Low Profile Additives Market 2025–2034: SMC Surface Engineering, Low-Carbon Marine Resins, and EV Lightweighting Driving $1,916 Million Outlook at 7.7% CAGR

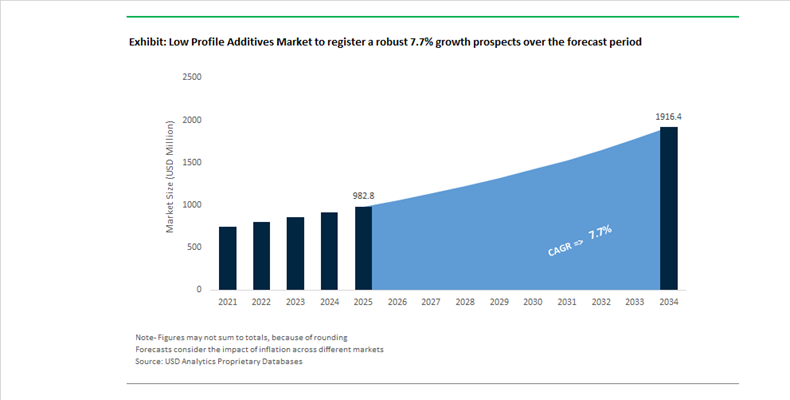

The Low Profile Additives (LPA) Market is projected to expand from $982.8 Million in 2025 to $1,916 Million by 2034, registering a CAGR of 7.7%. Growth is anchored in rising adoption of sheet molding compound (SMC), bulk molding compound (BMC), and unsaturated polyester resin (UPR) systems across automotive body panels, electric vehicle battery enclosures, marine hulls, rail interiors, and construction composites. Low profile additives, typically based on polyvinyl acetate, polystyrene, or thermoplastic modifiers, play a critical role in shrinkage control, surface smoothness, gloss retention, and dimensional stability. Increasing demand for Class A surface finish in lightweight composite components, particularly in EVs and premium marine applications, is driving formulation innovation that integrates LPAs directly with resin chemistry to reduce post-processing and painting requirements.

In February 2024, AOC commissioned a new production line in Nanjing to expand capacity for high-purity resins and associated low profile additives supporting China’s fast-growing EV sector. In March 2024, Polynt entered a non-binding Memorandum of Understanding to acquire Polyprocess, strengthening its European portfolio in gel coats and specialty resins tailored for aerospace tooling and high-precision LPA systems. Effective September 30, 2024, Reichhold do Brasil was merged into Polynt Composites Brazil, consolidating regional production and R&D for low shrink additives in automotive and infrastructure composites. In November 2024, AOC launched a UV-resistant automotive SMC system integrating advanced LPAs with specialized resin chemistry to eliminate read-through and enhance long-term exterior durability. These developments signal sustained investment in vertical integration and regional supply chain reinforcement.

In January 2025, IP Corporation completed the strategic integration of Interplastic and HK Research, combining LPA-enhanced resin platforms such as CoREZYN and Simlar with advanced gel coat technologies for marine and automotive markets. In the same month, AOC, Polynt, and Scott Bader released updated Life Cycle Assessment data via EcoInvent, quantifying environmental impact of LPA components and enabling verified sustainability credentials. In early 2025, Scott Bader introduced Crestapol 1240, incorporating internal additive technologies to reduce shrinkage and eliminate sanding during over-lamination in shipbuilding and rail manufacturing. In April 2025, Interplastic appointed new commercial leadership to accelerate uptake of low-exotherm and low-shrink resin systems utilizing advanced LPAs. In July 2025, LyondellBasell and Polynt collaborated on low-carbon marine resins compatible with bio-attributed feedstocks. At Plastindia 2026 in February, BASF demonstrated advanced light stabilizers co-formulated with LPAs to extend UV durability in construction profiles, reinforcing the convergence of surface performance and long-term structural stability in composite engineering.

Strategic Trends and High-Growth Opportunities Shaping the Low Profile Additives Market

Trend: Accelerated Shift Toward Bio-Derived and Recycled-Content Low Profile Additives

The low profile additives market is undergoing a structural transition as composite manufacturers align material choices with decarbonization targets and circular economy mandates. Policy frameworks such as the European Green Deal and U.S. Environmental Protection Agency objectives to divert 50% of composite waste by 2030 are pushing formulators away from conventional polyvinyl acetate based LPAs toward bio-derived and recycled-content alternatives. These next-generation additives are designed to deliver Class-A surface finish, low shrinkage, and dimensional stability while reducing embodied carbon in thermoset and vinyl ester systems.

Commercial momentum is already visible. In March 2024, BASF SE launched a portfolio of bio-based low profile additives engineered for structural composites used in automotive and industrial applications. Market analysts expect bio-based LPAs to grow at an annual rate approaching 9.5% through 2034, significantly outpacing traditional additive chemistries. Circularity validation is reinforcing this trend. A 2025 joint study conducted by NASA and the University of Alabama demonstrated fiber reclamation rates of 95% in polyester resin systems using advanced additives, directly supporting automotive circularity initiatives. Transparency is also becoming a competitive differentiator. In January 2025, producers including AOC and Polynt Group published updated life cycle assessment datasets via the EcoInvent 3.11 database, enabling tier-one suppliers to quantify the carbon advantages of next-generation UPR and vinyl ester systems incorporating sustainable LPAs.

Trend: Rheology Engineering to Enable High-Volume RTM and Vacuum Infusion

As aerospace, wind energy, and electric vehicle manufacturers scale resin transfer molding and vacuum assisted resin infusion, rheology control has emerged as a core performance requirement for low profile additives. LPAs are increasingly engineered to function as internal lubricants, lowering resin viscosity while maintaining uniform dispersion and shrinkage control. This capability is essential for achieving rapid fiber wet-out in dense carbon and glass fiber architectures without void formation.

Formulation breakthroughs during 2024 and 2025 have enabled ultra-low viscosity resin systems below 100 millipascal seconds even at high solids loadings. Peer-reviewed studies published in ACS Omega in 2024 reported that optimized diluent and additive ratios can reduce injection stabilization pressures by more than 70%, improving resin penetration into microfractures and complex core geometries. Industrial adoption is accelerating. In November 2024, AOC introduced a UV-resistant automotive SMC system that leverages advanced LPAs to control mold exotherm. This allows faster mold turnover and higher line utilization in high-speed automotive production. Infusion-specific LPAs are also gaining traction in large-scale structures such as wind turbine blades and marine hulls, where void-free laminates are critical for long-term fatigue performance and structural integrity.

Opportunity: LPAs for Mass Thermoforming of Continuous Fiber Thermoplastic Sheets

The automotive sector’s lightweighting agenda is unlocking a major growth opportunity for low profile additives in continuous fiber reinforced thermoplastic sheets. CFRTP and CFT materials offer cycle times under two minutes, making them suitable for high-volume structural parts including battery enclosures, rear seat shells, and underbody shields. However, maintaining dimensional stability during reheating and press forming remains a technical challenge that LPAs are uniquely positioned to address.

Rapid electric vehicle adoption is amplifying this opportunity. In 2025, global EV sales exceeded 17 million units, driving expanded use of polyamide-6-based continuous fiber composites such as those used in the Audi A8 rear seat shell, which achieves approximately 45% weight reduction compared to steel. Additive performance is central to manufacturability. Companies such as Avient and Lanxess have highlighted that their Tepex and Polystrand platforms rely on specialized additives to prevent blistering, control volumetric expansion, and preserve mechanical strength during post-forming. Recyclability further strengthens the business case. Unlike thermoset composites, CFT components are fully recyclable, aligning with the 2025 Joint Research Centre guidance on circular material use and positioning LPA-enhanced thermoplastics as a cornerstone of next-generation vehicle design.

Opportunity: Fire-Retardant Low-Shrink Systems for Mass Transit and Infrastructure

Stricter global fire, smoke, and toxicity standards are creating a high-value niche for low profile additives compatible with non-halogenated fire retardant systems. Regulations such as EN 45545-2 for rail applications are forcing composite suppliers to balance flame resistance with surface aesthetics and mechanical performance, particularly in interior panels and structural components for mass transit.

Technology demonstrations underscore this opportunity. In late 2024, AOC showcased flame-retardant composite systems at CAMX that achieved flame spread indices below 25 under ASTM E84 testing while maintaining smooth, defect-free surfaces. These systems rely on LPAs to counteract fiber print-through caused by high loadings of phosphorus-based or intumescent additives. Market demand is expanding as rail and metro operators increase capital spending on compliant materials. The global market for flame-retardant resin systems used in transit applications is projected to attract sustained investment through 2030, with vinyl ester formulations gaining preference for their chemical resistance and fire performance. Innovation is also moving toward multifunctionality. In 2025, Interplastic Corporation highlighted modified vinyl ester compounds that combine low smoke development, high fire retardant loading, and the smooth consistency required for premium interior finishes in aerospace and rail, positioning advanced LPAs as critical enablers of next-generation mass transit composites.

Low Profile Additives Market Share and Segmentation Insights

Polyvinyl Acetate Chemistry Leads Low Profile Additives Market in SMC and BMC Composite Manufacturing

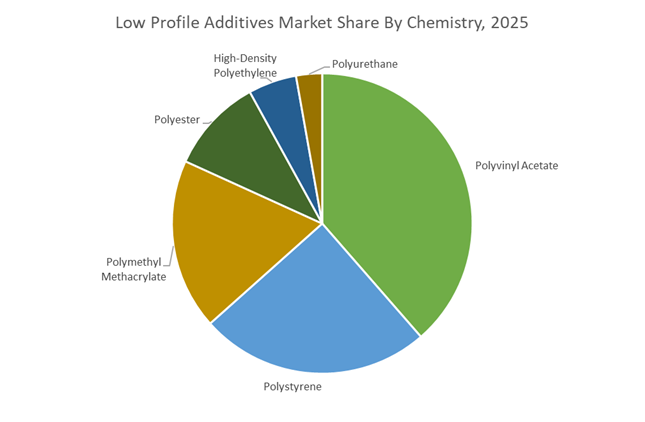

Polyvinyl acetate (PVAc) accounted for 38.60% of the Low Profile Additives Market share in 2025, positioning it as the leading chemistry used in thermoset composite processing. PVAc-based low profile additives are widely utilized in sheet molding compound (SMC) and bulk molding compound (BMC) manufacturing, where they control polymer shrinkage during curing and enable smooth, defect-free composite surfaces. These additives are essential for achieving high-quality surface finishes, dimensional stability, and improved mold release in polyester-based composite systems used in automotive and industrial components. PVAc chemistry offers a strong cost-to-performance ratio, compatibility with unsaturated polyester resins, and reliable processing characteristics, which has supported its widespread adoption across global composite production facilities. In 2025, manufacturers have increasingly developed hybrid low profile additive formulations combining PVAc with complementary polymer chemistries to tailor surface characteristics and reduce post-processing requirements. These advanced additive systems support the production of Class A surface finishes directly from compression molding processes, allowing composite components to meet demanding aesthetic and structural requirements without secondary finishing operations.

Automotive Sector Drives the Largest Demand for Low Profile Additives in Composite Components

Automotive applications accounted for 42.80% of the Low Profile Additives Market share in 2025, making the vehicle manufacturing industry the largest consumer of low profile additive technologies. Automotive manufacturers widely use SMC and BMC composite materials for the production of structural and cosmetic components including body panels, hoods, decklids, fenders, battery enclosures, and structural reinforcements. Low profile additives play a critical role in controlling polymerization shrinkage during thermoset curing, ensuring smooth surfaces that meet the stringent visual and dimensional standards required for automotive exterior panels. These additives enable composite parts to achieve paint-ready Class A surfaces, improved dimensional accuracy, and enhanced mechanical performance during high-volume automotive production. In 2025, the global push toward vehicle lightweighting and improved energy efficiency has accelerated the use of composite materials in passenger vehicles and commercial transportation platforms. Low profile additives therefore support the production of lighter composite automotive structures with reduced wall thickness while maintaining surface quality and mechanical strength, contributing to broader adoption of advanced composite materials across modern vehicle architectures.

Low Profile Additives Market Competitive Landscape

The low profile additives (LPA) market in 2026 is driven by EV lightweighting, zero-shrink SMC performance, and bio-based resin compatibility. Competitive focus is on vertically integrated resin-additive systems, low-carbon styrene solutions, and advanced surface control technologies that enable high-speed compression molding with minimal waviness and improved recyclability.

Polynt-Reichhold integrates resin and LPA chemistry to enable low-carbon composite systems

Polynt-Reichhold Group leads through deep vertical integration, controlling the full value chain from anhydrides to LPAs, ensuring precise compatibility with unsaturated polyester resins (UPR). Its collaboration with LyondellBasell on low-carbon styrene (+LC) solutions positions the company at the forefront of sustainable composite intermediates. With €2.16 billion turnover and 36 global plants, Polynt is scaling capacity in North America to meet EV-driven SMC demand. Its focus on zero-shrinkage performance and high-gloss finishes supports advanced automotive body panels and battery enclosure applications.

AOC accelerates automotive SMC innovation with UV-resistant and LCA-driven additive systems

AOC is strengthening its role as an automotive-grade LPA innovator by developing UV-resistant systems that maintain surface integrity and color stability without secondary coatings. Expansion in Nanjing enhances its ability to serve Asia-Pacific EV manufacturing hubs, while its pilot plant enables rapid co-innovation with Tier 1 suppliers. By providing detailed Life Cycle Assessment (LCA) data, AOC is aligning its LPA portfolio with regulatory demands for transparent, low-carbon materials. Strategic pricing actions further support margin stability amid raw material volatility.

Wacker advances hybrid silicone-PVAc LPAs for high-purity and thermal stability applications

Wacker Chemie AG differentiates through hybrid additive systems combining silicone and PVAc chemistries to deliver superior surface smoothness, pigmentation consistency, and impact resistance. Its VINNAPAS® resins function as high-efficiency LPAs, reducing shrinkage and enhancing Class A surface quality. New production capacity in China strengthens supply for advanced composites, while ongoing investments in semiconductor-grade purity enable LPAs that control coefficient of thermal expansion (CTE) in electronic housings. Cross-division integration supports multifunctional additives for both automotive and electronics applications.

INEOS scales LPA solutions for structural composites and recyclable FRP systems

INEOS Composites is leveraging its expertise in vinyl ester and UPR systems to deliver LPAs that prevent print-through and ensure dimensional stability in large-scale structures such as wind blades and chemical tanks. With over €800 million in sales and 17 global sites, the company is expanding production to meet EV-driven composite demand growth. Its research demonstrating 95% fiber reclamation in recyclable FRP highlights the role of advanced additives in enabling circular composite solutions aligned with 2030 waste reduction targets.

Interplastic enhances surface quality and process efficiency with integrated gel coat technologies

Interplastic Corporation is strengthening its position in North America through the integration of gel coat and resin businesses, creating a unified platform for advanced surfacing solutions. Its COR-Grip® low-shrink bonding technology improves cosmetic finishes in structural composites, while CoCure™ technology enables high-gloss, durable surfaces with minimal post-processing. The company’s focus on low-VOC formulations and process optimization services supports manufacturers transitioning to environmentally compliant, high-efficiency molding systems in 2026.

Swancor pioneers recyclable and bio-based LPAs for wind energy and infrastructure composites

Swancor Holding is advancing sustainable LPA technologies through its EzCiclo recyclable thermoset systems, enabling chemical recovery of both fiber and resin. Its development of lignin-based LPAs reduces reliance on petroleum-derived inputs, aligning with low-carbon automotive and infrastructure applications. Expansion in carbon fiber composites supports offshore wind blades exceeding 100 meters, where precise shrinkage control is critical. Leveraging strong Asia-Pacific demand, Swancor is targeting large-scale infrastructure projects with high-performance, environmentally advanced additive systems.

United States: Automotive Composites Localization and Medical-Grade Performance Demands

The United States low profile additives market is being reshaped by a measurable acceleration in automotive composite adoption and tightening trade dynamics. According to industry reporting from the American Composites Manufacturers Association, composite usage in U.S. automotive manufacturing increased by 11% during 2024–2025, directly elevating demand for Polyvinyl Acetate based low profile additives used to achieve Class A surface finishes on exterior body panels. This trend is particularly pronounced in electric vehicle battery enclosures, underbody shields, and lightweight structural components where shrinkage control and surface uniformity are critical to automated painting lines. In parallel, new U.S. tariffs imposed in early 2025 on selected imported chemical intermediates have materially altered cost structures, prompting domestic formulators to accelerate LPA localization strategies to protect margins through 2026.

Beyond transportation, medical and infrastructure applications are adding structural depth to U.S. demand. FDA communications during 2024–2025 highlighted increased adoption of Polymethyl Methacrylate in surgical instrument housings, driving the integration of PMMA-based LPAs to improve dimensional stability and thermal resistance in medical-grade fiber-reinforced plastics. At the same time, a 2024 Department of Energy assessment on advanced materials underscored higher penetration of anti-shrinkage additives in utility housings and electrical enclosures to meet new grid resilience standards. Reflecting this momentum, AOC Aliancys and INEOS Composites expanded U.S. technical service centers in 2025, providing real-time surface validation capabilities tailored to EV and energy infrastructure customers.

China: Scale Leadership with ESG-Driven Additive Upgrading

China remains the dominant global center for low profile additive production and consumption, but the market is transitioning from volume-led growth toward precision and sustainability. The Ministry of Industry and Information Technology 2026 work plan explicitly prioritizes high-end specialty rubbers and processing aids to support aerospace, electronics, and advanced transportation manufacturing. This policy direction is steering LPA development toward tighter shrinkage tolerances, improved compatibility with epoxy and vinyl ester systems, and enhanced performance in large-format composite structures.

Sustainability requirements are increasingly shaping competitive positioning. China’s 2025–2026 petrochemical work plan targets a 5% increase in chemical sector added value while emphasizing bio-based and low-VOC additives aligned with export market expectations. Within this context, BASF completed the transition of its Nanjing site to 100% renewable electricity in late 2025, reducing the product carbon footprint of specialty intermediates and LPAs by approximately 4%. Regulatory scrutiny is also intensifying, as the State Council Food Safety Commission’s May 2025 Comprehensive Governance Plan introduced higher transparency and traceability requirements for additives used in food-contact composite packaging, indirectly raising compliance thresholds across the LPA supply chain.

Germany: Circular Chemistry and Automotive Lightweighting Leadership

Germany’s low profile additives market is characterized by innovation intensity, circular economy leadership, and deep integration with the automotive value chain. At K 2025 in Düsseldorf, Evonik showcased mass-balanced certified VESTAMID and INFINAM materials optimized for low-profile performance, demonstrating CO2 emission reductions of up to 70% compared with conventional fossil-based resins. These developments underscore Germany’s role in translating circular chemistry principles into commercially viable processing additives for high-performance composites.

Automotive policy alignment further reinforces demand. The German Association of the Automotive Industry 2026 roadmap prioritizes composite-intensive vehicle architectures capable of delivering average weight reductions of around 15% in next-generation electric vehicles. High-efficiency LPAs are central to this strategy, enabling smooth surface finishes without secondary machining. Germany’s innovation pipeline remains robust, with more than 2,520 chemistry-related patents granted at the European Patent Office in 2024, many focused on non-PFAS processing additives and bio-based rheology modifiers relevant to future LPA formulations.

India: Specialty Chemical Upgrading and Global Value Chain Integration

India’s low profile additives market is entering a structural expansion phase driven by specialty chemical refocusing and policy-backed capacity creation. In December 2025, Arkema announced the divestment of its plastic additives business, including MBS and acrylic copolymers, to Indian industrial group Praana, with completion expected in Q1 2026. This transaction materially strengthens India’s capabilities in composite processing aids and positions domestic manufacturers closer to global OEM requirements.

Policy momentum is accelerating this transition. Realized investments under India’s Production-Linked Incentive scheme reached ₹1.76 lakh crore by mid-2025, catalyzing the construction of high-purity LPA manufacturing plants in Gujarat and western India. A 2025 NITI Aayog report identified specialty chemicals, including composite additives, as a priority segment in India’s ambition to capture 5–6% of the global chemical value chain by 2030. As a result, LPAs are increasingly being positioned not only for domestic infrastructure and automotive use, but also for export-oriented composite manufacturing.

Mexico: North American Automotive Additive Supply Reinforcement

Mexico is strengthening its role within the North American low profile additives supply network, supported by automotive-driven demand and multinational investment. BASF is expanding production capacity for lubricant and resin additives at its Puebla site, with completion targeted for 2026. While the expansion spans multiple additive categories, it directly supports rising demand for high-stability LPAs used in automotive composites across the U.S.–Mexico manufacturing corridor. This positions Mexico as a strategic extension of U.S. localization efforts, combining proximity advantages with competitive production economics.

Low Profile Additives Market: Country-Level Strategic Summary

Low Profile Additives Market County Level Snapshot

|

Country

|

Primary Demand Driver

|

Strategic Shift

|

Implication for LPAs

|

|

United States

|

Automotive composites, medical FRP

|

Localization under tariff pressure

|

Higher domestic LPA capacity and customization

|

|

China

|

Aerospace and advanced manufacturing

|

ESG and low-VOC upgrading

|

Shift from volume to precision additives

|

|

Germany

|

EV lightweighting, circular chemistry

|

Mass-balanced and non-PFAS innovation

|

Premium, low-carbon LPAs

|

|

India

|

Specialty chemical expansion

|

PLI-backed capacity and M&A

|

Emerging export-oriented LPA hub

|

|

Mexico

|

North American automotive supply

|

Multinational capacity expansion

|

Regional reinforcement of LPA supply

|

Low Profile Additives Market Report Scope

Low Profile Additives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$982.8 Million

|

|

Market Size (2034)

|

$1916 Million

|

|

Market Growth Rate

|

7.7%

|

|

Segments

|

By Chemistry (Polyvinyl Acetate, Polystyrene, Polymethyl Methacrylate, Polyester, Polyurethane, High-Density Polyethylene), By Function (Anti-Shrinkage, Surface Finish Improvement, Dimensional Stability, Pigmentation Control), By Manufacturing Process (Sheet Molding Compound, Bulk Molding Compound, Resin Transfer Molding, Pultrusion, Liquid Injection Molding), By End-Use Industry (Automotive, Construction, Electrical and Electronics, Marine, Aerospace)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Polynt-Reichhold Group, AOC Aliancys, INEOS Composites, Evonik Industries, BASF, Arkema, Wacker Chemie, Nouryon, Shin-Etsu Chemical, Swancor Holding, Interplastic Corporation, Scott Bader, Showa Denko, Praana Group, H.B. Fuller

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Low Profile Additives Market Segmentation

By Chemistry

- Polyvinyl Acetate

- Polystyrene

- Polymethyl Methacrylate

- Polyester

- Polyurethane

- High-Density Polyethylene

By Function

- Anti-Shrinkage

- Surface Finish Improvement

- Dimensional Stability

- Pigmentation Control

By Manufacturing Process

- Sheet Molding Compound

- Bulk Molding Compound

- Resin Transfer Molding

- Pultrusion

- Liquid Injection Molding

By End-Use Industry

- Automotive

- Construction

- Electrical and Electronics

- Marine

- Aerospace

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Low Profile Additives Market

- Polynt-Reichhold Group

- AOC Aliancys

- INEOS Composites

- Evonik Industries

- BASF

- Arkema

- Wacker Chemie

- Nouryon

- Shin-Etsu Chemical

- Swancor Holding

- Interplastic Corporation

- Scott Bader

- Showa Denko

- Praana Group

- H.B. Fuller

*- List not Exhaustive