Heat Resistant Coatings Market Size, Growth Outlook, and High-Temperature Protection Demand Dynamics (2025–2032)

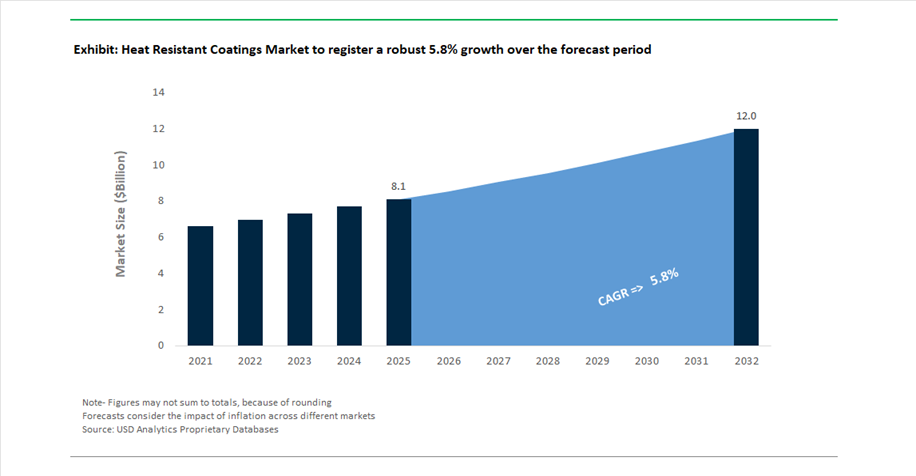

The global heat resistant coatings market reached a valuation of $8.1 billion in 2025, reflecting strong demand across energy, industrial manufacturing, automotive, and infrastructure sectors where thermal stability, corrosion resistance, and fire protection coatings are mission-critical. The market is projected to expand at a CAGR of 5.8% between 2025 and 2032, reaching $12 billion by 2032, driven by accelerating investments in high-temperature industrial coatings, intumescent coatings, and thermal barrier technologies.

A key growth catalyst is the increasing deployment of heat-resistant protective coatings in oil & gas pipelines, petrochemical plants, power generation systems, and EV battery systems, where exposure to extreme heat and thermal cycling is unavoidable. The shift toward corrosion under insulation (CUI) prevention coatings is gaining traction as asset owners prioritize lifecycle cost reduction and safety compliance. Additionally, stringent fire safety regulations in data centers, semiconductor fabs, and commercial infrastructure are boosting adoption of epoxy intumescent coatings and passive fire protection systems.

The market is also witnessing strong innovation in silicone-based coatings, powder coatings for EV batteries, and solvent-free heat-resistant formulations, aligning with sustainability mandates and performance efficiency. Growth in electric vehicles (EVs) and renewable energy infrastructure is creating new application areas for thermal management coatings, particularly in battery enclosures and high-voltage systems. Asia-Pacific, led by China and India, is emerging as a high-growth region due to rapid industrialization, while North America and Europe continue to lead in advanced coating technologies and regulatory-driven adoption.

Strategic Product Innovation and Capacity Expansion Accelerating the Heat Resistant Coatings Market

The heat resistant coatings industry is undergoing rapid transformation, marked by technological innovation, capacity expansion, and application-specific product development across high-temperature environments. In March 2026, Sherwin-Williams strengthened its leadership in corrosion-resistant coatings as its Heat-Flex CUI-mitigation product line received the prestigious Materials Performance Corrosion Innovation of the Year award. This recognition underscores growing industry emphasis on CUI-resistant coatings capable of withstanding extreme thermal cycling in energy infrastructure.

In January 2026, AkzoNobel expanded its footprint in Asia by investing over $5 million (36.5 million yuan) in its Suzhou facility, adding 7,000 tons of annual production capacity for solvent-free, high-performance heat-resistant coatings. This expansion specifically targets the energy sector, where demand for sustainable, low-VOC thermal coatings is rising. Similarly, PPG Industries introduced PPG PITT-THERM 909 in August 2025, a silicone-based spray-on insulation coating designed to replace conventional insulation systems that often trap moisture and accelerate corrosion. This innovation directly addresses a long-standing operational challenge in oil & gas and petrochemical environments.

Product innovation is also expanding into electric mobility applications, where thermal safety is critical. In June 2025, Jotun launched its powder coating solutions for EV battery systems, engineered to enhance electrical insulation and prevent thermal runaway. Complementing this, Axalta Coating Systems received the 2025 BIG Innovation Award for its Voltatex 8537PF, a high-performance insulating resin used in industrial motors and EV powertrains. These developments highlight the increasing convergence of heat resistant coatings and advanced electronics protection.

Earlier developments also reinforce this trend. In September 2024, PPG expanded the reach of its STEELGUARD 951 epoxy intumescent coating across the Americas, offering up to three hours of fire protection for critical infrastructure such as data centers and semiconductor facilities. Evonik, in June 2024, enhanced its TEGO Therm portfolio with ultra-thin coating materials tailored for space-constrained EV battery housings, while Hardide Coatings introduced CVD-based coatings capable of withstanding temperatures above 500°C for industrial spray equipment. Additionally, Carboline’s Carbothane DTM Mastic, launched globally in January 2024, enables coating application on hot surfaces up to 121°C, improving maintenance efficiency in operational facilities.

Thin-Film Ceramic Coatings Enhancing Turbocharger Performance and Thermal Efficiency

The heat resistant coatings industry is experiencing strong innovation momentum driven by the adoption of thin-film ceramic coatings in automotive and heavy-duty engine applications, particularly for turbocharger turbine housings. These coatings, typically based on materials such as alumina and yttria-stabilized zirconia, are engineered to withstand extreme exhaust temperatures while improving overall engine efficiency. One of the primary advantages is thermal retention, with ceramic coatings capable of reducing external surface temperatures by up to 35%, effectively maintaining higher energy levels within the exhaust stream to improve turbocharger responsiveness. This directly contributes to enhanced combustion efficiency and reduced fuel consumption. In terms of durability, ceramic-coated components demonstrate a 50% reduction in thermal fatigue cracking under rapid temperature cycling conditions ranging from 200°C to 950°C, significantly extending component lifespan. Additionally, these coatings reduce radiant heat transfer to adjacent components by up to 110°C, protecting sensitive electronics and polymer components in compact engine compartments. The use of thin-film coatings also enables weight reduction, as manufacturers can replace heavy high-nickel alloys with lighter substrates while maintaining oxidation resistance. These performance and efficiency gains are positioning ceramic heat resistant coatings as a critical technology in next-generation automotive and industrial engine systems.

Ceramic Coatings Replacing Metallic Cladding in Waste-to-Energy Boiler Systems

The waste-to-energy sector is increasingly transitioning from traditional metallic cladding systems, such as Inconel overlays, to advanced ceramic heat resistant coatings for waterwall tubes. This shift is primarily driven by the need to address chlorine-induced corrosion and erosion in high-temperature combustion environments. Ceramic coatings based on silicon carbide and high-purity alumina offer significantly enhanced resistance to corrosive molten salts and chlorine attack, delivering up to ten times greater protection compared to conventional metallic coatings at operating temperatures between 450°C and 600°C. Unlike thick metallic cladding, which can reduce thermal conductivity, ceramic thin-film coatings maintain efficient heat transfer, ensuring steam generation performance remains within 2% of design specifications. Operational efficiency is further improved through faster application processes, with spray-applied ceramic coatings reducing maintenance downtime by approximately 60% compared to weld-overlay techniques. In high-velocity environments where fly ash erosion is a concern, ceramic coatings demonstrate a 40% reduction in erosion rates, extending the service life of boiler tubes by five to eight years. These advantages are driving widespread adoption of ceramic coatings in industrial energy systems where durability, efficiency, and reduced maintenance are critical.

US DoD Standards Driving Adoption of Low-Emission Heat Resistant Coatings for Tactical Vehicles

The United States Department of Defense is creating a significant opportunity for advanced heat resistant coatings through updated procurement standards for tactical vehicle exhaust systems. These standards emphasize both performance and environmental compliance, driving demand for high-solids, silicone-based coatings with enhanced thermal stability. One of the key performance requirements is infrared signature suppression, with advanced coatings capable of reducing IR emissions by up to 25%, improving stealth capabilities in operational environments. Corrosion resistance is another critical factor, with coatings required to withstand 1,000 hours of salt spray testing after exposure to temperatures of 540°C, ensuring durability in maritime and high-humidity conditions. Environmental compliance is also shaping material selection, with a shift toward waterborne silicone coatings that maintain VOC levels below 100 grams per liter. These coatings must also demonstrate superior adhesion performance, maintaining a 5B rating even after prolonged exposure to temperatures as high as 650°C. These stringent requirements are positioning advanced silicone-based heat resistant coatings as essential materials in defense applications requiring durability, performance, and regulatory compliance.

India’s NTPC Mandate Driving Demand for Ceramic Coatings in Supercritical Power Plants

India’s National Thermal Power Corporation is driving significant demand for heat resistant coatings through its mandate to deploy ceramic coatings in supercritical and ultra-supercritical power plants. These facilities operate at steam temperatures exceeding 580°C, creating challenging conditions that accelerate oxidation, slagging, and fouling on boiler components. Ceramic coatings are being adopted to mitigate these issues, with performance data indicating a 20% reduction in slag formation and ash deposition, thereby maintaining optimal heat transfer efficiency. Additionally, ceramic-coated tubes exhibit an 80% reduction in scale formation on the steam side over extended operational periods, reducing the risk of overheating and tube failure. These improvements are critical in preventing forced outages, which can result in significant financial losses, estimated at approximately ₹35 lakh per day for a 660 MW unit. The broader context of India’s energy strategy, including plans to install over 50 gigawatts of new supercritical capacity by 2030, is further amplifying demand for high-performance coating solutions. These developments are positioning ceramic heat resistant coatings as a key enabler of efficiency, reliability, and cost optimization in modern thermal power generation infrastructure.

Heat Resistant Coatings Market Share 2025: High-Temperature Performance and Distributor Networks Lead Growth

Temperature Range Insights: High Heat Resistance Coatings Dominate Industrial and Automotive Applications

The high heat resistance segment leads the heat resistant coatings market with a 45% market share in 2025, driven by its optimal performance in the 300°C to 600°C temperature range, which represents the industrial “sweet spot.” These coatings, typically silicone-based and epoxy-modified formulations, are widely used in exhaust systems, industrial ovens, furnaces, boilers, and heat exchangers, where consistent thermal protection is required without the high cost of ultra-high temperature ceramic coatings. A major growth driver is the automotive aftermarket, where high-heat coatings are applied to exhaust headers, turbochargers, and manifolds operating between 450°C and 650°C, offering both protection and aesthetic finishes such as black, chrome, and ceramic-effect coatings. Their balance of cost efficiency, durability, and thermal stability makes them the preferred choice across industries. As demand for reliable mid-range thermal protection grows, high heat resistance coatings will continue to dominate the global market.

Sales Channel Insights: Industrial Distributors Lead with Technical Support and Product Availability

The industrial distributors segment holds the largest 44% share in the heat resistant coatings market in 2025, reflecting their critical role in providing ready access to a wide range of high-temperature coating solutions. Distributors maintain extensive inventories of silicone, epoxy, and ceramic-based heat resistant coatings, catering to diverse industries including petrochemical, power generation, automotive, and heavy manufacturing. Their ability to offer same-day availability for maintenance, repair, and operations (MRO) applications makes them indispensable for industrial customers requiring quick turnaround times. Additionally, industrial distributors provide valuable technical support, including guidance on surface preparation, coating selection, application techniques, and curing cycles, helping end-users achieve optimal performance. This advisory role bridges the gap between coating manufacturers and end-users such as fabricators, maintenance teams, and plant operators. As industries prioritize efficiency and uptime, distributor-led channels will remain central to heat resistant coatings market growth.

Heat Resistant Coatings Market Competitive Landscape: High-Temperature Protection, Energy Infrastructure, and Advanced Thermal Barrier Technologies Driving Competition

The heat resistant coatings market is driven by demand from energy, petrochemical, aerospace, and EV battery sectors. Key players are focusing on ultra-high-temperature coatings, CUI mitigation, and solvent-free formulations to enhance durability, reduce downtime, and meet stringent emission and performance standards.

Sherwin-Williams leads high-temperature coatings with award-winning CUI mitigation and industrial energy solutions

The Sherwin-Williams Company is a market leader in heat resistant coatings, driven by innovation in corrosion under insulation (CUI) mitigation technologies. Its Heat-Flex® ACE system earned the 2025 MP Corrosion Innovation of the Year Award, leveraging ultra-high-solids novolac epoxy chemistry to prevent failure in insulated piping. The Heat-Flex® 1200 Plus coating remains an industry benchmark, offering continuous protection up to 650°C, while Heat-Flex® AEB targets renewable energy and data center applications. The company has expanded its Global Core Portfolio to standardize high-performance coatings such as Zinc Clad® 2500 and Macropoxy® 4600 for multinational engineering projects. Its integrated applicator programs reduce downtime by 20% through turnkey installation services. This combination of performance, reliability, and service integration strengthens its dominance in industrial heat-resistant coatings.

PPG advances thermal and dielectric coating solutions for data centers and aerospace growth

PPG Industries is strengthening its position in the heat resistant coatings market through integrated protective solutions and sustainable innovation. The company reported Q1 2026 adjusted EPS of $1.83, supported by $15.9 billion in 2025 revenue and strong demand in aerospace and industrial sectors. In April 2026, PPG launched end-to-end coating systems for data centers, combining thermal resistance and dielectric protection to accelerate infrastructure deployment. It has also introduced heat-reflective coatings that reduce cooling demand in industrial buildings, aligning with its goal of achieving 44% sustainably advantaged product sales. Strategic investments in its Toulouse aerospace coatings facility are targeting growth in European aviation coatings. This integration of sustainability, performance, and infrastructure solutions enhances PPG’s competitive position.

AkzoNobel pioneers laser curing and high-temperature coatings for energy and architectural applications

AkzoNobel N.V. is advancing the heat resistant coatings market through cutting-edge curing technologies and high-performance products. In 2026, the company partnered with IPG Photonics to introduce laser-based curing, enabling faster processing and reduced energy consumption for powder coatings. Its Intertherm® series continues to lead in petrochemical and power generation sectors, offering protection up to 700°C for extreme heat environments. AkzoNobel has also become the exclusive supplier of Calosol heat-absorbing technology, transforming building façades into energy-generating systems. The expansion of its Indian production facility supports growing demand in the South Asian energy corridor. This combination of innovation, scalability, and sustainability strengthens its leadership in high-temperature coatings.

Jotun drives EV battery and offshore heat protection with solvent-free hybrid coating systems

Jotun A/S is expanding its presence in the heat resistant coatings market through advanced solutions for EV batteries and offshore environments. The company launched a comprehensive EV Battery Solution suite, addressing thermal runaway risks with coatings that provide both insulation and fire resistance. Its new R&D center in Norway is focused on hybrid silicone coatings capable of withstanding extreme thermal cycling and harsh marine conditions. Jotun has collaborated with Maersk to develop engine room coatings that reduce onboard temperatures and improve energy efficiency. The company is transitioning toward 100% solvent-free powder coatings to meet global VOC regulations while maintaining high performance in 150°C+ environments. This focus on innovation and sustainability reinforces its position in high-performance thermal coatings.

Axalta strengthens EV and industrial heat coatings with silicone-based technologies and low-bake efficiency

Axalta Coating Systems is enhancing its competitive position in heat resistant coatings through innovation in EV and industrial applications. In January 2026, the company received multiple innovation awards for its Alesta® e-PRO FG Black coating, designed to manage thermal runaway in EV battery enclosures. Its Alesta® HR range provides reliable protection up to 550°C, targeting applications such as boilers, lighting, and heating equipment. Axalta’s OEM Low-Bake technology enables simultaneous curing of metal and plastic components at 90°C, significantly reducing automotive manufacturing emissions. The company also leads in electrical steel coatings with Voltatex® 1255, supporting high-speed bonding in e-motor production. This combination of efficiency, innovation, and application diversity strengthens its role in high-temperature coatings.

Hempel expands smart heat-resistant coatings with sensor integration and energy transition focus

Hempel A/S is positioning itself as a key innovator in the heat resistant coatings market through smart technologies and energy transition alignment. The company is focusing on offshore wind and hydrogen sectors with its Hempafire Extreme 550 passive fire protection system. Its Versiline® and Hempaline® coatings are being re-engineered to withstand the demanding conditions of carbon capture and waste-to-energy facilities. Hempel is advancing Smart-Shield technologies, embedding sensors within coatings to detect thermal degradation before structural failure occurs. Following strategic restructuring, the company is prioritizing high-margin industrial heat barrier solutions in North America and EMEA. This integration of digital monitoring, sustainability, and advanced materials strengthens its competitive positioning.

United States Heat Resistant Coatings Market: Aerospace Resurgence and Semiconductor Expansion Driving High-Performance Demand

The United States heat resistant coatings market is witnessing a strong transformation, driven by the resurgence of aerospace manufacturing and large-scale investments in semiconductor fabrication. The expansion of advanced manufacturing clusters across Texas and Florida, particularly in the “New Space” economy, is accelerating demand for high-temperature coatings capable of withstanding extreme thermal cycling conditions ranging from -180°C to 600°C. These specialized coatings are increasingly critical for aerospace components, rocket systems, and cryogenic fuel storage, positioning the U.S. as a leader in advanced thermal barrier coatings.

Significant infrastructure investments under the CHIPS and Science Act have further strengthened the market, with over $150 billion in private capital flowing into semiconductor manufacturing as of early 2026. This surge has mandated the adoption of ultra-low-outgassing heat resistant coatings in cleanroom exhaust systems to ensure contamination-free environments. Additionally, product innovations such as Cerakote-hybrid coatings for electric vehicle batteries are enhancing thermal safety by preventing thermal runaway. Regulatory pressures, including the EPA’s VOC standards for industrial coatings, are also pushing manufacturers toward high-solids formulations that balance environmental compliance with superior heat resistance. The growing deployment of fusion bonded epoxy (FBE) and silicone-hybrid coatings in hydrogen pipeline networks further underscores the expanding industrial applications of heat resistant coatings in the U.S. market.

China Heat Resistant Coatings Market: Power Generation Expansion and High-Temperature Industrial Applications

China continues to dominate the global heat resistant coatings market, leveraging its massive industrial base and ongoing transition toward high-value, eco-friendly coating technologies. The country’s automotive sector, projected to reach 35 million units, is significantly driving demand for epoxy-silicone coatings used in under-the-hood applications for both internal combustion and hybrid engines. At the same time, China’s commitment to green manufacturing is accelerating the shift from conventional solvent-based coatings to water-based heat resistant coatings.

The rapid expansion of power generation infrastructure—including ultra-supercritical coal plants and nuclear reactors—is creating substantial demand for advanced ceramic-metallic (cermet) coatings capable of withstanding temperatures exceeding 800°C. Government-backed initiatives, such as subsidies for UV-cured powder coatings, are promoting energy-efficient production processes while reducing industrial energy consumption. Technological advancements, including graphene-enhanced coatings, are improving heat dissipation performance for high-tech applications like 5G base stations. Additionally, increased production of modified silicone resins in industrial clusters such as Jiangsu is strengthening China’s export capabilities in cost-effective, high-performance coatings. The widespread use of intumescent coatings in renewable energy projects, including large-scale installations in the Gobi Desert, further highlights China’s strategic focus on sustainable, high-temperature coating solutions.

Japan Heat Resistant Coatings Market: Radiative Cooling Innovations and Precision Engineering Leadership

Japan’s heat resistant coatings market is characterized by cutting-edge innovation, particularly in radiative cooling technologies and high-purity industrial applications. A major breakthrough was demonstrated at Expo 2025 Osaka, where a novel radiative cooling coating was developed to dissipate heat without energy consumption by emitting thermal radiation into outer space. This innovation represents a significant leap in sustainable cooling solutions and energy-efficient coatings.

Urban demand for heat reflective coatings is also rising, with government-backed rebate programs in cities such as Tokyo and Osaka encouraging adoption to combat the urban heat island effect. Japan continues to lead in precision-engineered coatings, including solvent-based epoxy systems widely used in industrial machinery for their superior adhesion and durability. Advanced nano-coatings capable of maintaining 99% optical clarity at temperatures up to 300°C are gaining traction in surgical robotics and automotive sensors. Regulatory mandates requiring energy-efficient building materials have standardized the use of infrared-reflective coatings in residential construction. Additionally, Japan’s dominance in optical fiber coatings ensures reliable performance in high-temperature industrial environments, reinforcing its leadership in specialized heat resistant coating technologies.

Saudi Arabia Heat Resistant Coatings Market: Oil & Gas Expansion and Vision 2030 Infrastructure Development

Saudi Arabia represents one of the most dynamic markets for heat resistant coatings in the Middle East, driven by large-scale oil & gas investments and infrastructure modernization under Vision 2030. The expansion of Saudi Aramco’s production capacity is significantly increasing the demand for heavy-duty silicone-aluminum and intumescent coatings across upstream and downstream facilities. These coatings play a critical role in protecting assets from extreme heat, corrosion, and mechanical stress in harsh desert environments.

The implementation of the Saudi Green Building Code in 2025 has further accelerated the adoption of low-VOC heat reflective coatings in commercial and government buildings, supporting energy efficiency and sustainability goals. Infrastructure developments, including desalination projects by the Saline Water Conversion Corporation, are driving demand for high-build epoxy coatings capable of withstanding high temperatures and salinity. Strategic partnerships with global coating manufacturers have led to the establishment of localized pipeline coating hubs, ensuring just-in-time delivery of specialized solutions. Advanced technologies such as dual-layer FBE systems are being widely deployed to enhance durability against thermal cycling and environmental wear, particularly in mega-projects like “The Line.”

Germany Heat Resistant Coatings Market: Hydrogen Economy and Sustainable Resin Innovation

Germany continues to lead Europe’s heat resistant coatings market, supported by strong R&D capabilities and stringent environmental regulations under REACH and EU decarbonization policies. The country is driving innovation in sustainable coating technologies, including the development of solvent-free silicone resin binders capable of withstanding extreme temperatures. These advancements are particularly relevant for industrial coatings used in energy-intensive applications.

The growing hydrogen economy is a key driver, with substantial investments in hydrogen electrolyzers increasing demand for fluoropolymer-based coatings such as PFA and FEP that offer chemical inertness and thermal stability. German manufacturers are also advancing bio-based resin formulations derived from renewable sources like soy and linseed oil, reducing dependence on petrochemicals. The adoption of UV-cured heat resistant coatings is improving manufacturing efficiency by reducing curing times in prefabrication processes. Regulatory requirements mandating migration-tested coatings for food-processing machinery are further shaping market dynamics. Additionally, smart coatings capable of changing color in response to temperature variations are gaining traction, offering innovative solutions for energy-efficient building design.

South Korea Heat Resistant Coatings Market: EV Battery Safety and Aerospace Defense Advancements

South Korea is emerging as a key player in the heat resistant coatings market, leveraging its strengths in electronics, automotive, and aerospace industries. The country’s focus on EV battery safety is driving the adoption of ceramic-infused coatings in battery modules, ensuring compliance with stringent fire safety standards such as UL 94-5VA. These coatings are critical in preventing thermal runaway and enhancing battery performance in electric vehicles.

In the aerospace sector, increasing investments in defense modernization are boosting demand for heat-resistant stealth coatings used in advanced fighter aircraft. The commercialization of multi-layer nanocomposite coatings is improving aerodynamic efficiency while providing superior thermal resistance. Additionally, significant investments in maintenance, repair, and overhaul (MRO) infrastructure are supporting the use of high-performance coatings to extend the lifespan of critical components. Regulatory updates under K-REACH are enforcing stricter standards for coating safety, particularly in healthcare and public infrastructure applications. The widespread use of fluoropolymer coatings in consumer electronics further demonstrates South Korea’s leadership in integrating heat management solutions into next-generation technologies.

Heat Resistant Coatings Market Report Scope

Heat Resistant Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.1 Billion

|

|

Market Size (2032)

|

$12 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Resin Type (Silicone, Epoxy, Acrylic, Polyester, Ethyl Silicate, Modified Resins, Advanced Materials), By Technology (Water-borne, Solvent-borne, Powder Coatings, UV), By Temperature Range (Low Heat Resistance, Medium Heat Resistance, High Heat Resistance, Ultra-High), By Substrate (Metals, Concrete and Masonry, Composites, Glass), By Application Method (Spray Applied, Brush and Roller Applied, Dip and Flow Coating, Coil Coating), By End-Use Industry (Automotive and Transportation, Power Generation, Oil and Gas and Petrochemical, Building and Construction, Consumer Goods, Aerospace and Defense, Industrial Manufacturing), By Sales Channel (Direct Sales, Industrial Distributors, Project-based Contracting, Retail)

|

|

Study Period

|

2019- 2025 and 2026-2032

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

The Sherwin-Williams Company, PPG Industries, Inc., AkzoNobel N.V., Jotun A/S, Hempel A/S, Axalta Coating Systems Ltd., Kansai Paint Co., Ltd., RPM International Inc., Nippon Paint Holdings Co., Ltd., Tnemec Company, Inc., Belzona International Ltd., Aremco Products, Inc., Teknos Group, KCC Corporation, Dampney Company, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Heat Resistant Coatings Market Segmentation

By Resin Type

- Silicone

- Epoxy

- Acrylic

- Polyester

- Ethyl Silicate

- Modified Resins

- Advanced Materials

By Technology

- Water-borne

- Solvent-borne

- Powder Coatings

- UV

By Temperature Range

- Low Heat Resistance

- Medium Heat Resistance

- High Heat Resistance

- Ultra-High

By Substrate

- Metals

- Concrete and Masonry

- Composites

- Glass

By Application Method

- Spray Applied

- Brush and Roller Applied

- Dip and Flow Coating

- Coil Coating

By End-Use Industry

- Automotive and Transportation

- Power Generation

- Oil and Gas and Petrochemical

- Building and Construction

- Consumer Goods

- Aerospace and Defense

- Industrial Manufacturing

By Sales Channel

- Direct Sales

- Industrial Distributors

- Project-based Contracting

- Retail

Leading Countries in the Industry

- North America (United States, Canada, Mexico)

- Europe (Germany, France, Spain, United Kingdom, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, MENA, Sub-Saharan Africa)

Top Companies in Heat Resistant Coatings Market

- The Sherwin-Williams Company

- PPG Industries, Inc.

- AkzoNobel N.V.

- Jotun A/S

- Hempel A/S

- Axalta Coating Systems Ltd.

- Kansai Paint Co., Ltd.

- RPM International Inc.

- Nippon Paint Holdings Co., Ltd.

- Tnemec Company, Inc.

- Belzona International Ltd.

- Aremco Products, Inc.

- Teknos Group

- KCC Corporation

- Dampney Company, Inc.

*- List not Exhaustive