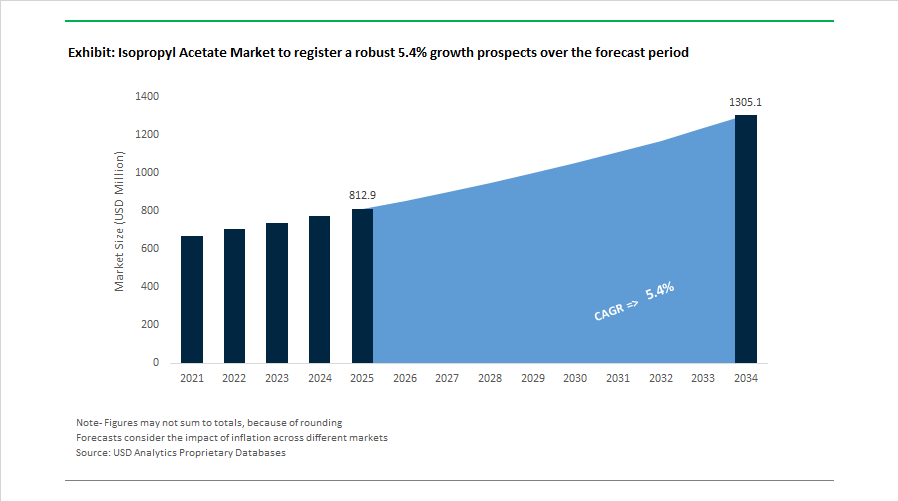

Isopropyl Acetate Market to Reach $1,305 Million by 2034 as Regional Capacity Shifts and Electronics Demand Accelerate

The Isopropyl Acetate Market is projected to expand from $812.9 Million in 2025 to $1,305 Million by 2034, registering a CAGR of 5.4%. Growth is being supported by rising demand from paints and coatings, pharmaceuticals, cosmetics, and increasingly, high-purity electronics applications. At the same time, the market is undergoing geographic rebalancing, pricing realignment, and supply-chain optimization as producers respond to energy cost volatility and trade policy shifts.

North America remains a strategic production center. In 2024, Dow expanded ester solvent capacity at its Deer Park, Texas facility, strengthening regional supply security for coatings and adhesives manufacturers. This move positioned Dow to capitalize on shifting trade flows and import disruptions. Building on this momentum, Dow launched its “Transform to Outperform” strategy in January 2026, targeting $1 billion in cost savings and reinforcing a pivot toward high-margin specialty esters, including electronic-grade isopropyl acetate. In parallel, ExxonMobil announced a $100 million investment in a new high-purity isopropyl-based plant in Baton Rouge, Louisiana, expected to enhance production of semiconductor-grade IPA and derivative isopropyl acetate by 2027. These investments underscore the solvent’s expanding role in precision cleaning for semiconductor wafers and optical components.

Europe is experiencing structural pressure. In November 2025, Ineos filed anti-dumping claims with the EU against low-cost acetate imports, arguing that high energy prices have undermined the competitiveness of domestic producers. Shortly thereafter, Celanese confirmed plans to cease operations at its Lanaken, Belgium acetate facility by the second half of 2026, citing unsustainable operating economics. At the same time, Moeve Global is preparing to commission Spain’s first major IPA and derivative production hub by late 2025, reducing Europe’s reliance on Middle Eastern imports and partially offsetting capacity rationalization in Northern Europe.

Asia-Pacific continues to strengthen its position. In 2024, Prasol Chemicals expanded acetate production capacity at its Maharashtra facility to meet rising pharmaceutical and cosmetic demand in India. Deepak Chem Tech followed in April 2025 with plans to expand IPA and derivative output to 100 kilotons by 2026, securing domestic feedstock integration. Meanwhile, BASF opened a Global Digital Hub in Hyderabad in January 2026 to deploy AI-enabled supply chain optimization across its acetate portfolio, improving inventory responsiveness in volatile markets.

Pricing discipline has returned after prior oversupply cycles. Eastman announced sequential ester price increases in early 2026, raising isopropyl acetate prices by $0.02–$0.04 per pound across multiple regions to offset raw material and freight inflation. Celanese also implemented global acetyl chain price increases in June 2025, reflecting heightened logistics costs and regulatory shifts.

Beyond industrial coatings, sustainable formulations are emerging as a competitive lever. In January 2026, Eastman partnered with Kolmar to advance bio-based and circular solvent technologies for cosmetics, incorporating sustainable grades of isopropyl acetate into fragrance and beauty applications. This signals a broader move toward lower-carbon solvent systems without sacrificing evaporation rate, solvency power, or formulation stability.

Trends and Opportunities Shaping the Global Isopropyl Acetate (IPAC) Market

Regulatory Substitution of HAP-Listed Solvents in Industrial Coatings

The Isopropyl Acetate market is undergoing structurally driven growth as regulators intensify enforcement against Hazardous Air Pollutant solvents across industrial coatings, automotive refinishing, and aerospace maintenance. The U.S. EPA’s National Emission Standards for Hazardous Air Pollutants, particularly the HON Rule amendments finalized in May 2024 and fully enforced through 2025, have materially altered solvent selection criteria. As a result, coatings formulators are accelerating the replacement of toluene, xylene, and methyl ethyl ketone with lower-toxicity alternatives that can meet tightening compliance thresholds without compromising performance.

A decisive catalyst came into force on January 17, 2025, when the EPA finalized revisions to the National VOC Emission Standards for Aerosol Coatings based on a relative reactivity framework. This Product-Weighted Reactivity approach structurally favors less reactive VOCs such as isopropyl acetate, enabling manufacturers to remain below regulatory limits that aggressive ketones increasingly fail to satisfy. This shift has elevated IPAC from a niche solvent to a strategic compliance tool in reformulated coating systems.

From a health and safety standpoint, IPAC is gaining preference due to its inclusion on the EPA Safer Chemical Ingredients List. Unlike MEK, which remains under persistent environmental and occupational scrutiny, IPAC is increasingly specified in wood, furniture, and plastic coatings as a lower-toxicity solvent that aligns with corporate ESG commitments. Industrial trials conducted during 2024 and 2025 confirm that IPAC delivers near performance parity, with an evaporation rate of approximately 3.0 compared to 3.8 for MEK, while offering superior resistance to blushing in high-humidity environments. This characteristic is especially critical in automotive refinishing and aerospace MRO operations, where surface defects directly translate into rework costs and downtime.

Upstream Feedstock Volatility from the Acetone and Propylene Value Chain

Despite strong downstream demand, the IPAC market remains exposed to pronounced feedstock volatility linked to acetone and propylene dynamics. Acetone is co-produced with phenol, tying its availability and pricing to bisphenol-A demand in construction and polycarbonate applications, while propylene costs fluctuate with global cracker operating rates. This structural linkage introduces margin uncertainty for IPAC producers, particularly during periods of regional oversupply or demand shocks.

In the third quarter of 2025, acetone prices displayed sharp geographic divergence. North American and European markets experienced declines ranging from 7.8% to 17.8% due to supply surpluses, while Middle Eastern prices strengthened amid robust petrochemical demand. This imbalance has forced IPAC producers to adopt dynamic surcharging mechanisms to stabilize profitability across contract and spot sales. Concurrently, global market assessments from October 2025 indicate that while crude oil prices stabilized near USD 63 per barrel, propylene feedstock costs remained volatile. These movements translated into quarterly fluctuations of roughly 2 to 3% in isopropyl alcohol pricing, the immediate precursor for IPAC.

Geopolitical trade flows further intensified volatility in late 2025. A sudden supply correction in the Chinese acetone market, with CFR Shanghai prices falling by 8.4% in October, triggered a surge of competitively priced exports into Southeast Asia. This disrupted traditional export corridors for U.S. and European IPAC producers, heightening competitive pressure and reinforcing the importance of flexible sourcing and regional diversification strategies for solvent manufacturers.

High-Purity Isopropyl Acetate for Botanical and Cannabinoid Extraction

One of the most attractive growth avenues for IPAC lies in botanical extraction and the legalized cannabinoid industry, where demand for green, food-grade solvents is scaling rapidly. As processors move away from n-hexane due to well-documented neurotoxicity and regulatory concerns, isopropyl acetate is emerging as a preferred alternative because of its favorable selectivity and Generally Recognized as Safe status.

By late 2025, extraction operators increasingly adopted IPAC-based broad-spectrum systems that efficiently solubilize cannabinoids and terpenes while rejecting polar impurities such as chlorophyll. This selectivity reduces the need for energy-intensive winterization steps, improving overall process economics. For pharmaceutical-grade CBD production, residue-free performance has become non-negotiable. IPAC’s medium boiling point of 88.8 degrees Celsius allows complete solvent removal under vacuum conditions without degrading heat-sensitive aromatic compounds, ensuring compliance with GMP requirements and tightening residual solvent limits.

Precision Cleaning Solvent Blends for Electronics and Optics Assembly

The rapid expansion of semiconductor fabrication, 5G smartphones, and advanced optics manufacturing has created a niche but high-margin opportunity for ultra-high-purity isopropyl acetate in precision cleaning applications. As device architectures shrink and tolerances tighten, manufacturers require solvents that balance cleaning efficacy with controlled evaporation.

In 2025, IPAC-based azeotropic blends gained traction for removing flux residues, oils, and particulates from precision optics, LED housings, and microelectronic assemblies without leaving streaks or residues. Compared to faster-evaporating alcohols, IPAC minimizes rapid cooling and condensation effects that can compromise yield in cleanroom environments. Equally important, IPAC demonstrates superior material compatibility across sensitive polymers and elastomers commonly used in aerospace, telecommunications, and advanced electronics hardware. This positions isopropyl acetate as a core component in multi-solvent cleaning systems designed to meet zero-defect manufacturing protocols, reinforcing its strategic relevance in high-value downstream industries.

Isopropyl Acetate Market Share and Segmentation Insights

Industrial Grade Isopropyl Acetate Leads the Market Through Cost-Effective Solvent Performance in Coatings and Cleaning

Industrial grade isopropyl acetate represented 52.80% of the Isopropyl Acetate Market share in 2025, making it the most widely consumed purity grade across industrial solvent applications. Industrial grade material typically contains 85–95% purity levels, which are sufficient for large-scale solvent uses in paints and coatings, printing inks, adhesives, and industrial cleaning formulations. Isopropyl acetate is valued for its balanced evaporation rate, strong solvency power, and relatively low toxicity compared with traditional aromatic and chlorinated solvents, enabling effective dissolution of resins, oils, and polymers used in industrial coatings and adhesives. Its compatibility with common resin systems such as acrylics, polyurethanes, and nitrocellulose supports widespread adoption across coating and ink manufacturing. In 2025, increasing regulatory scrutiny on high-VOC solvents and hazardous air pollutants has accelerated solvent substitution strategies within the chemical industry. Industrial-grade isopropyl acetate has therefore gained traction as a safer alternative to ketones, aromatics, and chlorinated cleaning solvents, helping manufacturers achieve regulatory compliance while maintaining performance in high-volume industrial processes.

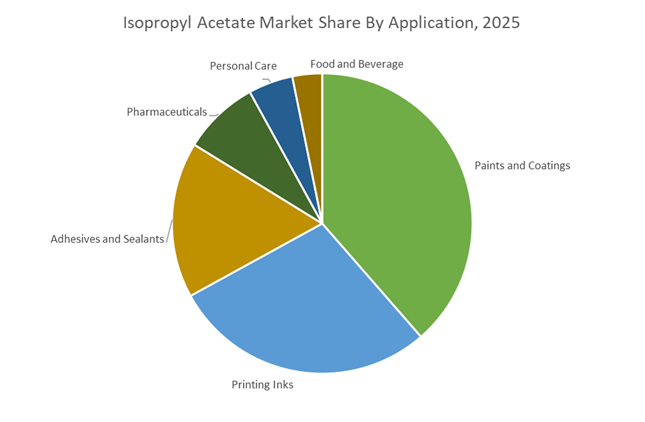

Paints and Coatings Industry Drives the Largest Demand for Isopropyl Acetate Solvents

Paints and coatings accounted for 38.60% of the Isopropyl Acetate Market share in 2025, making it the largest application segment for this solvent. Isopropyl acetate functions as an effective solvent and viscosity modifier in automotive refinish coatings, industrial protective coatings, wood finishes, and specialty coating formulations. The solvent’s moderate evaporation rate supports uniform film formation, smooth surface finish, and improved coating flow, which are critical properties in high-performance coatings used in automotive, industrial equipment, and construction applications. It also provides a low odor profile and strong resin solubility, allowing coating formulators to balance application performance with environmental compliance. In 2025, tightening industrial coating regulations regarding volatile organic compound emissions have increased demand for solvent systems that combine efficient solvency with improved environmental and safety profiles. As a result, isopropyl acetate is increasingly incorporated into low-VOC and compliant coating formulations, enabling manufacturers to maintain fast drying performance and production efficiency while aligning with global environmental standards governing industrial coating operations.

Competitive Landscape in Isopropyl Acetate Market

Dow Inc. Strengthens Low-VOC Oxygenated Solvent Leadership

Dow Inc. leverages its vertically integrated materials science platform to maintain a strong position in industrial-grade isopropyl acetate and broader oxygenated solvent portfolios. The solvent is valued for its rapid evaporation profile, low residue, and high dielectric strength, particularly in automotive refinishing and wood coating systems. Under its 2026 Decarbonize and Grow strategy, Dow is focusing on reducing Scope 1 and 2 emissions across chemical intermediates while expanding solvent capacity in high-growth regions. By late 2025, the company optimized solvent production lines to lower volatile organic compound profiles, aligning with stricter environmental regulations effective in 2026 across the EU and North America. Its global logistics network and downstream formulation partnerships reinforce supply reliability in performance coatings and industrial cleaning markets.

Eastman Chemical Company Targets High-Purity and Urethane-Grade Applications

Eastman Chemical Company differentiates its isopropyl acetate portfolio through high-purity solvent grades designed for pharmaceutical, medical device, and specialty urethane applications. The company is targeting adjusted EBITDA exceeding $450 million by year-end 2026, supported by solvent innovation and circular economy initiatives. Its Kingsport, Tennessee molecular recycling facility provides a technological foundation for future bio-based and circular solvent feedstocks. Eastman markets isopropyl acetate specifically for urethane-grade systems where moisture control, chemical resistance, and resin compatibility are critical for premium industrial finishes. In February 2026, Eastman signed a memorandum of understanding with Kolmar to accelerate sustainable personal care innovation, expanding solvent applications in fragrance extraction and cosmetic formulations.

BASF SE Expands Asian Supply and Carbon Transparency

BASF SE integrates isopropyl acetate production within its Verbund system to maximize feedstock efficiency and minimize waste streams. The startup of major units at the Zhanjiang Verbund site in China during 2026 significantly enhances local availability of chemical intermediates serving Asian coatings and printing ink manufacturers. Under its Winning Ways roadmap, BASF aims to achieve an annual cost reduction run rate of €2.3 billion by the end of 2026, channeling savings into green chemistry and low-carbon transformation initiatives. In February 2026, BASF outlined a free cash flow target of €1.5 billion to €2.3 billion, with capital expenditure prioritized for sustainability-driven projects. The company is accelerating rollout of detailed Product Carbon Footprint data for its solvent portfolio, offering transparent emissions tracking for each batch of isopropyl acetate supplied.

INEOS Group Secures Acetyl Integration and Pharmaceutical Focus

INEOS Group strengthened its isopropyl acetate supply chain through the $5 billion acquisition of BP’s acetyls and aromatics business, gaining control of 15 global production sites. This integration ensures secure acetic acid and propylene feedstock access critical for ester synthesis. Despite market volatility in late 2025, INEOS maintained high cracker utilization rates in early 2026 to safeguard raw material continuity. Project One in Antwerp, scheduled for late 2026 completion, is designed to be Europe’s most energy-efficient ethylene cracker, lowering the carbon intensity of downstream solvent production. INEOS is prioritizing hygienics and pharmaceutical markets, where high-purity isopropyl acetate is used for extraction of active ingredients and in medical-grade coatings.

Celanese Corporation Optimizes Acetyl Chain Efficiency

Celanese Corporation plays a central role in the acetyl chain, supplying acetic acid and related intermediates fundamental to isopropyl acetate production. The company reported 2025 net sales of $9.5 billion and is focusing on deleveraging and operational optimization within its Acetyl Chain segment during 2026. Divestiture of its Micromax business in early 2026 enables capital redeployment into core high-performance materials and solvent operations. Through a Footprint Optimization initiative, Celanese is consolidating manufacturing assets into highly efficient global hubs while strengthening supply to electronics and advanced materials sectors. A free cash flow target exceeding $770 million in 2026 supports balance sheet improvement and sustained investment in solvent and engineered material capabilities.

Tokyo Chemical Industry Dominates Ultra-High-Purity Laboratory Segment

Tokyo Chemical Industry occupies a specialized niche in ultra-high-purity isopropyl acetate for research, analytical, and pharmaceutical synthesis markets. The company supplies material exceeding 99.0% GC purity, targeting R&D laboratories and fine chemical producers requiring precise solvent specifications. Through a same-day dispatch logistics model operating from Japan and Hyderabad, TCI supports global just-in-time research demand. Unlike bulk solvent producers, TCI focuses on custom building block applications, positioning isopropyl acetate as a specialty reagent for complex organic synthesis pathways. Continuous optimization of storage and stability protocols ensures chemical integrity for high-sensitivity pharmaceutical and analytical environments.

China Isopropyl Acetate Market: Feedstock Reallocation and Electronic-Grade Acceleration

China’s isopropyl acetate industry is undergoing a decisive capacity and feedstock realignment driven by solvent demand growth rather than biopolymer expansion. In April 2025, Yuxin Co., Ltd. halted construction of its planned PBS facility and redirected capital toward a 200,000 tons per year isopropyl acetate and hydrogenation complex, alongside a 300,000 tons per year ethyl acetate unit. This strategic pivot reflects stronger near- to mid-term demand visibility for oxygenated solvents across coatings, electronics, and automotive refinishing. Policy alignment reinforces this shift, as the Ministry of Industry and Information Technology’s 2025–2026 growth blueprint prioritizes high-purity oxygenated solvents to lift the chemical sector’s added value through electronic-grade applications.

Regulatory pressure is accelerating downstream adoption. Tighter 2026 low-VOC protocols under China’s conformity assessment framework are positioning isopropyl acetate as a preferred substitute for restricted aromatic and ketone solvents, particularly in automotive coatings. Semiconductor and PCB manufacturing hubs in Zhejiang and Jiangsu are simultaneously driving a move toward ultra-high purity grades above 99.5% for precision cleaning. Pricing dynamics reflect this structurally firmer demand base, with export prices stabilizing in early 2026 after strong manufacturing activity during the prior automotive peak season. Vertical integration within coastal clusters is further buffering producers from feedstock volatility, improving margin predictability.

India Isopropyl Acetate Market: Vertical Integration and Import Shielding

India’s isopropyl acetate market is strengthening through feedstock integration and regulatory protection aimed at building domestic solvent resilience. In Maharashtra, GAIL (India) Limited is commissioning its first specialty chemicals complex at Usar, which includes dedicated isopropyl alcohol capacity. This development materially improves domestic availability of the primary feedstock for isopropyl acetate and supports downstream esterification economics. In Gujarat, Deepak Chem Tech Limited announced IPA capacity expansions in 2025, directly aligned with rising pharmaceutical demand for reaction solvents used in active ingredient synthesis.

Trade and efficiency policies are reinforcing this production push. The Directorate General of Foreign Trade’s September 2025 amendment restricting low-value acetate imports until 2026 has reduced exposure to predatory pricing, improving utilization rates for domestic plants. At the same time, the government’s January 2026 “Catalysts for Change” digital initiative targets solvent recovery optimization and distillation energy efficiency gains of 15% by 2027. Together, these measures are reshaping India from a net importer toward a more balanced producer-consumer market for isopropyl acetate.

United States Isopropyl Acetate Market: High-Purity Supply and Regulatory Alignment

The United States market is increasingly defined by high-purity requirements and regulatory-driven solvent selection. ExxonMobil is finalizing a USD 100 million high-purity IPA facility in Baton Rouge, with 2026 ramp-up expected to secure feedstock availability for electronic-grade isopropyl acetate used in semiconductor fabrication and medical diagnostics. This investment aligns with broader near-shoring trends as domestic producers prioritize supply reliability for advanced manufacturing sectors.

Regulatory developments are influencing downstream formulation choices. Consumer Product Safety Commission rules effective February 2026 have pushed formulators toward solvents with more favorable toxicity profiles, increasing preference for isopropyl acetate in household adhesives and cleaners. In parallel, Eastman Chemical Company introduced an electronic-grade solvent platform in late 2025 targeting EV and aerospace coatings that require controlled evaporation and leveling. With overall U.S. chemical exports softening in 2025 due to geopolitical friction, producers are refocusing volumes on North American personal care and specialty markets where demand visibility is stronger.

France Isopropyl Acetate Market: Pharmaceutical Scaling and Safer Solvent Substitution

France’s isopropyl acetate market is benefiting from pharmaceutical expansion and EU-wide solvent substitution dynamics. Seqens integrated a second isopropanol unit at the Roussillon platform, adding 50,000 metric tons of capacity and enabling scaled downstream production of pharmaceutical-grade isopropyl acetate from 2026 onward. This expansion strengthens Europe’s internal supply of high-purity esters used in complex API synthesis.

Regulatory momentum is amplifying demand. The European Chemicals Agency’s 2025 recommendations to expand the REACH Authorisation List are accelerating the replacement of chlorinated solvents across pharmaceutical and fine chemical operations. French research programs funded under the France 2030 plan are also positioning isopropyl acetate as a biocompatible carrier for next-generation drug delivery systems, extending its relevance beyond traditional solvent roles into formulation science.

Japan Isopropyl Acetate Market: Precision Applications and Energy-Efficient Manufacturing

Japan’s isopropyl acetate industry is characterized by precision manufacturing and process efficiency upgrades rather than capacity expansion. Sankyo Chemical Co., Ltd. and Kanto Chemical Co., Inc. have upgraded production lines to meet updated ISO 14001 and national industrial safety requirements, with a focus on applications such as silk screen printing and metal processing where solvent consistency is critical.

Process optimization is emerging as a competitive lever. From late 2025, major Japanese producers began deploying cyber-physical systems to monitor distillation latent heat in real time, targeting a 12% reduction in energy consumption for high-purity acetate production. These efficiency gains support Japan’s broader industrial decarbonization objectives while preserving its position as a supplier of premium, specification-driven isopropyl acetate grades.

Isopropyl Acetate Industry: Country-Level Strategic Snapshot

Isopropyl Acetate Market County Level Snapshot

|

Region

|

Primary Strategic Driver

|

Key Focus Area

|

Structural Impact

|

|

China

|

Capacity reallocation and MIIT policy

|

Electronic-grade and low-VOC solvents

|

Stronger domestic solvent self-sufficiency

|

|

India

|

Feedstock integration and import controls

|

Pharma and specialty synthesis

|

Reduced import exposure

|

|

United States

|

High-purity supply and safety regulation

|

Semiconductors and medical diagnostics

|

Near-shored premium volumes

|

|

France

|

Pharma capacity expansion and REACH

|

API synthesis and green solvents

|

Safer solvent substitution

|

|

Japan

|

Precision manufacturing and efficiency

|

Printing and metal processing

|

Premium, energy-efficient production

|

Isopropyl Acetate Market Report Scope

Isopropyl Acetate Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$812.9 Million

|

|

Market Size (2034)

|

$1305 Million

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Purity Grade (Industrial Grade, High Purity Grade, Ultra-High Purity Grade, Pharmaceutical Grade), By Function (Solvent, Chemical Intermediate, Cleaning and Degreasing Agent, Extraction Agent, Fragrance Carrier), By Application (Paints and Coatings, Printing Inks, Pharmaceuticals, Personal Care, Adhesives and Sealants, Food and Beverage), By Packaging Type (Drums, ISO Tanks, Flexitanks, Intermediate Bulk Containers)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dow Inc., Eastman Chemical Company, Seqens, INEOS Enterprises, BASF SE, Solvay S.A., Lotte Chemical Corporation, Mitsubishi Chemical Group, Kanto Chemical Co., Inc., Monument Chemical, Shandong Longze Chemical Co., Ltd., Deepak Chem Tech Limited, Yuxin Co., Ltd., Sankyo Chemical Co., Ltd., Ree Atharva Lifescience Pvt. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Isopropyl Acetate Market Segmentation

By Purity Grade

- Industrial Grade

- High Purity Grade

- Ultra-High Purity Grade

- Pharmaceutical Grade

By Function

- Solvent

- Chemical Intermediate

- Cleaning and Degreasing Agent

- Extraction Agent

- Fragrance Carrier

By Application

- Paints and Coatings

- Printing Inks

- Pharmaceuticals

- Personal Care

- Adhesives and Sealants

- Food and Beverage

By Packaging Type

- Drums

- ISO Tanks

- Flexitanks

- Intermediate Bulk Containers

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Isopropyl Acetate Industry

- Dow Inc.

- Eastman Chemical Company

- Seqens

- INEOS Enterprises

- BASF SE

- Solvay S.A.

- Lotte Chemical Corporation

- Mitsubishi Chemical Group

- Kanto Chemical Co., Inc.

- Monument Chemical

- Shandong Longze Chemical Co., Ltd.

- Deepak Chem Tech Limited

- Yuxin Co., Ltd.

- Sankyo Chemical Co., Ltd.

- Ree Atharva Lifescience Pvt. Ltd.

*- List not Exhaustive