Medical Membranes Market Overview: Size, Growth, and Industry Insights

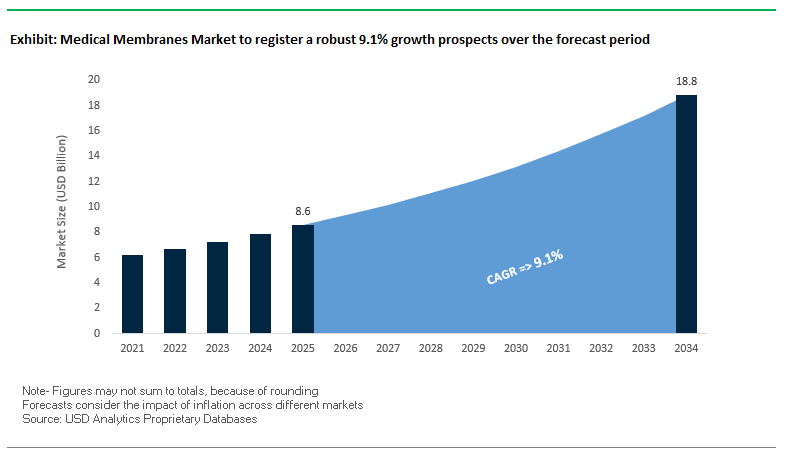

The global medical membranes market is valued at $8.6 billion in 2025 and is projected to reach $18.8 billion by 2034, growing at a strong CAGR of 9.1%. This growth is underpinned by the rising demand for biologics, expanding use in dialysis, emerging applications in wearable medical technologies, and stringent regulatory oversight. For industry professionals and decision-makers, medical membranes are no longer just auxiliary components—they are mission-critical technologies that determine the efficiency, safety, and scalability of modern medical treatments. From vaccine production to drug delivery devices, membranes are integral to innovation across the healthcare ecosystem.

Key Insights for Industry Professionals:

- Biologics fueling demand: Membranes are essential in filtration and purification for vaccines, monoclonal antibodies, and advanced biologics.

- Dialysis remains foundational: Hemodialysis continues to be a primary segment, driven by rising cases of chronic kidney disease globally.

- Wearable healthcare devices: Membrane integration in continuous monitoring and drug delivery devices reflects the rise of personalized medicine.

- Regulatory-driven quality: FDA and EMA standards require high-performance, sterile membranes, shaping design and manufacturing priorities.

- Convergence with high-tech: Innovations in nanotechnology and advanced materials expand applications in biosensors and next-gen devices.

Market Analysis: Recent Developments in the Medical Membranes Industry

The medical membranes industry is undergoing rapid transformation, with major advancements in materials science, manufacturing capacity, and biomedical applications. In August 2025, Asahi Kasei announced its plan to double production capacity of PIMEL™ photosensitive polyimide by 2030, a move that strengthens its footprint in electronics and medical devices alike. That same month, Sterlitech highlighted the increasing use of tangential flow filtration (TFF) for mRNA purification, underscoring how membranes are central to the production of mRNA vaccines and therapeutics.

In July 2025, Asahi Kasei further expanded its influence by announcing a new spinning plant in Japan dedicated to Planova™ virus removal filters, supported by Japan’s Ministry of Economy, Trade, and Industry. Meanwhile, DuPont’s FilmTec™ Fortilife™ XC160 Membrane won the prestigious R&D 100 Award, showcasing the company’s leadership in sustainable and high-performance filtration technology. In June 2025, TISSIUM received FDA IDE approval for its vascular sealant polymer, an innovation with potential crossover in medical filtration and device packaging. Additionally, in May 2025, Asahi Kasei introduced its Sunfort™ dry film photoresist, a material with applications in advanced semiconductor packaging that extend to medical device manufacturing.

Earlier in the year, Sterlitech announced in April 2025 that its track-etched polycarbonate membranes (PCTE) are being used to synthesize nanotubes and nanowires, paving the way for breakthroughs in biosensors and drug delivery. In March 2025, the approved merger of DS Smith and Mondi Group signaled consolidation within the packaging sector, potentially influencing downstream medical device and membrane packaging strategies.

Emerging Trends and High-Impact Opportunities in the Medical Membranes Market

Strategic Capacity Expansion to Support mRNA Vaccine and Therapeutic Production

The medical membranes market is experiencing a surge in capacity expansion driven by the growing mRNA vaccine and therapeutic sector. Leading material science companies are investing heavily to scale manufacturing of highly purified filtration membranes, which are critical for mRNA purification. The sustained demand stems from the expanding mRNA pipeline, including over 120 clinical trials for RNA-based cancer vaccines as of August 2025, alongside therapeutic development for genetic disorders. These advanced membranes enable streamlined bioprocessing, supporting modular manufacturing platforms that can reduce personalized vaccine production timelines from nine weeks to under four weeks. The trend also aligns with broader capital investments in biopharmaceutical manufacturing, such as a $120 million facility expansion in Germany for next-generation biologics. Collectively, these initiatives underscore the importance of specialized filtration membranes in meeting the growing demand for high-purity, mRNA-based therapies, and personalized medicine.

Regulatory Push for Advanced Pathogen Detection Driving Filtration Demand

New U.S. federal regulations are creating a pronounced need for precision filtration membranes in environmental and water quality monitoring. The Safe Drinking Water Act (SDWA) empowers the EPA to enforce stricter standards for microbial contaminants such as Cryptosporidium and Legionella, necessitating advanced filtration solutions for pathogen detection. Real-time monitoring is becoming critical, with modern sensors using membranes to filter particulates, ensuring accurate turbidity, dissolved oxygen, and contaminant measurements. Legislative frameworks, including the America’s Water Infrastructure Act (AWIA), require public water systems to implement risk and resilience assessments, further driving demand for membrane-based water monitoring technologies. These regulatory imperatives create a steady growth trajectory for filtration membranes, particularly in environmental monitoring and public health applications.

Development of Membranes for Point-of-Care Diagnostic Devices

The rise of decentralized healthcare has generated a high-growth opportunity for membrane-based point-of-care (POC) diagnostic devices. Membranes are essential for sample preparation, separation, and signal detection in rapid cartridge-based diagnostics for clinics, pharmacies, and home use. The global POC diagnostics market is expanding rapidly, with lab-on-a-chip devices relying heavily on thin, porous membranes to enable precise fluid manipulation and fast analyte detection. Membrane integration facilitates rapid disease diagnosis, with lateral flow assays capable of delivering results in 15 minutes or less. This opportunity positions membranes as a critical enabler of accessible, accurate, and fast POC testing, meeting the growing demand for decentralized and patient-friendly healthcare solutions.

Innovation in Membranes for Automated Cell Therapy Manufacturing

The scaling of autologous cell therapies, including CAR-T cells, presents a significant opportunity for novel membrane solutions in automated, closed-system manufacturing. Hollow fiber membrane bioreactors offer a controlled environment for optimal cell growth, providing large surface areas for gas exchange and nutrient delivery while maintaining high cell viability. These membranes enable closed-system manufacturing, reducing contamination risk and improving scalability for expensive, sensitive therapies. Integrated membrane-based gas exchange systems in bioreactors enhance cell expansion efficiency and ensure reproducibility, which is critical for commercializing advanced cell-based therapeutics. The trend highlights the strategic role of membranes in enabling cost-effective, safe, and high-quality cell therapy production.

Competitive Landscape: Key Players in the Global Medical Membranes Market

The global medical membranes market is defined by a mix of multinational corporations and specialized innovators. Companies compete on technology leadership, regulatory compliance, and the ability to integrate solutions into the fast-growing biopharmaceutical and dialysis industries. Strategic expansions, award-winning innovations, and cross-industry applications are setting the tone for competitive differentiation.

Pall Corporation: Leading Provider of Filtration and Purification Membranes

Pall Corporation, a Danaher subsidiary, is a global leader in filtration and separation solutions. Its membranes are extensively used in biopharmaceutical virus removal, sterile filtration, and cell harvesting. Key products like the Kleenpak™ Nova filter capsules and T-Series cassettes for TFF play a vital role in biologic drug manufacturing. Pall’s strength lies in its validated solutions and integrated single-use workflows, which help biopharma companies reduce contamination risks while accelerating time-to-market.

Asahi Kasei Corporation: Innovating with Planova™ Virus Removal Filters

Asahi Kasei is renowned for its Planova™ hollow-fiber filters, a global standard in virus removal for biopharmaceuticals. In July 2025, the company announced a new spinning plant in Japan, supported by government grants, to boost Planova™ production. Its “Trailblaze Together” growth strategy prioritizes life sciences as a core business pillar. With high-performance cellulose membranes offering both virus safety and protein permeability, Asahi Kasei continues to dominate the bioprocess membrane segment.

DuPont: Pioneering High-Performance Membranes for Life Sciences

DuPont has established itself as a leader in specialty membranes for water purification, pharmaceutical manufacturing, and bioprocessing. In July 2025, its FilmTec™ Fortilife™ XC160 Membrane won an R&D 100 Award, reflecting its commitment to sustainable, high-performance technologies. Leveraging R&D across industries, DuPont offers a broad membrane portfolio under FilmTec™ and Inge™ brands, with applications spanning reverse osmosis, ultrafiltration, and nanofiltration—key enablers of purity and process efficiency in medical manufacturing.

3M Company: Advancing Filtration and Separation for Biopharma

3M brings its diversified expertise in advanced materials into the medical membranes space, offering filters and chromatography media for biopharmaceutical purification. Its Zeta Plus™ depth filters are widely used in sterile filtration and cell clarification. 3M emphasizes knowledge leadership, publishing white papers on purification and water quality to strengthen its role as a trusted partner. With its broad technology base and cross-industry innovation model, 3M holds a strong competitive advantage in driving medical membrane adoption.

Sterlitech Corporation: Supporting R&D with Specialized Membranes

Sterlitech focuses on laboratory-scale membranes and filtration systems, catering to research and product development needs. In April 2025, it highlighted the use of its PCTE membranes in nanotube and nanowire synthesis, pointing to their role in next-gen biosensors and drug delivery platforms. The company’s strategy centers on enabling researchers with high-quality polymeric and ceramic membranes, along with bench-scale test equipment. With its integration capabilities and technical support, Sterlitech is a vital supplier in early-stage innovation for medical membrane applications.

Medical Membranes Market Share Insights

Microfiltration Leads Market Share by Technology in the Medical Membranes Industry

Microfiltration accounts for 35% of the global medical membranes market, positioning it as the cornerstone technology for sterility assurance. With pore sizes ranging from 0.1 to 10 microns, microfiltration membranes are indispensable in removing bacteria and particulates from injectable drugs, IV fluids, and medical gases used in ventilators and bioreactors. Their dominance is directly linked to the expansion of sterile pharmaceutical manufacturing and parenteral drug production, where zero microbial contamination is non-negotiable. Additionally, microfiltration is widely adopted in hospitals for in-line filtration of infusions, further reinforcing its recurring demand. While ultrafiltration and dialysis membranes are also critical technologies, microfiltration’s role as the universal workhorse in sterility compliance ensures it remains the largest contributor to market share.

Pharmaceutical Filtration Dominates Market Share by Application in Medical Membranes

Pharmaceutical filtration represents 30% of the medical membranes market, making it the largest application segment due to its essential role in drug manufacturing. From harvesting cell cultures to clarifying APIs, concentrating proteins, and removing viruses, membranes are integrated at nearly every stage of biologics and vaccine production. The complexity and high cost of these biologics drive reliance on ultrafiltration and nanofiltration membranes to ensure process integrity and product yield. At the same time, sterility requirements for injectable formulations mandate widespread use of microfiltration. The rapid growth of monoclonal antibodies, cell therapies, and next-generation vaccines ensures pharmaceutical filtration continues to dominate market value, as membrane technologies are irreplaceable in meeting regulatory, safety, and efficiency standards.

United States Medical Membranes Market Accelerates with FDA Regulations and Nanofiber Innovations

The U.S. medical membranes market is highly regulated under FDA standards, where advanced quality management systems and the Unique Device Identifier (UDI) system drive demand for high-purity, traceable membrane materials. Technological advancements in nanofiber membranes are enabling next-generation solutions for drug delivery, tissue engineering, and advanced filtration. A key trend is the development of single-use membrane assemblies to minimize cross-contamination in biopharmaceutical manufacturing.

Corporate investments are expanding capacity for specialized applications, exemplified by a major U.S. medical device company commissioning a membrane casting line in Massachusetts in late 2024 for gene therapy applications. Strong demand exists in biopharmaceutical manufacturing and dialysis, driven by the prevalence of chronic kidney disease and the growth of vaccine and monoclonal antibody production. Sustainability is gaining focus, with bio-based polymers being explored to reduce the environmental footprint of medical membranes.

Germany Medical Membranes Market Drives Growth with MDR Compliance and Bioprocessing Innovations

Germany’s medical membranes market operates under the EU Medical Device Regulation (MDR 2017/745), which requires enhanced traceability and stringent clinical data for all membrane-based devices. This regulatory pressure drives innovation in high-performance membranes for bioprocessing, sterile filtration, and single-use systems. Companies like Sartorius AG are leading the charge with next-generation single-use membrane technologies to meet pharmaceutical manufacturing needs.

Germany’s strong R&D ecosystem and robust pharmaceutical industry fuel demand for advanced membrane solutions. Strategic investments are being made to meet regulatory requirements and market needs, such as a French pharmaceutical firm investing €1.3 billion in insulin production in Frankfurt (August 2024), requiring high-quality filtration systems. Key applications span biopharmaceuticals, sterile filtration, and gene therapy, supported by Germany’s emphasis on quality healthcare and precision manufacturing.

China Medical Membranes Market Expands Through Domestic Manufacturing and Regulatory Streamlining

China’s medical membranes industry is supported by government initiatives, including the mid-2025 10-measure plan, aimed at accelerating high-end medical device production and streamlining approval processes. Regulatory reforms by the NMPA, including the draft Medical Device Administrative Law (MDAL), propose removing the requirement for imported devices to be pre-approved in their country of origin, simplifying market entry for foreign membrane manufacturers.

Technological investments in automation and AI are increasing production efficiency, supporting domestic high-end medical device manufacturing. The push for import substitution and circular products drives local expansion, with demand fueled by China’s booming pharmaceutical and healthcare sectors. Applications range from sterile filtration to specialized biopharma membranes, emphasizing quality, safety, and compliance with international standards.

India Medical Membranes Market Supported by Make in India and Advanced Manufacturing Policies

India’s medical membranes market is being propelled by the Make in India initiative and the National Medical Devices Policy 2023, promoting domestic manufacturing and innovation. In September 2025, the ICMR licensed nine cutting-edge health technologies, enhancing local production and commercialization. The CDSCO regulates medical devices, while the PLI Scheme incentivizes investment in MedTech manufacturing, including membrane technology.

Advanced membrane adoption is rising in dental, orthopedic, and cardiovascular applications, bolstered by joint ventures such as a Japanese company entering dialysis membrane production in India (late 2024). Investments in medical device parks like the Andhra Pradesh MedTech Zone (AMTZ) provide a favorable environment for R&D, production scaling, and advanced membrane manufacturing. The market benefits from growing healthcare infrastructure, rising medical device adoption, and high-performance, compliant membranes.

Japan Medical Membranes Market Leads with Precision Manufacturing and High-Performance Filtration

Japan’s medical membranes industry is driven by precision manufacturing and expertise in advanced material technologies, with companies like Asahi Kasei Medical and Toray Industries leading innovations in hemodialysis and virus filtration membranes. The PMDA enforces strict quality and safety regulations, while the May 2025 amendment to the Pharmaceuticals and Medical Devices Act strengthens supply stability, impacting manufacturing and supply chain logistics.

The market is increasingly focused on specialty and high-value membranes, particularly for sensitive devices requiring fast, reliable assembly and sterilization solutions. Demand is rising in surgical, dental, and advanced biopharma applications, where membranes must ensure sterility, efficiency, and superior performance. Japan’s emphasis on high-quality healthcare products and technological innovation positions it as a global leader in medical membrane solutions.

Brazil Medical Membranes Market Expands with UDI Implementation and Sustainable Membrane Development

Brazil’s medical membranes market is strengthened by the launch of the national UDI system (Siud) in July 2025, aligning with global traceability standards and impacting membrane labeling and compliance. Technological advancements focus on biodegradable, recyclable, and compostable membrane solutions, reflecting a growing sustainability trend.

Corporate investments are increasing, with companies establishing local manufacturing facilities to reduce dependency on imports and strengthen the domestic supply chain. For instance, Sonoco’s acquisition of its Brazilian joint venture stake (April 2022) expanded its local footprint. The market is driven by pharmaceuticals and medical device sectors, with rising demand for packaged, sterile, and high-performance membranes, supported by Brazil’s growing healthcare infrastructure and online retail expansion.

Medical Membranes Market Report Scope

Medical Membranes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.6 Billion

|

|

Market Size (2034)

|

$18.8 Billion

|

|

Market Growth Rate

|

9.1%

|

|

Segments

|

By Material (PES, PSU, PVDF, PP, PTFE, Cellulose Acetate, Others), By Technology (Microfiltration, Ultrafiltration, Nanofiltration, Dialysis, Gas Filtration, Others), By Application (Pharmaceutical Filtration, IV Infusion & Sterile Filtration, Hemodialysis, Drug Delivery, Bio-artificial Processes, Diagnostics), By End-User (Pharmaceutical & Biotechnology Companies, Hospitals & Clinics, Medical Device Manufacturers, Diagnostic Laboratories)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Merck KGaA (MilliporeSigma), Sartorius AG, 3M Company, Danaher Corporation (Pall Corporation), Asahi Kasei Corporation, W. L. Gore & Associates, Koch Membrane Systems, Inc., Toray Industries, Inc., Nipro Corporation, Medtronic plc, Mann+Hummel, GEA Group, Hangzhou Cobetter Filtration Equipment, Sterlitech Corporation, Novasep

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Medical Membranes Market Segmentation

By Material

- PES

- PSU

- PVDF

- PP

- PTFE

- Cellulose Acetate

- Others

By Technology

- Microfiltration

- Ultrafiltration

- Nanofiltration

- Dialysis

- Gas Filtration

- Others

By Application

- Pharmaceutical Filtration

- IV Infusion & Sterile Filtration

- Hemodialysis

- Drug Delivery

- Bio-artificial Processes

- Diagnostics

By End-User

- Pharmaceutical & Biotechnology Companies

- Hospitals & Clinics

- Medical Device Manufacturers

- Diagnostic Laboratories

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Medical Membranes Market

- Merck KGaA (MilliporeSigma)

- Sartorius AG

- 3M Company

- Danaher Corporation (Pall Corporation)

- Asahi Kasei Corporation

- W. L. Gore & Associates

- Koch Membrane Systems, Inc.

- Toray Industries, Inc.

- Nipro Corporation

- Medtronic plc

- Mann+Hummel

- GEA Group

- Hangzhou Cobetter Filtration Equipment

- Sterlitech Corporation

- Novasep

* List Not Exhaustive

Methodology

The research methodology for the global Medical Membranes market combines primary and secondary research, along with robust analytical modeling, to provide comprehensive insights tailored for industry professionals. Primary research involved interviews with membrane manufacturers, biopharmaceutical companies, dialysis equipment providers, regulatory authorities, and R&D experts to understand trends in filtration technologies, membrane materials, and specialized applications such as mRNA vaccine production and point-of-care diagnostics. Secondary research included the analysis of company reports, FDA, EMA, PMDA, and NMPA guidelines, industry publications, press releases, and technical white papers to validate innovations in microfiltration, ultrafiltration, and advanced membrane technologies. Market sizing, segmentation by material, technology, application, and end-user, as well as forecasting growth trajectories, was conducted using both top-down and bottom-up approaches, considering factors such as regulatory compliance, biopharmaceutical demand, dialysis adoption, wearable device integration, and emerging cell therapy applications. This methodology ensures that USDAnalytics delivers an accurate, data-driven overview of the competitive landscape, market drivers, and opportunities for strategic decision-making in the rapidly evolving medical membranes industry.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.