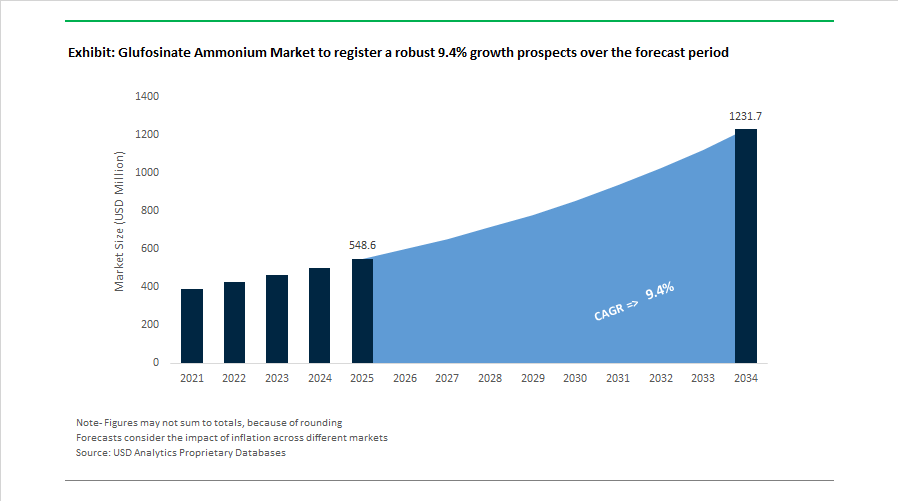

Glufosinate Ammonium Market to Reach $1,231.4 Million by 2034 at 9.4% CAGR Driven by Herbicide-Resistant Crops and L-Glufosinate Scale-Up

The Glufosinate Ammonium Market is projected to expand from $548.6 Million in 2025 to $1,231.4 Million by 2034, registering a robust CAGR of 9.4%. Growth is being propelled by rising adoption of glufosinate-resistant biotech crops, regulatory restrictions on older herbicides such as paraquat and dicamba, and the commercial scale-up of L-glufosinate and Glufosinate-P technologies. Increasing glyphosate-resistant weed pressure in major agricultural regions, including the U.S. Corn Belt and China’s soybean-producing provinces, is accelerating the shift toward multi-herbicide tolerance stacks and next-generation contact herbicides.

In January 2024, China’s Ministry of Agriculture and Rural Affairs approved three new genetically modified soybean varieties tolerant to glufosinate, significantly expanding domestic demand as the country accelerates biotech crop deployment to strengthen food security. In March 2024, Bayer CropScience launched a new liquid soluble glufosinate-ammonium formulation in Europe designed to comply with European Green Deal environmental standards. In June 2024, Lier Chemical Co., Ltd. commenced production at its 20,000 metric ton Glufosinate-P facility, marking a structural transition toward high-efficacy L-glufosinate technology capable of delivering equivalent weed control at reduced application rates. In July 2024, BASF SE announced the shutdown of its Knapsack and Frankfurt glufosinate production sites due to high European energy costs and intensified competition from generic manufacturers, signaling a shift toward outsourced active ingredient sourcing.

Regulatory approvals and trait technology expansion reinforced demand momentum in late 2024 and 2025. In August 2024, Pioneer, a brand of Corteva Agriscience, announced the commercial launch of Vorceed Enlist corn for the 2025 season, featuring quad-herbicide tolerance that includes glufosinate, 2,4-D choline, glyphosate, and FOP chemistries. In October 2024, BASF registered Liberty ULTRA herbicide utilizing proprietary Glu-L Technology, enabling 20% greater weed control efficacy and expanded acreage coverage per gallon. The same month, the United States Environmental Protection Agency approved higher usage rates for Glufosinate-P, positioning it as a front-line burndown alternative in regions facing restrictions on legacy herbicides. In January 2025, the Government of India extended the Minimum Import Price on glufosinate technical through January 2026 to shield domestic producers such as UPL Limited from low-cost imports and stimulate local manufacturing capacity.

Market consolidation and pricing dynamics intensified into 2026. In 2025, Guang’an Lihua, the joint venture between Lier Chemical and Corteva, completed construction and began contributing to profits through high-purity glufosinate intermediate production. In January 2026, Lier Chemical forecasted a 122% increase in net profit for 2025, attributed to successful L-glufosinate scale-up and strengthened multinational partnerships following recovery from 2023 price lows. Also in January 2026, China canceled export tax rebates on glufosinate, prompting an immediate RMB 2,100 per ton price increase and accelerating the consolidation of smaller, high-cost producers.

The Glufosinate Ammonium Market outlook reflects expanding herbicide-tolerant crop acreage, regulatory displacement of older chemistries, rapid commercialization of Glufosinate-P half-rate technology, regional policy interventions, and structural supply chain realignment. Competitive positioning increasingly depends on isomer-specific production efficiency, trait platform integration, cost-competitive large-scale manufacturing, and compliance with evolving environmental and agricultural regulations across North America, China, India, and the European Union.

Glufosinate Ammonium Market Trends and Strategic Growth Opportunities

Transition Toward L-Glufosinate Technology to Improve Efficacy and Environmental Performance

The glufosinate ammonium market is undergoing a decisive technology upgrade as manufacturers shift from conventional racemic formulations toward resolved L-glufosinate ammonium. Traditional products contain a 50:50 mix of biologically active L-isomers and inactive D-isomers, resulting in unnecessary chemical loading and higher application volumes. By contrast, L-glufosinate formulations concentrate the herbicidally active isomer, enabling stronger weed control at lower use rates. This evolution is directly aligned with global regulatory pressure to reduce pesticide intensity while maintaining agronomic productivity.

A key inflection point occurred in October 2024, when BASF received approval from the U.S. Environmental Protection Agency for Liberty ULTRA, the first resolved-isomer glufosinate powered by proprietary Glu-L technology. Field data demonstrated roughly 20% higher weed control efficacy versus standard glufosinate, allowing growers to treat approximately one-third more acreage per gallon. This efficiency gain translates into lower transportation volumes, reduced on-farm handling, and a smaller carbon footprint per hectare treated. BASF further reinforced this strategy in July 2024 by announcing the phase-out of standard glufosinate ammonium production at its Knapsack and Frankfurt sites by the end of 2025, reallocating capital toward advanced L-glufosinate innovation and third-party sourcing of legacy actives. Collectively, these moves signal a structural pivot toward higher-value, lower-impact herbicide chemistries consistent with European Green Deal and ESG objectives.

Seed Trait Stacking and Herbicide-Tolerant Crop Systems Drive Demand Stability

Beyond formulation chemistry, the commercial outlook for glufosinate ammonium is increasingly tied to its role within stacked-trait crop platforms that combine multiple herbicide tolerance mechanisms. In North America, adoption of Corteva’s Enlist E3 soybean system has reached scale, integrating tolerance to 2,4-D choline, glyphosate, and glufosinate. As dicamba use faces tightening restrictions, glufosinate has emerged as the primary rescue and tank-mix partner in Enlist systems, particularly for controlling resistant species such as Palmer amaranth and waterhemp.

Asia is following a similar trajectory. In January 2024, the Chinese Ministry of Agriculture and Rural Affairs approved multiple glufosinate-resistant soybean varieties as part of its agricultural modernization strategy under the 14th Five-Year Plan. This policy shift is expected to accelerate domestic adoption of glufosinate-based weed management as China prioritizes yield security and herbicide diversity. Together, these developments are embedding glufosinate more deeply into integrated weed control programs, insulating demand from single-chemistry substitution risks.

Essential Tool for Managing Herbicide Resistance and High-Value Specialty Crops

Glufosinate’s unique mode of action, inhibition of the glutamine synthetase enzyme, makes it one of the most effective alternatives for managing weeds resistant to glyphosate and PPO inhibitors. Industry assessments from 2024 and 2025 indicate that glufosinate is now the leading non-selective herbicide option for post-emergence and burndown control across more than 170 weed species. Its strong performance against Kochia and giant ragweed has reinforced its value in North America, which accounted for more than 40% of global glufosinate market value in 2024.

Beyond row crops, specialty agriculture represents a structurally attractive growth avenue. Orchard crops, vineyards, and horticultural systems increasingly favor glufosinate due to its limited systemic movement and reduced risk of long-term vine or tree injury compared with glyphosate. In 2025, large-scale horticulture investments, including a multiyear development program supported by the Asian Development Bank in India, accelerated adoption of glufosinate for weed control in high-value perennial systems. These applications offer premium pricing and more stable usage patterns, strengthening margins for suppliers.

Alignment With Conservation Agriculture and Regulated Vegetation Management

The global shift toward conservation agriculture is creating durable demand for glufosinate-based vegetation management systems. No-till and reduced-tillage farming practices rely on effective chemical burndown to terminate cover crops while preserving soil structure. Glufosinate’s rapid activity and short soil residual profile make it well suited for this role, enabling quick planting of subsequent cash crops without carryover risk.

Regulatory positioning further enhances this opportunity. New registrations such as Liberty ULTRA are among the first herbicide labels fully aligned with updated U.S. Endangered Species Act guidelines, strengthening the long-term regulatory security of glufosinate in environmentally sensitive applications. This compliance advantage extends beyond agriculture into non-crop vegetation management, including railways, utility corridors, and rights-of-way. In parallel, policy tools such as India’s extension of Minimum Import Pricing for high-purity glufosinate technical material through January 2026 are stabilizing domestic markets and encouraging local investment in compliant manufacturing. Together, these factors position glufosinate ammonium as a resilient, regulation-aligned herbicide with sustained relevance in global weed and vegetation management strategies.

Glufosinate Ammonium Market Share and Segmentation Insights

Conventional Glufosinate Ammonium Leads the Global Herbicide Market Through Large-Scale Agricultural Adoption

Conventional Glufosinate Ammonium accounted for 68.40% of the Glufosinate Ammonium Market share in 2025, making it the dominant product type within the global non-selective herbicide industry. Conventional glufosinate ammonium is produced as a racemic mixture of active compounds, enabling cost-effective manufacturing at industrial scale while delivering reliable herbicidal performance against a broad spectrum of weeds. This form has achieved widespread adoption due to established regulatory approvals, farmer familiarity, and integration into herbicide-resistant crop systems across major agricultural regions. Farmers utilize glufosinate-based herbicides for post-emergence weed control in crops such as corn, soybean, cotton, and horticultural crops, where effective weed suppression is critical for maintaining crop yield and productivity. In 2025, market dynamics are increasingly influenced by the emergence of L-glufosinate ammonium, the biologically active enantiomer of the compound. L-glufosinate offers comparable weed control at approximately half the application rate, reducing chemical load while improving cost efficiency for farmers. As patent protections expire and manufacturing capacity expands, particularly in China’s agrochemical industry, L-glufosinate is gaining commercial traction as a higher-value herbicide formulation.

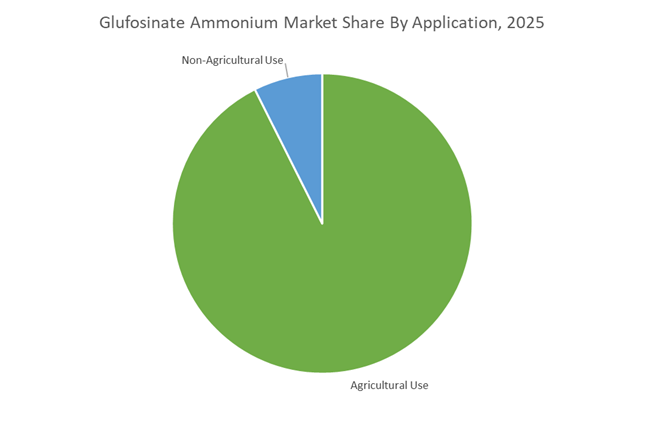

Agricultural Applications Dominate the Glufosinate Ammonium Market Through Global Crop Protection Demand

Agricultural Use represented 92.60% of the Glufosinate Ammonium Market share in 2025, highlighting the herbicide’s primary role in modern crop protection systems. Glufosinate ammonium is widely applied across row crops, orchards, vineyards, and vegetable cultivation, where it provides effective control of broadleaf weeds and grassy weeds that compete with crops for nutrients, water, and sunlight. The herbicide is particularly important in glufosinate-tolerant genetically modified crop systems, where farmers rely on its selective weed control properties to maintain field productivity. The scale of global agriculture ensures consistent demand, as glufosinate formulations are applied across millions of hectares of cultivated land each growing season. In 2025, agricultural usage patterns are expanding through increasing adoption of pre-harvest desiccation practices. Farmers apply glufosinate before harvest in crops such as potatoes, soybeans, and oilseeds to accelerate plant drying and achieve more uniform crop maturity, improving harvest efficiency and crop quality. This growing application area is strengthening demand for glufosinate-based herbicides within the global agricultural chemicals market.

Competitive Landscape in Glufosinate Ammonium Market

BASF SE Reinforces L-Glufosinate Leadership Through Precision Integration

BASF SE remains the technological benchmark in glufosinate ammonium through its Liberty® portfolio and next-generation L-glufosinate innovations. After ceasing active ingredient production at Knapsack and Frankfurt in 2024 and 2025, BASF transitioned to a third-party sourcing model in 2026 to enhance cost competitiveness against Chinese generics. Liberty® ULTRA, commercialized in late 2024 and 2025, delivers 20% greater weed control efficacy and treats 33% more acres per gallon than conventional formulations. The company is repositioning toward precision weed management by integrating L-glufosinate with Bosch-BASF Smart Spraying systems for targeted, data-driven herbicide application. Collaboration with Corteva on the HT4 soybean trait pipeline ensures multi-generational compatibility of glufosinate tolerance into the 2030s and 2040s.

UPL Limited Expands Generic Glufosinate Capacity Across Emerging Markets

UPL Limited leverages its large-scale Indian manufacturing footprint to supply cost-effective glufosinate ammonium formulations under the Lifeline® brand. The commissioning of a major formulation facility in Gujarat in 2024 strengthened its export capabilities to Southeast Asia and Africa, with 2026 marking peak utilization of this hub. Glufosinate has emerged as a top-five revenue contributor within UPL’s global herbicide portfolio, particularly as resistance to glyphosate intensifies in Latin America and Asia-Pacific. The company focuses on high-load soluble liquid formulations that improve logistics efficiency and farmer affordability. Its strategy emphasizes resilience and accessibility, targeting markets where regulatory pressure is phasing out paraquat and other non-selective herbicides.

Lier Chemical Dominates Technical-Grade and L-Isomer Production

Lier Chemical Co., Ltd. maintains the largest global production capacity for technical-grade glufosinate ammonium as of 2026. The company supplies multinational agrochemical firms as well as its own branded formulations, anchoring the global supply chain. Lier holds multiple patents for enzymatic synthesis of L-glufosinate, achieving high optical purity without reliance on costly chiral catalysts. This innovation supports the commercialization of high-concentration L-GA products aligned with next-generation herbicide programs. As a key reference point in the China price index, Lier contributed to stabilization of ex-factory glufosinate prices in early 2026 following overcapacity volatility between 2022 and 2025. Its portfolio spans technical material, 10% to 20% soluble liquid formulations, and premium L-isomer solutions for export markets.

Corteva Agriscience Secures Trait-Based Dominance in North America

Corteva Agriscience controls market influence through seed-chemical integration rather than active ingredient production. Its Enlist E3® soybean platform dominates North American acreage in 2026, with approximately 75 to 80% adoption supporting glufosinate as a primary over-the-top herbicide. The company’s 2026 integrated stewardship program mandates strict herbicide resistance management protocols to preserve glufosinate efficacy. Sonic Boom™, introduced in 2025 and 2026, combines multiple modes of action to reduce reliance on single-herbicide strategies. Corteva confirmed that its HT4 platform, featuring five-way herbicide tolerance including glufosinate, remains on schedule for 2027 commercialization, reinforcing long-term demand for Liberty-compatible chemistries.

Rainbow Agro Accelerates Global Registration and Distribution Expansion

Shandong Weifang Rainbow Chemical Co., Ltd., operating globally as Rainbow Agro, has expanded direct-to-market distribution into more than 80 countries by early 2026. The company secured new glufosinate registrations in Brazil and Argentina during 2025 and 2026, capitalizing on regulatory exits of other non-selective herbicides. Modernized production lines equipped with AI-driven digital controls enhance batch consistency and purity across its glufosinate formulations. Rainbow positions itself as a third-party supply partner for ag-retailers seeking ready-to-brand herbicide solutions. Its agility in regulatory registration and formulation customization strengthens penetration in high-growth Latin American markets.

Syngenta Group Integrates Glufosinate into Climate-Resilient Crop Systems

Syngenta Group incorporates glufosinate into its LibertyLink® trait-enabled corn and soybean hybrids, ensuring compatibility within integrated weed management programs. In 2026, the company emphasized its Artesian drought-tolerance technology combined with glufosinate tolerance, supporting climate-resilient farming systems. Syngenta leverages China-Swiss operational synergies to optimize cost structures for glufosinate-based herbicide mixes in North America. Its holistic crop protection approach positions glufosinate as a core burndown tool in minimum-tillage systems aligned with carbon sequestration objectives. Through coordinated seed technology sheets and agronomic guidance, Syngenta reinforces glufosinate’s role within sustainable and resistance-managed herbicide programs.

China: Scale-Driven Manufacturing Leadership and Isomer Transition

China has consolidated its position as the global manufacturing backbone for glufosinate ammonium, underpinned by an unprecedented expansion in technical grade capacity. By August 2025, national TC capacity reached approximately 154,970 tonnes per year, nearly tripling levels recorded in 2021. This rapid scale-up reflects China’s strategic prioritization of non-selective herbicides as glyphosate alternatives, particularly for export-oriented markets. Despite the surge in output, pricing dynamics stabilized through Q3 2025, with TC prices holding near USD 6,472 per tonne in September. The limited decline from early-2025 levels signals a transition from cyclical volatility toward a more balanced supply-demand environment.

A parallel structural shift is underway toward L-glufosinate production, which aligns with China’s Zero Growth policy for chemical pesticides. Producers such as Lier Chemical and Seven Continent are investing in higher-purity isomer output that delivers equivalent weed control at roughly half the dosage of racemic formulations. Export momentum remains strong, with overseas shipments rising more than 41% year on year through July 2025, driven by herbicide-tolerant crop adoption in Southeast Asia and South America. Intelligent manufacturing is reinforcing competitiveness, as AI-enabled automation is being deployed across multi-site production networks to optimize energy efficiency and chemical yield.

United States: Formulation Innovation and Regulatory Enablement

The United States glufosinate ammonium market is increasingly shaped by formulation-led differentiation and regulatory clarity. In 2025, BASF Agricultural Solutions advanced its Liberty ULTRA platform, deploying the product across more than 60 million acres of canola, corn, and cotton. The Liberty Lock formulation system delivers materially improved weed control performance versus generic products, reinforcing glufosinate’s role as a premium post-emergence solution in herbicide-tolerant cropping systems. Complementing product innovation, BASF introduced targeted 0 percent APR financing programs for 2026, easing grower adoption amid elevated input costs.

Regulatory developments have further strengthened market confidence. The Environmental Protection Agency finalized new tolerance levels for glufosinate residues in rice and tea commodities in November 2025, smoothing international trade flows for treated crops. Full EPA registration of Glufosinate-P in 2025 marked a pivotal milestone, enabling lower active-ingredient loading while preserving efficacy for the 2026 planting season. At the trait stewardship level, Corteva Agriscience has mandated stricter mode-of-action rotation and integrated weed management protocols to protect the long-term viability of glufosinate-tolerant seed technologies.

India: Regulatory Tightening and Indigenous Production Drive

India’s glufosinate ammonium landscape is defined by heightened regulatory oversight and a strategic push toward domestic technical manufacturing. During its 467th meeting in October 2025, the Central Insecticides Board and Registration Committee intensified scrutiny of manufacturing licenses, focusing on transparency and revalidation of technical registrations. This move reflects a broader policy objective to secure supply chain integrity while managing the rapid expansion of herbicide usage in conservation agriculture systems.

On the commercial front, UPL Limited expanded its Sweep Power brand in early 2025, positioning glufosinate ammonium as a cornerstone of climate-smart agriculture and reduced-till farming. India is simultaneously accelerating approvals for indigenous technical production under fast-tracked registration pathways, reducing dependence on Chinese imports and supporting local refineries capable of producing high-purity isomers. The approval of complementary bio-pesticides such as Trichoderma harzianum for integrated pest management underscores a policy-driven emphasis on combining chemical and biological tools for the 2026 rabi season.

Brazil: Volume Demand Anchored by GM Crop Adoption

Brazil has emerged as one of the most strategically important demand centers for glufosinate ammonium, supported by high penetration of genetically modified, herbicide-tolerant crops. By 2025, approximately one-quarter of the national soybean area was planted with glufosinate-resistant varieties, creating sustained volume demand and positioning Brazil as a focal market for global pricing strategies. This scale of adoption reinforces glufosinate’s role in resistance management programs where glyphosate efficacy has declined.

Regulatory and infrastructure developments are shaping supply dynamics. The Ministry of Agriculture is encouraging a transition toward L-glufosinate to reduce overall chemical load in sensitive biomes such as the Amazon and Cerrado. Concurrently, multinational suppliers have expanded regional formulation and blending hubs to bypass congestion at the Port of Santos, shortening lead times and improving supply reliability for the 2026 planting cycles.

European Union: Residue Surveillance and Precautionary Controls

Within the European Union, glufosinate ammonium is operating under an increasingly precautionary regulatory framework. Regulation (EU) 2025/854 has established a coordinated control program for 2026 to 2028, mandating systematic monitoring of pesticide residues across plant and animal origin products. This regime places glufosinate under intensified scrutiny as part of broader consumer exposure assessments aligned with the Green Deal objectives.

In parallel, the European Food Safety Authority highlighted data gaps in late 2025 concerning long-term mammalian risk for certain herbicides. These findings are translating into stricter application guidelines and stewardship requirements for glufosinate use in 2026. While this environment constrains volume growth, it favors higher-efficiency formulations and isomer-specific products that can meet efficacy targets at lower application rates.

Regional Snapshot: Glufosinate Ammonium Industry Dynamics

Glufosinate Ammonium Market County Level Snapshot

|

Region

|

Strategic Focus

|

Key Industry Direction

|

|

China

|

TC capacity scale and L-isomer transition

|

Export-driven manufacturing with AI-enabled efficiency

|

|

United States

|

Premium formulations and regulatory clarity

|

Trait stewardship and grower financing support

|

|

India

|

License revalidation and local production

|

Indigenous technical manufacturing with IPM integration

|

|

Brazil

|

GM crop penetration and logistics

|

Volume demand supported by regional formulation hubs

|

|

European Union

|

Residue monitoring and risk controls

|

Lower-dose, high-efficiency application frameworks

|

Glufosinate Ammonium Market Report Scope

Glufosinate Ammonium Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$548.6 Million

|

|

Market Size (2034)

|

$1231.4 Million

|

|

Market Growth Rate

|

9.4%

|

|

Segments

|

By Type (Conventional Glufosinate Ammonium, L-Glufosinate Ammonium), By Formulation (Soluble Liquid, Suspension Concentrate, Water Dispersible Granules), By Crop Type (Genetically Modified Crops, Non-Genetically Modified Crops), By Application (Agricultural Use, Non-Agricultural Use)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Bayer AG, Lier Chemical Co., Ltd., UPL Limited, Corteva Agriscience, Zhejiang Yongnong Chemical Industry Co., Ltd., Seven Continent Green Chemical Co., Ltd., Nufarm Limited, Jiangsu Huifeng Bio Agriculture Co., Ltd., Limin Chemical Co., Ltd., SinoHarvest Corporation, Shandong Luba Chemical Co., Ltd., Veyong, Syngenta AG, Adama Agricultural Solutions

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Glufosinate Ammonium Market Segmentation

By Type

- Conventional Glufosinate Ammonium

- L-Glufosinate Ammonium

By Formulation

- Soluble Liquid

- Suspension Concentrate

- Water Dispersible Granules

By Crop Type

- Genetically Modified Crops

- Non-Genetically Modified Crops

By Application

- Agricultural Use

- Non-Agricultural Use

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Glufosinate Ammonium Industry

- BASF SE

- Bayer AG

- Lier Chemical Co., Ltd.

- UPL Limited

- Corteva Agriscience

- Zhejiang Yongnong Chemical Industry Co., Ltd.

- Seven Continent Green Chemical Co., Ltd.

- Nufarm Limited

- Jiangsu Huifeng Bio Agriculture Co., Ltd.

- Limin Chemical Co., Ltd.

- SinoHarvest Corporation

- Shandong Luba Chemical Co., Ltd.

- Veyong

- Syngenta AG

- Adama Agricultural Solutions

*- List not Exhaustive