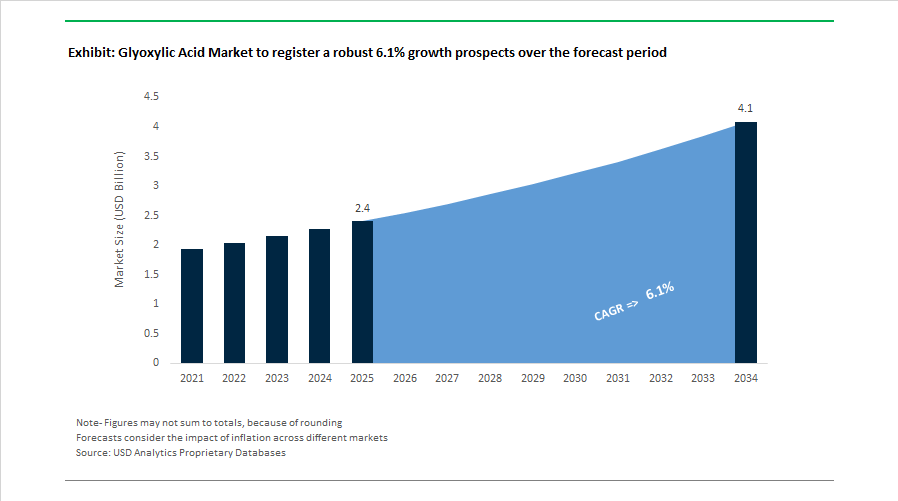

Glyoxylic Acid Market to Reach $4.1 Billion by 2034 at 6.1% CAGR Amid Vanillin Surge, EU Regulatory Scrutiny, and Pharma Intermediate Expansion

The Glyoxylic Acid Market is projected to grow from $2.4 billion in 2025 to $4.1 billion by 2034, registering a CAGR of 6.1%. Market growth is being shaped by strong demand for vanillin synthesis, pharmaceutical intermediates such as p-hydroxyphenylglycine, agrochemical building blocks, and emerging formaldehyde-free wood resin systems. At the same time, regulatory scrutiny in Europe regarding cosmetic applications and anti-dumping investigations on Chinese imports are materially influencing trade flows, pricing, and supply chain risk management strategies.

In early 2024, WeylChem Group completed a €15 million upgrade of its glyoxal production facility in Lamotte, France, increasing output by one-third and lowering carbon emissions by 20%. As one of only two European suppliers, the expansion strengthened regional security of supply for polymer and agrochemical precursors. In 2024, BASF SE optimized its Nanjing production network for high-purity C2 organic acids, indirectly reinforcing availability of glyoxylic acid for pharmaceutical and water treatment applications in Asia. During the same year, Hubei Hongyuan Pharmaceutical Co., Ltd. increased production of 50% pharmaceutical-grade glyoxylic acid to meet global demand for p-hydroxyphenylglycine used in amoxicillin manufacturing. In July 2024, the European Commission initiated an anti-dumping probe into Chinese glyoxylic acid imports, introducing uncertainty around potential tariffs and shifting procurement strategies among EU buyers.

Regulatory developments intensified in late 2024 and early 2025. In October 2024, ANSES issued an emergency alert linking glyoxylic acid-based hair straightening products to acute renal failure cases. In January 2025, ANSES formally recommended that French authorities propose an EU-wide restriction or ban on glyoxylic acid in cosmetic applications, potentially affecting the European hair-care segment. Concurrently, late 2024 and early 2025 logistics disruptions in the Red Sea constrained cargo inflows into European ports such as Hamburg, driving temporary inventory shortages and upward price pressure for pharmaceutical and fine chemical users. Market data from early 2025 indicated that vanillin production accounts for approximately 50–60% of total glyoxylic acid consumption, reflecting sustained growth in food flavorings and fragrance intermediates transitioning away from traditional petrochemical routes.

Product innovation and application diversification gained momentum in 2025–2026. In mid-2025, producers introduced low-impurity glyoxylic acid grades engineered to comply with updated FDA and EMA residue standards for vanillin and pharmaceutical excipients. Throughout 2025, wood-panel manufacturers piloted glyoxylic acid as a formaldehyde replacement cross-linker in resin systems to meet stricter indoor air emission regulations. In January 2026, IRO Group Inc. released updated technical specifications for glyoxylic acid 50%, establishing higher purity and reaction stability benchmarks for agrochemical synthesis, particularly herbicides and plant growth regulators requiring precise intermediate performance.

The Glyoxylic Acid Market outlook reflects vanillin-driven consumption concentration, pharmaceutical intermediate capacity expansion, anti-dumping trade realignments, cosmetic regulatory headwinds in Europe, logistics-driven price volatility, and substitution of formaldehyde in wood resins. Competitive differentiation increasingly depends on pharmaceutical-grade purity, low-residue compliance, carbon footprint reduction, diversified regional supply chains, and technical-grade consistency tailored to agrochemical and flavor synthesis requirements.

Glyoxylic Acid Market Trends and Strategic Growth Opportunities

Pharma-Grade Glyoxylic Acid Scaling Anchors Long-Term Demand Stability

The glyoxylic acid market continues to be structurally anchored by pharmaceutical manufacturing, which accounted for approximately 32.1% of global consumption by late 2024. Glyoxylic acid remains a non-substitutable intermediate in the synthesis of phenylglycine derivatives used in widely prescribed antibiotics such as amoxicillin and ampicillin, as well as in select cardiovascular and metabolic drugs. As global healthcare systems prioritize local API security and backward integration, demand is shifting decisively toward pharma-grade glyoxylic acid with tightly controlled impurity profiles.

To mitigate supply chain risk and cost volatility, production capacity is increasingly concentrated within large-scale chemical parks that offer feedstock integration and logistics advantages. Zhonglan Industry has emerged as a key supplier, reaching an estimated production capacity of 5,500 metric tons per month by late 2024. Its output is primarily focused on 50% concentration grades optimized for high-throughput API synthesis in India and China. This concentration level balances transport efficiency with downstream process compatibility, making it the preferred format for large-volume pharmaceutical customers.

Clinical innovation is reinforcing this trend. Controlled-release and modified-release drug formulations increasingly rely on glyoxylic acid for precise molecular tailoring that enhances bioavailability and pharmacokinetic stability. As a result, India’s rapidly expanding API sector prioritized procurement of consistent 50% grades throughout 2025. At a global level, production remains highly concentrated, with more than 80% of installed capacity located in coastal Chinese provinces such as Shandong and Jiangsu. These integrated clusters benefit from economies of scale that are estimated to be 20 to 25% more cost-efficient than Western standalone plants, reinforcing Asia’s structural advantage in glyoxylic acid supply.

Feedstock Volatility and Maleic Anhydride Dependency Tighten Supply Conditions

The glyoxylic acid supply chain remains tightly coupled to upstream glyoxal availability, which itself depends on the economics of maleic anhydride and n-butane feedstocks. Structural shifts in the global maleic anhydride market are therefore having a direct impact on glyoxylic acid pricing and availability. In Europe, supply has tightened significantly following the mid-2025 closure of Huntsman’s Moers facility and the shutdown of Bosnia-based GIKIL’s 12 kilotons-per-year plant in October 2025. These closures have increased Europe’s reliance on Asian imports, exposing buyers to freight costs and spot-market volatility.

In North America, maleic anhydride pricing remained relatively balanced but trended upward in late 2025. The regional price index increased by approximately 5.07% quarter over quarter, reaching an average of 1,286 dollars per metric ton, driven by steady n-butane pricing and export flows. This tightening feeds directly into cost-plus pricing models used by glyoxylic acid producers. By contrast, China experienced a 2.2% decline in maleic anhydride prices following plant restarts in Shandong, creating a pronounced regional divergence. As a result, global procurement managers are increasingly adopting region-specific sourcing strategies and flexible contract structures to hedge against localized surpluses or shortages.

Agrochemical Intermediates and Plant Growth Regulators Drive Portfolio Diversification

Beyond pharmaceuticals, glyoxylic acid is gaining strategic importance as a core building block in agrochemical value chains. It is a critical precursor for iminodiacetic acid, the key intermediate in glyphosate production and in newer herbicide classes such as HPPD inhibitors. As regulatory scrutiny intensifies around persistent crop protection chemicals, R&D investment is shifting toward bio-based and biodegradable alternatives. Bio-derived glyoxylic acid is increasingly evaluated for use in sustainable herbicide formulations, agricultural coatings, and biodegradable polymer systems.

Process innovation is further expanding opportunity. Catalytic efficiency improvements reported in 2025 have increased yields of allantoin, a glyoxylic acid derivative used in specialty fertilizers to enhance seed germination and root development. This application is opening a new active-ingredient revenue stream that sits between traditional agrochemicals and plant nutrition. European producers such as Akema S.r.l. and WeylChem are actively expanding portfolios of high-purity 50H grades specifically engineered for agro-intermediates, where trace contaminants can compromise formulation stability and field performance.

Clean Beauty Actives and Aroma Chemicals Unlock High-Margin Demand

The clean beauty movement is creating a fast-growing opportunity for glyoxylic acid as a gentler, multifunctional alternative to traditional petrochemical alpha hydroxy acids. Bio-based glyoxylic acid derived from renewable sugars and biomass is increasingly positioned as a low-irritation exfoliating and anti-aging active for premium skincare formulations. This sustainability-driven shift is particularly pronounced in Europe, where cosmetic retail sales reached approximately 96 billion euros in 2023 and brand owners are under mounting pressure to meet carbon neutrality and ingredient transparency targets.

Aroma and fragrance applications represent another high-margin growth channel. Approximately 28% of global glyoxylic acid consumption in the aroma sector is linked to vanillin synthesis, a cornerstone ingredient in flavor and fragrance formulations. With the global flavor and fragrance industry expanding at an estimated 4.8% annually through 2025, demand for high-purity glyoxylic acid as a reliable building block for natural-identical vanillin is rising steadily. In personal care, high-purity 99% glyoxylic acid is also gaining traction in formaldehyde-free hair straightening and repair treatments. These formulations deliver effective hair restructuring while complying with increasingly stringent occupational safety and consumer health regulations, positioning glyoxylic acid as a critical ingredient at the intersection of sustainability, performance, and regulatory compliance.

Glyoxylic Acid Market Share and Segmentation Insights

Vanillin and Ethyl Vanillin Production Drives the Largest Derivative Segment in the Glyoxylic Acid Market

Vanillin and Ethyl Vanillin accounted for 42.80% of the Glyoxylic Acid Market share in 2025, making this derivative category the dominant demand center for glyoxylic acid. Glyoxylic acid serves as a critical intermediate in the glyoxylic acid synthesis route for vanillin production, a process widely used by flavor and fragrance manufacturers due to its cost efficiency, high yield, and consistent product quality. Synthetic vanillin and ethyl vanillin are among the most widely consumed aroma molecules globally, used extensively in food products, beverages, confectionery, baked goods, dairy desserts, perfumes, and personal care formulations. The glyoxylic acid pathway has gained prominence because it produces high-purity vanillin suitable for large-scale commercial flavor production while maintaining competitive production costs. In 2025, market dynamics are increasingly influenced by the growing demand for natural-identical flavor ingredients. Manufacturers are developing bio-based glyoxylic acid production routes derived from renewable feedstocks, allowing flavor houses to produce vanillin with renewable origin claims while preserving the scalability and affordability associated with synthetic vanillin production.

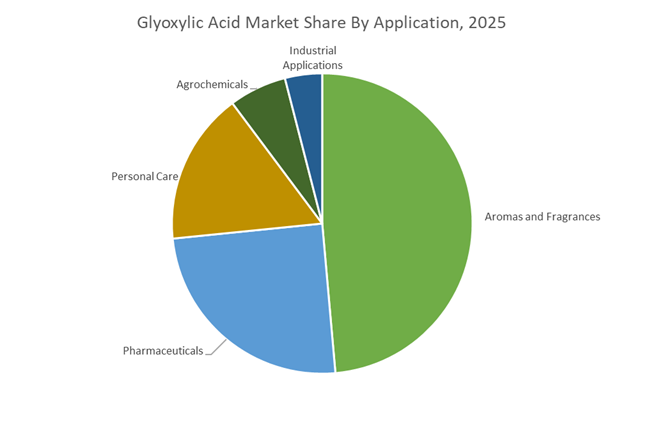

Aromas and Fragrances Lead the Glyoxylic Acid Market Through Global Flavor Ingredient Demand

Aromas and Fragrances represented 48.60% of the Glyoxylic Acid Market share in 2025, making it the largest application segment for glyoxylic acid derivatives. The compound is primarily consumed in the production of vanillin and ethyl vanillin, which are essential ingredients used in the flavoring and fragrance industry. Vanillin is one of the most widely used flavor molecules worldwide, appearing in chocolate products, bakery items, beverages, ice cream, confectionery, and flavored dairy products, while also serving as a fragrance ingredient in perfumes, cosmetics, and household products. As global consumption of processed foods and scented consumer goods continues to expand, demand for glyoxylic acid as a key precursor in vanillin synthesis remains strong. In 2025, sustainability initiatives across the flavor and fragrance industry are driving increased interest in renewable sourcing of key raw materials. Leading fragrance and flavor houses are investing in bio-based glyoxylic acid production pathways derived from renewable feedstocks such as glycolic acid or tartaric acid, enabling the development of renewably sourced vanillin ingredients that support clean label and sustainability claims in consumer products.

Competitive Landscape in Glyoxylic Acid Market

Arkema Leads Premium-Purity Glyoxylic Acid Production

Arkema operates as the global benchmark supplier of high-purity glyoxylic acid, holding approximately 30.4% of global market value as of early 2026. Its proprietary maleic anhydride ozone oxidation process delivers significantly lower impurity profiles compared to the conventional glyoxal-based route. The company primarily supplies 50% and 40% aqueous solutions tailored for vanillin synthesis, fine fragrance intermediates, and pharmaceutical applications requiring strict impurity control. In 2026, Arkema is positioning its European production base as a low-carbon intermediate platform aligned with the European Green Deal. Its focus on premium-grade glyoxylic acid strengthens supply reliability for regulated North American and European healthcare markets.

WeylChem Strengthens European Pharma-Grade Customization

WeylChem International GmbH serves as the principal European alternative to Arkema in pharmaceutical-grade glyoxylic acid. The company emphasizes vertical customization, developing tailored derivatives for advanced herbicides and plant growth regulators. In 2026, WeylChem is expanding distribution channels in North America to benefit from pharmaceutical companies adopting China+1 procurement strategies. Its high-stability technical grades are optimized to minimize polymerization risk during storage and long-distance transport. This specialization enhances WeylChem’s competitiveness in regulated agrochemical and pharmaceutical supply chains requiring consistent purity and stability.

Hubei Hongyuan Integrates Glyoxylic Acid with API Manufacturing

Hubei Hongyuan Pharmaceutical Technology Co., Ltd., listed on the Shenzhen Stock Exchange, remains one of the top three global volume producers. With a market capitalization near 8.72 billion CNY in early 2026, glyoxylic acid serves as a key driver of its pharmaceutical intermediates revenue. The company leverages captive glyoxylic acid production for atenolol and amoxicillin intermediates, preserving cost advantages in API synthesis. During 2025 and 2026, it expanded into higher-value industrial grade applications for textiles and leather tanning, where biodegradable cross-linkers are gaining adoption. Vertical integration into active pharmaceutical ingredients differentiates Hongyuan within the Chinese supply ecosystem.

Qingdao Guolin Advances Ozone-Based Cost Leadership

Qingdao Guolin Technology Group Co., Ltd. has emerged as a technological disruptor through its large-scale ozone oxidation platform operated by Xinjiang Guolin New Materials. By refining ozone-based maleic anhydride oxidation at industrial scale, Guolin produces high-purity glyoxylic acid at competitive cost levels. By 2026, the company is expanding crystalline glyoxylic acid production to reduce transportation weight and improve product stability. Its Xinjiang hub is scaling capacity to serve the global vanillin precursor market, particularly for food and beverage applications. The firm’s quality-cost leadership strategy positions it as a rising competitor to established European producers.

Jiaxing Zhonghua Secures Closed-Loop Vanillin Integration

Jiaxing Zhonghua Chemical Co., Ltd. operates through its dominance in synthetic vanillin production. Most of its glyoxylic acid output is internally consumed for ethyl vanillin synthesis, forming a closed-loop integration model that mitigates raw material price volatility. In 2026, the company is advancing its Green Flavor initiative by deploying enzymatic and improved catalytic processes to lower wastewater intensity during oxidation steps. Strategic partnerships with global fragrance houses rely on traceable glyoxylic acid feedstocks to meet sustainability certification standards. Its integration across the flavor and fragrance value chain reinforces supply security and cost stability in vanillin markets worldwide.

China: Cost Leadership Anchored by Vanillin and Agrochemical Integration

China continues to anchor the global glyoxylic acid industry through a combination of policy support, feedstock integration, and downstream dominance. Under the 2025–2026 Petrochemical Stabilization Plan issued by the Ministry of Industry and Information Technology, subsidies are being selectively directed toward high-end fine chemicals such as glyoxylic acid, while discouraging excess investment in legacy coal-to-methanol capacity. This policy framework has helped stabilize margins and redirected capital toward value-added oxidation chemistry.

Shandong and Jiangsu remain the most competitive production hubs globally, benefiting from tight vertical integration with glyoxal and nitric acid units. As a result, Chinese producers are operating at production costs estimated to be 20% to 25% below Western benchmarks, reinforcing China’s export competitiveness. In late 2025, Guolin New Materials commissioned new high-purity crystalline glyoxylic acid lines following its successful European market entry. These lines are specifically aligned with clean-label vanillin synthesis, a segment that now absorbs roughly 28% of China’s domestic glyoxylic acid consumption. Parallel optimization of p-hydroxyphenylglycine synthesis has strengthened China’s position in antibiotics and herbicide intermediates ahead of the 2026 export cycle.

France: Sustainability-Driven Specialty and Cosmetic Supply

France has emerged as Europe’s reference point for sustainably manufactured glyoxylic acid, particularly for cosmetic and pharmaceutical applications. At its Trosly-Breuil site, WeylChem Lamotte S.A.S. completed ISO 50001 energy efficiency upgrades in late 2025, materially lowering the carbon intensity of its proprietary C2 oxidation process. This capability has positioned the facility as a preferred supplier for European brands prioritizing traceable, low-emission ingredient sourcing.

The company’s EcoVadis Platinum certification in 2025 further strengthened its standing with premium cosmetic formulators using glyoxylic acid in hair straightening systems and dermatological peels. Looking ahead to 2026, French chemical clusters are piloting enzymatic and bio-catalytic oxidation routes designed to replace nitric acid pathways altogether. These initiatives aim to eliminate NOx emissions while improving batch-to-batch purity, particularly for medical-grade glyoxylic acid destined for active pharmaceutical ingredient synthesis.

India: Pharmaceutical Pull and Regulatory Tightening

India’s glyoxylic acid market is increasingly shaped by pharmaceutical integration and evolving chemical governance. Under the Production Linked Incentive framework, domestic API manufacturers have increased procurement of 50% glyoxylic acid solutions for the synthesis of beta-lactam antibiotics such as amoxicillin and ampicillin. This trend reflects India’s broader strategy to localize critical intermediates ahead of patent cliffs and export expansion in 2026.

On the supply side, Amzole India announced capacity and infrastructure enhancements in 2025 to serve rising demand from the personal care and aroma chemical segments. At the regulatory level, India’s upcoming Chemical Management and Safety Rules will introduce REACH-like requirements by mid-2026. These rules will impose stricter stability, impurity, and documentation standards for glyoxylic acid monohydrate, increasing compliance costs for importers and accelerating the shift toward qualified domestic suppliers.

United States: Stable Pricing and Application-Specific Oversight

The United States glyoxylic acid industry in 2025 has been characterized by pricing stability and application-driven regulation. Domestic prices remained steady through Q4 2025, supported by consistent imports from Asian production hubs and predictable demand from the Permian Basin, where glyoxylic derivatives are used in specialty water treatment biocides.

From an industrial perspective, BASF confirmed that its Cincinnati bio-based surfactant expansion, scheduled for completion in 2026, will increase availability of alkyl polyglucosides and chelating systems that rely on organic acid intermediates such as glyoxylic derivatives. At the same time, regulatory scrutiny has intensified in personal care. The U.S. Human Foods Program issued updated 2025 guidance on professional hair straightening formulations, setting explicit concentration limits for glyoxylic acid to mitigate formaldehyde-related off-gassing risks, thereby raising formulation and compliance requirements for salons and manufacturers.

Germany: Contract Synthesis and Energy-Efficient Concentration

Germany’s role in the glyoxylic acid industry is centered on advanced intermediates and contract development for sustainable polymers. In late 2025, WeylChem International GmbH showcased expanded platforms for the synthesis of glyoxylic acid salts and functional esters tailored to biodegradable polymer systems, aligning with EU circular economy objectives.

Manufacturing efficiency is also a priority. German producers are adopting Mechanical Vapor Recompression technology in 50% solution concentration units, targeting a 12% reduction in steam consumption by the end of 2026. This shift is driven by both energy cost pressures and national sustainability mandates that increasingly favor low-emission fine chemical production over conventional thermal evaporation methods.

Japan: Precision Applications in Electronics and Aging-Care Formulations

Japan represents a niche but strategically important glyoxylic acid market driven by precision cleaning and demographic-led skincare demand. In 2025, Japanese chemical firms expanded the use of 70% technical-grade glyoxylic acid for cleaning sensitive electronic components and heavy machinery, displacing more aggressive mineral acids such as hydrochloric acid to reduce corrosion and residue risks.

Demographics are shaping downstream demand. With over 29% of the population aged 65 and above, Japan has seen a marked increase in demand for anti-aging creams and masks formulated with high-purity glyoxylic acid monohydrate. This has led to increased imports of pharmaceutical and cosmetic-grade material from European suppliers, reinforcing Japan’s position as a high-purity, regulation-sensitive end market rather than a volume producer.

Comparative Snapshot: Glyoxylic Acid Industry by Country

Glyoxylic Acid Market County Level Snapshot

|

Country / Region

|

Primary Strategic Focus

|

Structural Impact on Industry

|

|

China

|

Cost leadership and vanillin integration

|

Global supply backbone with agrochemical depth

|

|

France

|

Sustainable cosmetic and pharma sourcing

|

Premium supplier for low-carbon formulations

|

|

India

|

API localization and regulatory alignment

|

Rising domestic demand with compliance-driven shifts

|

|

United States

|

Application oversight and price stability

|

Steady consumption in water treatment and care

|

|

Germany

|

Contract intermediates and energy efficiency

|

Advanced derivatives for biodegradable polymers

|

|

Japan

|

Precision electronics and aging-care demand

|

High-purity, specialty consumption hub

|

Glyoxylic Acid Market Report Scope

Glyoxylic Acid Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.4 Billion

|

|

Market Size (2034)

|

$4.1 Billion

|

|

Market Growth Rate

|

6.1%

|

|

Segments

|

By Derivative Type (Allantoin, Vanillin, Ethyl Vanillin, p-Hydroxyphenylglycine, Heliotropin), By Grade (Technical Grade, Pharmaceutical Grade, Cosmetic Grade), By Product Form (Liquid Solution, Crystalline Form), By Application (Aromas and Fragrances, Pharmaceuticals, Personal Care, Agrochemicals, Industrial Applications)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

WeylChem International GmbH, BASF SE, Zhonglan Industry Co., Ltd., Hubei Hongyuan Pharmaceutical Technology Co., Ltd., Akema Fine Chemicals, Guolin New Materials, Stan Chemicals, Haihang Industry Co., Ltd., Zhonghua Chemical, Amzole India Pvt. Ltd., Hefei TNJ Chemical Industry Co., Ltd., Labeyond Chemicals Co., Ltd., Arkema S.A., Huntsman Corporation, Japan Glycols

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Glyoxylic Acid Market Segmentation

By Derivative Type

- Allantoin

- Vanillin

- Ethyl Vanillin

- p-Hydroxyphenylglycine

- Heliotropin

By Grade

- Technical Grade

- Pharmaceutical Grade

- Cosmetic Grade

By Product Form

- Liquid Solution

- Crystalline Form

By Application

- Aromas and Fragrances

- Pharmaceuticals

- Personal Care

- Agrochemicals

- Industrial Applications

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Glyoxylic Acid Industry

- WeylChem International GmbH

- BASF SE

- Zhonglan Industry Co., Ltd.

- Hubei Hongyuan Pharmaceutical Technology Co., Ltd.

- Akema Fine Chemicals

- Guolin New Materials

- Stan Chemicals

- Haihang Industry Co., Ltd.

- Zhonghua Chemical

- Amzole India Pvt. Ltd.

- Hefei TNJ Chemical Industry Co., Ltd.

- Labeyond Chemicals Co., Ltd.

- Arkema S.A.

- Huntsman Corporation

- Japan Glycols

*- List not Exhaustive