- Kemira Oyj

- Tetra Technologies, Inc.

- Innospec Inc.

- Auburn Manufacturing, Inc.

- *- List not Exhaustive

*- List not Exhaustive