Market Overview: Automotive Lightweighting and High-Temperature Electronics Are Structurally Expanding the High-Performance Polyamides Market

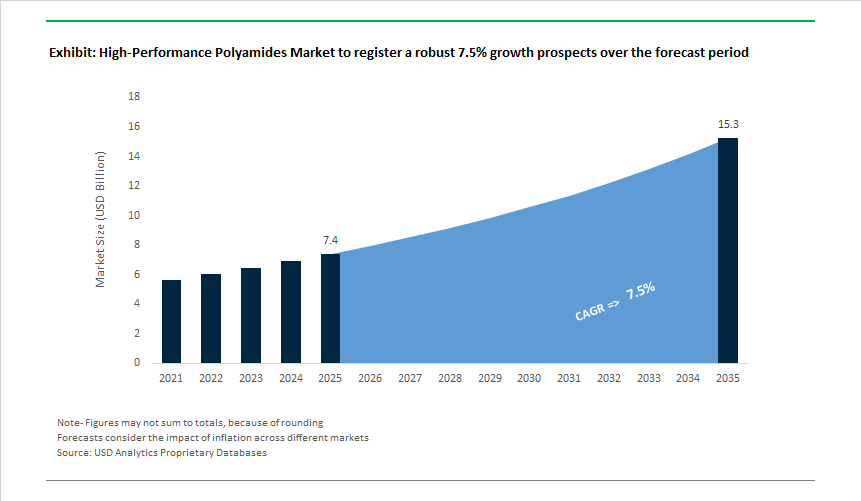

The High-Performance Polyamides (HPPA) Market (USD 7.4 billion in 2025; projected to reach USD 15.3 billion by 2035 at a 7.5% CAGR) is being structurally driven by transportation electrification, vehicle lightweighting mandates, and the rapid scaling of high-temperature electronics across automotive, industrial, and communications infrastructure. Unlike standard nylons, HPPAs are specified where dimensional stability, hydrolytic resistance, and sustained thermal performance directly influence system reliability, safety, and lifetime - positioning them as enablers of next-generation electrical and fluid-handling architectures.

Automotive applications account for approximately 39.5% of global HPPA revenue, reflecting accelerated substitution of metals and lower-grade polymers in EV battery housings, under-the-hood components, fuel and fluid systems, and high-voltage connectors. Polyphthalamides (PPAs) and long-chain polyamides have become mission-critical in these environments due to their ability to maintain mechanical strength and chemical resistance under continuous exposure to elevated temperatures, aggressive fluids, and cyclic thermal loading. In parallel, PA12 and PA11 dominate fuel lines, brake systems, flexible tubing, and additive manufacturing powders, where low moisture uptake, chemical durability, and consistent melt behavior are essential for both conventional extrusion and SLS-based 3D printing.

Beyond transportation, demand for high-temperature polyamide families such as PA 6T/66 and PA 9T is scaling with the expansion of 5G infrastructure, power electronics, and fine-pitch connectors. In these applications, dimensional stability above 150°C is non-negotiable, as even minor creep or warpage can compromise signal integrity, solder joint reliability, and long-term electrical performance. OEMs increasingly specify these grades to enable higher circuit density and component miniaturization without sacrificing reliability under sustained thermal stress.

Over the forecast period, competitive differentiation in the HPPA market will be defined by grade specialization, feedstock security, and sustainability alignment rather than volume growth alone. Bio-based PA11, derived from renewable castor oil, is gaining strategic importance as automotive and electronics OEMs embed renewable-content targets into material specifications, while recycling and mass-balance approaches are emerging as prerequisites for supplier qualification.

Market Analysis: Capacity Moves, Circularity and New Grades Shaping HPPA Demand

Recent industry activities show simultaneous traction on three fronts: product innovation, regional capacity expansion, and sustainability/circularity. In November 2024, Evonik completed trial production of a second long-chain polyamides reactor in Shanghai, signaling plans to double production capacity in Asia to meet surging demand for PA12/PA11 in EVs and oil & gas applications. Early 2025 supply-side shocks were visible when April 2025 Ascend Performance Materials temporarily curtailed PA66 output due to feedstock shortages, underlining systemic vulnerability in ADN and other upstream inputs that can ripple across HPPA availability and pricing.

The pace of grade innovation accelerated through mid-late 2025 as suppliers launched low-carbon and high-performance solutions. June-October 2025 saw multiple product and investment announcements: June 2025 (BASF) rolled out new bio-based Ultramid® specialty polyamides; July 2025 Arkema announced a $20 million investment to expand Rilsan® PA11 transparent production in Singapore (50% capacity lift, start-up Q1 2026), strengthening APAC supply for medical, consumer and industrial markets; August 2025 Sumitomo introduced a PA12 grade with enhanced chemical resistance tailored for aggressive automotive and industrial environments. In October 2025, both BASF and Evonik signalled circularity and low-carbon product launches - BASF with new Polyamide-6 recycling routes from end-of-life vehicles, and Evonik showcasing mass-balanced PA12 (VESTAMID®) with up to 70% CO₂ reduction vs. fossil feedstock.

High-Performance Polyamides Market Trends and Opportunities

Long-Chain Polyamides Engineered for 800V+ EV Battery and Powertrain Systems

The shift toward 800V and emerging 1,000V EV architectures is forcing materials to perform simultaneously as electrical insulators, pressure-resistant fluid carriers, and structurally stable housings under fast-charge thermal spikes. Long-chain polyamides are gaining traction because their lower moisture uptake and superior dielectric stability directly mitigate failure risks at high voltage.

In June 2025, BASF introduced Ultramid® Advanced N3U42G6, a PPA grade engineered specifically for high-voltage EV connectors. The material delivers high Comparative Tracking Index (CTI) values while maintaining mechanical strength in electrolytically aggressive environments—an area where conventional PA 66 grades show premature surface tracking and corrosion-driven degradation.

Cooling system reliability is emerging as an equally decisive factor. Technical disclosures from Evonik (2025) show that VESTAMID® PA 12 coolant lines retain ~30% higher burst pressure after 3,000 hours in glycol-water mixtures at 130 °C, compared with standard short-chain polyamides. This performance directly addresses one of the most critical EV safety risks: coolant leakage adjacent to high-voltage cells.

From a system-level perspective, OEM trials in 2025 indicate that replacing aluminum battery module covers with glass-fiber-reinforced PA 610 and PA 612 can cut component weight by 40–50% without compromising impact resistance. This lightweighting supports compliance with U.S. CAFE efficiency targets while offsetting the mass penalties associated with larger battery packs and reinforced enclosures.

Low-Dielectric PPAs Unlocking mmWave 5G and RF Miniaturization

As global networks migrate toward mmWave frequencies (24–39 GHz), material selection has become a first-order RF design variable. Housing and antenna materials must minimize signal attenuation while maintaining dimensional stability through reflow soldering and outdoor exposure.

Next-generation polyphthalamide (PPA) formulations are now achieving dielectric constant (Dk) values of ~2.8–3.1 with dissipation factors below 0.005, even under high humidity. According to specifications released by Solvay for its Amodel® PPA portfolio, these properties materially reduce insertion loss in mmWave antenna windows and radomes—critical for small-cell base stations and compact smartphone antenna modules.

Thermal stability is equally strategic. With heat deflection temperatures exceeding 280 °C, PPAs can pass SMT reflow soldering without warpage, enabling dense RF component integration. Industry assessments in 2025 suggest that this dimensional stability supports a ~25% reduction in antenna module footprint, accelerating the miniaturization of telecom hardware.

Demand visibility is reinforced by infrastructure scale. Government disclosures from Ministry of Industry and Information Technology confirm that China surpassed 3.5 million deployed 5G base stations in 2025. This rollout is structurally increasing demand for low-Dk, UV-stable, and thermally robust polyamides capable of protecting mmWave electronics over multi-year outdoor service lifetimes.

Lightweight Polyamides Enabling More-Electric Aircraft Interiors and MRO Efficiency

Aerospace platforms are undergoing electrification at the subsystem level, creating demand for materials that combine FST compliance, low mass, and manufacturability. High-performance polyamides are increasingly specified for cabin interiors, electrical ducting, and secondary structures as OEMs reduce reliance on metals and thermosets.

By 2025, flame-retardant HPPA grades such as PA 2210 FR have been validated against FAR 25.853 requirements, passing the 60-second vertical burn test while delivering lower smoke density and toxicity. These materials are now flight-qualified for components including seat mechanisms, PSU housings, and interior partitions—areas where every kilogram saved directly improves payload efficiency.

Additive manufacturing is amplifying this opportunity. Research published in 2025 demonstrates that SLS-printed PA 12 spare parts achieve ~30% weight reduction versus machined aluminum equivalents, while meeting mechanical and thermal performance requirements. Airlines are increasingly adopting this capability for on-demand cabin refurbishment, reducing spare-part inventories and aircraft-on-ground downtime.

Policy support is reinforcing localization. Regional aerospace initiatives, including India’s 2025 defense and aerospace manufacturing programs, explicitly promote thermoplastic adoption to strengthen domestic supply chains and reduce lifecycle emissions.

Corrosion-Resistant Polyarylamides Replacing Metals in Chemical and Energy Infrastructure

In chemical processing, desalination, and offshore energy, corrosion—not mechanical strength—is the dominant lifecycle cost driver. Polyarylamides (PARA) and PPAs are increasingly displacing stainless steel and specialty alloys in pumps, valves, manifolds, and liners.

Studies published in 2025 indicate that PARA-based components can reduce maintenance frequency by ~40% in high-salinity and chemically aggressive environments, eliminating pitting and crevice corrosion mechanisms inherent to metals. This directly translates into lower unplanned downtime in water treatment and chemical plants.

Processing advances are broadening design freedom. Ixef® PARA from Solvay combines high flowability with tensile strengths approaching 280 MPa, enabling thin-walled, complex geometries that rival cast metals in performance while offering superior surface finish and chemical resistance.

In offshore oil and gas, long-chain PA 11 and PPA materials are increasingly specified for subsea umbilical liners, with certified lifespans approaching 50 years against hydrolysis and hydrogen-induced cracking. As operators prioritize reliability over short-term CAPEX, corrosion-immune polyamides are becoming integral to next-generation deep-water infrastructure.

Market Share Analysis: High-Performance Polyamides Market

Market Share by Product Form: Pelletized HPPA Compounds Dominate Metal-Replacement Programs

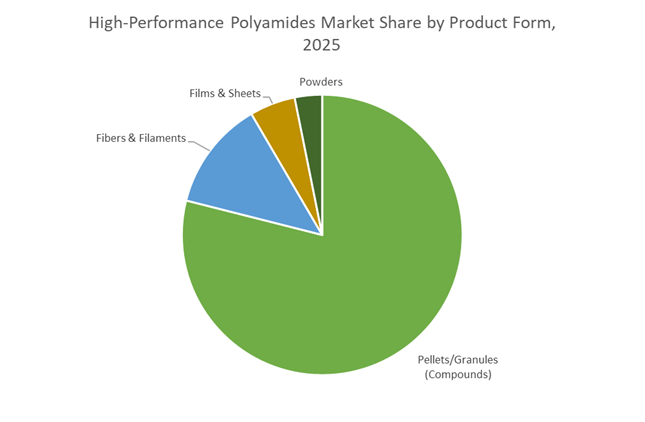

Pellets and granules account for approximately 75% of the High-Performance Polyamides (HPPA) Market because they align directly with how OEMs execute metal-replacement strategies at scale. In 2025, automotive, electrical, and industrial manufacturers are no longer buying base polyamides; they are procuring pre-compounded HPPA pellets engineered with glass fiber, carbon fiber, heat stabilizers, and hydrolysis resistance already embedded at the resin level. This format eliminates in-house compounding variability and ensures predictable mechanical performance across millions of molded parts. The dominance of pellets is tightly linked to long-term durability metrics—particularly in aggressive thermal and chemical environments—where PPAs retain over 90% of mechanical strength after prolonged exposure to hot coolant systems, far outperforming legacy PA66. Dimensional stability has become another decisive driver: low water absorption in advanced HPPA compounds prevents tolerance drift in sensor housings, connectors, and precision brackets, directly reducing warranty risks. From a manufacturing economics standpoint, newer “cold-moldable” HPPA pellets lower tooling temperatures and cycle energy, reinforcing their role as the most scalable, ESG-aligned form factor. These combined factors—lifetime reliability, process efficiency, and system-level risk reduction—cement pellets and granules as the structural backbone of the HPPA market.

Market Share by Application: Under-the-Hood and Powertrain Remain the Ultimate Performance Gatekeepers

Under-the-hood and powertrain applications represent around 40% of total HPPA demand, making them the single largest and most defensible end-use segment. This dominance is not volume-driven alone; it is qualification-driven. Powertrain components operate at the intersection of extreme heat, vibration, chemical exposure, and long service life—conditions that disqualify most engineering plastics. As turbocharged ICE platforms push localized temperatures upward and EV architectures introduce new thermal stress points around batteries and inverters, HPPA has become a non-negotiable material class. OEMs increasingly replace aluminum with HPPA in housings, coolant lines, and transmission components to achieve up to 50% weight reduction per part, directly supporting emissions compliance and range optimization. Beyond weight, HPPA’s superior resistance to hot acidic coolants and biofuel blends has driven adoption in next-generation thermal management systems, where failure tolerance is near zero. An emerging differentiator in 2025 is NVH performance—HPPA gears and structural components damp vibration more effectively than metals, enhancing cabin quietness in both premium ICE and EV models. Coupled with the rise of bio-based HPPA grades that materially reduce Scope 3 emissions, powertrain applications remain the highest-value, highest-barrier segment anchoring HPPA market share.

Competitive Landscape: Five Global Players Scaling Capacity, Circularity and Specialty PA Grades To Capture HPPA Growth

The HPPA competitive field is characterised by global chemical groups and vertically integrated producers that combine advanced resin chemistries (PPA, PA6T, PA12/11), compounding/customisation, and regional capacity plays. Market leaders differentiate via high-temperature grade portfolios, bio- and recycled-feedstock programs, additive-manufacturing powders, and upstream feedstock integration.

BASF SE: Broad Ultramid® PPA Portfolio and Recycling Initiatives Strengthening High-Temp Credentials

BASF offers a wide Ultramid® family including PPA and high-temperature PA 6T/6I grades engineered for dimensional stability and thermal resistance necessary in EV power electronics and under-hood components. The company is advancing chemical recycling for PA6 sourced from end-of-life vehicles (Oct 2025) to create circular, high-quality polyamides-aligning product innovation with sustainability mandates. BASF’s Ultramid H33 L (Sept 2025) and simulation services (Ultrasim) illustrate a strategy to pair materials with design-for-performance tools for rapid OEM qualification.

Arkema S.A.: Rilsan® PA11 Bio-Based Leadership and Singapore Expansion To Serve Clear-Grade and Medical Markets

Arkema is the leading proponent of bio-based PA11 (Rilsan®), derived from castor oil, targeting flexible tubing, high-pressure hydraulic lines and SLS/AM powders. The $20M Singapore Rilsan Clear unit (Jul 2025) will boost PA11 transparent capacity by ~50%, enabling new applications in medical devices and consumer goods. Arkema’s positioning combines sustainable feedstock credentials with powdered grades for industrial additive manufacturing and high-abrasion fluid systems.

Evonik Industries AG: Global PA12 Scale, VESTAMID® Sustainability and Medical-Grade Focus

Evonik is the world’s largest PA12 producer (VESTAMID®) and has expanded long-chain polyamide capacity in Shanghai (Nov 2024) to service Asia’s EV and oil & gas needs. The company’s mass-balanced VESTAMID® eCO PA12 (Oct 2025) demonstrates a major CO₂ reduction pathway (~70%), and its medical-grade VESTAMID® Care compounds meet stringent biocompatibility standards-supporting both industrial and healthcare segments.

Solvay S.A.: Ultra-High-Temperature PAI (Torlon®) and PPA Expertise For Aerospace and Severe-Service Parts

Solvay’s Torlon® polyamide-imide (PAI) delivers continuous use up to ~250°C, making it a go-to resin for aerospace, gas-turbine and severe-service industrial components. The firm’s PPA and specialty polyamides enable metal replacement in E&E and powertrain parts, and its integrated R&D centers work on dielectric strength and hydrolytic stability enhancements required for high-reliability applications.

Ascend Performance Materials: Vertically Integrated PA66 Producer With Compounding and High-Temp Innovations

Ascend (Vydyne® PA66) is the leading fully integrated PA66 producer with control of adiponitrile feedstock, giving it a resilience advantage versus feedstock volatility. The company has been expanding compounding lines to offer glass- and carbon-filled PA66 variants for metal-replacement structural parts and launched Hi-D PA66 grades tailored for thermal hotspots and coolant-exposed components in modern vehicle architectures.

The United States high-performance polyamides market is being reshaped by the convergence of semiconductor policy, automotive lightweighting, and circular-economy mandates. In 2025, expanded U.S. Department of Energy (DOE) programs targeting vehicle efficiency drove a 15% year-on-year increase in the use of high-heat-resistant polyamides for structural and under-the-hood components, reinforcing HPPA adoption across EV platforms. Crucially, CHIPS and Science Act funding is now cascading beyond fabs into advanced polymer substrates, with PPA-based thermal interface materials (TIMs) specified to manage heat in dense AI-accelerator server clusters and high-frequency electronics.

Circularity is becoming a competitive differentiator. In October 2025, BASF introduced two U.S.-based chemical recycling routes for polyamide 6 (PA6) sourced from end-of-life vehicles—solvent-based purification and depolymerization—enabling closed-loop HPPA production with recovered, high-purity monomers. This combination of policy pull (CHIPS/DOE) and technology push (chemical recycling) positions the U.S. as a hub for AI hardware-grade, circular polyamides.

China: EV-Led Capacity Doubling and Whole-Chain Governance of HPPA

China remains the world’s largest producer-consumer nexus for engineering plastics, with 2025 policy focused on 70% self-sufficiency in strategic new materials tied to the EV supply chain. In November 2025, Evonik completed successful trial production on a second polyamides reactor in Shanghai, effectively doubling Asian capacity for long-chain polyamides (LCPA) to meet surging EV connector, fuel-line, and battery component demand.

Regulatory standardization is tightening quality thresholds. The Ministry of Industry and Information Technology (MIIT) finalized 2025 standards for high-temperature polyamides, pairing fiscal incentives with requirements for high-purity PA9T and PA6T production. Simultaneously, revised export monitoring on specialized polymer precursors in late 2025 underscores China’s intent to act as a “whole-chain” governor—from monomers to finished HPPA—amplifying its leverage across global EV and electronics markets.

Germany: Clean Industrial Deal Drives Low-CO₂ PA12 and Monomaterial Design

Germany is leading Europe’s transition toward sustainability-linked high-performance polyamides, even as energy costs pressure commodity production. At K 2025, German producers showcased mass-balanced certified PA12 (VESTAMID®) with up to 70% lower CO₂ footprint versus fossil routes—an explicit response to OEM demand for verified life-cycle reductions. This shift elevates PA12 as a preferred material for lightweight automotive systems, fuel lines, and industrial components.

Public funding is catalyzing new applications. In 2025, subsidies from the Federal Ministry for Economic Affairs and Climate Action supported R&D into PA12 liners for high-pressure hydrogen tanks, leveraging superior gas-barrier performance. In parallel, German engineering teams demonstrated monomaterial vehicle seating using tailored polyamide grades, simplifying recycling and aligning with the EU Circular Economy Action Plan—positioning Germany as a leader in design-for-recycling HPPA architectures.

France: World-Scale Precursors Anchor PA6.6 and Aerospace Polyamides

France has consolidated its role as a critical upstream node in Europe’s HPPA value chain through world-scale precursor capacity. In June 2025, BASF commissioned a 260,000-ton hexamethylenediamine (HMD) plant in Chalampé, securing feedstock for PA6.6 and stabilizing supply for automotive, electrical, and industrial markets across Europe.

Downstream, Arkema expanded Rilsan® (PA11) capacity in July 2025, with France’s aerospace cluster a primary beneficiary for bio-based polyamides used in aircraft fluid lines and clips. Medical innovation added momentum in September 2025, as French majors launched autoclave-resistant medical-grade HPPA for surgical robotics—broadening France’s footprint across aerospace and high-sterility medical applications.

India: Component PLI Spurs PPA Localization for 5G and EV Platforms

India is transitioning from consumption to manufacturing depth in high-performance polyamides, underpinned by targeted incentives and fast-growing domestic demand. The ₹25,000 crore (USD 3 billion) Component PLI (Budget 2025) is channeling investment into PPA production for high-density connectors in smartphones, servers, and 5G infrastructure, accelerating local substitution of imports.

Capacity utilization is rising quickly. After a 40% capacity increase in 2024, BASF India reported in 2025 that Ultramid® lines are fully integrated into EV battery housing supply chains for leading Indian OEMs. Complementing resin production, the Ministry of Chemicals and Fertilizers prioritized Plastic Parks in Gujarat and Tamil Nadu dedicated to glass-filled polyamide compounding, strengthening India’s role as a China+1 HPPA manufacturing base.

Japan: 6G Dielectrics and Bio-Based HPPA Breakthroughs

Japan’s HPPA strategy in 2025 centers on 6G connectivity, sustainability, and advanced recycling. In September 2025, Asahi Kasei unveiled a PFAS-free recycling technology enabling recovery of carbon fiber from HPPA–CFRP automotive pressure vessels without toxic byproducts—addressing both environmental compliance and material recovery.

Telecom-driven innovation is accelerating. Japanese firms are piloting PA12 thin films as low-moisture dielectric layers for 6G hardware, where terahertz signal integrity demands ultra-stable polymers. In October 2025, a Fraunhofer–Japan collaboration announced “Caramide,” a fully bio-based polyamide derived from cellulose byproducts with higher thermal stability than conventional nylon—signaling Japan’s leadership in bio-hybrid, high-frequency HPPA solutions.

2025 National Strategic Matrix: High-Performance Polyamides

High-Performance Polyamides Matrix

|

Country

|

Primary Market Driver

|

2025 Strategic Milestone

|

Material / Technology Focus

|

|

United States

|

AI hardware & circularity

|

Closed-loop PA6 via chemical recycling

|

PPA TIMs, circular HPPA

|

|

China

|

EV supply chain scale

|

LCPA capacity doubling (Shanghai)

|

Long-chain polyamides, PA9T

|

|

Germany

|

Lightweighting & hydrogen

|

Low-CO₂ PA12; monomaterial design

|

Mass-balanced PA12

|

|

France

|

PA6.6 value chain

|

260 kt HMD plant startup

|

Precursors (HMD), PA11

|

|

India

|

Electronics reshoring

|

₹25k Cr Component PLI

|

PPA for 5G connectors

|

|

Japan

|

6G & sustainability

|

PFAS-free CFRP recycling; Caramide

|

Low-loss dielectrics, bio-HPPA

|

High-Performance Polyamides Market Report Scope

High-Performance Polyamides Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.4 Billion

|

|

Market Size (2035)

|

$15.3 Billion

|

|

Market Growth Rate

|

7.5%

|

|

Segments

|

By Material Type (Polyphthalamides, PA 11, PA 12, PA 46, PARA, Specialty High-Temperature Blends & Copolymers), By Product Form (Pellets/Granules, Fibers & Filaments, Films & Sheets, Powders), By Application (Under-the-Hood Automotive Components, E-Mobility & Electrical, Industrial Machinery, Medical & Healthcare, Consumer Goods, Aerospace & Defense), By Processing Method (Injection Molding, Extrusion, Blow Molding, Additive Manufacturing)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Arkema S.A., Evonik Industries AG, Solvay (Syensqo), EMS-CHEMIE HOLDING AG, DuPont de Nemours Inc., Toray Industries Inc., Kuraray Co. Ltd., Mitsui Chemicals Inc., Asahi Kasei Corporation, Ascend Performance Materials, DOMO Chemicals, UBE Industries Ltd., LANXESS AG, Unitika Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

High-Performance Polyamides Market Segmentation

By Material Type

- Polyphthalamides

- PA 11

- PA 12

- PA 46

- PARA (Polyarylamide)

- Specialty High-Temperature Blends & Copolymers

By Product Form

- Pellets/Granules

- Fibers & Filaments

- Films & Sheets

- Powders

By Application

- Under-the-Hood Automotive Components

- E-Mobility & Electrical

- Industrial Machinery

- Medical & Healthcare

- Consumer Goods

- Aerospace & Defense

By Processing Method

- Injection Molding

- Extrusion

- Blow Molding

- Additive Manufacturing (3D Printing)

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in High-Performance Polyamides Market

- BASF SE

- Arkema S.A.

- Evonik Industries AG

- Solvay (Syensqo)

- EMS-CHEMIE HOLDING AG

- DuPont de Nemours, Inc.

- Toray Industries, Inc.

- Kuraray Co., Ltd.

- Mitsui Chemicals, Inc.

- Asahi Kasei Corporation

- Ascend Performance Materials

- DOMO Chemicals

- Ube Industries, Ltd.

- Lanxess AG

- Unitika Ltd.

*- List not Exhaustive