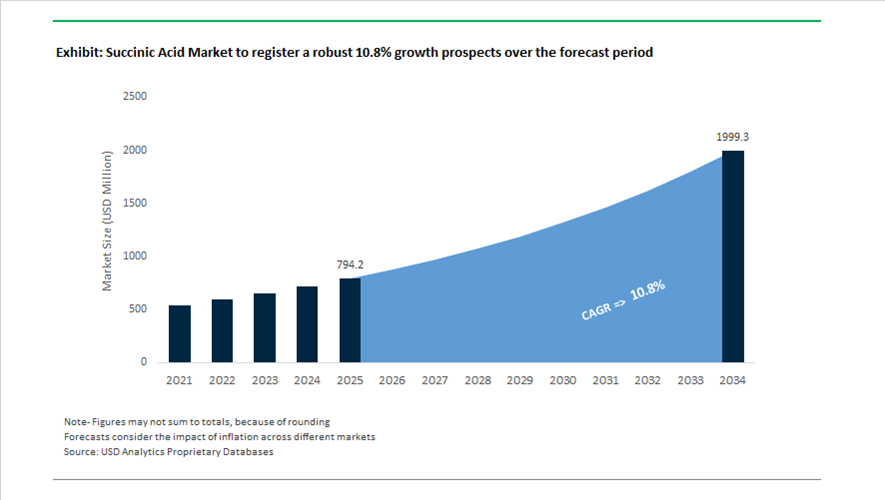

Succinic Acid Market Valuation 2025–2034: $794.2 Million to $1,998.9 Million at 10.8% CAGR Powered by Bio-Based PBS, BDO Integration, and Sustainable Chemistry Platforms

The global succinic acid market is valued at $794.2 million in 2025 and is projected to reach $1,998.9 million by 2034, expanding at a rapid CAGR of 10.8%. Growth is being driven by accelerating adoption of bio-based succinic acid in polybutylene succinate (PBS) bioplastics, 1,4-butanediol (BDO) intermediates, low-VOC coatings, pharmaceutical excipients, and personal care formulations. As regulatory mandates tighten around carbon emissions, compostable packaging, and renewable feedstocks, bio-succinic acid is emerging as a critical platform chemical for circular polymer production and sustainable solvents. Market momentum is reinforced by fermentation-based manufacturing technologies, integrated BDO value chains, and licensing models that enable turnkey bio-refinery deployment across North America, Europe, and Asia-Pacific.

Strategic alliances and fermentation scale-up defined 2024. In March 2024, BYOMA launched a succinic-acid-infused body care line, signaling the compound’s transition from industrial intermediate to high-visibility cosmetic active. In early 2024, CJ CheilJedang and BioAmber finalized plans to establish a joint venture in China to serve Asia-Pacific demand for bio-succinic acid in bioplastics and specialty polymers. In September 2024, Lygos and CJ BIO formed a long-term partnership to develop a commercial-scale biorefinery integrating high-yield microbial fermentation with global manufacturing infrastructure. In late 2024, Proviron and Reverdia introduced Provichem 2511 Eco, a bio-based dimethyl succinate marketed as a sustainable coalescing agent for low-VOC emulsion paints, replacing fossil-derived solvents. Throughout 2024 and early 2025, Roquette optimized BIOSUCCINIUM® production to exceed 99.5% purity and secured IFSCC certification in 2025, strengthening its position in pharmaceutical and cosmetic applications.

Regulatory catalysts and polymer integration accelerated demand in 2025. In February 2025, the European Union’s Packaging and Packaging Waste Regulation (PPWR) came into force, enforcing stricter recyclability and bio-content mandates. This regulatory shift significantly boosted adoption of PBS resins derived from bio-succinic acid as compostable alternatives to conventional petrochemical packaging materials. In April 2025, Roquette completed its acquisition of IFF Pharma Solutions, leveraging its bio-succinic acid platform to expand plant-based excipient offerings for drug delivery systems. In 2025, Technip Energies advanced licensing packages for integrated bio-succinic acid and BDO facilities, promoting circular chemical production models designed to reduce Scope 3 emissions in polymer value chains. LCY Chemical’s CDP “A” rating recognition in 2024 further strengthened sustainable procurement frameworks, enabling expanded incorporation of bio-succinic acid in polymer solutions showcased at K 2025.

Capacity expansion and downstream integration intensified entering 2026. In February 2026, BASF increased production capacity across its Ludwigshafen BDO value chain, utilizing advanced succinic acid intermediates to secure engineering plastics supply for automotive and textile sectors. In the same month, BASF introduced AdBlue® GE manufactured using 100% renewable electricity, reflecting broader decarbonization of nitrogen and bio-based chemical intermediates. These biorefinery partnerships, regulatory-driven PBS adoption, pharmaceutical-grade purity upgrades, BDO integration strategies, and circular technology licensing initiatives are positioning the succinic acid market for sustained double-digit expansion through 2034.

Structural Trends and Monetizable Opportunities in the Succinic Acid Market

Industrial Scale-Up of Bio-Based Succinic Acid for Circular Polymer Value Chains

The Succinic Acid Market is undergoing a decisive structural shift from petro-derived intermediates toward Bio-Based Succinic Acid, driven by accelerating demand for circular and biodegradable polymers such as Polybutylene Succinate and bio-based Thermoplastic Polyurethanes. Packaging, textile, and specialty polymer producers are no longer evaluating bio-succinic acid at pilot scale. Instead, they are locking in long-term offtake agreements supported by multi-thousand-ton commercial fermentation assets that provide cost stability and lifecycle carbon reduction.

By late 2024, industrial validation of high-yield fermentation pathways had been achieved through joint initiatives between BASF and Corbion, leveraging proprietary microorganisms such as Basfia succiniciproducens to improve conversion efficiency and downstream purification economics. Commercial facilities in Southern Europe are now targeting capacities between 25,000 and 50,000 tons per annum, a scale threshold considered critical to displacing fossil-based succinic acid in PBS, TPU, and polyester polyols. Feedstock strategy is simultaneously evolving. While corn-derived carbohydrates retained a 38.4% share in 2025 due to process familiarity and yield reliability, rapid expansion of sugarcane and cassava feedstocks across Asia-Pacific bio-hubs reflects a strategic move to mitigate food security concerns and stabilize input costs through agricultural diversification.

Mandated Transition Toward Succinate-Based De-Icing and Anti-Icing Fluids

Environmental compliance has emerged as a non-negotiable demand driver for succinic acid salts in aviation de-icing applications. Regulatory frameworks administered by the United States Environmental Protection Agency and European Chemicals Agency have tightened limits on Chemical Oxygen Demand and Biochemical Oxygen Demand in airport runoff, accelerating the substitution of traditional glycols. Potassium succinate is increasingly specified in next-generation de-icing fluids due to its rapid biodegradation profile and low aquatic toxicity.

Comparative performance data show that succinate-based formulations can achieve mineralization rates approaching 97% within 24 hours under aerobic conditions, significantly outperforming urea and glycol alternatives. Beyond environmental metrics, safety and asset protection considerations are reinforcing adoption. Industry disclosures from specialty de-icing suppliers highlight that succinate salts reduce catalytic oxidation risks associated with carbon-composite aircraft brake systems. This advantage is particularly relevant for modern wide-body fleets such as those operated on Boeing 787 and Airbus A350 platforms, where brake integrity and corrosion control are tightly linked to lifecycle operating costs.

Bio-Based Succinate Solvents for Low-Toxicity Battery Manufacturing

One of the most compelling growth opportunities in the Succinic Acid Market lies in battery manufacturing solvents as regulators intensify scrutiny on toxic chemistries such as N-methyl-2-pyrrolidone. Under REACH and TSCA frameworks, battery producers are under mounting pressure to identify safer, recyclable solvent systems without sacrificing electrochemical performance. Succinic acid derivatives, particularly dimethyl succinate, are gaining traction as co-solvents in electrode slurry processing.

In 2025, battery manufacturers began evaluating succinate-based solvents for their ability to sustain ionic conductivities around 2.5 mS per centimeter while reducing dependence on dry-room infrastructure and hazardous solvent recovery units. Public research emerging from Japanese and European institutions indicates that these solvents can simplify recycling loops and reduce overall manufacturing complexity. Thermal safety advantages further strengthen the value proposition. Accelerated calorimetry testing conducted in mid-2025 confirmed that succinate-based electrolytes exhibit wider operating temperature windows and lower flammability compared with conventional carbonate systems, positioning bio-succinic derivatives as a premium input for next-generation lithium-ion and sodium-ion batteries.

Flavor Modulation and pH Control in Clean-Label Plant-Based Foods

The plant-based protein segment is creating a structurally durable opportunity for food-grade succinic acid as brands pursue clean-label formulations with improved sensory performance. Succinic acid functions simultaneously as a mild acidulant, shelf-life extender, and umami-enhancing compound capable of masking the bitter off-notes associated with pea and soy proteins. This multifunctionality reduces formulation complexity and aligns with ingredient transparency demands.

Commercial validation of bio-succinic acid in antimicrobial applications has already been demonstrated in animal nutrition trials, including nursery pig studies conducted by BioAmber, where lower inclusion rates delivered measurable microbial control. By late 2025, this efficacy was being translated into human food systems, with major flavor houses actively promoting natural succinic acid as a fermentation-derived ingredient that supports gut-health positioning and product stability in vegan meat analogs. Supply-side readiness is also improving. Companies such as ADM and Advanced Biotech are now offering non-GMO, fermentation-based succinic acid with full traceability. This enables premium plant-based brands to sustain natural flavor claims and non-synthetic positioning, which are increasingly critical across functional food, natural cosmetics, and clean-label nutrition markets.

Succinic Acid Market Share and Segmentation Insights

Bio-Based Succinic Acid Leads the Market as Renewable Platform Chemical Adoption Accelerates

Bio-based succinic acid accounted for 68.40% of the succinic acid market in 2025, reflecting its strong adoption as a sustainable alternative to petroleum-derived chemical intermediates. Produced primarily through fermentation processes using renewable feedstocks, bio-based succinic acid offers a lower carbon footprint and supports renewable content claims in downstream materials. Its versatility enables use in bioplastics, solvents, resins, plasticizers, and specialty chemicals, positioning it as a key renewable platform molecule in the bio-based chemicals industry. The 2025 market driver is the growing recognition of succinic acid as a renewable building block for sustainable materials, prompting investments in large-scale bio-succinic acid production capacity as manufacturers shift toward low-carbon chemical value chains.

Polymers and Bioplastics Drive Global Succinic Acid Consumption

Polymers and bioplastics accounted for 38.60% of succinic acid market demand in 2025, making this the largest application segment as demand for biodegradable polymers accelerates. Bio-based succinic acid serves as a critical monomer in the production of polybutylene succinate (PBS) and related biodegradable polyesters used in packaging films, compostable bags, and agricultural materials. These materials provide functional performance comparable to conventional plastics while supporting circular economy initiatives. The 2025 growth catalyst is the rapid expansion of biodegradable packaging materials, where regulatory pressure on single-use plastics and consumer demand for sustainable products are driving investments in PBS production and increasing demand for bio-based succinic acid.

Succinic Acid Market Competitive Landscape

The succinic acid market in 2026 is shaped by feedstock flexibility, bio-based fermentation, and integration into PBS and bio-BDO value chains. Competition centers on low-carbon production, circular feedstocks, and high-purity applications across biodegradable packaging, coatings, and specialty polymers.

Roquette Strengthens Bio-Based Succinic Acid Leadership Through Integrated Pharma and Food Applications

Roquette is reinforcing its position in the bio-based succinic acid market through its Health & Bioindustry platform and diversified plant-based feedstocks. The company reported a 12.6% EBITDA margin in 2025, with specialty products driving resilience amid global overcapacity. Its “Shift & Lead” strategy launched in 2026 prioritizes high-value bio-based chemicals and sustainable excipients. Roquette supplies high-purity succinic acid for pharmaceutical formulations and food acidulants, supported by integration with IFF Pharma Solutions. Its vertically integrated starch processing ensures consistent fermentation feedstock availability. The company’s strong positioning in oral dosage systems enhances its footprint in regulated life sciences markets.

BASF Expands PBS and Bio-Based Succinic Acid Production via Zhanjiang Verbund Integration

BASF is leveraging its Verbund model to scale bio-based succinic acid as a key intermediate for Polybutylene Succinate (PBS) and specialty resins. The company expects earnings growth in 2026 driven by rising demand for sustainable intermediates. Its Zhanjiang Verbund site in China is central to expanding PBS production capacity aligned with regional plastic ban regulations. BASF is reducing product carbon footprint through renewable energy integration and targeting CO2 emissions between 17.2 and 18.2 million metric tons. Succinic acid is integrated into polyester polyols and alkyd resins for coatings and construction applications. Its backward integration into raw materials ensures cost efficiency and supply stability.

Mitsubishi Chemical Advances High-Purity Bio-Succinic Platforms for Electronics and Automotive Applications

Mitsubishi Chemical Group is aligning its bio-succinic acid strategy with advanced specialty materials and mobility applications. Its DURABIO™ plant-based polymer, incorporating bio-derived intermediates, has been adopted in automotive interior components such as AI-enabled systems. The company is implementing structural reorganization in 2026 to streamline its functional materials portfolio and enhance supply chain agility. Its collaboration with MUFG Bank and Refinverse supports circular plastic recycling linked to succinic-based polymers. Mitsubishi focuses on ultra-high purity grades for electronics, minimizing trace metal contamination. Its innovation capabilities position it strongly in ICT and EV-related material ecosystems.

PTT Global Chemical Scales Bio-Succinic Acid for PBS and Compostable Polymer Applications

PTT Global Chemical is a key producer of bio-succinic acid, targeting large-scale PBS and PBST applications in biodegradable packaging. Its materials are widely used in agricultural films and compostable food service products. In 2026, the company is regionalizing supply chains to mitigate tariff pressures and optimize global distribution. GC Innovation America is advancing microbial engineering to reduce downstream purification costs, targeting production costs of $1.15–$1.30 per kg. Strong policy support from Thailand’s Eastern Economic Corridor enhances scalability of renewable chemicals. Its integrated production network connects Asian feedstocks with North American demand centers.

Kawasaki Kasei Focuses on High-Stability Petro-Based Succinic Acid for Industrial and Electronics Markets

Kawasaki Kasei maintains a strong position in petro-based succinic acid, focusing on high-purity and high-stability industrial applications. The company optimized its butane oxidation processes in 2025 to improve yields and reduce byproduct formation, enhancing overall product quality. Its portfolio includes succinic anhydride and refined acid grades used in pigments, resins, and coatings. Kawasaki targets cost-sensitive, non-consumer applications such as cement additives and soldering fluxes. It is a preferred supplier to the Japanese electronics industry for toner and printing ink intermediates. Its strategy emphasizes performance consistency and cost efficiency over bio-based transition trends.

United States Succinic Acid Market Driven by Cost Targets and Downstream Integration

The United States succinic acid industry is undergoing a structural shift from pilot-scale bio-production toward cost-competitive industrial deployment. A central catalyst is the Department of Energy’s 2025 cost-down roadmap, which explicitly targets reducing bio-succinic acid prices to the $1–$2/kg range to enable direct substitution of petroleum-derived intermediates. This policy signal has accelerated capital allocation toward fermentation-based production, with industry surveys in 2025 indicating that more than two-thirds of U.S. chemical companies now prioritize microbial fermentation as their primary development pathway for specialty organic acids. These investments are increasingly focused on strain optimization, low-pH fermentation, and downstream separation efficiency to close the cost gap with maleic-anhydride-based routes.

Demand-side pull is equally strong. In 2025, OQ Chemicals expanded its Oxblue non-phthalate plasticizer portfolio using commercial volumes of bio-succinic acid from Louisiana, reinforcing the material’s role in food-contact and flexible packaging applications. Automotive suppliers have also accelerated adoption of succinic-acid-derived polyester polyols for polyurethane seating foams, achieving an estimated 30% lifecycle carbon reduction versus adipic-acid-based systems. Beyond polymers, high-purity electronic-grade succinic acid recorded a demand uptick in 2025 due to its use in advanced semiconductor cleaning chemistries at sub-5 nm nodes, while pilot programs under Sustainable Aviation Fuel mandates explored succinic acid as a renewable precursor for bio-kerosene components.

China Succinic Acid Market Anchored by Bioplastics and Feedstock Diversification

China has consolidated its position as a global manufacturing hub for succinic-acid-based polymers, supported by strong policy alignment and scale economics. The ongoing joint venture initiatives between CJ CheilJedang and BioAmber signal continued commitment to high-capacity bio-succinic acid production dedicated to the Asian bioplastics value chain. This momentum is reinforced by the 14th Five-Year Plan’s environmental mandates, which require comprehensive Environmental Impact Assessments for new facilities and explicitly favor low-emission fermentation routes over coal-derived chemical synthesis.

Downstream integration remains a defining feature. China leads global Polybutylene Succinate and PBSA production, with hubs in Anhui and Zhejiang upgrading in 2025 to integrated waste-to-acid platforms that link agricultural residues with polymer-grade succinic acid output. Semiconductor localization policies have further raised purity benchmarks, prompting domestic suppliers to introduce 99.9% grades suitable for electronics manufacturing. At the feedstock level, national pilots launched in 2025 to convert corn stover and other residues into fermentable sugars are strategically important, reducing reliance on food-grade glucose and strengthening the sustainability narrative of bio-succinic acid.

France Succinic Acid Market Positioned Around Pharma and Low-Carbon Credentials

France’s succinic acid landscape is shaped by its strong pharmaceutical and specialty materials ecosystem. The 2025 integration of IFF Pharma Solutions into Roquette’s Health and Pharma Solutions group created a vertically integrated platform for succinic-acid-based excipients and drug-delivery solutions, reinforcing France’s leadership in high-purity, regulated applications. Roquette’s BIOSUCCINIUM product continues to gain traction, with reported cradle-to-gate carbon footprint reductions of up to 90% compared with fossil-based alternatives, a metric increasingly valued by European footwear, textile, and coatings manufacturers.

Regulatory dynamics are amplifying this positioning. Updates to EU REACH in 2025 have driven demand for ECOCERT-certified, clean-label succinic acid in cosmetics and personal care, an area where French producers have moved early. Complementing regulatory pressure, national decarbonization incentives introduced in 2025 encourage industrial users to replace adipic acid with bio-succinic acid in resins and coatings, strengthening demand visibility in construction and industrial finishes.

India Succinic Acid Market Emerging Through Pharma and Bio-Manufacturing Policy

India’s succinic acid market is transitioning from niche consumption toward broader industrial relevance, underpinned by national bio-manufacturing and pharmaceutical strategies. The BioE3 Policy launched in mid-2025 formally designated bio-based chemicals as a priority thematic area, unlocking government-backed biomanufacturing hubs and funding for fermentation technologies. This policy framework aligns closely with India’s pharmaceutical base, where domestic utilization of succinic acid increased by around 20% in 2025 for API synthesis, including sedatives and corticosteroid intermediates.

Foreign and domestic investment momentum is accelerating. Under the Invest India framework, international producers have secured fast-track approvals to establish high-purity succinic acid units aimed at reducing import dependence for critical drug inputs. Concurrently, publicly funded research has expanded into novel applications, such as succinic-acid-based deep eutectic solvents supported by the Department of Biotechnology. These initiatives position succinic acid as both a pharmaceutical building block and a platform molecule for green solvent systems in metal processing and extraction.

Germany Succinic Acid Market Defined by Integrated Bio-Refineries and Coatings Innovation

Germany represents the most mature European market for bio-succinic acid integration, characterized by process sophistication and environmental governance. In 2025, the legacy Succinity technology was fully transitioned into an integrated bio-refinery model, optimizing low-pH yeast fermentation and improving yields from mixed carbohydrate streams. This shift has enhanced cost stability and reinforced Germany’s role as a technology reference point for bio-based dicarboxylic acids.

Environmental compliance is a competitive differentiator. German producers have led adoption of EMAS certification for succinic acid facilities, providing EU buyers with high transparency on emissions, resource use, and continuous improvement metrics. On the application side, the automotive cluster in Baden-Württemberg has driven commercialization of UV-curable succinic-acid-based polyurethane coatings, valued for their surface performance and reduced reliance on fossil-derived diacids. These coatings illustrate how Germany’s demand is increasingly tied to high-value, performance-led substitution rather than bulk volume growth.

Comparative Snapshot: Succinic Acid Industry by Country

Succinic Acid Market County Level Snapshot

|

Country

|

Primary Growth Driver

|

Key Applications

|

Strategic Positioning

|

|

United States

|

DOE cost-down targets

|

Plasticizers, PU foams, semiconductors

|

Scale-up of fermentation and downstream pull

|

|

China

|

Bioplastics leadership

|

PBS/PBSA, electronics

|

Integrated waste-to-acid manufacturing

|

|

France

|

Pharma and low-carbon demand

|

Excipients, textiles, coatings

|

Carbon footprint differentiation

|

|

India

|

Pharma expansion and BioE3 policy

|

APIs, green solvents

|

Import substitution and bio-manufacturing

|

|

Germany

|

Process integration and compliance

|

PU coatings, industrial uses

|

Bio-refinery efficiency and EMAS leadership

|

Succinic Acid Market Report Scope

Succinic Acid Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$794.2 Million

|

|

Market Size (2034)

|

$1998.9 Million

|

|

Market Growth Rate

|

10.8%

|

|

Segments

|

By Type (Bio-based Succinic Acid, Petro-based Succinic Acid), By Grade (Industrial Grade, Food and Beverage Grade, Pharmaceutical Grade, Electronic Grade), By Application (Polymers and Bioplastics, Chemical Intermediates, Solvents and Plasticizers, Food and Beverages, Pharmaceuticals, Personal Care and Cosmetics, Coatings and Resins)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Roquette Frères, BASF SE, Cargill, Incorporated, Mitsubishi Chemical Group Corporation, Anhui Sunsing Chemicals Co., Ltd., Kawasaki Kasei Chemicals Ltd., CJ CheilJedang Corporation, Nippon Shokubai Co., Ltd., Gadiv Petrochemical Industries Ltd., BioAmber Inc., Myriant Corporation, Shandong Lixing Chemical Co., Ltd., Technip Energies N.V., Anqing Hexing Chemical Co., Ltd., DSM-Firmenich

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Succinic Acid Market Segmentation

By Type

- Bio-based Succinic Acid

- Petro-based Succinic Acid

By Grade

- Industrial Grade

- Food and Beverage Grade

- Pharmaceutical Grade

- Electronic Grade

By Application

- Polymers and Bioplastics

- Chemical Intermediates

- Solvents and Plasticizers

- Food and Beverages

- Pharmaceuticals

- Personal Care and Cosmetics

- Coatings and Resins

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Succinic Acid Industry

- Roquette Frères

- BASF SE

- Cargill, Incorporated

- Mitsubishi Chemical Group Corporation

- Anhui Sunsing Chemicals Co., Ltd.

- Kawasaki Kasei Chemicals Ltd.

- CJ CheilJedang Corporation

- Nippon Shokubai Co., Ltd.

- Gadiv Petrochemical Industries Ltd.

- BioAmber Inc.

- Myriant Corporation

- Shandong Lixing Chemical Co., Ltd.

- Technip Energies N.V.

- Anqing Hexing Chemical Co., Ltd.

- DSM-Firmenich

*- List not Exhaustive