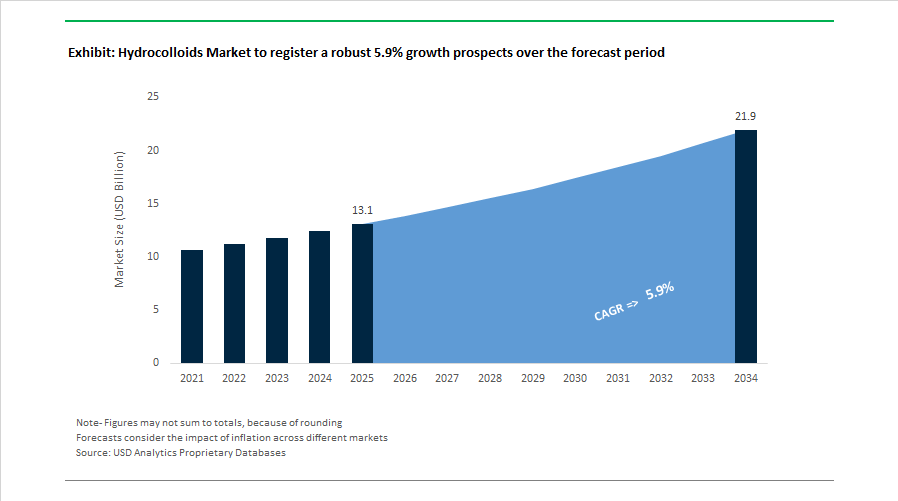

Hydrocolloids Market to Reach $21.9 Billion by 2034 at 5.9% CAGR Fueled by Clean Label Texturants, Fermentation Gums, and Regenerative Supply Chains

The Hydrocolloids Market is projected to expand from $13.1 billion in 2025 to $21.9 billion by 2034, registering a CAGR of 5.9%. Growth is being driven by rising demand for clean label stabilizers, plant-based texturants, fermentation-derived gums, and functional hydrocolloid systems in bakery, dairy alternatives, beverages, pharmaceuticals, and nutrition products. Increasing focus on mouthfeel optimization, sugar reduction, GLP-1 diet compatibility, and supply chain sustainability is reshaping competitive positioning. Major manufacturers are accelerating portfolio integration, microbial production scale-up, and regenerative sourcing strategies to secure long-term raw material resilience and margin stability in the global hydrocolloid industry.

In January 2024, Kerry Group completed the €150 million acquisition of the lactase enzyme business from Chr. Hansen and Novozymes, strengthening its integrated hydrocolloid-enzyme platform for lactose-free and sugar-reduced dairy solutions. In Q1 2024, Ingredion finalized the acquisition of PureCircle, enhancing its plant-based sweetener capabilities while expanding clean label hydrocolloid applications for beverages and dairy alternatives. During 2024, DuPont invested approximately $50 million to scale microbial hydrocolloid production, upgrading purification and fermentation controls for xanthan and gellan gums to meet pharmaceutical and food-grade specifications. In 2024, Gelita AG announced a major expansion of its Iowa facility to increase output of gelatin and collagen-based hydrocolloids for North American nutraceutical and food markets. Roquette also expanded pea-derived hydrocolloid capacity in Asia-Pacific in 2024, deploying advanced automation to supply consistent plant-based texturant systems for meat and dairy analogs. In November 2024, Tate & Lyle finalized its $1.8 billion acquisition of CP Kelco, forming a global specialty hydrocolloid leader combining pectin, specialty gums, and texture solutions under a unified portfolio.

Strategic consolidation and innovation accelerated through 2025. In September 2025, ADM announced restructuring within its Nutrition segment, consolidating its soy protein network and closing an Illinois facility as part of a $500 to $750 million cost-efficiency program designed to optimize specialty ingredient and hydrocolloid operations. In September 2025 at IBIE, IFF launched DANISCO® GRINDSTED® Pectin FB 420, a bake-stable citrus-derived pectin positioned as a label-friendly starch alternative for reduced-sugar bakery products, enhancing flavor release and mouthfeel. Following the CP Kelco acquisition, Tate & Lyle reported in September 2025 that integration efforts were progressing toward $50 million in targeted synergies, focusing on texture and mouthfeel solutions aligned with the expanding GLP-1 medication-driven dietary segment. In late 2025, IFF introduced CURE™, a portfolio of enzyme-hydrocolloid blends engineered to mitigate commodity volatility in eggs and cocoa while preserving product structure and stability.

In 2025, Tate & Lyle extended its regenerative agriculture program to European corn production, deploying AI-driven soil analytics to secure sustainable starch feedstock for hydrocolloid precursors and improve supply chain traceability. The hydrocolloids market is increasingly defined by fermentation technology upgrades, plant-based protein-texturant integration, regenerative raw material sourcing, enzyme-hydrocolloid hybrid systems, and portfolio consolidation among global ingredient leaders serving bakery, dairy, beverage, pharmaceutical, and functional nutrition sectors.

Hydrocolloids Market Trends and Opportunities Driving Functional Ingredient Innovation

Clean-Label and “Free-From” Ingredient Movement Accelerating Adoption of Plant-Based Hydrocolloids

The hydrocolloids market is experiencing strong momentum from the global clean-label and “free-from” food movement, as consumers increasingly avoid synthetic stabilizers and ultra-processed additives. Food manufacturers are therefore shifting toward seaweed- and plant-derived hydrocolloids such as pectin, guar gum, carrageenan, and alginates to deliver texture, viscosity, and stability while maintaining transparent ingredient lists. This transition is particularly visible in processed foods, beverages, and functional nutrition products where natural thickening agents and non-GMO stabilizers are becoming critical for regulatory compliance and consumer acceptance.

Regulatory pressure and corporate portfolio expansion are reinforcing this trend. In May 2025, the Food Safety and Standards Authority of India (FSSAI) restricted misleading “100% Natural” claims on products containing synthetic modifiers, accelerating the adoption of pectin and guar gum as primary thickening agents in the South Asian food industry. Ingredient innovation is also increasing, illustrated by Roquette’s launch of Amysta L 123 at Fi Europe 2025, a thermally processed soluble pea starch designed as a clean-label alternative to modified starches in soups and beverages. Meanwhile, Tate & Lyle’s acquisition of CP Kelco in 2024 significantly expanded its nature-based hydrocolloid portfolio, integrating pectin and gellan gum solutions to meet rising demand for organic-compliant and non-GMO stabilizers. Additionally, the Clean Label Project’s 2025 findings on heavy metal contamination risks in plant proteins are pushing food manufacturers toward hydrocolloid suppliers capable of delivering certified low-lead and low-cadmium botanical gums, creating premium supply opportunities.

Plant-Based and Alternative Protein Innovation Increasing Demand for Advanced Hydrocolloid Texturization Systems

The rapid expansion of plant-based foods and alternative proteins is significantly increasing the need for advanced hydrocolloid texturizing systems capable of replicating the sensory attributes of conventional meat and dairy products. Hydrocolloids play a critical role in protein stabilization, moisture retention, gel formation, and mouthfeel enhancement, helping manufacturers recreate the fibrous structure and juiciness of animal proteins in vegan formulations. As the plant-based food industry scales globally, demand is rising for multi-functional hydrocolloid blends that enable stable high-protein formulations with improved sensory performance.

Recent collaborations highlight this innovation trajectory. In June 2025, Meala partnered with dsm-firmenich to launch Vertis PB Pea, a texturizing pea protein technology incorporating hydrocolloid-like functionality to improve the fibrous structure of plant-based meat analogues. At the same time, increased regulatory scrutiny on dairy analogue beverages by authorities including FSSAI has pushed manufacturers to utilize high-stability hydrocolloids such as iota-carrageenan and gellan gum to prevent sedimentation and phase separation during shelf life. Ingredient circularity is also emerging as a growth avenue, demonstrated by Fuji Brandenburg’s launch of FiPea in 2025, an upcycled pea polysaccharide that enhances mouthfeel and stabilizes proteins in acidic beverages. Complementing these innovations, ADM’s 2025 investor strategy emphasizes “texture-first” formulation systems, combining soy protein hydrolysates with botanical hydrocolloids to deliver high-protein foods with simplified ingredient lists.

Precision Fermentation and Cultivated Meat Creating New Functional Roles for Hydrocolloid Systems

Emerging precision fermentation and cultivated meat technologies are opening a new frontier for hydrocolloid applications. In these next-generation food systems, hydrocolloids act as encapsulation agents, stabilizers, and structural scaffolds that enable the development of bio-engineered proteins and cultured tissues. As the alternative protein industry moves toward commercialization, the demand for functional biopolymers such as agar, alginates, collagen, and chitosan is expected to expand significantly.

The precision fermentation sector, valued at approximately $5.93 billion in 2025, is increasingly using agar and alginate hydrocolloids to encapsulate engineered microbes and stabilize proteins in products developed by companies such as Perfect Day and The EVERY Company. In the cultivated meat segment, a 2026 research review published in PMC identified scaffold design as a critical bottleneck for scaling production, with hydrocolloids like collagen and chitosan being explored as biodegradable matrices capable of supporting three-dimensional muscle cell growth. Beyond human food, the cultivated pet protein segment is also emerging, with companies such as Bond Pet Foods and UMAMI Bioworks utilizing hydrocolloid-based formulations to stabilize fermentation-derived proteins and enable high-speed extrusion for pet food manufacturing.

Expanding Pharmaceutical, Nutraceutical, and Wound-Care Applications Unlocking High-Value Hydrocolloid Demand

Beyond the food industry, hydrocolloids are increasingly penetrating pharmaceutical, nutraceutical, and medical applications, where their gel-forming, moisture-retention, and controlled-release properties provide significant functional advantages. These characteristics make hydrocolloids valuable for wound management products, targeted drug delivery systems, and advanced nutraceutical delivery technologies, opening new high-margin growth segments for hydrocolloid manufacturers.

Clinical research published in February 2025 confirmed the rapid expansion of hydrocolloid dressings in dermatology and acne care, particularly in consumer “pimple patch” treatments that form a protective gel layer to accelerate healing and reduce infection risk. In pharmaceutical applications, studies in 2025 highlighted the use of oxidized kappa-carrageenan combined with magnetic nanoparticles to enable zero-order controlled drug release, improving dosing consistency and reducing side effects. Meanwhile, in the global nutraceutical market, hydrocolloids such as pectin and alginate are being utilized in beadlet delivery systems that encapsulate probiotics and vitamins, protecting them from gastric degradation and ensuring targeted release in the lower gastrointestinal tract. These innovations are positioning hydrocolloids as critical functional biomaterials across healthcare, functional nutrition, and advanced therapeutic formulations.

Hydrocolloids Market Share and Segmentation Insights

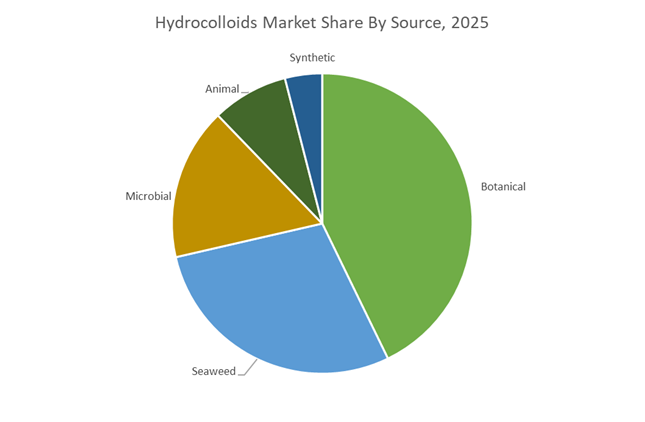

Botanical Hydrocolloids Dominate the Market Through Natural Ingredient Demand and Agricultural Supply Chains

Botanical hydrocolloids accounted for 42.80% of the Hydrocolloids Market share in 2025, making them the largest source category across food, pharmaceutical, and industrial formulations. Botanical hydrocolloids including pectin, guar gum, locust bean gum, modified starches, and cellulose derivatives dominate the market due to their broad functional versatility in thickening, gelling, stabilizing, and water-binding applications. Their dominance is also supported by strong consumer preference for plant-derived, clean-label ingredients, particularly in food and beverage formulations where natural positioning significantly influences purchasing decisions. Established agricultural supply chains for crops such as guar beans, citrus fruits, apples, and potatoes ensure reliable global production of botanical hydrocolloid raw materials. In 2025, manufacturers are increasingly integrating upcycled botanical sourcing strategies, extracting hydrocolloids from food processing byproducts such as citrus peel for pectin, apple pomace for fiber-rich hydrocolloids, and potato starch residues, aligning ingredient production with circular economy principles. This approach improves raw material efficiency, reduces food waste, and strengthens sustainability narratives for ingredient suppliers targeting environmentally conscious food manufacturers.

Food and Beverage Industry Drives the Largest Hydrocolloid Consumption

Food and Beverages represented 58.60% of the Hydrocolloids Market share in 2025, establishing the sector as the primary consumer of hydrocolloid ingredients worldwide. Hydrocolloids play a critical role in modern food formulation by delivering texture modification, viscosity control, gel formation, moisture retention, and product stability, which are essential attributes in processed foods. They are widely used in applications such as sauces and dressings, dairy products, confectionery, bakery fillings, frozen desserts, and ready-to-eat meals, where they enhance mouthfeel and prevent phase separation or syneresis. The sector is also undergoing a significant transformation driven by the rapid expansion of plant-based food products, including dairy alternatives and meat analogs. In 2025, hydrocolloid demand is being shaped by the need to replicate functional and sensory properties of animal-derived ingredients, with specialized hydrocolloid systems developed for vegan cheese elasticity, plant-based yogurt creaminess, and fibrous structures in meat substitutes. These formulations typically combine multiple hydrocolloids to achieve the required rheological properties, creating strong growth opportunities for suppliers offering tailored hydrocolloid blends.

Competitive Landscape in the Hydrocolloids Market

The Hydrocolloids Market is characterized by strong competition among global food ingredient and biotechnology companies focusing on natural texturants, stabilizers, emulsifiers, and gelling agents used across food & beverages, pharmaceuticals, personal care, and nutraceutical formulations. Leading players are strengthening market positions through strategic acquisitions, fermentation-based biopolymer production, clean-label ingredient innovation, and AI-driven supply chain optimization. Increasing demand for plant-based foods, low-sugar formulations, functional beverages, and texture-enhancing ingredients is driving investment in pectin, xanthan gum, carrageenan, gellan gum, guar gum, and acacia-based hydrocolloid solutions, making R&D capabilities and global sourcing networks critical competitive differentiators.

Tate & Lyle Expands Global Hydrocolloid Leadership Through the $1.8 Billion CP Kelco Acquisition

Tate & Lyle PLC has significantly strengthened its presence in the global hydrocolloids market following the $1.8 billion acquisition of CP Kelco completed in November 2024, positioning the company as a leading supplier of pectin, carrageenan, specialty gums, and nature-based texturants. By the first quarter of 2026, the integration contributed to a 15% increase in group revenue, supported by strong demand for texture and mouthfeel solutions in reduced-sugar food formulations. The company expects to generate over $50 million in annual run-rate cost synergies by FY2027, while cross-selling opportunities in its innovation pipeline increased by more than 33% in Q4 2025. Tate & Lyle now operates the world’s largest pectin production facility in Lille Skensved, Denmark, where $10.7 million (DKK 60 million) has been invested to expand GENU® amidated pectin production for low-sugar and dairy applications, serving customers in over 120 countries.

Ingredion Drives Clean-Label Hydrocolloid Innovation for Plant-Based Food Applications

Ingredion Incorporated is strengthening its position in the functional hydrocolloids and clean-label ingredient market by focusing on advanced texturizing systems for plant-based dairy and alternative protein products. In 2025, the company launched NOVATION® Indulge 2940, a functional native corn starch designed to replicate the creamy mouthfeel of fat in dairy alternatives while maintaining clean-label declarations without modified starch labeling. Sustainability initiatives are also central to its strategy, with 40% of global energy consumption transitioned to renewable sources by late 2025, alongside investments in localized supply chains across the Asia-Pacific region, the fastest-growing hydrocolloid market. Ingredion’s 2026 innovation roadmap emphasizes “texture-plus-nutrition”, integrating hydrocolloids such as guar gum and acacia with plant proteins to solve structural challenges in 3D-printed plant-based meat formulations. The company also collaborates with food-tech startups using machine-learning algorithms to predict hydrocolloid blend rheology, reducing product development cycles by approximately 25%.

IFF Strengthens Fermentation-Based Hydrocolloid Production for Food and Medical Nutrition Markets

International Flavors & Fragrances Inc. (IFF) continues to expand its role in the biopolymer hydrocolloids market through its Health & Biosciences division, which specializes in fermentation-derived ingredients such as xanthan gum and gellan gum. In its 2025 full-year report released in February 2026, the segment generated $2.28 billion in revenue with a 26% adjusted operating EBITDA margin, driven by high-single-digit growth in its Food Biosciences unit. IFF remains a leader in bio-fermented hydrocolloid production, recently launching dysphagia-grade biopolymers in 2025 designed for medical nutrition products that require stable particle suspension and safe swallowing characteristics. As part of its portfolio optimization strategy, the company plans to divest its Soy Crush, Concentrates, and Lecithin business by March 31, 2026, allowing greater focus on high-margin specialty texturants. Internal consumer research also indicates 40% of global consumers prioritize texture in food choices, guiding IFF’s “Mouthfeel Solutions” innovation platform.

Cargill Utilizes AI-Driven Supply Chain Optimization to Expand Hydrocolloid Ingredient Solutions

Cargill, Incorporated is leveraging its global ingredient supply chain and digital infrastructure to strengthen its presence in the industrial hydrocolloids market, particularly in pectin, carrageenan, and functional biopolymers used across food processing applications. In January 2026, Cargill was recognized in the BIG Innovation Awards as a “Top 10 Innovator”, highlighting its large-scale deployment of AI and predictive analytics to optimize food ingredient manufacturing and distribution networks. Responding to volatility in global pectin supply, the company introduced a cost-effective pectin replacer in late 2025, targeting confectionery and fruit preparation markets in emerging economies. Sustainability initiatives also contributed to a reduction of 31,500 metric tons of CO₂ emissions, achieved through logistics and manufacturing optimization that reduces Scope 3 emissions for hydrocolloid customers. Cargill’s hydrocolloids operations are now integrated into its Port Optimizer logistics system, delivering an estimated 30× return on investment through improved shipping efficiency.

Kerry Group Expands Sustainable Hydrocolloid Solutions Through Accelerate 2.0 Manufacturing Strategy

Kerry Group plc continues to expand its presence in the specialty hydrocolloid and food texturants market, focusing on sustainable nutrition and advanced ingredient solutions. In fiscal year 2025, reported in February 2026, Kerry generated €6.8 billion in revenue with an 18% EBITDA margin, supported by 3% volume growth that outperformed the global food and beverage sector. Following the successful completion of its KerryAccelerate program (2022–2025), the company launched Accelerate 2.0 (2025–2028) to enhance digital manufacturing capabilities and optimize its global network of hydrocolloid and texturant production facilities. Strong end-use demand was recorded in meat applications, which grew by 8%, and dairy applications, which increased by 5% during 2025, reflecting the industry shift toward clean-label and nutritionally enhanced food formulations. Sustainability initiatives have also achieved a 52% carbon reduction and a 54% decrease in food waste, while Kerry’s nutrition solutions now reach more than 1.46 billion consumers worldwide.

United States: Regulatory Reformulation and Cross-Sector Hydrocolloid Innovation

The United States hydrocolloids industry is undergoing accelerated reformulation driven by regulatory change, ingredient localization, and expanding non-food applications. In April 2025, the U.S. Food and Drug Administration announced measures to phase out petroleum-based synthetic dyes, including Red No. 3, during the 2025–2026 period. This decision has triggered a rapid shift toward natural color systems that depend on hydrocolloid matrices to stabilize plant-derived pigments such as butterfly pea, spirulina, and gardenia blue, particularly in acidic beverage formulations where color degradation is a persistent challenge.

Industrial players are reinforcing this transition with automation and adjacent-market exploration. Cargill deployed AI-enabled robotic units in October 2025 to improve safety and consistency in texturizer production at facilities serving the U.S. market. Earlier in May 2025, Cargill partnered with Arizona State University to investigate hydrocolloid use in semiconductor polishing and packaging, signaling expansion beyond traditional food and beverage applications. Portfolio centralization is also reshaping competition. In October 2025, Ingredion appointed a new executive vice president for Global Texture and Healthful Solutions, consolidating hydrocolloid assets to accelerate fiber-fortified and reduced-sugar texturizing systems. Looking ahead, trade policy adjustments in early 2026 are encouraging domestic R&D in corn-derived and microbial hydrocolloids such as xanthan gum, as U.S. producers seek to offset rising import costs for agar and carrageenan sourced from Asia-Pacific suppliers.

India: Domestic Ingredient Nationalism and Processing Capacity Expansion

India’s hydrocolloids market is being shaped by food ingredient localization, pharmaceutical demand, and preservation infrastructure investment. At the AAHAR-2025 summit in March 2025, the Ministry of Food Processing Industries emphasized a Made-in-India agenda for food ingredients. This policy stance catalyzed the World Food India 2025 summit, where rapid testing frameworks for hydrocolloid purity and authenticity were prioritized to strengthen domestic supply credibility.

Chemical capacity optimization is supporting this agenda. By mid-2025, Gujarat Alkalies and Chemicals Ltd. optimized high-purity chemical lines to support the synthesis of guar gum derivatives for pharmaceutical formulations and oilfield drilling fluids. Regulatory incentives are reinforcing downstream adoption. Updated MoFPI scheme guidelines released in January 2025 provide financial support for processors expanding cold-chain and preservation capacity, explicitly encouraging integration of advanced hydrocolloids to improve freeze-thaw stability and texture retention in frozen foods. Together, these initiatives are moving India from bulk hydrocolloid consumption toward regulated, application-specific usage.

Brazil: Algaculture Scale-Up and Biodiversity-Linked Supply Chains

Brazil is emerging as a strategic hub for seaweed-based hydrocolloids, anchored in climate commitments and regulatory clarity for marine farming. At COP30 in November 2025, Brazil formally joined the United Nations Global Seaweed Initiative, committing to scale domestic algaculture with a focus on Kappaphycus alvarezii for high-quality carrageenan production. This commitment positions hydrocolloids as both an industrial input and a climate-positive agricultural activity.

Policy support is translating into bankable projects. In 2026, the Ministry of Fisheries and Aquaculture introduced a new regulatory framework for marine farming that streamlines licensing and investment approvals for large-scale seaweed processing plants along the Brazilian coast. Environmental outcomes are reinforcing social license. Community-led red algae cultivation pilots in Paraty reported measurable returns of marine species in late 2025, demonstrating biodiversity restoration alongside income generation. These results are strengthening Brazil’s case for hydrocolloid production as a regenerative economic activity.

Germany: Industrial Hydrocolloids in Catalysis and Emissions Compliance

Germany’s hydrocolloids industry is increasingly tied to advanced industrial applications rather than food alone. In 2026, BASF expanded its X3D catalyst technology, which leverages hydrocolloid-based binders to shape high-selectivity catalysts for fine chemical reactions. This approach improves flow dynamics and surface area control in reactors, highlighting hydrocolloids as functional materials in precision chemistry.

Regulatory drivers are accelerating adoption. Following EU REACH updates in 2025, Clariant pivoted toward chromium-free hydrogenation platforms that rely on hydrocolloid-stabilized catalyst carriers. These systems are designed to comply with the 2026 Industrial Emissions Directive while maintaining reaction efficiency. Germany’s trajectory underscores a shift toward hydrocolloids as enablers of low-emission, high-performance industrial processes.

China: Medical Localization and Circular Polymer Systems

China’s hydrocolloids industry is advancing through localization mandates and integration with circular materials strategies. Under the Made in China 2025 tail-end objectives, the Ministry of Industry and Information Technology prioritized medical-grade hydrocolloids for wound care and drug delivery, targeting 70% domestic content. This focus is strengthening local supply of alginates, cellulose derivatives, and gelatin substitutes for healthcare use.

Circular polymer innovation is also influencing demand. In January 2025, a joint facility in Shanghai operationalized chemical recycling for Nylon 6 that incorporates specialized colloidal systems to enable textile-to-textile circularity under the loopamid platform. These developments position hydrocolloids as functional agents not only in life sciences but also in advanced materials recovery and reuse.

European Union: Regulatory Streamlining and Digital Compliance

At the regional level, the European Union is reshaping hydrocolloid usage through pharmaceutical and chemical regulatory modernization. The revised Variations Regulation, effective January 2025 with full implementation by January 15, 2026, streamlines how pharmaceutical manufacturers update formulations that include hydrocolloid excipients. This change reduces approval timelines for texture and stability improvements in human medicines.

Supply chain transparency is also evolving. A July 2025 proposal by the European Commission allows digital labeling for hazardous chemicals, directly affecting industrial-grade hydrocolloid suppliers managing multi-country distribution. Digital documentation is expected to reduce compliance friction and improve traceability across complex EU logistics networks.

Summary Table: Country-Level Strategic Signals in the Hydrocolloids Industry

Hydrocolloids Market County Level Snapshot

|

Geography

|

Primary Strategic Driver

|

Key Hydrocolloid Focus

|

Structural Implication

|

|

United States

|

FDA dye phase-out, tariff shifts

|

Natural color stabilization, xanthan gum

|

Reformulation and domestic innovation

|

|

India

|

Made-in-India policy, MoFPI schemes

|

Guar derivatives, food preservation

|

Localized supply and quality control

|

|

Brazil

|

UN seaweed commitment, algaculture law

|

Carrageenan from red algae

|

Regenerative growth and export potential

|

|

Germany

|

Industrial catalysis, emissions rules

|

Hydrocolloid binders

|

High-value industrial applications

|

|

China

|

Medical localization, circular polymers

|

Medical-grade hydrocolloids

|

Import substitution and circularity

|

|

European Union

|

Pharma regulation, digital labeling

|

Excipient reformulation

|

Faster compliance and transparency

|

Hydrocolloids Market Report Scope

Hydrocolloids Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$13.1 Billion

|

|

Market Size (2034)

|

$21.9 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Source (Botanical, Seaweed, Microbial, Animal, Synthetic), By Function (Thickening Agents, Gelling Agents, Stabilizers and Emulsifiers, Fat Replacers, Coating and Film-Forming Agents), By Application (Food and Beverages, Pharmaceuticals and Healthcare, Cosmetics and Personal Care, Industrial Applications)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Cargill, Incorporated, Ingredion Incorporated, CP Kelco, International Flavors & Fragrances Inc., Archer Daniels Midland Company, Tate & Lyle PLC, Kerry Group plc, BASF SE, Darling Ingredients Inc., Gelymar S.A., DuPont de Nemours, Inc., Ashland Inc., FMC Corporation, Alland & Robert, Acadian Seaplants Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Hydrocolloids Market Segmentation

By Source

- Botanical

- Seaweed

- Microbial

- Animal

- Synthetic

By Function

- Thickening Agents

- Gelling Agents

- Stabilizers and Emulsifiers

- Fat Replacers

- Coating and Film-Forming Agents

By Application

- Food and Beverages

- Pharmaceuticals and Healthcare

- Cosmetics and Personal Care

- Industrial Applications

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Hydrocolloids Industry

- Cargill, Incorporated

- Ingredion Incorporated

- CP Kelco

- International Flavors & Fragrances Inc.

- Archer Daniels Midland Company

- Tate & Lyle PLC

- Kerry Group plc

- BASF SE

- Darling Ingredients Inc.

- Gelymar S.A.

- DuPont de Nemours, Inc.

- Ashland Inc.

- FMC Corporation

- Alland & Robert

- Acadian Seaplants Limited

*- List not Exhaustive