Fluoropolymer Coating Market Growth Driven by EV Battery Demand, Semiconductor Expansion, and High-Durability Coating Systems

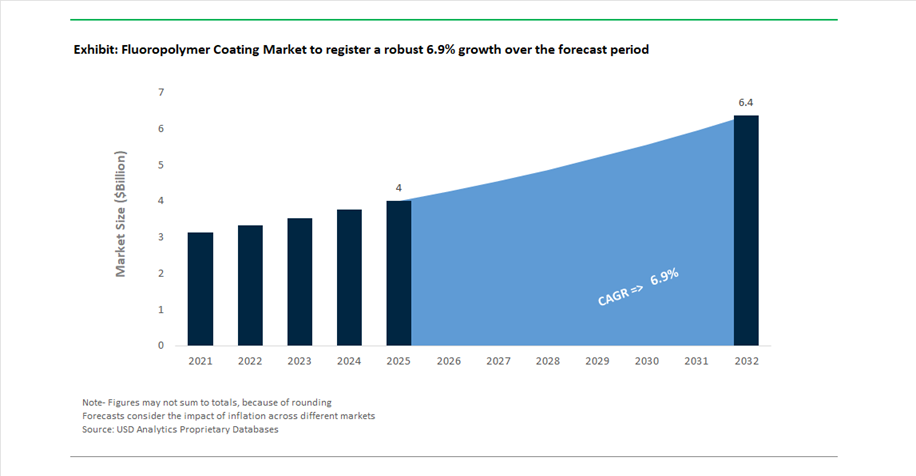

The global Fluoropolymer Coating Market was valued at USD 4 billion in 2025 and is projected to grow at a CAGR of 6.9% between 2025 and 2032, reaching USD 6.4 billion by 2032. This strong growth trajectory is driven by rising demand for high-performance, chemically inert, and ultra-durable coatings across automotive, electronics, energy, and industrial applications.

Fluoropolymer coatings—including PVDF, PTFE, FEP, and FEVE-based systems—are critical in environments requiring exceptional corrosion resistance, UV stability, non-stick properties, and long service life. A key structural driver is the rapid expansion of electric vehicle (EV) manufacturing, where fluoropolymer coatings are used in battery components, insulation layers, and protective systems to ensure thermal stability and chemical resistance under extreme operating conditions.

Another major growth catalyst is the global surge in semiconductor fabrication capacity, particularly for advanced nodes such as 2nm and 3nm. Fluoropolymer coatings are essential for high-purity processing environments, including chemical handling systems and wafer fabrication equipment, where contamination control is critical. Additionally, the expansion of renewable energy infrastructure, especially hydrogen production and solar technologies, is creating new demand for fluoropolymer-based protective coatings.

Sustainability and regulatory compliance are also shaping the market. The industry is transitioning toward PFAS-conscious and surfactant-free production technologies, enabling manufacturers to meet stringent environmental regulations without compromising performance. Furthermore, innovations in low-energy curing and high-efficiency coating systems are reducing the environmental footprint of fluoropolymer applications.

Laser-Curing Breakthroughs, and Fluorospecialty Expansion Reshape Market Dynamics

The fluoropolymer coating market is undergoing a major structural transformation driven by industry consolidation, advanced manufacturing technologies, and strategic portfolio realignment. In November 2025, AkzoNobel and Axalta Coating Systems announced a $25 billion merger, combining their architectural and industrial fluoropolymer portfolios to create a dominant global player with extensive R&D capabilities focused on next-generation high-durability coatings.

Technological innovation in curing processes is redefining production efficiency. In March 2026, PPG Industries partnered with IPG Photonics to commercialize laser-based powder curing, a breakthrough for fluoropolymer coatings such as PVDF and FEVE. This technology enables near-instantaneous cross-linking while reducing energy consumption by up to 90%, significantly improving sustainability and enabling application on heat-sensitive substrates.

Demand from EV and energy sectors is accelerating growth in fluorospecialties. In February 2026, Arkema reported 16% year-over-year growth in its fluorospecialty segment, driven by strong demand for PVDF coatings in EV batteries and expanded production capacity in the United States and Asia.

Sustainability-driven innovation is reshaping production methods. In August 2024, AGC Inc. introduced a surfactant-free fluoropolymer manufacturing process, enabling the production of high-performance coatings without traditional PFAS-related chemicals. Complementing this, in April 2026, Syensqo (formerly Solvay) completed the phase-out of fluorosurfactants at its Italian facility, aligning with EU Green Deal requirements.

Expansion into renewable energy infrastructure is creating new growth avenues. AGC Inc. is investing heavily in fluoropolymer-based membranes and coatings for hydrogen production, with new facilities scheduled to begin operations in June 2026, supporting the global expansion of green hydrogen technologies.

Regional expansion strategies are strengthening supply chains. In March 2026, Daikin Industries established a high-purity fluoropolymer coatings unit in India, targeting semiconductor and electronics manufacturing hubs that require zero-leaching, chemically inert surfaces.

Strategic funding and commercial agreements are also shaping market positioning. In November 2025, The Chemours Company secured $10 million in grant funding to develop advanced fluoropolymer coating technologies for critical mineral processing. Additionally, in January 2026, PPG Industries became the exclusive supplier for Quality Collision Group, reinforcing the role of fluoropolymer coatings in premium automotive refinish applications.

Fluoropolymer Coating Market Share 2025: Spray Coating and Service Applicators Drive Industry Adoption

Coating Process Insights: Spray Coating Leads with Versatility and Precision Application

The spray coating segment dominates the fluoropolymer coating market with a 40% market share in 2025, driven by its unmatched versatility and precision across industrial and architectural applications. Spray techniques such as airless, HVLP (high-volume low-pressure), and electrostatic spraying are widely used for applying PTFE, PFA, FEP, and PVDF coatings on complex substrates including molds, valves, rollers, and architectural metal components. This method enables both factory-based and on-site coating applications, making it ideal for diverse industries ranging from chemical processing to construction. A key advantage is its ability to deliver controlled thin-film thickness, typically 15–50 microns for PVDF architectural coatings and 5–25 microns for non-stick cookware primers, ensuring consistent gloss, corrosion resistance, and release properties. As demand for high-performance, precision-engineered fluoropolymer coatings grows, spray coating will continue to lead due to its flexibility and efficiency.

Distribution Channel Insights: Service-Based Applicators Dominate with Specialized Coating Expertise

The service-based applicators segment holds the largest 45% share in the fluoropolymer coating market in 2025, reflecting the growing trend of outsourcing specialized coating processes. Many industries, including semiconductor manufacturing, chemical processing, and food production, rely on licensed applicators equipped with advanced infrastructure such as curing ovens, grit blasting systems, and certified spray booths to apply fluoropolymer coatings. This approach eliminates the need for costly in-house investments while ensuring high-quality results. Additionally, leading manufacturers such as Chemours, Daikin, and AGC authorize specific applicators, providing customers with warranty-backed performance, adhesion reliability, and full traceability of coating processes. This level of quality assurance is critical in high-performance applications where coating failure is not an option. As industries prioritize efficiency, compliance, and performance guarantees, service-based applicators will remain a key distribution channel in the fluoropolymer coating market.

Fluoropolymer Coating Market Competitive Landscape: PFAS Transition, Semiconductor Demand, and High-Performance Innovation Driving Market Leaders

The fluoropolymer coating market is dominated by global chemical leaders advancing PFAS-free technologies, semiconductor-grade purity, and sustainable high-performance coatings. Companies are leveraging capacity expansion, digital integration, and advanced resin innovation to address demand across EV batteries, data centers, aerospace, and infrastructure applications.

Chemours strengthens fluoropolymer leadership through capacity expansion and renewable coating innovation

The Chemours Company is reinforcing its dominance in the fluoropolymer coatings market through strategic capacity expansion and sustainable product innovation. In 2026, it commissioned upgraded FEP and PFA production lines, increasing output by 15% to support AI-driven data center cooling and high-frequency communication applications. The company has successfully scaled Teflon EcoElite™, a renewably sourced water repellent containing 60% plant-based materials that outperforms silicone coatings by a factor of 7-to-1. With 85% global B2B brand awareness, Chemours maintains strong market control through its Licensed Coater program, ensuring ASTM-certified application quality. Its vertically integrated fluorine value chain enables production of PTFE micro-powders using non-fluorinated surfactants, ensuring compliance with 2026 REACH regulations. This integration of sustainability, scale, and brand strength solidifies Chemours’ leadership in advanced fluoropolymer coatings.

Daikin accelerates semiconductor-grade fluoropolymer coatings with PFAS-free processing innovation

Daikin Industries is expanding its competitive position in fluoropolymer coatings through semiconductor-focused growth and PFAS-free material innovation. In March 2026, the company established Daikin Chemical India Pvt. Ltd. in Gurugram to capture rapid growth in India’s semiconductor and EV battery sectors under the “Make in India” initiative. It introduced a rapid-cure FEP powder coating that reduces industrial oven energy consumption by 18%, targeting large-scale chemical processing applications. Daikin has also commercialized high-purity Neoflon™ PFA coatings engineered with sub-ppb metal extractables, enabling contamination-free production in advanced 3 nm chip fabrication. The company is transitioning toward DAIKIN PPA DAHC-101, a 100% PFAS-free processing aid that maintains traditional fluoropolymer throughput. This strategic combination of localization, innovation, and regulatory alignment strengthens Daikin’s leadership in high-performance coatings.

AGC drives high-margin fluoropolymer growth through advanced architectural and 6G coating technologies

AGC Inc. is strengthening its position in the fluoropolymer coatings market through high-margin product innovation and advanced communication materials. Under its AGC plus-2026 strategy, the company is targeting ¥100 billion in operating profit, driven by its LUMIFLON™ FEVE resin segment. Its Fluon® ETFE and FEP films have been enhanced for 6G infrastructure, achieving a dissipation factor below 0.0005 to ensure high-speed signal integrity in satellite communications. The LUMIFLON™ series remains a global benchmark for architectural coatings, offering over 30 years of UV resistance and weatherability for infrastructure such as bridges and airports. AGC’s CYTOP™ technology provides over 95% transparency for thin-film coatings used in optical and medical applications. This diversified, high-performance portfolio positions AGC as a leader in both industrial and specialty fluoropolymer coatings.

Arkema expands PVDF leadership with EV battery integration and circular material innovation

Arkema S.A. is reinforcing its leadership in fluoropolymer coatings through PVDF capacity expansion and circular economy solutions. In Q2 2026, the company commenced operations of a new PVDF production line in Kentucky, supporting the growing North American EV battery supply chain. It also announced a 20% expansion of its Changshu facility in China, further solidifying its position as the world’s largest PVDF producer. Arkema is scaling its Elium® resin system, a recyclable thermoplastic solution that integrates fluoropolymer additives to enhance UV stability in wind energy composites. Additionally, the company is leveraging its 100% bio-based Rilsan® Polyamide 11 alongside Kynar® coatings to create sustainable “Green-Safety” solutions for automotive thermal management. This integrated approach strengthens Arkema’s position in next-generation fluoropolymer applications.

PPG advances PFAS-free fluoropolymer coatings with digital integration and high-durability systems

PPG Industries is enhancing its competitive position in fluoropolymer coatings through PFAS-free innovation and digital ecosystem integration. At Ambiente 2026, the company introduced Fusion Pro, a high-gloss non-stick coating free from PFAS substances, capable of exceeding 50,000 wet abrasion cycles. Its PPG ECLIPSE® PTFE coatings deliver up to 60,000 release cycles, meeting the demands of commercial and gourmet kitchen applications. Following the divestiture of its architectural retail business, PPG has refocused R&D on industrial OEM and aerospace coatings, emphasizing high-performance Xylan® FEP/PTFE systems. The integration of its Whitford Xylan® portfolio into the PPG LINQ™ platform enables real-time monitoring of coating thickness and curing uniformity. This convergence of durability, sustainability, and digitalization reinforces PPG’s leadership in advanced fluoropolymer coatings.

Syensqo captures PFAS transition demand with high-performance coatings and specialty additive innovation

Syensqo is emerging as a key player in the fluoropolymer coatings market by capitalizing on regulatory-driven demand and advanced material innovation. In 2026, the company is executing significant capacity investments to fill the market gap created by 3M’s exit from PFAS manufacturing. Its Addibond™ 106 additive enhances adhesion and corrosion resistance (C4 protection), strengthening performance in high-purity industrial environments. Syensqo dominates the healthcare and medical FEP coatings segment through its Hyflon® and Algoflon® product lines, offering superior lubricity for catheters and surgical tools. The company also maintains global leadership in fluoropolymer membranes for hydrogen fuel cells and water filtration, where chemical and thermal stability are critical. This strategic positioning enables Syensqo to lead in next-generation, sustainable fluoropolymer coating solutions.

China Fluoropolymer Coating Market: Scaling High-Purity Production and EV Battery Integration

China dominates the global fluoropolymer coating market, leveraging its scale to transition toward high-value applications in lithium-ion batteries, semiconductors, and renewable energy systems. The country’s aggressive expansion in fluoropolymer production is evident in strategic capacity increases, such as Arkema’s Changshu facility, which significantly boosted output to meet surging demand for PVDF binder coatings in EV battery manufacturing.

Domestic players like Dongyue Group are also strengthening their position by expanding purity-grade PFA and FEP coatings, catering to the fast-growing semiconductor equipment segment. Government-backed initiatives across solar hubs in Ningxia and Xinjiang are mandating the use of fluoropolymer backsheet coatings to ensure long-term durability and performance under extreme UV exposure, reinforcing China’s leadership in photovoltaic infrastructure.

Technological advancements are accelerating the adoption of water-based PVDF dispersions, reducing VOC emissions and aligning with green manufacturing targets under the Five-Year Plans. Additionally, increased localization of semiconductor production has driven demand for ETFE-lined chemical piping systems, ensuring high-purity processing environments. Offshore wind projects in the South China Sea are further boosting demand for anti-fouling fluoropolymer coatings, designed to withstand high-salinity corrosion.

United States Fluoropolymer Coating Market: High-Tech Manufacturing Resurgence and Aerospace Innovation

The U.S. fluoropolymer coatings market is witnessing a strong resurgence, fueled by the reshoring of semiconductor manufacturing, EV battery production, and aerospace engineering. Strategic investments, including the development of battery-grade PVDF facilities, are strengthening the domestic supply chain for advanced coating materials.

Regulatory developments such as the EPA’s PFAS Strategic Roadmap (2025) are accelerating the transition toward low-emission fluoropolymer coatings and non-fluorinated surfactant technologies, reshaping product innovation strategies. Companies like Chemours are introducing advanced Teflon™ coatings tailored for AI-driven data center cooling systems, offering enhanced thermal management and dielectric performance.

The aerospace sector is a key growth driver, with increasing adoption of cryogenic-stable FEP coatings for liquid oxygen and hydrogen fuel systems, particularly in the expanding “New Space” industry. Additionally, EN 9100-compliant PTFE coatings are being integrated into next-generation aircraft designs to reduce frictional drag and improve fuel efficiency.

Healthcare applications are also expanding, with medical-grade fluoropolymer coatings being used in surgical robotics, where high biocompatibility and resistance to sterilization processes are critical. These factors collectively position the U.S. as a leader in high-performance fluoropolymer coating technologies.

Japan Fluoropolymer Coating Market: Nanocomposite Innovation and Semiconductor Purity Leadership

Japan continues to lead the fluoropolymer coatings industry through its focus on nanocomposite materials, ultra-high-purity coatings, and advanced electronics applications. The commercialization of graphene-enhanced fluoropolymer nanocomposite coatings represents a significant technological milestone, delivering superior mechanical strength and thermal barrier properties for aerospace and industrial applications.

Japanese manufacturers are also pioneering high-performance fluoropolymer films for 5G and emerging 6G technologies, offering extremely low dissipation factors to minimize signal loss in high-frequency communication systems. The country’s semiconductor ecosystem is further strengthened by initiatives under the Economic Security Act, prioritizing the development of high-purity PFA coatings for sub-2nm chip fabrication environments.

Sustainability initiatives are gaining traction, with the introduction of closed-loop recycling systems for ETFE architectural films, enabling high material recovery rates and reducing environmental impact. Japan also maintains dominance in optical fiber coatings, where fluoropolymers are used as low-refractive-index cladding materials to enhance performance in medical imaging and telecommunications.

Germany Fluoropolymer Coating Market: Hydrogen Economy and Regulatory-Driven Innovation

Germany serves as the backbone of the European fluoropolymer coatings market, driven by strong investments in green hydrogen infrastructure, automotive electrification, and stringent chemical safety regulations under REACH. The expansion of hydrogen electrolyzer projects, particularly in the North Sea region, is creating significant demand for FEP and PFA-lined components capable of withstanding high-pressure and corrosive environments.

Corporate expansions, including the establishment of localized EV and energy storage solution hubs, are enhancing Germany’s role in supplying fluoropolymer-based binder coatings for advanced battery systems. Regulatory leadership in Europe is evident through Germany’s advocacy for PFAS “essential-use” exemptions, ensuring continued use of fluoropolymer coatings in critical sectors such as healthcare and pharmaceuticals.

The automotive sector is driving innovation through the integration of PTFE-based coatings in high-voltage EV charging systems, preventing electro-corrosion and enhancing system reliability. In construction, the adoption of FEVE topcoats for high-rise buildings ensures compliance with fire safety standards while providing superior UV resistance and long-term durability. Additionally, specialized coating centers are advancing electrostatic powder coating technologies for complex industrial components.

India Fluoropolymer Coating Market: Industrial Growth and Infrastructure-Led Demand Surge

India is rapidly emerging as a key growth engine in the global fluoropolymer coatings market, driven by robust expansion in electronics manufacturing, pharmaceuticals, automotive production, and infrastructure development. The country’s electronics sector is witnessing exponential growth, leading to increased demand for ETFE and FEP cable insulation coatings used in 5G infrastructure and advanced communication systems.

Investments in semiconductor manufacturing are further boosting the adoption of high-purity PFA coatings, essential for wafer processing and cleanroom environments. The pharmaceutical industry is also contributing significantly, with regulatory approvals for fluoropolymer-coated medical devices, including drug-eluting stents, highlighting the material’s growing importance in healthcare applications.

The automotive sector’s transition toward lightweight materials has increased the use of fluoropolymer coatings in fuel systems and wiring, improving efficiency and durability. Infrastructure initiatives under the National Infrastructure Pipeline (NIP) are driving demand for PVDF-coated aluminum panels in airport construction, ensuring long-term weather resistance and reduced maintenance.

Additionally, the expansion of wastewater treatment facilities is boosting the adoption of PTFE-based membrane coatings, improving filtration efficiency and supporting environmental compliance. These developments position India as a high-growth market with strong long-term potential.

South Korea Fluoropolymer Coating Market: Advancing Battery Safety and High-Tech Manufacturing

South Korea is strengthening its position in the fluoropolymer coatings market through innovation in energy storage systems (ESS), EV batteries, and advanced electronics manufacturing. The development of flame-retardant fluoropolymer coatings achieving UL 94-5VA ratings is enhancing safety in battery modules, preventing thermal runaway and improving reliability.

Marine engineering applications are also expanding, with FEP-based anti-fouling coatings being used in LNG carrier sensors to protect against corrosion and bio-growth in harsh marine environments. Significant investments by companies like Samsung SDI and LG Energy Solution are driving R&D in solid-state battery coatings, where fluoropolymers play a critical role in electrolyte stabilization.

Government initiatives promoting solvent-free fluoropolymer powder coatings are aligning the industry with sustainability and carbon reduction goals. Technological advancements, such as multi-layer hydrophobic fluoropolymer coatings, are being widely adopted in OLED manufacturing equipment to prevent chemical damage and improve durability.

A key application area includes the use of FEP-coated aluminum foils in battery current collectors, enhancing cycle life and safety in high-nickel cathode systems. These innovations underscore South Korea’s leadership in high-performance fluoropolymer coating technologies.

Fluoropolymer Coating Market Report Scope

Fluoropolymer Coating Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4 Billion

|

|

Market Size (2032)

|

$6.4 Billion

|

|

Market Growth Rate

|

6.9%

|

|

Segments

|

By Form (Liquid Coatings, Powder Coatings, Films and Membranes), By Coating Process (Coil Coating, Extrusion Coating, Spray Coating, Dip and Spin Coating, Fluidized Bed Coating), By Substrate (Metal, Concrete and Masonry, Plastics and Elastomers, Glass and Ceramics, Composites), By End-Use Industry (Chemical Processing, Building and Construction, Food and Beverage, Electrical and Electronics, Automotive and Transportation, Aerospace and Defense, Medical and Healthcare, Energy), By Functional Property (Corrosion and Chemical Resistance, Non-stick, Weather and UV Resistance, Electrical Insulation, Low Friction, Thermal Stability), By Distribution Channel (Direct Sales, Specialty Distributors and Wholesalers, Service-based Applicators)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Daikin Industries, Ltd., The Chemours Company, PPG Industries, Inc., AkzoNobel N.V., The Sherwin-Williams Company, AGC Inc., Arkema S.A., Axalta Coating Systems Ltd., Solvay S.A., 3M Company, Jotun A/S, Kansai Paint Co., Ltd., Hempel A/S, Dongyue Group Limited, Gujarat Fluorochemicals Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Fluoropolymer Coating Market Segmentation

By Form

- Liquid Coatings

- Powder Coatings

- Films and Membranes

By Coating Process

- Coil Coating

- Extrusion Coating

- Spray Coating

- Dip and Spin Coating

- Fluidized Bed Coating

By Substrate

- Metal

- Concrete and Masonry

- Plastics and Elastomers

- Glass and Ceramics

- Composites

By End-Use Industry

- Chemical Processing

- Building and Construction

- Food and Beverage

- Electrical and Electronics

- Automotive and Transportation

- Aerospace and Defense

- Medical and Healthcare

- Energy

By Functional Property

- Corrosion and Chemical Resistance

- Non-stick

- Weather and UV Resistance

- Electrical Insulation

- Low Friction

- Thermal Stability

By Distribution Channel

- Direct Sales

- Specialty Distributors and Wholesalers

- Service-based Applicators

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Fluoropolymer Coating Market

- Daikin Industries, Ltd.

- The Chemours Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- The Sherwin-Williams Company

- AGC Inc.

- Arkema S.A.

- Axalta Coating Systems Ltd.

- Solvay S.A.

- 3M Company

- Jotun A/S

- Kansai Paint Co., Ltd.

- Hempel A/S

- Dongyue Group Limited

- Gujarat Fluorochemicals Limited

*- List not Exhaustive