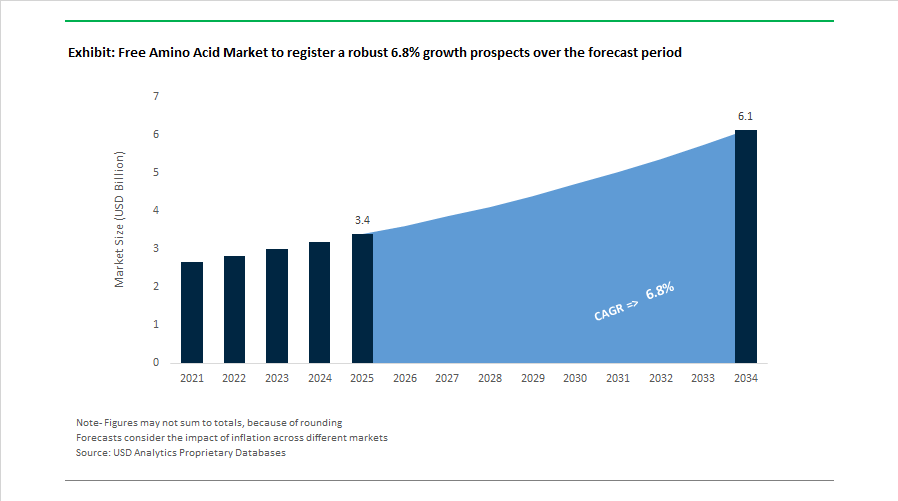

Free Amino Acid Market Size 2025–2034: $3.4 Billion to $6.1 Billion at 6.8% CAGR Driven by AminoScience Expansion, Fermentation Innovation and Supply Chain Realignment

The Free Amino Acid Market is projected to expand from $3.4 billion in 2025 to $6.1 billion by 2034, registering a robust CAGR of 6.8%. Market growth is supported by rising demand for pharmaceutical-grade amino acids, sports nutrition supplements, animal feed additives, biostimulants, and fermentation-derived functional ingredients. L-lysine, L-methionine, L-tryptophan, L-valine, L-phenylalanine, and specialty derivatives such as recombinant albumin remain core value drivers. The sector is increasingly shaped by fermentation optimization, backward integration strategies, regulatory compliance in China, and expansion into plant nutrition and biopharmaceutical applications.

In February 2026, Daesang Corporation entered the Japanese distribution market at the Supermarket Trade Show, signaling expansion of fermentation-based amino acid ingredients into high-quality retail and health-focused channels. In the first quarter of 2026, Ajinomoto relocated its headquarters to accelerate “value co-creation” within its AminoScience platform, reinforcing R&D intensity in health and performance nutrition. In January 2026, Evonik marked 50 years at IPPE by highlighting its backward integration project at its Mobile, Alabama methionine hub, strengthening supply security for MetAMINO® and Biolys® across the Americas.

Throughout late 2025, market volatility intensified. In November 2025, CJ CheilJedang reported a 72% decline in operating profit within its BIO segment due to aggressive pricing pressure from Chinese amino acid manufacturers, prompting a strategic pivot toward manufacturing efficiency and higher-margin specialty products. In November 2025, Evonik partnered with InVitria to supply animal component-free recombinant human serum albumin, integrating fermentation-derived amino acid technology into the biopharmaceutical value chain. In July 2025, Kyowa Hakko Bio completed the transfer of its amino acid and Human Milk Oligosaccharide businesses, narrowing focus to specialized branded ingredients. Earlier in March 2025, China’s NMPA suspended imports from Kyowa Hakko Bio’s Hofu facility over compliance concerns, disrupting regional supply of pharmaceutical-grade Tryptophan, Phenylalanine, and L-Valine. In early 2025, Ajinomoto unveiled its “Eat Well, Live Well” business plan emphasizing expansion of amino acid supplements for aging populations and athletes, supported by its AI-driven i-LiveWell wellness platform. In March 2025, BASF’s Isobionics expanded its fermentation-based portfolio, highlighting the broader industry migration toward lab-grown amino acid precursors.

Strategic collaborations and agricultural diversification accelerated during 2024. In April 2024, Evonik debuted its joint venture Evonik Vland Biotech at the China Feed Industry Expo, integrating amino acids with enzymes and probiotics for advanced animal gut health solutions. In September 2024, Ajinomoto and Danone launched a partnership aimed at reducing dairy-related greenhouse gas emissions through amino acid-enhanced feed efficiency strategies. In late 2023 and early 2024, Redox and CJ Bio introduced AMIBOOST, an amino acid-enriched biostimulant designed to enhance plant metabolism and crop yield resilience, marking expansion of free amino acids into stress tolerance and precision agriculture markets.

Trends and Opportunities in the Global Free Amino Acid Market

Precision Fermentation Scaling and the Rise of “AminoScience” Platforms

The structural shift toward animal-free and bio-based production is accelerating investment in microbial fermentation technologies for essential free amino acids such as L-Lysine, L-Tryptophan, L-Threonine, and L-Valine. In its 2025 ASV Report, Ajinomoto Co., Inc. reaffirmed its Vision 2030 strategy, positioning its AminoScience platform as a core growth engine across food, healthcare, and biopharmaceutical inputs. Expansion of fermentation capacity across ASEAN and Latin America is specifically designed to reduce exposure to geopolitical risk and stabilize long-cycle supply contracts.

Platform-level innovation is also accelerating in animal-component-free production. In November 2025, Evonik Industries AG announced a strategic partnership with InVitria to expand the global availability of ACF amino acids and peptides. These inputs are critical for biopharmaceutical cell culture media, where regulatory scrutiny around animal-derived components is intensifying.

Profitability dynamics are also shifting in favor of fermentation-derived amino acids. In November 2025, CJ CheilJedang reported margin expansion in bulk amino acids such as L-Lysine and L-Threonine in Europe. Anti-dumping duties on synthetic imports and rising quality expectations are pushing buyers toward fermentation-based alternatives with consistent optical purity and traceability, reinforcing the long-term competitiveness of biotech-led producers.

Integration into Clinical Nutrition and Targeted Medical Foods

Free amino acids are increasingly positioned as therapeutic actives rather than commodity nutrients, particularly in aging, liver health, and metabolic disease management. Clinical research updated in September 2025 by Maastricht University Medical Center under trial NCT06553794 is generating critical data on how aging gastrointestinal systems absorb amino acids. Findings on transporter expression are directly influencing formulation strategies for geriatric medical foods, where bioavailability is a primary differentiator.

Demand is also rising sharply in hepatic and metabolic support. Industry analysis in 2025 highlights strong growth in L-Glutamine, L-Arginine, and branched-chain amino acids used in enteral and parenteral nutrition for liver regeneration and metabolic balance. This trend is closely tied to the global increase in non-alcoholic fatty liver disease and post-operative recovery protocols.

Regulatory clarity is reinforcing market confidence. In 2025, multiple GRAS evaluations were completed by the U.S. FDA for fermentation-derived amino acids, enabling pharmaceutical-grade suppliers to expand into regulated medical food applications under Title 21 CFR. This is accelerating the convergence of the food ingredient and clinical nutrition value chains.

Cognitive Health and the Nootropic Free Amino Acid Segment

The convergence of cognitive wellness and amino acid chemistry represents a structurally attractive growth opportunity. A systematic review published in late 2024 and highlighted in April 2025 confirmed that L-Theanine at daily doses of 200 to 450 mg modulates GABA and dopamine pathways. This evidence has repositioned L-Theanine as a clinically supported adjunct for anxiety, ADHD, and cognitive stress, driving demand for pharmaceutical-grade, clean-label formulations.

Stacked nootropic formulations are gaining momentum. Updated research from the Alzheimer’s Drug Discovery Foundation in April 2025 demonstrated that combinations of L-Theanine and caffeine deliver superior improvements in reaction time and visual attention versus single-ingredient products. This stacking trend is expanding demand for standardized L-Theanine, L-Tyrosine, and related precursors in gaming, professional productivity, and mental performance supplements, where consistency and purity are non-negotiable.

Growth Media Optimization for Cultivated Meat and Fermentation-Derived Proteins

Free amino acids have emerged as the single largest cost driver in serum-free growth media used for cultivated meat and precision-fermented proteins. A December 2025 analysis by The Good Food Institute showed that replacing pharmaceutical-grade amino acids with food-grade equivalents can reduce media costs by up to 100 times. This cost reduction is essential to achieving the industry target of £1 per litre for growth media, a threshold required for commercial competitiveness with conventional protein.

Scale-driven partnerships are already demonstrating feasibility. In August 2024, Believer Meats validated an animal-component-free medium costing £0.50 per litre, projecting production costs near £5 per pound at scale. Continuous manufacturing and tailored free amino acid inputs were central to this breakthrough, highlighting the volume potential for suppliers capable of delivering consistent, GMP-aligned ingredients.

At the industrial level, suppliers such as Evonik are gaining traction with advanced amino acid and peptide portfolios that address solubility and stability challenges in high-density bioreactors exceeding 20,000 liters. These innovations improve titers, reduce waste, and directly enhance process economics, positioning free amino acids as strategic enablers of the broader bioeconomy rather than standalone commodities.

Free Amino Acid Market Share and Segmentation Insights

Essential Amino Acids Lead Nutritional and Feed Supplementation Markets Due to Physiological Necessity

Essential Amino Acids accounted for 58.70% of the Free Amino Acid Market share in 2025, making them the dominant product category across global nutrition and feed applications. Essential amino acids—including histidine, isoleucine, leucine, lysine, methionine, phenylalanine, threonine, tryptophan, and valine—cannot be synthesized by the human body and must therefore be obtained through dietary intake or supplementation. This biological necessity drives strong demand across multiple sectors, including animal feed optimization, sports nutrition supplements, clinical nutrition products, and fortified functional foods. In livestock production, amino acids such as lysine and methionine are widely incorporated into feed formulations to improve protein utilization efficiency and animal growth performance, reducing reliance on expensive protein feedstocks like soybean meal. In 2025, the essential amino acid segment is witnessing rapid innovation driven by the growing importance of branched-chain amino acids (BCAAs)—leucine, isoleucine, and valine—in human nutrition markets. BCAAs are increasingly incorporated into sports performance supplements, recovery drinks, and clinical nutrition formulations, supported by emerging research linking them to muscle protein synthesis, fatigue reduction, and muscle preservation in aging populations. As a result, manufacturers are developing optimized amino acid blends tailored to specific physiological outcomes, reinforcing the leadership of essential amino acids in the global free amino acid market.

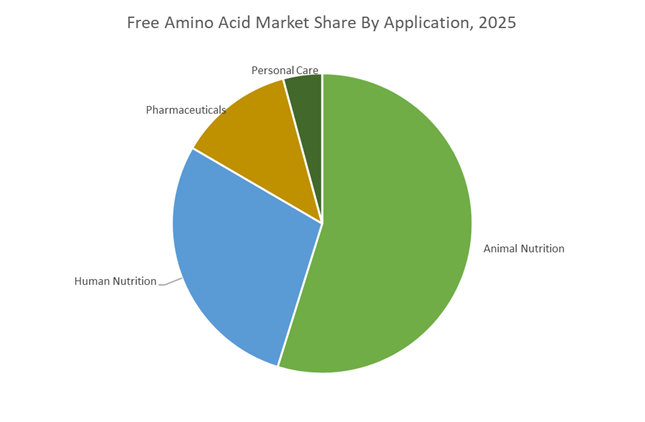

Animal Nutrition Drives the Largest Consumption of Free Amino Acids in Global Feed Production

Animal Nutrition represented 54.80% of the Free Amino Acid Market share in 2025, making it the largest application segment within the global amino acid industry. Modern livestock production relies heavily on precise feed formulation strategies designed to maximize animal growth performance, feed efficiency, and protein conversion ratios. Free amino acids are widely used in poultry, swine, aquaculture, and ruminant feed formulations to ensure animals receive optimal levels of essential nutrients without requiring excessive protein inputs. This approach not only improves animal productivity and feed cost efficiency, but also helps reduce nitrogen emissions and environmental impacts associated with excess dietary protein. In 2025, demand growth within the animal nutrition sector is particularly strong for methionine and lysine, two amino acids critical for high-performance feed formulations. Methionine plays a key role in fish and shrimp diets within rapidly expanding aquaculture industries, while lysine is essential for improving growth rates in swine and poultry production systems. As global seafood consumption continues to rise, aquaculture feed producers are developing specialized amino acid formulations designed for aquatic species, including water-stable amino acid delivery systems and palatability-enhancing additives.

Competitive Landscape in Free Amino Acid Market

Ajinomoto Leads High-Purity AminoScience and Bio-Pharma Integration

Ajinomoto Co., Inc. remains the global benchmark in fermentation-derived free amino acids under its AminoScience platform. For FY2025/26 ending March 31, 2026, the company forecasted sales of ¥1,618 billion with projected business profit of ¥180 billion, reflecting continued margin expansion in healthcare and specialty materials. In late 2025, Ajinomoto divested Ajinomoto Althea Inc. to streamline focus on high-growth bio-pharma services and specialty ingredients. In November 2025, it partnered with Forge Biologics to develop advanced culture media supplements aimed at improving gene therapy productivity, reinforcing its presence in cell and gene therapy raw materials. Under its 2030 Roadmap, Ajinomoto targets over 10% business profit CAGR, emphasizing high-purity amino acids for pharmaceuticals, nutraceuticals, and semiconductor substrates rather than commodity MSG-linked applications.

Evonik Strengthens Methionine Integration and Sustainable Animal Nutrition

Evonik Industries AG remains a dominant supplier of essential amino acids, particularly DL-methionine, for global animal nutrition markets. In January 2026, the company highlighted its backward integration expansion at its Mobile, Alabama methionine hub, securing long-term supply for the Americas. Logistics upgrades in Antwerp during late 2025 enhanced global distribution flexibility for MetAMINO®. Sustainability initiatives include recyclable paper packaging for 25 kg methionine bags introduced in July 2025 to align with the EU Packaging and Packaging Waste Regulation. Evonik is actively evaluating restructuring or partnerships for non-core amino and keto acid assets in France and China, concentrating capital on specialty chemicals and digital farming services. This integration model stabilizes pricing in volatile feed-grade amino acid markets while supporting premium positioning.

CJ CheilJedang Dominates Fermentation Scale and Expands Human Nutrition Portfolio

CJ CheilJedang is the world’s largest producer of lysine, tryptophan, and valine in the global tryptophan market. Its production network spans Brazil, Indonesia, China, and the United States, reinforcing global-for-local manufacturing resilience. In 2025, CJ expanded eco-friendly fermentation lines that reduce carbon emissions by more than 20% compared to traditional processes. In early 2026, the company intensified R&D in specialty amino acids such as citrulline and arginine targeting sports nutrition and aging demographics. While maintaining leadership in feed-grade amino acids, CJ is strategically pivoting toward higher-margin human nutrition and clinical ingredients to balance exposure to cyclical livestock demand.

Daesang Accelerates Pharmaceutical-Grade Expansion Through European Acquisition

Daesang Corporation strengthened its pharmaceutical amino acid footprint through the December 2025 acquisition of Amino GmbH for approximately $34 million. Completed in March 2026, the deal secured three German production facilities and direct entry into Europe’s infusion and cell culture media markets. Traditionally known for fermentation products ranging from MSG to essential amino acids such as phenylalanine and arginine, Daesang is leveraging Amino GmbH’s pharmaceutical compliance infrastructure to expand into North America and Asia. CEO Lim Jung-bae confirmed aggressive biotech expansion plans in early 2026, signaling a strategic shift from food-grade fermentation to high-margin pharmaceutical and bioprocessing amino acids.

Fufeng Globalizes Supply Chain Through Kazakhstan Corn Fermentation Hub

Fufeng Group continues to expand large-scale fermentation capacity, leveraging cost advantages in raw materials and energy. In June 2025, the company announced an $800 million investment in a vertically integrated corn processing and bio-fermentation complex in Kazakhstan, with the first phase costing $350 million. The facility is designed to process one million tons of corn annually, producing lysine, glutamine, and threonine for export to Europe and the Middle East. In March 2025, Fufeng resolved a major intellectual property dispute, securing RMB 233 million in settlement related to fermentation trade secrets. By diversifying outside China, Fufeng mitigates tariff exposure and strengthens its EMEA supply chain positioning in bulk amino acids.

Kyowa Hakko Focuses on High-Purity Clinical Amino Acids and CGT Materials

Kyowa Hakko Bio Co., Ltd., part of the Kirin Group, remains a leader in pharmaceutical-grade free amino acids and specialty dipeptides. Under Kirin’s Health Science strategy, the company is pivoting toward life-changing biomaterials for cell and gene therapy applications. Its high-purity L-Alanyl-L-Glutamine product Sustamine® continues to dominate medical nutrition and advanced recovery supplements. In early 2026, Kyowa Kirin announced renewed strategic alignment in its Rocatinlimab program, reflecting deeper integration between antibody development and amino acid science. The company is progressively reducing exposure to bulk commodity amino acids and increasing focus on Human Milk Oligosaccharides and specialty dipeptides that command premium margins in clinical nutrition and biopharma manufacturing.

China: Feed Reform, Biotech Approvals, and Green Fermentation Reshaping Scale Economics

China remains the structural anchor of the global free amino acid market, with policy-driven feed reform acting as the primary demand catalyst. The national mandate to reduce soymeal inclusion in animal feed from 13% in 2023 to 10% by 2030 is accelerating substitution with crystalline amino acids, particularly L-lysine and L-threonine, to preserve feed efficiency while lowering dependence on imported soybeans. This policy has materially expanded domestic consumption of feed-grade amino acids and reinforced China’s role as the largest producer and exporter of bulk free amino acids.

Simultaneously, the market is moving up the value chain. In early 2025, the National Medical Products Administration approved several high-purity amino acid production strains for infant formula and clinical nutrition, including strains used for 2’-fucosyllactose. This marks a strategic shift toward biotech-derived, pharma-grade ingredients. Capacity economics are being further optimized through petrochemical integration in Zhejiang, where large chemical hubs are embedding amino acid synthesis units into 2025–2026 expansion plans to leverage upstream ammonia and hydrogen. Environmental compliance audits in Shandong and Hebei in late 2025 temporarily tightened supply but accelerated adoption of green fermentation technologies that reduce nitrogen discharge, favoring large, compliant producers.

Japan: Pharmaceutical-Grade Focus and Functional Nutrition for an Aging Society

Japan’s free amino acid market is increasingly oriented toward pharmaceutical, biopharma, and precision nutrition applications. In its 2025 Creating Shared Value report, Ajinomoto outlined a strategic pivot toward regenerative medicine and CDMO services, with a 2026 scale-up of animal-origin-free amino acids for cell culture media. These inputs are critical for biologics manufacturing, where contamination control and batch consistency are non-negotiable.

Industry restructuring is reinforcing this specialization. In July 2025, Kyowa Hakko Bio transferred its amino acids and human milk oligosaccharides business to a subsidiary of Meihua Holdings Group, allowing Kyowa to concentrate on pharmaceutical-grade ingredients while Meihua gains access to Japanese process expertise. Public funding is also supporting demand-side innovation, with government-backed 2026 R&D programs targeting functional amino acids such as L-arginine and L-citrulline for cardiovascular health and sarcopenia prevention in Japan’s aging population.

United States: Regulatory Scrutiny and Specialty Nutrition Driving Purity Standards

The United States free amino acid market is defined by regulatory rigor and specialty application growth rather than bulk volume. Under the Modernization of Cosmetics Regulation Act, the U.S. Food and Drug Administration intensified oversight during 2025–2026 of amino acid-based surfactants and skin-repair actives. This has elevated documentation and safety dossier requirements, shifting demand toward high-purity, pharma-grade free amino acids for premium skincare and dermatological formulations.

Nutrition security is another defining factor. Major players such as Abbott expanded domestic production lines for hypoallergenic amino acid-based infant formulas during 2024–2025, ensuring supply resilience for clinical nutrition products used in gastrointestinal disorders. On the innovation front, U.S. startups are integrating AI-designed amino acid sequences into functional proteins and fragrance fixatives, applying generative biology to create novel amino acid derivatives with differentiated performance attributes.

South Korea: Profit Recovery, European Expansion, and AI-Led Fermentation

South Korea’s free amino acid market has rebounded strongly on the back of favorable pricing for bulk products and strategic overseas expansion. In 2025, CJ CheilJedang reported a sharp profit increase driven largely by lysine and other bulky amino acids. The company is expanding its Selecta soybean processing and amino acid production to stabilize margins amid volatility in specialty segments.

Cross-border growth is accelerating. In December 2025, Daesang Corporation acquired Amino GmbH in Germany, with integration planned for March 2026, signaling a decisive move into the European pharmaceutical-grade amino acid market. Operational efficiency is also improving through AI-integrated fermentation, with CJ CheilJedang applying machine learning to optimize microbial cycles for L-methionine and L-valine, lowering cost of goods manufactured and improving yield consistency.

Germany: Cell Culture Prioritization and Sustainable Packaging Leadership

Germany plays a strategic role in high-value amino acids for nutrition, healthcare, and advanced manufacturing. In 2025, Evonik reported solid growth in its Nutrition and Care division while reorganizing its Health Care portfolio to focus on cell culture ingredients and mRNA lipids. The planned exit from keto-acid production in Hanau by the end of 2025 reflects a deliberate reallocation toward higher-growth biopharma inputs.

Logistics and sustainability are reinforcing competitiveness. Evonik upgraded its Antwerp infrastructure for MetAMINO during October 2025, improving global supply security ahead of the 2026 fiscal year. German producers are also leading compliance with the EU Packaging and Packaging Waste Regulation by adopting plastic-free paper packaging for 25-kilogram amino acid bags, aligning bulk amino acid distribution with circular economy requirements.

Brazil: Feed-Grade Export Scale and Biofuel Integration

Brazil has consolidated its position as a key export hub for feed-grade free amino acids, supported by scale, logistics, and agricultural integration. Facilities in Piracicaba operated by CJ CheilJedang achieved record export volumes to North America in late 2025, underscoring Brazil’s role in global feed additive supply chains.

Looking ahead, investment momentum is shifting toward integration with the bio-ethanol sector. Planned 2026 projects are linking amino acid fermentation plants with ethanol refineries, using sugarcane and corn byproducts as low-cost substrates. This feedstock synergy lowers input costs, improves carbon efficiency, and strengthens Brazil’s competitiveness in large-volume amino acid exports.

Summary of Country-Level Strategic Drivers in the Free Amino Acid Market

Free Amino Acid Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Implications for Free Amino Acids

|

|

China

|

Soymeal reduction and biotech approvals

|

Expansion of feed-grade volume and infant nutrition ingredients

|

|

Japan

|

Biopharma focus and aging population

|

Growth in pharma-grade and functional amino acids

|

|

United States

|

Regulatory scrutiny and specialty nutrition

|

Demand for high-purity, documentation-ready amino acids

|

|

South Korea

|

Profit recovery and European expansion

|

Scale-up of bulk amino acids and entry into pharma-grade markets

|

|

Germany

|

Cell culture prioritization and sustainability

|

Shift toward biopharma inputs and compliant bulk packaging

|

|

Brazil

|

Export scale and ethanol integration

|

Cost-competitive feed-grade amino acid supply

|

Free Amino Acid Market Report Scope

Free Amino Acid Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.4 Billion

|

|

Market Size (2034)

|

$6.1 Billion

|

|

Market Growth Rate

|

6.8%

|

|

Segments

|

By Type (Essential Amino Acids, Non-Essential Amino Acids), By Source (Plant-Based, Animal-Based, Synthetic and Fermentation-Based), By Grade (Pharma Grade, Food Grade, Feed Grade, Cosmetic Grade), By Application (Animal Nutrition, Human Nutrition, Pharmaceuticals, Personal Care)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Ajinomoto Co., Inc., CJ CheilJedang Corporation, Evonik Industries AG, Archer Daniels Midland Company, Meihua Holdings Group Co., Ltd., Kyowa Hakko Bio Co., Ltd., Daesang Corporation, Global Bio-chem Technology Group Co., Ltd., Fufeng Group Limited, Amino GmbH, Prinova Group LLC, DSM-Firmenich AG, Lonza Group AG, Novus International, Inc., Vedan International Holdings Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Free Amino Acid Market Segmentation

By Type

- Essential Amino Acids

- Non-Essential Amino Acids

By Source

- Plant-Based

- Animal-Based

- Synthetic and Fermentation-Based

By Grade

- Pharma Grade

- Food Grade

- Feed Grade

- Cosmetic Grade

By Application

- Animal Nutrition

- Human Nutrition

- Pharmaceuticals

- Personal Care

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Free Amino Acid Industry

- Ajinomoto Co., Inc.

- CJ CheilJedang Corporation

- Evonik Industries AG

- Archer Daniels Midland Company

- Meihua Holdings Group Co., Ltd.

- Kyowa Hakko Bio Co., Ltd.

- Daesang Corporation

- Global Bio-chem Technology Group Co., Ltd.

- Fufeng Group Limited

- Amino GmbH

- Prinova Group LLC

- DSM-Firmenich AG

- Lonza Group AG

- Novus International, Inc.

- Vedan International Holdings Limited

*- List not Exhaustive