Ink Resins Market to Reach $5 Billion by 2034 at 4% CAGR as UV-Curable, Bio-Attributed, and Digital Packaging Systems Reshape Resin Architecture

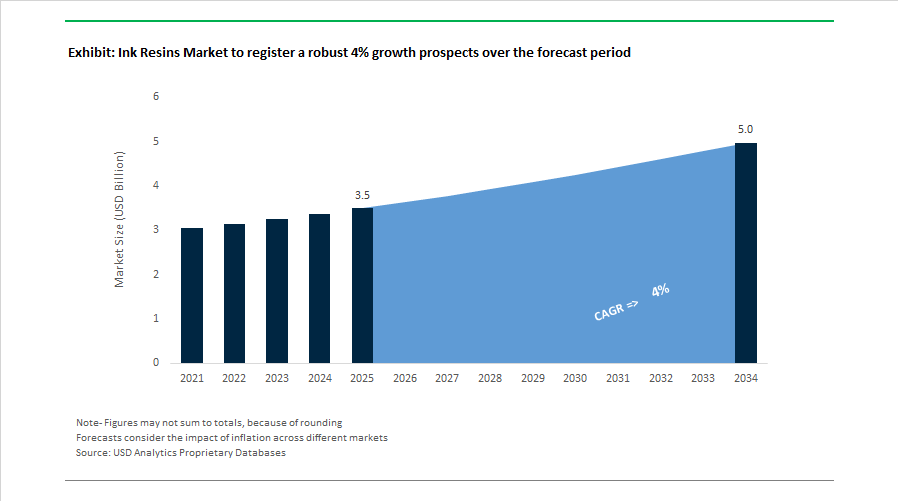

The Ink Resins Market is projected to expand from $3.5 billion in 2025 to $5 billion by 2034, registering a CAGR of 4%, driven by growth in UV-curable inks, food-contact compliant packaging, and sustainable resin chemistries. Between 2024 and 2026, the sector has undergone strategic restructuring and capacity localization, with major producers prioritizing ISCC PLUS certification, waterborne resin systems, and digital inkjet-compatible binders. Resin performance requirements are increasingly defined by adhesion to complex substrates, low-viscosity formulation for high-speed printing, and compatibility with circular economy mandates such as deinkability and CMR-free compliance.

In March 2024, Ideal Chemi Plast, a subsidiary of DIC Corporation, commenced operations at a new coating resins production facility in Maharashtra, India, alongside a dedicated Application Lab to tailor resin chemistries for the South Asian packaging and industrial coatings markets. In May 2024, DuPont introduced its Artistri PN1000 low-viscosity pigment ink series at Drupa 2024, leveraging proprietary resin technology to deliver higher optical density and food-contact compliance for high-speed commercial and digital packaging printing. Early 2024 also marked the beginning of Evonik’s 50% expansion of its precipitated silica plant in Charleston, South Carolina, with completion scheduled for early 2026. The silica produced serves as a critical rheology modifier and matting agent within advanced ink resin systems across North America.

The market’s digital transformation accelerated in 2025. In June 2025, Siegwerk launched the SICURA Litho Pack UV offset series across EMEA, built on a new CMR-free and fully deinkable resin system aligned with brand-owner sustainability standards. In July 2025, INX International introduced INXJet MDLM, a UV-curable inkjet resin platform for high-speed beverage can decoration, emphasizing adhesion durability and regulatory compliance for food-contact packaging. In 2025, Evonik launched its POLYVEST® ST-E 60 polybutadiene facility in Shanghai, strengthening binder technologies that enhance water resistance and electrical insulation properties in industrial coatings and inks. In November 2025 at CHINACOAT, Sun Chemical partnered with its parent DIC Corporation to showcase next-generation sustainable resin technologies for automotive and industrial coatings, reinforcing a green transformation narrative across the ink value chain.

Strategic portfolio optimization and certification milestones further reshaped competitive positioning in 2026. In December 2025, Arkema announced the proposed divestment of its impact modifiers and processing aids business to Praana, expected to close in Q1 2026, allowing Arkema to concentrate its Coating Solutions segment on higher-value specialty and sustainable resin materials. In January 2026, Arkema confirmed that more than 70% of its coating sites had achieved ISCC PLUS certification, enabling bio-attributed resin solutions with at least 20% lower carbon footprint. In February 2026, BASF added a new dispersions and resins production line at its Mangalore, India site to serve the fast-growing packaging and construction markets with localized supply. In parallel, Evonik announced further global expansion of hydroxyl-terminated polybutadiene (HTPB) capacity following its 2024 Marl expansion, including a new production line in Germany and engineering work for a major Asian facility, underscoring rising demand for high-performance resin binders in automotive and industrial ink systems.

Ink Resins Market Trends and Opportunities

Accelerated Transition to High-Performance Waterborne PUDs in Flexible Packaging

The Ink Resins Market is undergoing a decisive structural shift as flexible packaging converters respond to the strict enforcement of Regulation (EU) 2025/40 under the Packaging and Packaging Waste Regulation framework, which entered into force in February 2025. This regulation is actively phasing out solvent-based polyurethane inks, particularly in food and hygiene packaging, and accelerating the adoption of waterborne polyurethane dispersions (PUDs) that can meet both environmental and productivity benchmarks.

A critical commercial breakthrough occurred in 2025 when resin producers such as Sun Chemical advanced their BLUEPUR and HYDRAN GP waterborne PUD platforms to solids contents exceeding 50%. This innovation has materially changed converter economics. Higher solids enable thicker ink films per pass, significantly reducing drying energy and allowing water-based flexographic and gravure presses to operate at speeds approaching 600 meters per minute. As a result, the long-standing throughput disadvantage versus solvent systems has largely been eliminated in reverse printing and lamination applications.

Regulatory pressure is reinforcing this momentum. Updates to REACH Annex XVII have driven the complete removal of N-Methyl-2-pyrrolidone and amine neutralizers from modern PUD formulations. Beyond compliance, this transition has delivered tangible commercial value by lowering residual odor and improving food-pack suitability, particularly for snack pouches and personal care packaging where sensory performance is closely audited by brand owners.

Equally significant is progress in adhesion performance. New self-crosslinking PUD chemistries introduced in 2024 and scaled through 2025 have demonstrated strong adhesion to untreated polyolefin films such as OPP and PE. Industry case studies show that converters can now achieve target bond strengths without intensive corona or plasma pretreatment, translating into estimated operational energy savings of 15 to 20% per production line. This combination of regulatory compliance, productivity parity, and cost efficiency is structurally embedding waterborne PUDs as the default resin backbone for next-generation flexible packaging inks.

Strategic Scaling of Bio-Based and Natural-Carbon Resin Backbones

Parallel to water-based adoption, the Ink Resins Market is experiencing a strategic pivot toward bio-based and natural-carbon polymer backbones as brand owners hardwire Scope 3 decarbonization targets into procurement contracts. Rather than incremental green labeling, the focus has shifted to resins synthesized from plant-derived monomers such as itaconic acid and succinic acid, with verified C14 natural carbon content.

Between 2024 and 2025, Covestro significantly expanded its portfolio of partly bio-based UV-curable resins under the NeoRad and AgiSyn platforms. Certain commercial grades now reach up to 83% bio-based content by mass, utilizing soybean oil and other renewable biomass feedstocks. Ink formulators using these systems have reported carbon footprint reductions of 25 to 30% in digital printing applications compared to conventional fossil-derived resins, without sacrificing gloss, cure speed, or abrasion resistance.

Capacity scaling is moving rapidly upstream. In March 2025, BASF and other major chemical producers disclosed substantial capital allocations toward pilot facilities for bio-based aniline intermediates and specialized polyols. These investments are strategically aimed at transitioning sustainable ink resins from niche, high-cost offerings to industrial-scale materials by 2027, signaling long-term confidence in demand durability.

Procurement behavior is amplifying this trend. By 2025, FMCG brand owners had begun enforcing sustainable ink mandates that require a minimum of 20% renewable content in all secondary packaging inks. Third-party certifications such as NAPIM BioRenewable Content verification and UL ECOLOGO have become de facto gating criteria, transforming bio-based resin capability into a competitive necessity rather than a differentiation lever.

Specialized Resins for High-Refractive Index Security Inks

Rising global counterfeiting has created a premium opportunity segment within the Ink Resins Market, particularly for high-refractive index security inks used in banknotes, government documents, and luxury packaging. The anti-counterfeiting packaging segment alone was valued at over USD 400 billion in 2024, with increasing emphasis on machine-verifiable authentication.

Security ink applications demand resins with exceptional optical clarity to support optically variable inks, iridescent flakes, and holographic elements, while also forming a mechanically robust shell capable of withstanding circulation lifetimes of four to five years. Resin performance directly determines whether these features retain visual fidelity under abrasion, folding, and chemical exposure.

An emerging opportunity lies in resins engineered to host multiple functional additives within a single stable matrix. These multi-layer authentication systems integrate UV-fluorescent and infrared-responsive markers, enabling overt consumer recognition alongside covert forensic verification. Late-2025 deployments by luxury brands using invisible cryptographic ink signatures reduced counterfeit penetration by 20 to 30% within 18 months, underscoring the commercial value of resin systems that do not interfere with machine-readable encryption.

Ultra-Low Migration Resins for Direct-to-Food Digital Printing

The rapid growth of late-stage customization and digital inkjet printing for primary food packaging has created a structurally attractive opportunity for ultra-low migration ink resins. Compliance with the Swiss Ordinance, EuPIA guidelines, and evolving national food-contact regulations has shifted resin selection from performance-first to contamination-first decision making.

Ink manufacturers are responding with NC-free and BPA-free resin systems specifically engineered for food packaging. Companies such as Siegwerk and INX International have launched low-migration UV and LED-curable resin platforms, including the INXhrc RC LM series, designed for the non-food contact side of primary packaging while maintaining compliance margins under worst-case migration testing.

A particularly strong growth vector is electron beam curable resins. By eliminating photoinitiators entirely, EB systems offer instant cure with no residual low-molecular-weight species capable of migrating into food. This positions EB-curable ink resins as a long-term solution for high-speed digital printing in regulated food applications.

Recyclability is reinforcing adoption. In September 2025, a collaboration between Borouge, Siegwerk, and TPN Food Packaging successfully demonstrated a fully recyclable mono-material pouch. The project relied on a specialized ink resin that remained chemically stable throughout 100% PE recycling, proving that ultra-low migration performance and circularity objectives can be achieved simultaneously. This convergence of food safety, digital flexibility, and recyclability defines one of the most strategically important opportunity spaces in the Ink Resins Market through 2030.

Ink Resin Market Share and Segmentation Insights

Acrylic Resins Lead Ink Resin Demand Through Versatile Performance in Water-Based and Solvent Ink Systems

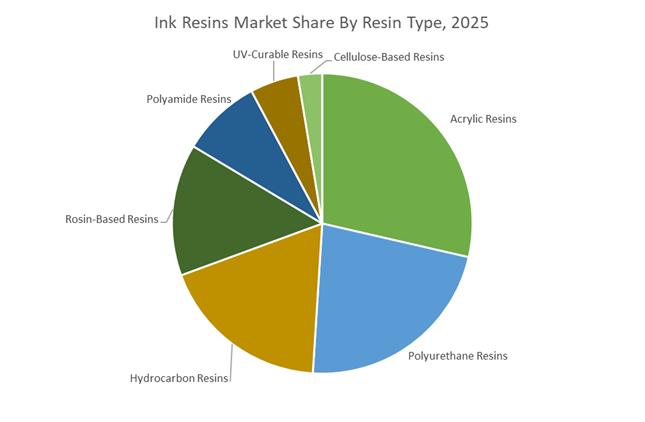

Acrylic resins accounted for 28.60% of the Ink Resins Market share in 2025, establishing them as the leading resin chemistry in modern printing ink formulations. Acrylic polymers are widely used in water-based inks, solvent-based inks, and hybrid ink systems because they deliver strong pigment wetting, reliable film formation, and excellent adhesion across multiple substrates including plastic films, paperboard, aluminum foils, and coated papers. These performance characteristics make acrylic resins highly suitable for flexographic printing, gravure printing, and commercial printing applications where color consistency, gloss control, and print durability are essential. Acrylic technology has become increasingly important as the printing industry shifts toward low-VOC and environmentally compliant ink formulations, particularly in packaging and publication printing. In 2025, resin producers have significantly advanced water-based acrylic resin technology, improving drying speed, block resistance, and resolubility in press systems. These improvements address traditional limitations of water-based inks while maintaining regulatory compliance with global environmental standards governing printing ink emissions and packaging sustainability.

Flexible Packaging Sector Drives the Largest Consumption of Ink Resins in Printing Applications

Flexible packaging represented 42.80% of the Ink Resins Market share in 2025, making it the dominant end-use application for printing ink resin technologies. Flexible packaging formats such as stand-up pouches, multilayer films, snack wrappers, sachets, and laminated packaging materials require specialized inks capable of adhering to non-porous substrates including polyethylene, polypropylene, polyester, and aluminum foil. Ink resins play a central role in delivering adhesion, film integrity, gloss development, abrasion resistance, and chemical stability, ensuring that printed graphics remain durable throughout packaging production, filling, distribution, and retail display. The continued shift from rigid containers toward lightweight flexible packaging in food, beverage, personal care, and pharmaceutical industries has significantly increased demand for advanced ink resin systems compatible with high-speed flexographic and gravure printing processes. In 2025, sustainability initiatives across global packaging supply chains have also accelerated innovation in recyclable and de-inkable ink resin formulations, with manufacturers developing simplified resin chemistries that support polyolefin recycling streams and compostable packaging materials while maintaining print quality and production efficiency.

Competitive Landscape in Ink Resins Market

BASF SE Expands Low-Carbon Dispersion and UV Resin Capabilities

BASF SE maintains leadership in dispersion and ink resin technology through its integrated Verbund production model, enabling cost optimization and feedstock efficiency. In November 2025, BASF commissioned a new high-performance dispersant and resin production line in Nanjing, China, utilizing Controlled Free Radical Polymerization technology to lower Product Carbon Footprint in acrylic and specialty resin systems. Under its 2026 Winning Ways strategy, the company is prioritizing high-margin packaging resin solutions in Asia and North America to offset structural demand weakness in Europe. Its Jonon and Laromer brands include advanced water-based and energy-curable UV and EB resins tailored for food packaging, flexible substrates, and high-end industrial coatings. With a projected 2026 adjusted EBITDA of €6.2 billion to €7.0 billion, BASF continues to strengthen its Dispersions and Resins division through sustainability-aligned polymer innovation.

DIC Corporation Strengthens Digital and Functional Resin Innovation

DIC Corporation, primarily through Sun Chemical, is a global leader in printing ink production and vertically integrated resin supply. In February 2026, the company advanced its DIC Vision 2030 Phase 2 strategy, accelerating functional resin development for sustainable packaging, healthcare applications, and smart living technologies. On February 17, 2026, DIC expanded its coating and ink resin operations in India, reinforcing the region as a growth engine within its Asia-Pacific portfolio. The TrinDy resin line includes specialized dental and industrial DLP resins engineered for high-resolution additive manufacturing and precision 3D printing. Through its Digital Leap in R&D initiative, DIC is investing in AI robotics and physical AI platforms in partnership with Emerald to accelerate molecular discovery and formulation optimization, strengthening competitiveness in high-performance acrylic and polyurethane ink binder systems.

Evonik Industries AG Integrates Hyperdispersants with Radiation-Curing Resins

Evonik Industries AG differentiates its ink resin portfolio through integrated system solutions that combine specialty additives with resin chemistry. In January 2026, the company introduced TEGO Dispers 695, a hyperdispersant and resin compatibilizer optimized for radiation-curing and solvent-borne polyurethane ink systems. Its February 2026 North American distribution streamlining appointed regional technical specialists to enhance localized service for ink and coating formulators. Evonik targets more than 50% of sales from Next Generation Solutions by 2030, with 2026 marking expansion into bio-attributed acrylic and polyurethane resins designed for low-migration food packaging applications. With €15.2 billion in 2024 sales and a strategic focus on Specialty Additives, Nutrition and Care, and Smart Materials divisions, Evonik reinforces its role in advanced resin engineering for high-speed packaging and digital printing markets.

Arkema S.A. Advances Bio-Based Thermoplastic and Low-VOC Resin Systems

Arkema S.A. has repositioned as a pure-play specialty materials company, emphasizing bio-based polyamide and recyclable thermoplastic resin technologies for industrial coatings and specialty ink binders. At JEC World 2026, the company showcased its 100% bio-based and recyclable Elium resins, enabling industrial-scale recycling of thermoplastic composites and advanced ink systems. Arkema reported 2025 EBITDA of €1,251 million and anticipates slight EBITDA growth in 2026, supported by capacity expansions in Asia and the United States. Its portfolio focuses on ultra-low VOC waterborne, UV-LED, and powder resin technologies aligned with tightening REACH and UK REACH regulatory standards. The recent expansion of bio-based Rilsan Polyamide 11 capacity strengthens its supply of high-durability binders for mobility, transportation, and specialty packaging inks.

Lubrizol Corporation Prioritizes PFAS-Free and Surface-Engineered Resins

Lubrizol Corporation leverages its expertise in surface science to supply high-performance binders for digital, textile, and flexible packaging printing markets. The Aptalon polyamide polyurethane and Carboset acrylic resin families are engineered for chemical resistance, durability, and premium soft-touch aesthetics in packaging substrates. In 2026, Lubrizol intensified its transition toward PFAS-free surface modifiers and fluorine-free resin systems to comply with tightening global regulations between 2026 and 2028, utilizing advanced hyperdispersants to maintain slip and surface performance. The company presented its One Lubrizol brand identity and polymer innovations at the American Coatings Show 2026, reinforcing its leadership in next-generation resin technologies. Expansion of technical service and procurement teams in Bangkok enhances responsiveness to Southeast Asia’s growing digital print and specialty packaging markets.

Flint Group Integrates Bio-Renewable Resins into Sustainable Ink Systems

Flint Group strengthens its competitive position in the ink resins market through vertical integration and sustainability-driven product development. The PRISM 2030 Sustainability Vision targets a 46% reduction in Scope 1, 2, and 3 emissions by 2030, supported by increased utilization of bio-renewable resin feedstocks. In February 2026, the company introduced flake-free white ink foundations for shrink sleeve applications, utilizing specialized resins engineered to prevent cracking under complex container heating geometries. Its AQUACode water-based and TerraCode bio-renewable ink lines incorporate plant-derived resin technologies sourced from non-food-competing feedstocks. In late 2025, Flint confirmed that its ZenCode solvent-based inks achieved Cradle to Cradle Material Health Certification, marking a milestone for high-performance polyurethane-based resin systems within sustainable packaging applications.

United States Ink Resins Market: Mass-Balance Scale-Up, PFAS Substitution, and UV-Curable Expansion

The United States ink resins industry is advancing through carbon-intensity reduction, portfolio consolidation, and accelerated innovation for sustainable packaging and advanced manufacturing. In November 2025, BASF confirmed that its Cincinnati, Ohio facility is progressing toward commissioning a new production line for bio-based intermediates by late 2026. The line applies a mass-balance approach to deliver high-performance ink resins with a materially lower product carbon footprint, directly supporting brand-owner decarbonization targets in flexible and paper-based packaging. Parallel to this, regulatory guidance updated for 2026 has materially shifted U.S. R&D pipelines toward water-based acrylic and maleic resins, which now account for more than half of active development programs as converters reduce reliance on solvent-borne systems.

Portfolio optimization and specialty capacity additions are reinforcing competitiveness. Evonik Industries announced the consolidation of U.S. silica and resin-related production with scheduled closures of the Watervliet, New York and Aberfeldy, Maryland sites, redirecting output to larger hubs to improve economies of scale for matting agents and specialty resins. Barrier innovation is also accelerating as Mitsubishi Chemical Group unveiled PFAS-free SoarnoL gas barrier resin solutions in December 2025 for paper packaging inks and coatings. In advanced applications, ALTANA expanded Cubic Ink UV-curing resin capacity in early 2025 from its New Jersey site to serve industrial 3D printing and medical technology, while Sun Chemical committed $100 million in 2025 to a new U.S. facility dedicated to compostable and recyclable ink resins.

China Ink Resins Market: Policy-Led Upgrading, Circular Polymers, and Smart Parks

China’s ink resins sector is being reshaped by industrial policy, emissions standards, and scale investments in advanced polymerization. In September 2025, the Ministry of Industry and Information Technology issued a petrochemical work plan mandating the upgrading of traditional products into high-end electronic chemicals and advanced ink resins, targeting sustained value growth through 2026. Compliance pressure is intensifying. From June 2026, GB 30981.1-2025 will enforce stringent VOC limits, accelerating the phase-out of toluene-based resins in favor of high-solid and water-borne alternatives across printing and coatings.

Capacity and technology investments are aligning with these mandates. BASF commissioned a Controlled Free Radical Polymerization line in Nanjing in November 2025 to produce high-performance dispersants and resins for industrial and automotive applications. Earlier in 2025, BASF also launched its first commercial loopamid polyamide 6 facility in Shanghai with 500 metric tons annual capacity, supplying recycled resins to textile inks and fibers with reported CO2 reductions of up to 70%. At the cluster level, the Jiangbei New Material Technology Park has been designated a 2026 innovation hub, deploying Smart Park infrastructure for real-time monitoring of resin synthesis and emissions to improve compliance and energy efficiency.

Germany Ink Resins Market: Platinum Sustainability, Bio-Based Acrylics, and Circular Composites

Germany’s ink resins industry is positioned at the intersection of certified sustainability and premium performance. In late 2025, ALTANA achieved EcoVadis Platinum status, placing its resin and additive operations among the top one percent globally and underscoring the commercial relevance of sustainability credentials. The company reported that a significant share of 2025 sales derived from products launched within the last five years, highlighting rapid innovation cycles in specialty resins.

Bio-based and circular materials are expanding in parallel. Arkema launched the ENCOR range of bio-based waterborne acrylic dispersions in January 2025 with up to 30% bio-based content, targeting substantial carbon footprint reduction for textile and industrial printing. Energy efficiency milestones further strengthen the ecosystem as German firms including BYK and Evonik Industries reported more than 70% reductions in Scope 1 and 2 emissions versus 2014 baselines. At K 2025, German manufacturers also showcased Elium thermoplastic resins under the Zebra projects, emphasizing full recyclability for composite and ink-adjacent applications.

India Ink Resins Market: Policy Roadmap, Packaging Demand, and Regional Export Support

India’s ink resins industry is transitioning from bulk polymers to higher-value downstream derivatives under a clear policy framework. The 2025 NITI Aayog roadmap targets a larger share of the global chemicals value chain by 2030, explicitly encouraging movement into specialty ink resins and functional coatings. This policy direction is catalyzing investments in formulation, testing, and customer application support.

Operational expansion is translating policy into capacity. Siegwerk finalized the expansion of blending and resin-testing operations in Gujarat in late 2025 to serve India’s fast-growing flexible packaging sector and export demand from Southeast Asia. Downstream infrastructure is also stimulating resin demand. SIG commissioned its first aseptic carton plant in India in December 2025, increasing requirements for high-adhesion ink resins compatible with multi-layer barrier coatings used in food and beverage packaging.

Ink Resins Industry: Country-Level Strategic Snapshot

Ink Resins Market County Level Snapshot

|

Region

|

Primary Strategic Driver

|

Core Resin Focus

|

Structural Direction

|

|

United States

|

Mass balance decarbonization and PFAS substitution

|

Bio-based acrylics, UV-curables, barrier resins

|

Low-PCF, water-based systems with specialty scale

|

|

China

|

Policy-led upgrading and VOC enforcement

|

High-solid, water-borne, recycled PA6

|

Value-added growth with smart manufacturing

|

|

Germany

|

Certified sustainability and circularity

|

Bio-based acrylics, recyclable thermoplastics

|

Premium, low-carbon specialty resins

|

|

India

|

Policy roadmap and packaging infrastructure

|

High-adhesion and flexible packaging resins

|

Export-ready specialty formulations

|

Ink Resins Market Report Scope

Ink Resins Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.5 Billion

|

|

Market Size (2034)

|

$5 Billion

|

|

Market Growth Rate

|

4%

|

|

Segments

|

By Resin Type (Rosin-Based Resins, Hydrocarbon Resins, Cellulose-Based Resins, Acrylic Resins, Polyamide Resins, Polyurethane Resins, UV-Curable Resins), By Technology (Oil-Based, Solvent-Based, Water-Based, UV-Curable), By Printing Process (Lithographic, Gravure, Flexographic, Digital Inkjet, Screen Printing), By End-Use Application (Flexible Packaging, Corrugated Packaging, Publishing and Printing, Textiles, Industrial Labeling and Security Printing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Dow Inc., Evonik Industries AG, Arkema S.A., DIC Corporation, ALTANA AG, Lawter Inc., Covestro AG, Kraton Corporation, Arakawa Chemical Industries, Ltd., Harima Chemicals Group, Inc., Mitsubishi Chemical Group, Indulor Chemie GmbH, IGM Resins, Wacker Chemie AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Ink Resins Market Segmentation

By Resin Type

- Rosin-Based Resins

- Hydrocarbon Resins

- Cellulose-Based Resins

- Acrylic Resins

- Polyamide Resins

- Polyurethane Resins

- UV-Curable Resins

By Technology

- Oil-Based

- Solvent-Based

- Water-Based

- UV-Curable

By Printing Process

- Lithographic

- Gravure

- Flexographic

- Digital Inkjet

- Screen Printing

By End-Use Application

- Flexible Packaging

- Corrugated Packaging

- Publishing and Printing

- Textiles

- Industrial Labeling and Security Printing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Ink Resins Industry

- BASF SE

- Dow Inc.

- Evonik Industries AG

- Arkema S.A.

- DIC Corporation

- ALTANA AG

- Lawter Inc.

- Covestro AG

- Kraton Corporation

- Arakawa Chemical Industries, Ltd.

- Harima Chemicals Group, Inc.

- Mitsubishi Chemical Group

- Indulor Chemie GmbH

- IGM Resins

- Wacker Chemie AG

*- List not Exhaustive