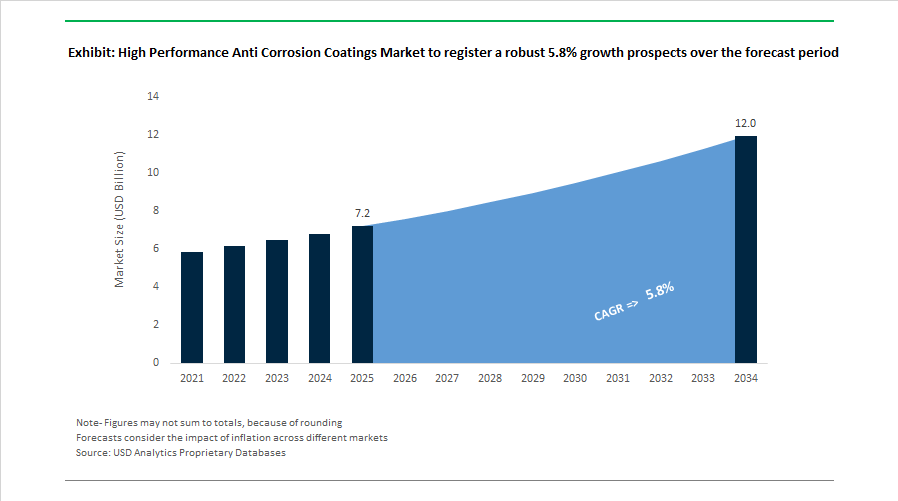

High Performance Anti Corrosion Coatings Market to Reach $12 Billion by 2034 at 5.8% CAGR Driven by EV Battery Protection, Offshore Durability, and Smart Coating Technologies

The High Performance Anti Corrosion Coatings Market is projected to expand from $7.2 billion in 2025 to $12 billion by 2034, registering a CAGR of 5.8%. Growth is anchored in rising infrastructure investments, offshore wind expansion, electric vehicle battery protection, marine fleet modernization, aerospace lightweighting, and long-life architectural metal applications. Demand for zinc-rich primers, epoxy systems, fluoropolymer powder coatings, solvent-free tank linings, and advanced fouling-control systems is increasing as asset owners prioritize lifecycle extension, corrosion resistance, and carbon footprint reduction in steel-intensive industries.

In January 2025, Hempel A/S launched Avantguard 750 Pro, a next-generation zinc-rich primer engineered for offshore structures requiring more than 35 years of durability. The product significantly reduces maintenance intervals and supports decarbonization strategies by minimizing steel replacement cycles. In the same month, Nippon Paint introduced Danziora, an anti-corrosion coating optimized for salt-heavy coastal infrastructure. The technology uses moisture-reactive pigments to reinforce barrier performance and was selected for the restoration of the Waka-To Bridge in Japan. In March 2025, Sherwin-Williams expanded its Global Core standardized line, enabling identical inorganic zinc and epoxy primer specifications across continents, a strategic move supporting multinational infrastructure and energy projects.

Electrification and mobility applications intensified in mid to late 2025. In June 2025, Jotun introduced EV Battery Solutions, powder coatings designed to provide electrical insulation, corrosion resistance, and thermal stability for high-voltage battery packs. In September 2025, AkzoNobel and NIO received the Altair Enlighten Award for a co-developed Interpon A1000 powder coating that extended EV battery bottom plate lifespan from 5 to 15 years while reducing coating thickness by 70%. In October 2025, Hempel launched Hempaline Defend 430, a solvent-free tank lining designed for rapid curing and single-coat efficiency in energy storage infrastructure where chemical and thermal resistance are critical. At the AIA Conference 2025, PPG Industries presented third-party validation showing its Coraflon Platinum coating maintains color retention 20 times longer than competitive systems over five years while delivering one-coat corrosion protection.

Strategic consolidation and intelligent coating innovation accelerated into 2026. In December 2025, AkzoNobel and Axalta Coating Systems announced a definitive all-stock merger, entering regulatory review in early 2026 to integrate marine and protective coatings R&D into a unified global platform. In December 2025, AkzoNobel also invested in U.S. aerospace coatings infrastructure to support lightweight anti-corrosion systems for next-generation aircraft. In January 2026, Jotun launched Smart Coatings incorporating micro-sensor technologies capable of signaling corrosion initiation through color change or embedded detection responses, enabling predictive maintenance for offshore and industrial assets. In February 2026, Hempel completed first applications of Hempaguard NB on Maersk vessels, integrating high-performance anti-corrosion and fouling control systems directly into shipbuilding processes. Meanwhile, UK-based Cyanoskin advanced commercialization of an algae-based carbon capture coating in late 2025, targeting a 2026 launch that combines surface protection with active CO2 absorption.

The High Performance Anti Corrosion Coatings Market is increasingly defined by long-life zinc-rich primers, fluoropolymer powder coatings, solvent-free epoxy linings, intelligent sensor-enabled systems, EV battery insulation coatings, marine fouling control technologies, and carbon-reducing formulation strategies. Competitive positioning is centered on durability extension beyond 30 years, coating thickness optimization, corrosion monitoring integration, and alignment with global decarbonization mandates across infrastructure, maritime, aerospace, and energy storage sectors.

High-Performance Anti-Corrosion Coatings Market Trends and Opportunities

Regulatory-Driven Shift Toward High-Solids and Waterborne Epoxy Coating Systems

The global high-performance anti-corrosion coatings market is undergoing a structural transition as regulatory pressure on volatile organic compound emissions tightens across marine, offshore, and heavy industrial maintenance cycles. The transition from solvent-rich primers to high-solids and waterborne epoxy systems is no longer optional, as regulators now align air-quality objectives with industrial asset protection standards. This regulatory convergence is forcing asset owners to modernize coating specifications without compromising long-term corrosion resistance.

In January 2025, the U.S. Environmental Protection Agency finalized amendments to the National VOC Emission Standards, harmonizing federal limits with the California Air Resources Board framework. These amendments prioritize low-reactivity formulations, accelerating adoption of waterborne epoxies and high-solids systems across ports, shipyards, refineries, and steel infrastructure. Market response has been rapid. In March 2025, Allnex expanded its waterborne resin production capacity to address surging demand from infrastructure and marine maintenance contractors. Similarly, Olin Corporation introduced a next-generation waterborne curing agent in early 2025, engineered to deliver C5-M marine durability traditionally associated with solvent-based epoxies.

From an operational perspective, high-solids epoxy systems with volume solids exceeding 80% are now achieving single-coat dry film thickness above 200 microns. Field performance data from 2024 to 2025 show that these systems can reduce labor and downtime costs by approximately 30% while maintaining corrosion protection benchmarks exceeding 25 years in high-salinity and offshore exposure zones. This combination of compliance, productivity, and lifecycle performance is making high-solids and waterborne epoxies the default specification across new and maintenance coating programs.

Co-Development of Anti-Corrosion Coatings for Hydrogen and CCUS Infrastructure

The rapid build-out of green hydrogen and carbon capture, utilization, and storage infrastructure is redefining corrosion risk profiles for steel assets. Hydrogen embrittlement, permeation losses, and supercritical CO2 corrosion are emerging as dominant degradation mechanisms, pushing coating manufacturers into co-development partnerships with energy and equipment providers. These collaborations aim to create advanced barrier systems rather than incremental upgrades to legacy coatings.

Hydrogen transport presents unique challenges, as hydrogen molecules diffuse through steel at rates roughly 15% higher than methane. In response, material developers are qualifying ceramic-metallic and high-nickel primer systems capable of reducing hydrogen permeability by several orders of magnitude compared to uncoated carbon steel. In mid-2025, performance testing showed that next-generation barrier coatings could reduce hydrogen diffusion by up to ten thousand times, significantly improving pipeline integrity and storage safety.

Parallel innovation is occurring in electrolyzer environments. In June 2025, Resillion coating technology demonstrated corrosion mitigation performance that exceeded U.S. Department of Energy benchmarks for proton exchange membrane electrolyzers, where exposure to high-purity water and fluctuating electrochemical conditions accelerates degradation. At the policy level, the Clean Hydrogen Joint Undertaking 2025 work program has earmarked substantial funding for materials and standards development, explicitly prioritizing anti-corrosion linings for high-pressure hydrogen storage tanks and cross-border hydrogen pipelines. These initiatives are anchoring a long-term growth runway for specialized coatings designed for the hydrogen and CCUS economy.

Digitalized Asset Integrity Through Smart and Sensing Coatings

The convergence of digitalization and corrosion protection is creating a high-value opportunity for smart coatings that function as both protective barriers and diagnostic systems. Offshore wind farms, subsea oil and gas assets, and marine structures are increasingly adopting coatings embedded with sensing capabilities to reduce reliance on manual inspections and remotely operated vehicles.

Recent studies published in late 2025 show that polyurethane-urea coatings reinforced with carbon nanotubes and graphene can improve erosion resistance by 60 to 99% while enabling autonomous healing of micro-cracks before corrosion initiation. These systems leverage predictive algorithms to anticipate damage progression, extending coating service life in high-impact environments such as wind turbine leading edges. Conductive-layer coatings are also gaining traction. In the North Sea, operators are deploying multi-layer systems where changes in electrical resistance between the coating and steel substrate provide real-time alerts of barrier failure. Early deployments suggest potential offshore maintenance cost reductions of $50,000 to $100,000 per asset annually.

As coating suppliers integrate cloud-based monitoring platforms with these smart surfaces, predictive maintenance models are emerging. By 2025, such integrated solutions are projected to extend the first major maintenance interval of offshore wind foundations from 15 years to more than 20 years, materially improving project economics for renewable energy operators.

Advanced Barrier Coatings for EV Battery Housings and Electrical Components

The electrification of transport is creating a distinct opportunity for high-performance anti-corrosion coatings that deliver electrical insulation, thermal resistance, and chemical protection in a single system. EV battery housings and busbars are exposed to road salts, thermal cycling, and high-voltage environments, requiring coatings that go beyond conventional corrosion resistance.

In October 2025, Axalta Coating Systems launched a specialized battery coating platform engineered to withstand ignition temperatures up to 1200 degrees Celsius while maintaining zero-smoke performance during thermal runaway events. This secondary fire-protection capability is increasingly mandated by global EV safety standards. Dielectric performance is equally critical. OEM specifications introduced in 2025 now require coatings to pass 6 kilovolt hipot tests and comply with UL 94 V0 and IEC 60243-1 standards for use in 800-volt and higher charging architectures.

Lightweighting trends are further shaping this opportunity. As manufacturers transition from copper to aluminum busbars to reduce vehicle mass by up to 40%, galvanic corrosion risks increase at metal junctions. To address this, MacDermid Enthone is deploying advanced electroless nickel barrier technologies that provide uniform, non-porous protection on complex geometries. These coatings enable long-term corrosion resistance while supporting the automotive industry’s dual objectives of lightweight design and high-voltage reliability.

Competitive Landscape in the High-Performance Anti-Corrosion Coatings Market

The High Performance Anti-Corrosion Coatings Market is highly competitive, led by global coatings manufacturers focusing on advanced protective coatings, corrosion-resistant powder coatings, intumescent fire protection coatings, and smart monitoring technologies for industrial infrastructure. Key companies are strengthening market leadership through strategic mergers, PFAS-free coating formulations, energy-efficient curing technologies, and specialized coatings for offshore wind, marine vessels, EV batteries, and oil & gas infrastructure. Rising demand from marine engineering, renewable energy installations, industrial pipelines, water infrastructure, and high-salinity offshore environments is accelerating innovation in high-solids coatings, corrosion under insulation (CUI) mitigation technologies, and environmentally sustainable coating systems, making R&D intensity and sustainability compliance key competitive differentiators.

AkzoNobel Strengthens Offshore and Marine Corrosion Protection Through Axalta Merger Strategy

AkzoNobel remains a dominant player in the high performance anti-corrosion coatings market, supported by its extensive global portfolio of marine protective coatings, offshore corrosion protection technologies, and industrial asset protection solutions. In December 2025, the company announced a transformative all-stock merger with Axalta, a strategic move aimed at creating a world-leading coatings enterprise with expanded anti-corrosion R&D capabilities, expected to close between late 2026 and early 2027. To sharpen its focus on high-growth sectors such as offshore wind and marine coatings, AkzoNobel divested its stake in Akzo Nobel India Ltd. in 2025 for €922 million, representing a 25× EBITDA valuation. The company has also achieved significant decarbonization progress, reducing Scope 1 and 2 carbon emissions by 47% compared with its 2018 baseline, largely through electrification of more than 25 global production sites. Its coatings were recently deployed on China’s deep-sea drilling vessels, highlighting strong performance in high-salinity, high-pressure offshore environments.

PPG Industries Advances Laser-Based Powder Coating Technologies for Energy-Efficient Corrosion Protection

PPG Industries continues to expand its presence in the industrial anti-corrosion coatings market through innovation in energy-efficient powder coatings and advanced protective materials for EV and industrial applications. In March 2026, PPG announced a strategic partnership with IPG Photonics and Whirlpool to commercialize laser-based powder curing technology, significantly reducing the energy consumption associated with applying anti-corrosive coatings while improving adhesion performance. The company also launched PPG STEELGUARD® 652 in February 2026, a next-generation intumescent coating for interior structural steel that enhances both fire resistance and corrosion protection in complex architectural structures. At FABTECH 2025, PPG introduced its ENVIROLUXE™ PFAS-free powder coatings portfolio, incorporating recycled industrial plastics (rPET) to support circular economy initiatives. Additionally, its ENVIROCRON® High-Transfer Efficiency (HTE) powder coating system delivers first-pass transfer rates of up to 85%, reducing coating waste by 20%–25% compared with conventional systems.

Jotun Develops Smart Anti-Corrosion Coatings with Real-Time Structural Monitoring Capabilities

Jotun is emerging as a technology leader in the smart corrosion protection coatings market, particularly in marine infrastructure, offshore wind installations, and high-voltage electrical equipment protection. In 2026, the company introduced an advanced smart anti-corrosion coating platform capable of signaling surface degradation or micro-crack formation through integrated color-changing sensors, enabling operators to detect corrosion initiation before structural damage occurs. Jotun also remains the only coatings manufacturer offering a third-party verified CX-rated anticorrosive powder solution under ISO 12944, designed for extreme environments such as transformers and power generation equipment exposed to high salinity. The company launched EV Battery Powder Coatings in 2025, providing both electrical insulation and corrosion resistance for high-voltage battery systems, reducing thermal runaway risks. Jotun also joined the EOLMED floating offshore wind project in France, supplying specialized coatings engineered for harsh hydrodynamic and atmospheric conditions.

Hempel Expands Marine and Energy Infrastructure Coatings with Strong Sustainability Performance

Hempel continues to strengthen its position in the marine anti-corrosion coatings and energy infrastructure coatings market, driven by its “Double Every 5 Years” growth strategy and focus on fuel-efficient maritime technologies. The company achieved record profitability in 2024, reporting €392 million in adjusted EBITDA with a 17.9% margin, largely fueled by strong demand for its Hempaguard hull coatings, which significantly improve vessel fuel efficiency and reduce CO₂ emissions. Hempel has also made substantial sustainability progress, achieving a 65% reduction in Scope 1 and 2 carbon emissions by 2024, with a target of 90% reduction by 2026. Its Energy & Infrastructure segment generated €823 million in revenue, driven primarily by strong growth in the Middle East oil and gas sector, where the company provides high-temperature insulation and corrosion protection systems. Additionally, Hempel reduced landfill waste by 97% by the end of 2024, targeting near-zero landfill operations across 25 production sites.

Sherwin-Williams Introduces Single-Layer Anti-Corrosion Coating Systems for Offshore and Industrial Assets

Sherwin-Williams Protective & Marine division is advancing the industrial anti-corrosion coatings market through innovative high-solids single-layer coating technologies designed to simplify maintenance operations for offshore and industrial assets. In late 2024, the company launched Repacor™ SW-1000, a 100% volume solids anti-corrosion coating capable of replacing traditional two- or three-layer protective coating systems with a single 500-micron application, significantly reducing installation time and applicator exposure to chemicals. Sherwin-Williams also received the 2025 MP Corrosion Innovation of the Year Award for its Heat-Flex® CUI mitigation coating system, engineered to prevent Corrosion Under Insulation (CUI) in pipelines and high-temperature industrial equipment. In September 2025, the company recognized infrastructure innovation through its Water Infrastructure Impact Awards, highlighting corrosion-resistant linings that extend municipal water system asset life by 15–20 years. Additionally, Sherwin-Williams expanded its Global Core Product Offering in 2025, standardizing premium anti-corrosive coatings across 120 countries.

High Performance Anti Corrosion Coatings Market Share and Segmentation Insights

Epoxy Resin Systems Lead the High Performance Anti Corrosion Coatings Market in Industrial Protection

Epoxy coatings accounted for 42.80% of the High Performance Anti Corrosion Coatings Market share in 2025, establishing them as the most widely used resin system for corrosion protection across industrial infrastructure and heavy-duty environments. Epoxy coatings are favored because they provide excellent adhesion to metal substrates, superior chemical resistance, and high impermeability, forming durable protective barriers that prevent moisture, oxygen, and corrosive agents from reaching the underlying material. These characteristics make epoxy coatings the preferred technology for marine vessels, offshore oil and gas platforms, pipelines, storage tanks, bridges, and industrial processing equipment exposed to harsh environmental conditions. Epoxy systems are also widely used as primer and intermediate layers in multi-coat protective coating systems, ensuring long-term corrosion resistance and mechanical durability. In 2025, technological advancements have improved epoxy coating performance through the development of surface-tolerant epoxy formulations capable of adhering effectively to damp or minimally prepared substrates. These advanced formulations reduce the need for extensive abrasive blasting during maintenance painting, significantly lowering surface preparation costs while maintaining the long-term corrosion protection required in industrial infrastructure projects.

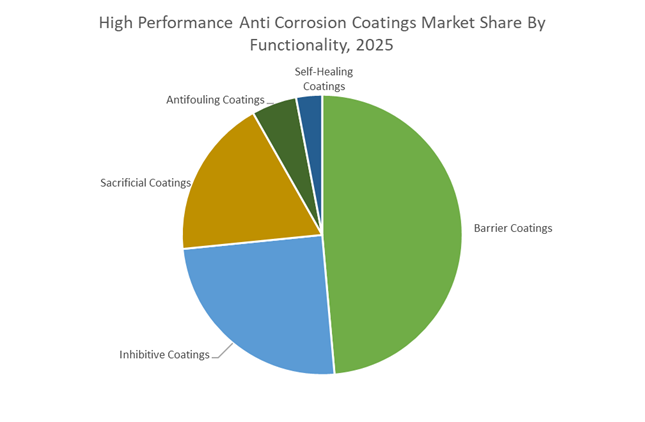

Barrier Coatings Drive the Largest Functional Segment in High Performance Anti Corrosion Coatings

Barrier Coatings represented 48.60% of the High Performance Anti Corrosion Coatings Market share in 2025, making them the most widely applied corrosion protection mechanism within industrial coating systems. Barrier coatings function by creating a dense, impermeable film that blocks water, oxygen, salts, and other corrosive electrolytes from contacting metal surfaces, thereby preventing electrochemical corrosion reactions. High-build coatings based on epoxy and polyurethane resin systems are commonly used as barrier coatings in protective systems applied to steel infrastructure, marine equipment, transportation assets, and industrial facilities. These coatings play a critical role in extending the service life of structural components exposed to aggressive environments. In 2025, the barrier coating segment is experiencing innovation through the development of nanocomposite coating technologies that incorporate materials such as nano-clays, graphene platelets, and layered silicate structures. These advanced additives improve the coating’s resistance to permeability, enabling enhanced corrosion protection even at reduced film thickness. Such nanostructured coatings are particularly valuable in transportation equipment and large infrastructure assets, where lighter coating systems and longer maintenance intervals provide operational and economic advantages.

China: Deep-Sea Engineering, Smart Shipping, and Infrastructure Compliance

China’s high performance anti-corrosion coatings industry is being shaped by deep-sea engineering requirements, maritime decarbonization, and stricter infrastructure compliance standards. In January 2025, AkzoNobel deployed advanced protective coating systems for China’s flagship deep-sea drilling vessel Mengxiang. These systems were engineered to withstand extreme hydrostatic pressure, high salinity, and long-duration immersion in the South China Sea, reinforcing China’s position in offshore exploration and subsea asset protection.

Strategic maritime partnerships are strengthening long-term demand visibility. During Marintec China 2025, AkzoNobel signed an expanded supply agreement with Winning Shipping, securing International brand coatings including the Intercept 8500 LPP antifouling system for six large vessels scheduled for drydocking in 2026. On the regulatory side, enforcement under the GB 18352.6-2025 framework has intensified inspections of anti-corrosion applications across Belt and Road Initiative projects. Contractors are now mandated to use low-VOC, high-solids epoxy systems for cross-border bridges and rail corridors to improve durability and environmental compliance. Innovation is also emerging from domestic players. Guangdong Yufeng Industries commercialized RTV antifouling coatings with embedded sensors in late 2025, enabling real-time hull condition monitoring aligned with China’s Smart Shipping roadmap for 2026.

United States: Aerospace Expansion, PFAS Transition, and Offshore Modernization

The United States high performance anti-corrosion coatings market is undergoing structural change driven by aerospace investment, environmental regulation, and offshore energy upgrades. In May 2025, PPG Industries announced a USD 380 million investment to build a new manufacturing facility in North Carolina dedicated to aerospace coatings and sealants. This expansion directly supports rising production of next-generation jetliners, where corrosion resistance, weight efficiency, and durability are critical certification parameters.

Environmental policy is accelerating formulation shifts. The U.S. Environmental Protection Agency has adopted a group-based approach to PFAS regulation for 2025–2026, prompting U.S. formulators to phase out fluorinated anti-corrosion additives in favor of PFAS-free and self-healing coating technologies. Offshore energy infrastructure is another major demand driver. Government assessments in late 2025 indicated that more than 57% of U.S. offshore platforms require mandatory corrosion upgrades, leading to a sharp increase in investment toward green, low-VOC systems. Trade policy is reinforcing domestic sourcing. New tariffs introduced in 2025 on imported Chinese chemicals have shifted procurement toward U.S.-produced cold-galvanized and zinc-rich coatings, as project owners prioritize supply chain resilience and cost predictability.

Germany: E-Mobility Protection and Hydrogen-Ready Coatings

Germany’s high performance anti-corrosion coatings industry is evolving at the intersection of electric mobility, emissions regulation, and hydrogen infrastructure development. At the K 2025 trade fair, German manufacturers introduced dielectric anti-corrosion coatings tailored for electric vehicle battery packs. These coatings provide chemical resistance to cooling fluids while acting as a barrier against short-circuit risks and thermal runaway, making them a critical material layer for the 2026 European EV platform rollout.

Regulatory pressure continues to reshape industrial coating systems. Amendments to the EU Industrial Emissions Directive in 2025 have compelled German chemical clusters to adopt Best Available Techniques, accelerating the transition toward water-borne and powder-based anti-corrosion coatings across the Ruhr region. Innovation is extending into the hydrogen economy. German firms such as AIVAM launched sensor-embedded smart varnish layers in late 2025, now being piloted on domestic hydrogen transport pipelines. These coatings detect moisture ingress and early corrosion using low-power electronics, improving safety and maintenance efficiency for hydrogen infrastructure.

Norway: Offshore Wind Growth and Bio-Based Coating Leadership

Norway’s high performance anti-corrosion coatings industry is closely aligned with offshore wind expansion and the country’s broader green transition agenda. In early January 2026, Jotun introduced next-generation anti-corrosion systems featuring ultra-high-build zinc formulations. These coatings are engineered for superior adhesion and long service life in highly saline offshore environments, specifically targeting wind turbine foundations and marine energy assets.

Demand fundamentals are reinforced by rapid offshore wind deployment. Norway reported more than 54% growth in turbine installations across 2025–2026, driving record consumption of UV-resistant and corrosion-resistant coatings for monopiles and substructures. Policy leadership further differentiates the market. Norway has mandated the use of 100% natural-component coating films for selected maritime assets, accelerating R&D into plant-based resins that deliver performance comparable to conventional epoxies. This regulatory stance positions Norway as a testbed for bio-based anti-corrosion technologies at commercial scale.

India: Maritime Investment and Functional Nanocoatings

India’s high performance anti-corrosion coatings market is expanding alongside large-scale maritime investment and tightening industrial standards. In 2025, the Ministry of Shipping allocated over INR 4.32 lakh crore for maritime infrastructure upgrades. Major programs such as Bharathmala and Sagarmala are incorporating advanced anti-corrosion coating systems for ports, coastal bridges, and logistics corridors to improve asset life in aggressive marine environments.

Innovation is emerging from domestic startups. Panlys Nanotech launched a visible-light photocatalytic titanium-dioxide-based coating in 2025 that combines corrosion protection with oxidation of surface-borne pathogens. This dual-function technology is gaining adoption in public transport assets and healthcare facilities. Regulatory tightening will further formalize demand. From January 2026, the Bureau of Indian Standards has mandated quality certification for industrial coatings used in state-run oil refineries, standardizing requirements for load-bearing performance and rust resistance across critical energy infrastructure.

Summary Table: Country-Level Strategic Signals in the High Performance Anti-Corrosion Coatings Industry

High Performance Anti Corrosion Coatings Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Key Application Focus

|

Structural Implication

|

|

China

|

Deep-sea assets, smart shipping

|

Offshore vessels, BRI infrastructure

|

System-level corrosion management

|

|

United States

|

Aerospace investment, PFAS regulation

|

Aircraft, offshore platforms

|

PFAS-free and domestic sourcing

|

|

Germany

|

EV safety, hydrogen pipelines

|

Battery packs, industrial assets

|

High-spec functional coatings

|

|

Norway

|

Offshore wind growth, green mandates

|

Turbine foundations, marine assets

|

Bio-based and zinc-rich systems

|

|

India

|

Maritime funding, BIS standards

|

Ports, refineries, public assets

|

Scale-driven adoption with innovation

|

High Performance Anti Corrosion Coatings Market Report Scope

High Performance Anti Corrosion Coatings Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.2 Billion

|

|

Market Size (2034)

|

$12 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Resin Type (Epoxy, Polyurethane, Acrylic, Alkyd, Zinc-Rich, Chlorinated Rubber, Specialty Resins), By Technology (Solvent-Borne Coatings, Water-Borne Coatings, Powder Coatings, Radiation-Cured Coatings), By Functionality (Barrier Coatings, Sacrificial Coatings, Inhibitive Coatings, Self-Healing Coatings, Antifouling Coatings), By Application Method (Spray Application, Electrostatic Application, Dipping and Brushing, Roll and Coil Coating), By End-Use Industry (Marine, Oil and Gas, Infrastructure, Energy, Industrial Manufacturing, Automotive and Aerospace)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

AkzoNobel N.V., PPG Industries, Inc., The Sherwin-Williams Company, Jotun A/S, Hempel A/S, Kansai Paint Co., Ltd., Axalta Coating Systems Ltd., Nippon Paint Holdings Co., Ltd., BASF SE, RPM International Inc., Sika AG, Chugoku Marine Paints, Ltd., Henkel AG & Co. KGaA, 3M Company, Ashland Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

High Performance Anti-Corrosion Coatings Market Segmentation

By Resin Type

- Epoxy

- Polyurethane

- Acrylic

- Alkyd

- Zinc-Rich

- Chlorinated Rubber

- Specialty Resins

By Technology

- Solvent-Borne Coatings

- Water-Borne Coatings

- Powder Coatings

- Radiation-Cured Coatings

By Functionality

- Barrier Coatings

- Sacrificial Coatings

- Inhibitive Coatings

- Self-Healing Coatings

- Antifouling Coatings

By Application Method

- Spray Application

- Electrostatic Application

- Dipping and Brushing

- Roll and Coil Coating

By End-Use Industry

- Marine

- Oil and Gas

- Infrastructure

- Energy

- Industrial Manufacturing

- Automotive and Aerospace

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the High Performance Anti-Corrosion Coatings Industry

- AkzoNobel N.V.

- PPG Industries, Inc.

- The Sherwin-Williams Company

- Jotun A/S

- Hempel A/S

- Kansai Paint Co., Ltd.

- Axalta Coating Systems Ltd.

- Nippon Paint Holdings Co., Ltd.

- BASF SE

- RPM International Inc.

- Sika AG

- Chugoku Marine Paints, Ltd.

- Henkel AG & Co. KGaA

- 3M Company

- Ashland Inc.

*- List not Exhaustive