Market Overview: Co-Product Supply Inelasticity and Mission-Critical End Uses Are Structuring the Global Hafnium Market

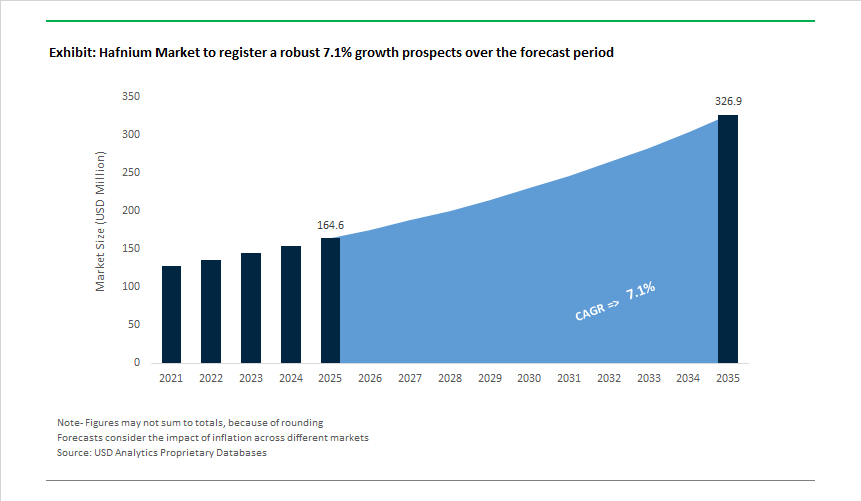

The Global Hafnium Market is valued at USD 164.6 million in 2025 and is projected to reach USD 326.8 million by 2035, expanding at a 7.1% CAGR as hafnium consolidates its role as a strategic, non-substitutable material across aerospace propulsion, advanced semiconductors, hypersonics, and nuclear systems. Today, market dynamics are not volume-driven; they are defined by structural supply rigidity and high-value, low-tolerance demand.

Hafnium’s defining characteristic is its inelastic supply structure. Global output is generated exclusively as a co-product of zirconium refining, at a relatively fixed ratio of approximately 1 part hafnium to 50 parts zirconium. This means supply cannot respond elastically to price signals or demand surges. Even when hafnium demand accelerates, production remains constrained by zirconium end-market economics and refinery separation capacity. As a result, the market is structurally prone to periodic tightness, price volatility, and strategic procurement risk, particularly for industries requiring ultra-high-purity grades.

On the demand side, aerospace and propulsion systems anchor long-term consumption. Nickel-based superalloys used in gas turbines and jet engines are increasingly formulated with 1-2% hafnium additions to stabilize grain boundaries and enhance creep resistance under extreme “hot-end” operating conditions. As turbine inlet temperatures continue to rise to improve efficiency and thrust-to-weight ratios, hafnium loading is not declining; it is becoming structurally embedded in next-generation engine design. This ties hafnium demand directly to global aircraft production, defense aviation programs, and gas turbine installations.

Defense and advanced materials applications further elevate hafnium’s strategic profile. Hafnium carbide (HfC), with a melting point near 3,890°C-the highest of any known binary compound, is now central to ultra-high-temperature ceramic (UHTC) systems used in hypersonic vehicles, re-entry systems, and advanced propulsion components. These applications operate in thermal regimes where substitution is not technically feasible, locking hafnium into long program lifecycles with limited supplier optionality.

Semiconductor manufacturing represents another non-negotiable demand pillar. Hafnium oxide (HfO₂) is the industry-standard high-k gate dielectric, enabling transistor scaling at 7 nm nodes and below, which underpins logic density growth for AI accelerators, high-performance computing (HPC), and advanced mobile processors. As chip architectures continue to scale and AI workloads intensify, hafnium demand remains directly linked to wafer starts, node transitions, and dielectric stack complexity, rather than cyclical consumer electronics trends.

Nuclear energy provides long-duration demand stability. Hafnium’s neutron absorption cross-section is roughly 60× higher than zirconium, making it one of the most effective materials for reactor control rods and neutron-absorbing components. As nuclear fleets extend operating lifetimes and new reactors are planned in selected regions, reactor-grade hafnium maintains a steady, qualification-driven demand profile insulated from short-term market fluctuations.

Market Analysis: Supply-Side Shockwaves, Aerospace-Semiconductor Demand Acceleration, and Government Supply Chain Interventions

The global Hafnium industry underwent significant pricing, policy, and demand realignment during 2024-2025. In October 2025, Argus Media reported a dramatic 38% month-on-month price spike in Europe, pushing Hafnium close to $5,800/kg, driven by a perfect storm of electronics and gas turbine demand combined with Chinese export licensing restrictions. The effect was immediate: Western buyers accelerated stockpiling, semiconductor manufacturers tightened procurement cycles, and aerospace companies renewed long-term supply agreements. In September 2025, demand surged further when analysts confirmed that global gas turbine orders-driven partly by power generation expansion for AI datacenters-reached 80 GW, marking unprecedented requirements for Hafnium-containing nickel superalloys.

Governments responded rapidly to supply-chain vulnerabilities. In July 2025, the U.S. Department of Defense launched new grant funding programs to strengthen domestic Zirconium-Hafnium refining capabilities, directly targeting dependence on foreign co-product supply chains. Similarly, China’s formal implementation of dual-use export controls in June 2025 slowed the movement of unwrought Hafnium into global markets, reinforcing its strategic status. On the other hand, the semiconductor ecosystem received a boost when Materion introduced ultra-high purity HfO₂ sputtering targets in April 2025, engineered specifically for next-generation ALD processes used in 7 nm and sub-7 nm nodes. Parallel to this, research breakthroughs in February 2025 revealed new Hafnium Carbonitride (HfCN) compounds synthesized at lower processing temperatures, opening new pathways for advanced hypersonic UHTC materials.

On the supply front, stabilization efforts progressed as Framatome confirmed in January 2025 that maintenance at the Jarrie Zirconium facility was nearing completion, with Hafnium output expected to normalize by mid-year-a relief to nuclear and aerospace buyers. Longer-term diversification gained momentum when Australian Strategic Materials (ASM) secured major funding in November 2024 for Phase 2 of the Dubbo Project, one of the few Western candidates capable of providing an independent zirconium-hafnium supply chain.

Hafnium Market Trends and Opportunities

Trend 1: Qualification of Hafnium-Aluminide Environmental Barrier Coatings for Next-Generation Jet Engines

The aerospace sector is entering a new materials qualification cycle as engine OEMs push turbine inlet temperatures beyond the limits of conventional nickel-based superalloys to unlock fuel efficiency gains and compatibility with Sustainable Aviation Fuels (SAF). The increasing use of Silicon Carbide (SiC) Ceramic Matrix Composites (CMCs) in hot-section components—already visible in engines such as the GE9X and LEAP—has fundamentally shifted the role of coatings from oxidation resistance to full environmental barrier protection. In 2025, engine certification data indicates that hafnium-aluminide (HfAl) intermetallic coatings are becoming indispensable, as they form stable, slow-growing oxide scales that protect CMC substrates from water-vapor-driven recession at temperatures exceeding 1,300 °C. Without hafnium-based EBCs, CMC blades and vanes experience rapid surface degradation, eroding the very efficiency benefits they are designed to deliver. This trend is reinforced by supply-side realities: refined hafnium capacity remains highly concentrated, with France’s Jarrie refinery accounting for roughly 43% of global output and supplying key European aerospace programs. At the same time, defense and space applications are accelerating qualification timelines. During 2024–2025, U.S. DoD and NASA programs expanded the use of hafnium-niobium alloys in ultra-high-temperature ceramics for hypersonic vehicles and rocket nozzles, where hafnium’s 2,233 °C melting point provides a critical thermal safety margin. Collectively, these developments are repositioning hafnium from a niche alloying element to a strategic aerospace material tied directly to propulsion efficiency, mission endurance, and thermal survivability.

Trend 2: Rising Hafnium Intensity in Advanced Semiconductor Logic and Etch Processes

The semiconductor industry’s migration to sub-3 nm logic nodes is structurally increasing hafnium consumption per wafer, reversing earlier assumptions that scaling would reduce high-k material usage. As of late 2025, leading foundries have committed to Gate-All-Around (GAA) nanosheet transistor architectures for 3 nm and 2 nm nodes, replacing FinFETs. These designs dramatically increase effective surface area, requiring highly conformal, angstrom-level thin films deposited via Atomic Layer Deposition (ALD). Hafnium oxide has emerged as the dominant high-k dielectric in this transition, not only because of its dielectric performance but also due to its proven reliability under extreme electric fields. At the same time, hafnium’s role is expanding beyond the transistor gate stack. Advanced plasma etch tools used for high-aspect-ratio features in 3D NAND and next-generation DRAM increasingly specify hafnium-based chamber linings and hard masks. In 2025, fab-level data shows that plasma-resistant hafnium oxide coatings extend etch chamber component lifetimes by more than 25% compared to yttrium-based alternatives, directly improving tool uptime and yield stability. This trend is amplified by the explosive growth of AI and data-center processors, where power densities continue to rise as transistor densities exceed 200 million/mm². Hafnium-enabled high-k metal gate (HKMG) stacks are now essential for suppressing gate leakage and managing thermal loads in high-performance computing chips, embedding hafnium deeper into the economics of advanced logic manufacturing.

Opportunity 1: Hafnium Control Rods as a Core Enabler of Small Modular and Advanced Reactors

The global push to deploy Small Modular Reactors (SMRs) and next-generation nuclear systems is creating a high-value opportunity for hafnium as a critical nuclear safety material. Hafnium’s exceptionally high neutron absorption cross-section, combined with its ability to absorb neutrons without producing helium gas, gives it a decisive advantage over boron-based alternatives. In compact SMR cores—where space is constrained and refueling intervals are extended—this property prevents swelling, cracking, and long-term degradation of control rods. In March 2025, the allocation of HALEU fuel by the U.S. Department of Energy to multiple advanced reactor developers signaled that several SMR and non-light-water designs are moving from demonstration toward commercialization. Many of these designs, including liquid-metal-cooled and molten-salt reactors, rely on hafnium control elements to maintain reactivity control under elevated temperatures and neutron flux. From an economic standpoint, nuclear hardware suppliers report that hafnium control rods exhibit negligible loss of mechanical or neutronic performance even after nine years of service, materially reducing replacement cycles and total cost of ownership. As nuclear operators prioritize lifetime reliability and passive safety, hafnium is emerging as a non-substitutable material for the next wave of reactor deployments.

Opportunity 2: Hafnium-Zirconium High-K Films for Ultra-Scaled DRAM Capacitors

Memory scaling is opening a second, highly specialized growth avenue for hafnium through its role in next-generation DRAM capacitor dielectrics. As DRAM manufacturers transition toward the 1c and 1d nodes, maintaining sufficient capacitance within shrinking cell geometries has become a central bottleneck. Hafnium-zirconium oxide (HZO) alloys are now at the forefront of this challenge. Research published in 2025 demonstrates that carefully engineered HZO films fabricated near the morphotropic phase boundary can achieve dielectric constants above 64—nearly double that of conventional hafnium oxide—while maintaining thicknesses below 5 nm. This performance is critical for keeping leakage current densities below 10⁻⁶ A/cm², a threshold required to prevent bit-flip errors in high-density memory used in AI servers and advanced mobile devices. The strategic advantage of HZO is further reinforced by supply-chain dynamics: because hafnium is produced as a byproduct of zirconium refining, blending the two elements enables cost optimization while allowing strain and phase tuning of the dielectric layer. As memory architectures become more vertically integrated and electrically demanding, hafnium-based high-k films are positioned as a key enabler of continued DRAM scaling rather than a temporary materials solution.

Market Share Analysis: Hafnium Market

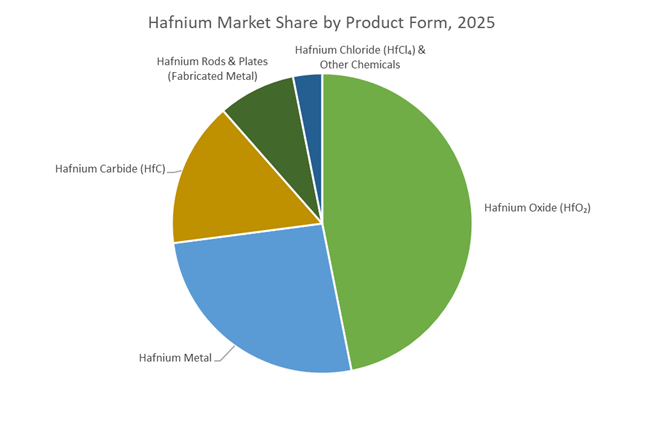

Market Share by Product Form: Hafnium Oxide (HfO₂) as the Core Enabler of Angstrom-Era Semiconductors

Hafnium oxide (HfO₂) accounts for approximately 45% of the global hafnium market in 2025 because it has become structurally indispensable to advanced semiconductor manufacturing rather than a discretionary materials choice. The decisive factor is its high-k dielectric constant (k≈25)—nearly six times that of legacy silicon dioxide—which allows transistor gate stacks below 2 nm to function without catastrophic leakage. This capability directly aligns with the industry’s transition to sub-5 nm and 2 nm nodes, where traditional insulating materials fail at a physics level. Demand intensity is further amplified by EUV lithography, where HfO₂’s refractive index above 2.0 and laser damage threshold exceeding 10 J/cm² make it the default optical coating for next-generation exposure tools. These performance requirements have pushed the market into a structural supply squeeze: hafnium prices surged 117% in 2025, reaching nearly $9,500/kg, reflecting aggressive stockpiling by leading foundries and the high cost of achieving 99.99% (4N) semiconductor purity with zirconium contamination constrained to ppm levels. As a result, hafnium oxide’s market share is not cyclical but locked in by process physics, making it the dominant and fastest-value-accreting product form in the hafnium value chain.

Market Share by Application: Microelectronics Dominates Through AI-Driven Transistor and Memory Architectures

Microelectronics represents around 50% of total hafnium demand in 2025, anchored by the AI-driven transition to new transistor and memory architectures that materially increase hafnium consumption per wafer. The shift to Gate-All-Around (GAA) transistors at the 2 nm node has raised hafnium oxide usage by 15–20% per wafer compared with FinFET designs, creating a step-change in material intensity rather than incremental volume growth. Beyond logic, hafnium’s role has expanded into next-generation memory, where hafnium-zirconium oxide (HZO) enables ferroelectric RAM with endurance levels of 10¹² cycles—roughly 1,000× higher than conventional Flash—positioning hafnium as a foundational material for AI edge computing and in-memory processing. Performance benchmarks showing sub-10-nanosecond switching at operating voltages below 0.9 V further explain why microelectronics captures half of global market value despite hafnium’s niche status by volume. Critically, supply concentration intensifies this dominance: over 80% of global separation capacity is controlled by a handful of Western players, and post-2024 export controls have forced chipmakers into premium long-term contracts for guaranteed delivery. This combination of architectural dependency, rising per-device usage, and constrained supply structurally cements microelectronics as the leading application segment in the hafnium market.

Competitive Landscape: Vertically Integrated Refiners and Advanced Materials Specialists Lead the Global Hafnium Market

The Hafnium competitive landscape is characterized by a small number of vertically integrated Zirconium refiners, advanced materials companies specializing in ultra-high purity metals, and mining developers working to establish independent Western supply chains. Companies that can reliably separate Hafnium from Zirconium, deliver ultra-low interstitial purity grades, and supply both metal and oxide forms for aerospace, nuclear, and semiconductor applications hold clear strategic advantage. With governments now prioritizing supply-chain sovereignty for critical minerals, these players are increasingly central to defense, electronics, and energy infrastructure resilience.

Framatome Sa - Vertically Integrated Nuclear-Grade Hafnium Supplier

Framatome is one of the most influential players in the global Hafnium ecosystem, operating highly specialized Zirconium-Hafnium separation facilities in Europe. As a major nuclear control rod manufacturer, it is both a producer and a captive consumer of reactor-grade Hafnium metal. The company’s acquisition of Valinox Nucléaire in 2024 boosted tubing capacity by 15%, increasing demand for Hafnium-containing nuclear components. Through its fleet Lifetime Extension Programs in the U.S. and Europe, Framatome ensures recurring demand for high-purity Hafnium, while maintaining one of the few Western-integrated supply chains capable of consistently producing reactor-grade sponge and ingots.

ATI Inc. - High-Performance Metals Specialist For Aerospace and Defense

ATI plays a leading role in supplying Hafnium-enhanced nickel-based superalloys and refractory metal systems for aerospace engines and hypersonic defense platforms. The company uses the iodide crystal-bar refining process to produce ultra-low interstitial Hafnium (typically <60 ppm oxygen), essential for ductility in severe thermal environments. ATI collaborates with GE Additive to qualify Hafnium-rich powders for additive manufacturing applications, broadening its portfolio for next-generation propulsion systems. Additionally, ATI is a key supplier of Hafnium mill forms and inserts used in plasma cutting torches-an important category within industrial precision processing.

Western Zirconium (Allegheny Technologies) - Cornerstone Of U.S. Domestic Hafnium Processing

Western Zirconium is one of the largest U.S.-based processors of high-purity Hafnium and reactor-grade Zirconium, playing a critical role in domestic defense and nuclear supply chains. The company supports DOE and DoD programs through specialized material supply for advanced nuclear reactor development. Its operations include complex chemical separation processes required to convert Zirconium co-product streams into high-purity Hafnium sponge and ingots. With national policy increasingly focused on domestic critical mineral resilience, Western Zirconium’s role in supplying secure, traceable Hafnium is becoming more strategic.

Materion Corporation - Semiconductor-Focused Leader in High-Purity Hafnium Oxide

Materion is a global leader in Hafnium-based engineered materials for semiconductors and electronics, with sputtering targets and high-k dielectric precursors forming a substantial share of its revenue. In April 2025, the company launched a new ultra-high purity HfO₂ target line optimized for ALD processes used in AI, 5G, and HPC chip fabrication. Materion also produces foils, films, powders, and granules in multiple purity grades, enabling precise deposition in memory, logic devices, and optical coatings. Its long-standing expertise in contamination control positions it as a preferred partner among leading semiconductor fabs.

Alkane Resources Ltd. - Developing A New Western Hafnium Supply Chain

Alkane Resources is advancing the Dubbo Project, a globally significant polymetallic deposit containing large quantities of Zirconium and associated Hafnium. The project is positioned to become one of the first major independent Western sources of separated Hafnium, addressing long-standing reliance on China and Russia. With Phase-2 funding secured and multiple offtake discussions underway in 2024-2025, Alkane is building vertically integrated refining infrastructure intended to produce Hafnium Oxide (HfO₂) and other high-value products for the electronics and advanced materials sectors. Its strategy aligns directly with global critical minerals security priorities.

The United States hafnium market in 2025 has shifted decisively toward supply chain defense and industrial sovereignty, reflecting the metal’s rising importance in aerospace superalloys, nuclear control systems, and advanced semiconductor fabrication. The April 2025 presidential trade mandate imposing a cumulative 79.5% tariff on Chinese-origin hafnium represents one of the most aggressive tariff regimes applied to any minor metal. This policy is explicitly designed to force domestic refining, protect U.S. turbine and defense contractors, and reduce structural exposure to Chinese metallurgical bottlenecks.

Reinforcing this stance, the Final 2025 USGS Critical Minerals List reaffirmed hafnium as a priority material, unlocking accelerated access to federal financing under the Defense Production Act (DPA). However, near-term consequences have been acute. February 2025 customs data showed zero Chinese hafnium imports, triggering a temporary supply crunch that forced U.S. aerospace OEMs to draw down strategic inventories and source higher-cost European material. This environment is rapidly reshaping procurement strategies, with long-term offtake agreements and recycling initiatives becoming central to U.S. hafnium risk mitigation.

China: Export Control Leverage and Capacity Dominance Ambitions

China’s hafnium strategy in 2025 is anchored in export control leverage and domestic prioritization, positioning the metal as a dual-use strategic asset rather than a freely traded byproduct. Expanded dual-use export licensing has significantly tightened global availability, with multiple international shipments delayed or revoked due to stringent end-user verification. These controls have increased transaction friction, injecting volatility into spot pricing and reinforcing China’s influence over downstream users.

At the same time, reports of a 140-ton-per-year hafnium metal capacity target—equivalent to current global demand—signal China’s intent to dominate pricing through scale. Crucially, this capacity expansion is largely earmarked for domestic nuclear reactor build-outs and advanced electronics, ensuring internal supply security before export allocation. As a result, China’s role in the hafnium market is evolving from volume supplier to strategic gatekeeper, reshaping global trade dynamics.

France: Western Refining Anchor and Nuclear-Driven Demand

France remains the cornerstone of non-Chinese, non-Russian hafnium supply, acting as the refined-material backbone for Europe and allied economies. In 2025, Framatome’s successful capacity ramp at its Jarrie facility lifted refined hafnium and zirconium alloy output to 45 tonnes per year, directly supporting Europe’s nuclear renaissance and aerospace manufacturing base. This expansion has positioned France as the most reliable Western source of nuclear-grade hafnium.

Strategically, France has adopted a defensive export posture, introducing targeted tariffs on certain hafnium exports to the U.S. to prioritize European industrial demand. Complementing primary refining, French policy and industry leaders are accelerating hafnium recycling from spent nuclear components, reducing dependence on raw feedstock and lowering lifecycle emissions. This dual focus on capacity and circularity reinforces France’s leadership in secure, ESG-aligned hafnium supply.

Australia: Dubbo Project and Ex-China Supply Chain Breakthrough

Australia is emerging as one of the most strategically important ex-China hafnium diversification plays globally. The Dubbo Project in New South Wales, advanced by Australian Strategic Materials (ASM), represents a rare integrated mining-to-metal opportunity, with a multi-decade reserve base spanning hafnium, zirconium, and rare earths. By 2025, the project had reached a construction-ready stage, supported by growing geopolitical interest.

Downstream, ASM’s Korean Metals Plant has become a critical validation hub, producing customer-qualified hafnium metal samples and enabling faster market entry. The successful A$55 million capital raise in October 2025 underscores investor confidence in Australia’s role within allied critical mineral frameworks such as AUKUS. If executed as planned, Australia could become the first scalable, non-Chinese source of refined hafnium with full upstream control.

South Korea: Semiconductor-Centric Metallization Innovation

South Korea’s hafnium market positioning in 2025 is defined by process innovation and semiconductor demand pull rather than raw material control. Breakthrough validation of a low-energy metallization process—using solid oxide membranes instead of carbon electrodes—has the potential to cut refining costs by up to 50%, materially improving the economics of high-purity hafnium production.

Demand-side momentum is equally strong. Rapid adoption of hafnium zirconium oxide (HZO) in ferroelectric RAM and advanced FinFET architectures has driven a 35% year-over-year increase in domestic consumption of ≥99.99% hafnium oxide. As AI-centric chip designs proliferate, South Korea is positioning itself as the world’s most sophisticated processing and application hub for hafnium-based electronics materials.

Russia: Sanctioned Supply and Additive Manufacturing Focus

Russia’s hafnium industry in 2025 remains operational but increasingly isolated, centered on domestic technological sovereignty rather than export growth. The Chepetsky Mechanical Plant (CMP), under Rosatom’s TVEL division, continues as the country’s sole producer of nuclear-grade hafnium. Recent commissioning of hafnium and titanium powder lines for additive manufacturing reflects a strategic pivot toward aerospace and space-sector self-sufficiency.

Geopolitical constraints have created a two-tier pricing structure. Russian-origin hafnium trades at a discount in non-Western markets, while certified non-Russian material commands a substantial premium in Europe and the U.S., often exceeding USD 4,500/kg in mid-2025. This divergence underscores how geopolitical risk—not geology—is now the primary determinant of hafnium market value.

2025 Strategic Matrix: Hafnium National Benchmarking

Hafnium Market Matrix

|

Country

|

Strategic Driver

|

2025 Key Milestone

|

Primary Application Focus

|

|

United States

|

Defense sovereignty

|

~80% tariff on Chinese hafnium

|

Aerospace & defense superalloys

|

|

China

|

Supply leverage

|

140 t/yr capacity expansion target

|

Nuclear control rods & electronics

|

|

France

|

European independence

|

45 t/yr refined output achieved

|

Nuclear fuel & high-temp alloys

|

|

Australia

|

Supply diversification

|

A$55M raise for Dubbo Project

|

Integrated mining-to-metal

|

|

South Korea

|

Semiconductor innovation

|

Low-energy metallization validated

|

High-K dielectrics (HfO₂, HZO)

|

|

Russia

|

Tech sovereignty

|

Hafnium 3D-printing powders launched

|

Space & aerospace tooling

|

Hafnium Market Report Scope

Hafnium Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$164.6 Million

|

|

Market Size (2035)

|

$326.8 Million

|

|

Market Growth Rate

|

7.1%

|

|

Segments

|

By Product Form (Hafnium Metal, Hafnium Oxide, Hafnium Carbide, Hafnium Chloride, Rods & Plates), By Purity Grade (Industrial, Nuclear, Semiconductor), By Application (Superalloys, Nuclear Energy, Microelectronics, Plasma Cutting, Optical Coatings, High-Temperature Ceramics)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

ATI (Allegheny Technologies Incorporated), Framatome (EDF Group), American Elements, KITZ Corporation, Australian Strategic Materials, Aremco Products Inc., Zhengzhou Vigorous Tech Co. Ltd., Nanjing Youtian Metal Technology Co. Ltd., CXMET, A.C.I. Alloys, Phelly Materials Inc., China Nuclear JingHuan Zirconium Industry Co. Ltd., Zirconium Technology Corporation, Alkane Resources Ltd., Haverhill Chemicals

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Hafnium Market Segmentation

By Product Form

- Hafnium Metal

- Hafnium Oxide (HfO2)

- Hafnium Carbide (HfC)

- Hafnium Chloride (HfCl4)

- Hafnium Rods & Plates

By Purity Grade

- Industrial Grade

- Nuclear Grade

- Semiconductor Grade

By Application

- Superalloys

- Nuclear Energy

- Microelectronics

- Plasma Cutting

- Optical Coatings

- High-Temperature Ceramics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Hafnium Market

- ATI (Allegheny Technologies Incorporated)

- Framatome (EDF Group)

- American Elements

- KITZ Corporation

- Australian Strategic Materials (ASM)

- Aremco Products, Inc.

- Zhengzhou Vigorous Tech Co., Ltd.

- Nanjing Youtian Metal Technology Co. Ltd.

- CXMET

- A.C.I. Alloys

- Phelly Materials Inc.

- China Nuclear JingHuan Zirconium Industry Co. Ltd.

- Zirconium Technology Corporation

- Alkane Resources Ltd.

- Haverhill Chemicals

*- List not Exhaustive