Industrial Protective Clothing Fabrics Market to Reach $24 Billion by 2034 at 7.9% CAGR Driven by PFAS-Free Innovation, Bio-Based Aramids, and Connected Worker PPE

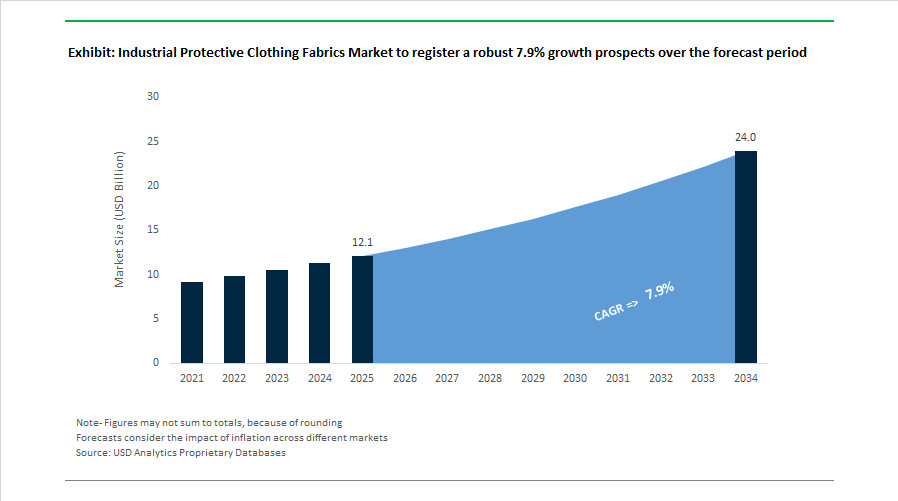

The Industrial Protective Clothing Fabrics Market is projected to expand from $12.1 billion in 2025 to $24 billion by 2034, registering a robust CAGR of 7.9%. Growth is anchored in tightening occupational safety regulations, increasing industrial automation, expansion of energy and infrastructure projects, and accelerating ESG mandates across manufacturing, oil and gas, utilities, mining, and emergency response sectors. Demand is shifting toward advanced flame-resistant (FR) fabrics, chemical protective textiles, high-visibility UV-resistant materials, and smart PPE fabrics integrating sensor compatibility. Manufacturers are prioritizing breathable barrier fabrics, PFAS-free chemistries, low-carbon aramid fibers, and recyclable textile systems to meet regulatory and corporate sustainability benchmarks.

Innovation momentum strengthened beginning in 2024. In May 2024, Teijin Frontier introduced a multifunctional polyester fabric inspired by traditional bamboo blind structures, incorporating a three-dimensional slit architecture to deliver high air permeability with 85% UV protection, targeting heat-exposed outdoor industrial workers. In September 2024, DuPont commercially launched a new bio-based aramid fiber with a 30% lower carbon footprint compared to petroleum-based equivalents, reinforcing the shift toward sustainable inherent flame-resistant textiles. In November 2024, Honeywell formed a strategic partnership to embed IoT-enabled biometric sensors into FR apparel, advancing the “connected worker” model by enabling real-time monitoring of environmental hazards and physiological stress.

Regulatory pressure and circular economy strategies accelerated in 2025. In December 2024, Milliken became the first textile manufacturer to offer non-PFAS materials across all three layers of firefighter turnout gear, positioning suppliers ahead of U.S. state-level PFAS bans taking effect in 2027. In April 2025, Cintas launched a nationwide recycling program for end-of-life FR garments, converting used protective apparel into reusable raw materials. That same month, Milliken released its 2024 Sustainability Report, confirming that 100% of new product developments underwent sustainability assessment under its N/XT Life™ circularity initiative. In May 2025, TenCate Protective Fabrics marked 100 years of U.S. textile manufacturing in Georgia, reinforcing domestic FR fabric production resilience amid global supply volatility. In June 2025, Teijin Frontier announced the upcoming Fall/Winter 2026 launch of SOLOTEX® stretch fabric utilizing PTT polymers instead of polyurethane, improving durability and weight efficiency in industrial workwear.

Advanced barrier and certification capabilities expanded significantly in late 2025. In November 2025, DuPont unveiled Tyvek® APX™ at the A+A trade fair in Germany, introducing a next-generation disposable chemical protective fabric engineered to improve breathability while maintaining stringent hazardous chemical barrier performance. In November 2025, India’s National Technical Textiles Mission confirmed the development of indigenous heat-resistance testing systems for convective, radiant, and contact heat protection, strengthening domestic compliance with global PPE standards. Earlier in January 2025, 3M completed the acquisition of a specialty textile technology firm, gaining proprietary moisture-wicking treatments compatible with flame-retardant garments, improving wearer comfort in high-temperature industrial environments. These developments underscore a structural transformation of the industrial protective clothing fabrics market toward high-performance, low-carbon, sensor-compatible, and PFAS-free textile systems aligned with evolving safety, environmental, and performance standards.

Industrial Protective Clothing Fabrics Market Trends and Opportunities

Mandatory Transition to NFPA 70E (2024 Edition) and NFPA 2112 Compliant Inherent FR Fabrics

The enforcement cycle following the 2024 update of NFPA 70E has transformed flame-resistant protective clothing from a discretionary safety upgrade into a compliance-critical procurement category for utilities, energy producers, and industrial maintenance contractors. The revised standard places heightened emphasis on Electric Shock Risk Assessments, energized work under “normal operating conditions,” and documentation of personal protective equipment performance. As a result, industrial buyers are systematically replacing treated cotton FR fabrics with inherent flame-resistant fibers that deliver permanent protection across the garment lifecycle.

This regulatory shift is reinforced by the tightening alignment between NFPA 70E and NFPA 2112, which now requires third-party certification not only of fabrics but also of finished garments. This has elevated demand for inherently flame-resistant fibers with proven Arc Thermal Performance Value consistency after repeated industrial laundering. Market audits conducted across North American utility operators in 2025 indicate that garments manufactured from inherent FR fabrics reduce replacement frequency by up to 30% over a five-year service window, offsetting higher upfront costs. Insurance underwriters have further accelerated adoption by explicitly excluding untreated synthetic blends from acceptable risk profiles, given arc flash temperatures that can exceed 35,000°F and cause molten polymer injuries. Collectively, these forces are pushing the market toward premium, traceable, standards-compliant fabric platforms that minimize compliance risk while extending asset life.

Lightweight Multi-Hazard Fabrics for Semiconductor and Biopharma Cleanroom Operations

A second structural trend is emerging from the rapid expansion of semiconductor fabrication plants and biopharmaceutical clean manufacturing facilities. These environments require protective clothing fabrics that simultaneously meet ISO Class 1 to 5 cleanroom standards and provide resistance to aggressive chemical exposures, including hydrofluoric acid and solvent-based etchants. Traditional chemical protective fabrics struggle to meet ultra-low linting and outgassing thresholds, creating demand for engineered multilayer and laminated nonwoven textiles.

By mid-2025, leading cleanroom operators were specifying fabrics capable of blocking more than 99.9% of sub-micron particulates while maintaining high tensile integrity under repetitive movement. At the same time, worker heat stress has become a measurable productivity constraint. Industry pilot data from advanced packaging and biologics assembly lines show that next-generation breathable chemical barrier fabrics can reduce core body temperature rise by approximately 1.2°C versus legacy PVC-coated materials. This performance gain translates into longer continuous work intervals, fewer breaks, and higher yield stability in high-precision manufacturing. As a result, cleanroom-compatible, lightweight, multi-hazard protective fabrics are transitioning from niche applications into a high-growth segment of the industrial protective clothing fabrics market.

Smart Protective Fabrics for Proactive Heat Stress and Worker Health Monitoring

Regulatory momentum around occupational heat exposure is opening a high-impact opportunity for sensor-integrated protective clothing fabrics. The proposed U.S. OSHA Heat Injury and Illness Prevention rule in 2025 establishes defined temperature thresholds that trigger mandatory monitoring and intervention. This framework is accelerating adoption of smart fabrics embedded with physiological and environmental sensors capable of tracking heart rate, respiration, and ambient heat in real time.

Field trials conducted in 2025 across construction, foundry, and utility maintenance environments demonstrate that sensor-embedded garments can detect multiple physiological strain states with accuracy approaching 99%. These systems enable predictive alerts before workers reach dangerous heat stress levels, reducing incident rates and medical downtime. Advances in washable, energy-harvesting e-textiles announced in early 2025 have removed one of the primary adoption barriers by eliminating bulky batteries and preserving garment comfort. For employers, smart protective fabrics are evolving into a risk management and productivity tool, with early adopters reporting up to 40% reductions in heat-related incidents in high-exposure operations.

PFAS-Free Durable Water Repellent Finishes for Food Processing and Agriculture

The final major opportunity shaping the market is the rapid phase-out of PFAS-based durable water repellent finishes across food processing, agriculture, and allied industrial sectors. Regulatory bans introduced in key U.S. states and reinforced through EU REACH restrictions have made PFAS-free compliance a non-negotiable requirement for protective clothing used around food oils, fats, and biological contaminants.

As of January 2025, major textile certification frameworks eliminated all intentionally added PFAS, forcing fabric manufacturers to commercialize alternative chemistries. Bio-based and inorganic hybrid solutions are emerging as viable replacements, with recent trials showing that plant-derived and ceramic-modified coatings can achieve oil and water repellency comparable to legacy fluorochemicals. The commercial challenge lies in durability under industrial laundering, where garments must retain repellency through 50 or more wash cycles. Early performance data from 2025 indicate that next-generation PFAS-free finishes are approaching this threshold, creating a scalable opportunity for suppliers that can combine regulatory compliance, lifecycle durability, and cost efficiency. As food safety audits tighten globally, PFAS-free repellent protective fabrics are positioned to become a standard specification rather than a premium option.

Industrial Protective Clothing Fabrics Market Share and Segmentation Insights

Aramid Fiber Blends Dominate Industrial Protective Clothing Fabrics Through Inherent Flame Resistance

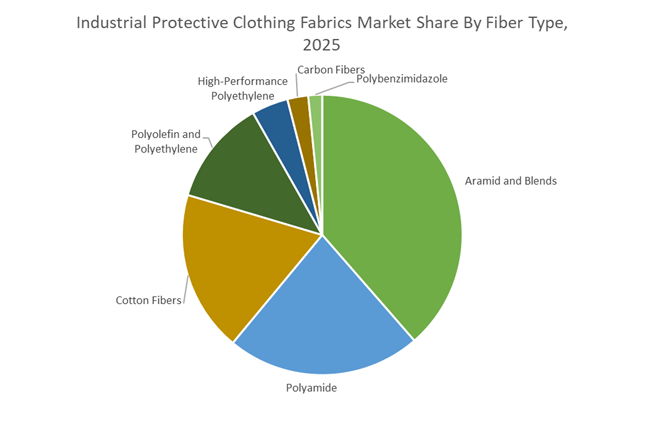

Aramid and blended fibers accounted for 38.60% of the Industrial Protective Clothing Fabrics Market share in 2025, making them the leading fiber category used in advanced protective garments. Aramid fibers including meta-aramid and para-aramid are widely used in industrial protective clothing because they deliver inherent flame resistance, exceptional thermal stability, high tensile strength, and long-term durability without requiring chemical flame-retardant treatments. These characteristics make aramid-based fabrics the preferred material for protective garments used in oil and gas operations, fire service uniforms, electrical utility maintenance, welding operations, and high-temperature industrial environments. Unlike treated fabrics, aramid fibers retain flame-resistant performance throughout the life of the garment because the protection is built directly into the fiber structure. In 2025, textile manufacturers are advancing fiber spinning technologies, hybrid fabric constructions, and moisture management finishes to improve wearer comfort and breathability while maintaining strict protective performance standards. These innovations address long-standing concerns about garment stiffness and heat buildup, supporting better worker compliance with mandatory safety apparel programs.

Oil and Gas Industry Drives the Largest Demand for Industrial Protective Clothing Fabrics

Oil and Gas represented 32.80% of the Industrial Protective Clothing Fabrics Market share in 2025, establishing it as the largest end-use sector for flame-resistant industrial textiles. Oil and gas operations involve numerous high-risk environments including drilling rigs, offshore platforms, pipeline systems, refineries, and petrochemical plants, where workers are exposed to potential hazards such as flash fires, hydrocarbon fires, electrical arcs, and high-temperature equipment. To mitigate these risks, most energy companies enforce strict flame-resistant (FR) clothing programs that require protective garments for field personnel, maintenance crews, and plant operators. These programs generate continuous demand for high-performance protective fabrics capable of meeting stringent industrial safety standards. In 2025, the increasing globalization of energy operations has accelerated demand for protective fabrics that comply with multiple international safety certifications such as NFPA, EN, and ISO standards within a single garment design. Multinational energy companies prefer standardized protective clothing programs that can be deployed across global facilities, ensuring consistent worker protection and simplifying procurement across international operations.

Competitive Landscape in the Industrial Protective Clothing Fabrics Market

The Industrial Protective Clothing Fabrics Market is shaped by leading material science and safety technology companies focusing on multi-risk PPE fabrics, flame-resistant (FR) textiles, aramid fiber innovations, and sustainable protective clothing solutions. Market leaders are strengthening their competitive positions through PFAS-free textile development, circular economy initiatives, advanced aramid fibers, high-performance reflective materials, and vertically integrated manufacturing capabilities.

DuPont Strengthens Multi-Hazard PPE Leadership with Nomex® and Kevlar® Fabric Innovations

DuPont Personal Protection remains a global benchmark in the industrial protective clothing fabrics market, driven by its flagship Nomex® and Kevlar® aramid fiber technologies that dominate high-performance flame-resistant PPE. In November 2025, DuPont introduced its first Global Innovation Awards at the A+A trade fair, highlighting next-generation fabrics engineered for multi-hazard protection against electric arc, chemical exposure, and thermal risks, particularly for renewable energy applications. The company also commercialized post-consumer Nomex® Recycled garments in 2025, developed with Iturri SA, incorporating 30% recycled materials to reduce the environmental footprint of aramid fiber production. DuPont further advanced firefighter protection with Nomex® Xtreme Max and Nomex® Nano FlexLAM AIR technologies, the latter utilizing an innovative air cushion fabric structure to enhance breathability while maintaining particulate protection. Additionally, through its partnership with SureWerx, DuPont launched the 40 Cal LAN Series Arc Flash Suit in late 2025, delivering ultra-lightweight protection for electrification and utility sector workers.

Milliken Advances PFAS-Free Protective Textile Innovation and Firefighter Gear Technology

Milliken & Company has emerged as a leader in sustainable industrial protective fabrics, becoming the first major U.S. textile manufacturer to eliminate PFAS-based finishes and fibers from its entire industrial textile portfolio by 2025. This milestone positions the company as a preferred supplier for environmentally responsible protective workwear and fluorine-free PPE systems.

In late 2024, Milliken launched Milliken Assure™, North America’s first non-PFAS, non-halogenated flame-resistant moisture barrier for firefighter turnout gear, exceeding UL-certified NFPA 1971-2018 standards. The company also strengthened its innovation credentials through a strategic collaboration with NASA in 2024 to develop next-to-skin flame-resistant fabrics for Artemis astronauts, designed to maintain thermal protection and skin integrity in oxygen-rich environments. Supported by 22 vertically integrated manufacturing facilities across the southeastern United States, Milliken maintains full fiber-to-finish control, enabling rapid development of advanced fabrics such as the Polartec® Power Shield™ Pro bio-based waterproof membrane technology.

Teijin Aramid Expands Circular Aramid Fiber Ecosystem for High-Strength Protective Textiles

Teijin Aramid, a subsidiary of Teijin Limited, is a global leader in para-aramid and meta-aramid fiber technology, supplying high-strength materials for industrial protective clothing, motorsports safety gear, and high-risk work environments. The company accelerated its “Recovery over Landfilling” circularity strategy between 2024 and 2025, collaborating with industrial laundries and garment manufacturers to create a closed-loop recycling system for aramid-based PPE, supporting its carbon neutrality target by 2050.

Teijin’s Twaron® para-aramid and Teijinconex® neo meta-aramid fibers are widely adopted in next-generation industrial workwear and racing suits, offering strength up to six times greater than steel on a weight-for-weight basis, which significantly reduces garment weight and worker fatigue. The company also expanded its dope-dyed fiber technology, embedding pigments directly into polymer solutions before spinning to improve UV resistance, colorfastness, and lifecycle durability of protective fabrics used in harsh outdoor industrial environments. In 2024, Teijin Aramid received the EcoVadis Gold Medal for sustainability, highlighting its leadership in environmental stewardship and responsible material sourcing.

Lakeland Industries Expands Fire and Industrial PPE Portfolio Through Strategic Acquisitions

Lakeland Industries has undergone a major strategic transformation, rebranding as Lakeland Fire + Safety to accelerate its expansion within the global fire services and industrial protective clothing market. Between late 2024 and early 2026, Lakeland executed several strategic acquisitions including LHD, Jolly Scarpe, Pacific Helmets, and Arizona PPE Recon, enabling the company to transition from basic protective garments to a comprehensive head-to-toe firefighter and industrial safety equipment provider.

In early 2026, Lakeland reported pursuing approximately $178 million in global safety equipment tenders, including a 12-year contract renewal with Fire and Emergency New Zealand and a major protective equipment contract with Argentina’s National Civil Aviation Administration (ANAC). To enhance supply chain resilience amid tariff pressures, Lakeland increased its strategic inventory by $14.2 million in early 2025, ensuring consistent supply of chemical protective suits and firefighting turnout gear. The 2025 acquisition of PPE Recon businesses also introduced a new recurring revenue stream focused on inspection, cleaning, and repair (ISP) services for protective garments, increasingly mandated by industrial safety regulations.

3M Enhances Industrial Visibility and Flame-Resistant Safety Fabrics with Scotchlite™ Technology

3M’s Personal Safety Division continues to dominate the high-visibility industrial protective fabric components market, integrating retroreflective materials with flame-resistant textile technologies to improve worker safety in hazardous environments. The company’s 3M™ Scotchlite™ Reflective Material 8935 Series remains a key product line for 2025–2026, engineered to withstand more than 50 industrial wash cycles while maintaining ANSI/ISEA 107 high-visibility performance standards.

For heavy industrial sectors, 3M optimized its Scotchlite™ 8940 Series specifically for oil, gas, and mining operations, using advanced beaded retroreflection technology that enhances visibility from wide viewing angles in low-light environments near heavy machinery. Through its Technical Solutions Service global laboratories, 3M provides PPE manufacturers with visibility modeling and flame-resistant compatibility testing, ensuring reflective trims maintain the FR integrity of cotton-blend protective garments. Looking ahead to 2026, the company is prioritizing the development of low-carbon-footprint reflective materials aligned with the sustainability requirements of European and North American energy and utility industries.

United States Industrial Protective Clothing Fabrics Market: Portfolio Realignment, PFAS Exit, and High-Risk Application Innovation

The United States industrial protective clothing fabrics market is undergoing structural repositioning driven by corporate portfolio realignment, accelerated PFAS-free adoption, and expanding high-risk end-use applications. In January 2026, DuPont de Nemours Inc. disclosed that it is evaluating the potential sale of its Nomex and Kevlar brands as part of a broader corporate restructuring separating its electronics and water businesses. While these brands remain embedded within DuPont’s Industrial Technology division, the announcement signals a potential reshaping of ownership and long-term capital allocation around aramid-based protective fabrics used across firefighting, defense, utilities, and industrial safety markets.

Material innovation and regulatory alignment continue to define U.S. demand dynamics. In June 2025, Milliken & Company, in collaboration with Fire-Dex, equipped the East Providence Fire Department with the first department-wide non-PFAS turnout gear in the country. The solution utilizes Milliken Assure, a non-PFAS and non-halogenated flame-resistant moisture barrier that complies with NFPA 1971-2018 standards, marking a critical inflection point for PFAS-free firefighter protective fabrics. Milliken’s technical textiles unit is also finalizing flame-resistant undergarment fabric prototypes for NASA Artemis III, scheduled for 2026, combining Polartec knitting structures with Westex FR technologies to withstand high-oxygen lunar environments. Complementing this, SureWerx received recognition at the 2025 DuPont Innovation Awards for its 40 Cal LAN Series arc flash suit, addressing safety requirements in renewables and electrification projects. The competitive landscape further shifted in May 2025 when Honeywell completed the sale of its PPE business to Protective Industrial Products, consolidating high-performance fabric portfolios within mining and construction-focused distribution channels.

Netherlands Industrial Protective Clothing Fabrics Market: Aramid Supply Security and Circular Manufacturing Transition

The Netherlands occupies a strategic position in the global industrial protective fabrics supply chain through aramid fiber production and sustainability-led manufacturing. In August 2025, Teijin Aramid successfully resumed operations at its Delfzijl facility following a major fire incident, restoring global supply continuity for Twaron high-modulus para-aramid fibers used in ballistic protection, industrial PPE, and energy infrastructure. Rapid recovery at this site mitigated downstream supply disruptions for European and North American protective fabric converters.

Sustainability has become a central differentiator. In the same period, Twaron production achieved ISCC PLUS certification, enabling Teijin Aramid to offer bio-based and circular aramid fibers aligned with customer decarbonization targets. Strategic expansion into energy infrastructure is also underway. Teijin Aramid, alongside FibreMax, secured funding from the Just Transition Fund to support floating wind infrastructure in the North Sea, utilizing high-performance fabrics and yarns for reinforcement applications. Leadership continuity was reinforced with the appointment of Taiichi Machida as CEO in August 2025, tasked with executing the Formulating Tomorrow strategy focused on recycling aerospace composites and recovering high-value fibers and resins.

China Industrial Protective Clothing Fabrics Market: Domestic High-Tech Capacity and Environmental Compliance

China’s industrial protective clothing fabrics market is advancing through state-backed capacity expansion and tightening environmental standards. Under the final phase of the Made in China 2025 program, the country has established forty national innovation centers dedicated to high-tech materials, accelerating domestic production of high-tensile aramid and carbon-fiber blends for aviation, firefighting, and new-energy vehicle safety applications. This initiative is materially reducing reliance on imported protective fabrics while improving local performance benchmarks.

Product-level innovation is reinforcing this trajectory. In November 2025, Ibena Shanghai introduced the Rambo Outershell Fabric, integrating Nomex spun yarn with Kevlar filament to deliver approximately 30% higher tensile strength than conventional firefighting fabrics. Regulatory pressure is also shaping manufacturing practices. From June 2026, the Ministry of Industry and Information Technology will enforce GB 30981.1-2025, mandating reduced use of hazardous chemical finishes on industrial textiles and accelerating the shift toward aqueous and eco-friendly coating treatments across protective fabric production lines.

France Industrial Protective Clothing Fabrics Market: Multi-Hazard Design and Eco-Performance Balance

France’s industrial protective fabrics sector is characterized by multi-hazard performance requirements combined with sustainability-driven finishing technologies. In November 2025, Groupe Mulliez-Flory launched the Phenix line of protective clothing using Nomex Comfort fabric with EcoForce finish. The solution is engineered to meet 2026 operational requirements across oil, gas, and electrical sectors while lowering environmental impact through optimized durability and reduced finishing chemistry intensity.

Specialized personal protection is also evolving. French safety specialist S.E.R.B. Regain Perform introduced an advanced sleeve combining anti-laceration, flame resistance, and antistatic properties. Targeted at law enforcement and glass manufacturing environments, the product reflects rising demand for modular protective textiles capable of addressing multiple risk profiles without increasing garment weight or complexity.

India Industrial Protective Clothing Fabrics Market: Incentivized Capacity and Standards Harmonization

India’s industrial protective clothing fabrics market is expanding through policy-driven capacity building and regulatory alignment with global safety norms. During 2025–2026, the government extended the Production-Linked Incentive scheme to include high-tenacity technical textiles, accelerating domestic investment in fire-retardant and chemical-resistant fabric manufacturing, particularly within the Gujarat industrial belt. This policy shift is strengthening local supply chains for industrial PPE used in chemicals, energy, and infrastructure sectors.

Standardization is reinforcing market credibility. In late 2025, the Bureau of Indian Standards issued updated codes for industrial coveralls, aligning domestic manufacturing requirements with ISO 11612 for heat and flame protection. This harmonization is improving export readiness of Indian-made protective fabrics while raising baseline safety performance for domestic industrial users.

Industrial Protective Clothing Fabrics Industry: Country-Level Strategic Snapshot

Industrial Protective Clothing Fabrics Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Key Fabric or Policy Focus

|

Structural Impact

|

|

United States

|

Portfolio realignment and PFAS-free transition

|

Aramid brands, non-PFAS turnout gear, arc flash fabrics

|

Technology-driven repositioning of high-performance PPE

|

|

Netherlands

|

Supply security and circular manufacturing

|

Twaron aramids, ISCC PLUS certification

|

Resilient aramid supply with sustainability premium

|

|

China

|

Domestic high-tech material expansion

|

Aramid-carbon blends, eco-coatings

|

Reduced import reliance and environmental compliance

|

|

France

|

Multi-hazard protection with eco finishes

|

Nomex Comfort, modular protective textiles

|

Balanced performance and sustainability

|

|

India

|

Incentivized capacity and standards alignment

|

FR and chemical-resistant fabrics, ISO harmonization

|

Scaled domestic production with export readiness

|

Industrial Protective Clothing Fabrics Market Report Scope

Industrial Protective Clothing Fabrics Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$12.1 Billion

|

|

Market Size (2034)

|

$24 Billion

|

|

Market Growth Rate

|

7.9%

|

|

Segments

|

By Fiber Type (Aramid and Blends, Polyamide, Polyolefin and Polyethylene, Cotton Fibers, Polybenzimidazole, Carbon Fibers, High-Performance Polyethylene), By Fabric Type (Woven Fabrics, Non-Woven Fabrics, Knitted Fabrics, Coated Fabrics), By Protection Level (Flame Resistant, Chemical and Biological Protection, Ballistic and Mechanical Protection, Arc Flash and Thermal Protection, High-Visibility and Cleanroom Protection), By End-Use Industry (Oil and Gas, Fire Service and Emergency Response, Manufacturing and Metalworking, Construction and Mining, Healthcare and Laboratories, Military and Law Enforcement)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

DuPont de Nemours, Inc., Teijin Aramid B.V., Milliken & Company, TenCate Protective Fabrics, Honeywell International Inc., Protective Industrial Products, 3M Company, PBI Performance Products, Inc., Lenzing AG, W. L. Gore & Associates, Inc., Lakeland Industries, Inc., Carrington Textiles Ltd., Kermel, Yantai Tayho Advanced Materials Co., Ltd., Glen Raven, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Industrial Protective Clothing Fabrics Market Segmentation

By Fiber Type

- Aramid and Blends

- Polyamide

- Polyolefin and Polyethylene

- Cotton Fibers

- Polybenzimidazole

- Carbon Fibers

- High-Performance Polyethylene

By Fabric Type

- Woven Fabrics

- Non-Woven Fabrics

- Knitted Fabrics

- Coated Fabrics

By Protection Level

- Flame Resistant

- Chemical and Biological Protection

- Ballistic and Mechanical Protection

- Arc Flash and Thermal Protection

- High-Visibility and Cleanroom Protection

By End-Use Industry

- Oil and Gas

- Fire Service and Emergency Response

- Manufacturing and Metalworking

- Construction and Mining

- Healthcare and Laboratories

- Military and Law Enforcement

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Industrial Protective Clothing Fabrics Industry

- DuPont de Nemours, Inc.

- Teijin Aramid B.V.

- Milliken & Company

- TenCate Protective Fabrics

- Honeywell International Inc.

- Protective Industrial Products

- 3M Company

- PBI Performance Products, Inc.

- Lenzing AG

- W. L. Gore & Associates, Inc.

- Lakeland Industries, Inc.

- Carrington Textiles Ltd.

- Kermel

- Yantai Tayho Advanced Materials Co., Ltd.

- Glen Raven, Inc.

*- List not Exhaustive