Market Overview: Mesoporous Silica Market Size, High-Growth Outlook, and Performance Benchmarks

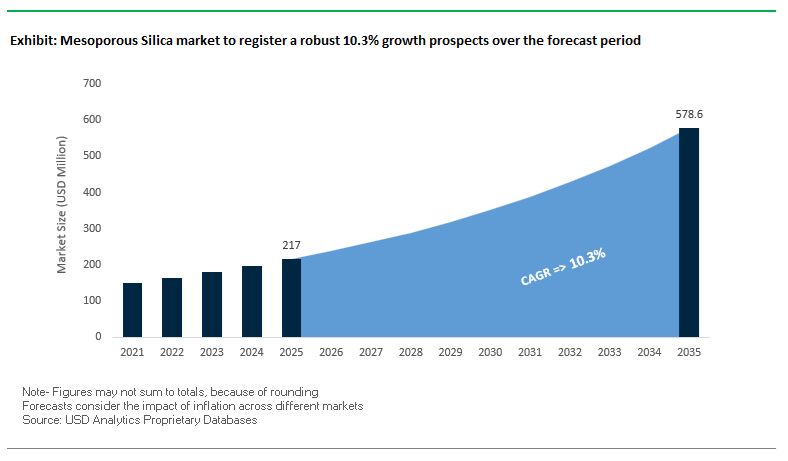

The Mesoporous Silica Market, valued at USD 217 million in 2025, is projected to reach USD 578.4 million by 2035, expanding at a strong CAGR of 10.3% (2025–2035). The market is witnessing accelerated adoption across pharmaceuticals, catalysis, nanomedicine, and environmental engineering due to continued advancements in surface engineering, pore-size control, and scalable synthesis technologies. Manufacturers and vendors are heavily investing in high-performance SBA-15 and MCM-41 materials, production automation, and biologically safer nanoparticle designs to meet evolving compliance requirements and performance expectations. Increasing demand for drug delivery carriers, bioavailability enhancers, heterogeneous catalysts, and high-efficiency adsorbents continues to structurally support the market’s growth trajectory.

Industry performance indicators show remarkable manufacturing precision, with pore size polydispersity below 10%, enabling consistent drug-release kinetics in nano-therapeutics. Advanced MSNs demonstrate drug loading efficiencies above 40%, positioning mesoporous silica as a premium excipient and carrier for poorly soluble APIs. In catalysis, engineered materials maintain surface areas of at least 900 m²/g post-functionalization, ensuring strong active site dispersion and reaction stability. Commercial synthesis methods, particularly template-assisted continuous flow processes, have reduced costs significantly, delivering more than 30% yield improvement due to enhanced surfactant recovery and process optimization. However, regulatory hurdles remain high for nanomedicine applications, where long-term toxicity and biodistribution studies often span 5–7 years, slowing the transition from research to commercial-scale therapeutics.

Key Industry Insights

- Uniform pore size distribution (<10% deviation) is enhancing controlled drug release performance.

- Drug loading efficiencies exceeding 40% w/w are boosting adoption in bioavailability-enhanced formulations.

- Catalysis-grade mesoporous silica consistently delivers ≥900 m²/g surface area, supporting high-value chemical reactions.

- Advanced continuous-flow synthesis has improved commercial yields by over 30%, reducing production costs.

- Nanomedicine applications face stringent regulatory scrutiny with 5–7 year safety evaluation cycles.

Market Analysis: Strategic Moves, Patents, Expansions, and Funding Trends Shaping the Mesoporous Silica Sector

The global Mesoporous Silica Market is undergoing structural transformation driven by mergers, product innovations, patent filings, sustainability initiatives, and government-backed nanotechnology funding. A major strategic milestone occurred in January 2025, when Evonik Industries merged its Silica and Silanes divisions into a unified entity, Smart Effects, enabling the integration of molecular silane chemistry with silica particle engineering. This move positions the company strongly in emerging markets such as CO₂ capture, green chemistry, and functional surface coatings. In parallel, innovation in therapeutic applications advanced with Sigrid Therapeutics securing a U.S. patent for its SiPore platform in December 2024, targeting metabolic disorder prevention through engineered mesoporous silica structures.

Product development geared toward biomedical markets accelerated in April 2024 with the launch of new high-purity mesoporous silica materials offering tunable pore structures and advanced surface functionalization for drug-delivery applications. Environmental applications of mesoporous silica are also gaining traction; in September 2025, a specialty chemical manufacturer entered a partnership with an environmental-technology firm to develop next-generation silica adsorbents for wastewater treatment and gas-separation technologies—broadening the material’s relevance beyond pharmaceuticals and catalysts.

Capacity expansion remains a key theme, especially in Asia-Pacific. Taiyo Kogyo Corporation reported an 18% production capacity increase in Osaka (referenced in 2024 reports for its 2023 expansion) to meet surging demand for pharmaceutical-grade silica in the region. Intellectual property activity remains robust, with approximately 55% of new silica-related patents focusing on mesoporous structures engineered for durability, functionalization, and chemical reactivity—highlighting the innovation intensity in biosensors and smart material development. M&A activity also plays a significant role; the acquisition of nanoComposix by Fortis Life Sciences in July 2021 expanded high-precision nanomaterial supply for diagnostics and assay development.

Government funding is strengthening the ecosystem as well. The U.S. federal nanotechnology budget exceeded USD 2.16 billion in 2024, a sizable portion directed to translational research supporting advanced materials such as mesoporous silica for medical, environmental, and energy applications. This convergence of public funding, patents, product launches, and corporate expansions is reinforcing the global market’s growth momentum.

Breakthrough Trends Driving Advanced Adoption of Mesoporous Silica Across Biopharma and Climate Technologies

Market Trend 1: Rapid Integration of Mesoporous Silica Nanoparticles into Next-Generation mRNA Therapeutic Delivery Platforms

Mesoporous silica nanoparticles (MSNs) are undergoing a significant surge in relevance within the biopharmaceutical and vaccine ecosystem as researchers seek delivery systems that outperform lipid nanoparticles (LNPs) in stability, transfection efficiency, and regulatory compatibility. In vivo studies show that virus-like MSN formulations coated with lipid bilayers achieve extended systemic circulation, recording half-life values of ~7 hours compared to 4.2 hours for benchmark LNP systems. This enhanced circulation time directly improves mRNA availability in target tissues, making MSNs a compelling candidate for next-generation genetic medicines.

Furthermore, MSN-based delivery vectors demonstrate markedly higher cellular transfection efficiency across specific liver and non-liver cell lines. This enables stronger protein expression and therapeutic potency—two critical performance metrics in mRNA vaccines, gene editing therapies, and protein replacement therapies. The industry’s confidence in silica is reinforced by a critical regulatory milestone: FDA approval of silica-based Cornell dots (C-dots) for Phase I human clinical trials, firmly establishing silica’s biocompatibility profile for human use and lowering the regulatory barrier for MSN-enabled mRNA therapies.

The nanoconfinement effect of MSNs—enabled by their tunable 2–50 nm pores—provides a structurally rigid, non-degradable host that minimizes mRNA aggregation and protects against nuclease-mediated degradation. This stability advantage positions the Mesoporous Silica Market as a foundational materials supplier for the shift toward ultra-stable, targeted, and scalable mRNA therapeutics.

Market Trend 2: Emerging Use of Mesoporous Silica as a Regenerable High-Capacity Sorbent for Direct Air Capture (DAC)

Another transformative trend is the increasing deployment of amine-functionalized MSNs in Direct Air Capture systems, driven by their superior adsorption, desorption, and reusability characteristics. High-performance MSN structures such as SBA-15 and MCM-41 achieve CO₂ adsorption capacities of 2.4–2.6 mmol/g (10–11 wt%), positioning them as leading solid sorbents in the carbon removal sector.

A core technological advantage is their ability to undergo low-temperature regeneration, with complete CO₂ desorption occurring at mild conditions below 110°C, and in some prototype systems, even as low as 80°C. This dramatically reduces the energy penalty associated with DAC regeneration cycles and supports the global push for scalable carbon removal solutions.

MSN-based sorbents also demonstrate exceptional cycling stability, retaining high amine utilization efficiencies (e.g., 0.20 mol CO₂/mol N) across multiple adsorption-desorption cycles, validating their commercial durability. The tunable pore structure, especially in systems like SBA-15 with 5–30 nm pores, enhances polymeric amine loading and ensures high functional density for CO₂ capture. These properties collectively strengthen mesoporous silica’s strategic role in the next generation of energy-efficient carbon capture technologies.

Emerging Commercial Opportunities Enabled by Mesoporous Silica Across Agriculture and Pharmaceuticals

Market Opportunity 1: Acceleration of Smart Agricultural Inputs Through Precision Nutrient and Pesticide Release

In the agricultural sector, MSNs present a high-value opportunity to replace traditional nutrient and pesticide systems with precision-controlled, environmentally safe smart delivery platforms. MSN carriers loaded with fertilizers such as urea demonstrate extended soil release profiles lasting up to five times longer than uncoated fertilizers—illustrated by data showing 78% urea release over 5 days versus 24 hours for bulk formulations. This controlled release reduces nutrient loss, improves crop uptake, and minimizes over-fertilization.

MSN-based pesticide formulations represent a breakthrough in environmental stewardship, with studies reporting drastically reduced acute toxicity—for example, an LC50 of 257.867 mg/L, dramatically safer than free-form pesticides. In field applications, even untreated MSNs have delivered up to 75% reduction in fertilizer requirements for turfgrass species like zoysiagrass with minimal impact on initial growth, signalling significant cost and sustainability benefits.

What sets MSNs apart is their ability to be engineered with stimulus-responsive gatekeepers, enabling pore opening only under specific soil-trigger conditions such as local pH changes or enzyme activity at the root interface. This positions MSNs as a foundational technology for the transition toward smart, climate-resilient, resource-efficient agriculture.

Market Opportunity 2: Establishment of Mesoporous Silica as a Platform Excipient for Oral Drug Solubility Enhancement

MSNs offer a transformative opportunity in pharmaceutical formulation by enabling dramatic solubility and bioavailability improvement for poorly soluble Biopharmaceutical Classification System (BCS) Class II drugs. The nanoconfinement effect stabilizes drug molecules in their amorphous state by preventing recrystallization—an inherent limitation of traditional amorphous solid dispersions.

Pharmacokinetic studies in animal models consistently show 1.8× to 2.3× increases in relative bioavailability (AUC) for MSN-based formulations compared to commercial tablets, marking a step-change in oral drug delivery performance. Key material attributes—including specific surface area exceeding 700 m²/g and pore volume up to 1.5 cm³/g—enable high drug loading and rapid dissolution into supersaturated, therapeutically relevant concentrations.

MSNs have demonstrated successful solubility enhancement across a diverse set of APIs such as valsartan, ritonavir, and fenofibrate, reinforcing their potential as a standardized, commercially scalable, and multifunctional platform excipient. This opportunity positions mesoporous silica as a strategic enabler in next-generation oral drug development programs targeting enhanced therapeutic bioavailability.

Mesoporous Silica Market Share Analysis

Market Share by Structure: MCM-41 Solidifies Leadership in High-Performance Mesoporous Silica Applications

MCM-41 maintains the largest share of the mesoporous silica market—approximately 28% in 2025—anchored by its structurally ordered hexagonal pore network, high specific surface area, and cost-efficient synthesis, which collectively position it as the most widely adopted mesoporous variant across research and industrial settings. Its simple and scalable preparation route using cationic surfactant templates, combined with tunable pore sizes between 2–10 nm, enables manufacturers and researchers to achieve consistent performance across adsorption, catalysis, and drug delivery applications. The segment’s dominance is further reinforced by its excellent functionalization potential, allowing MCM-41 to be engineered with amine, thiol, metal, or ligand groups, which significantly enhances its applicability in precision drug delivery, pollutant adsorption, and catalytic processes in the chemical and petrochemical industries. As industries shift toward engineered nanostructures for controlled release systems, high-capacity adsorption technologies, and fine-chemical synthesis, MCM-41’s flexibility and well-documented behavior make it the preferred mesostructure for both academic innovation and commercial deployment. Its widespread availability, lower production cost compared to more complex cubic or fibrous structures like MCM-48, KIT-6, or KCC-1, and strong alignment with emerging nanotechnology applications ensure it retains a commanding share of the mesoporous silica landscape.

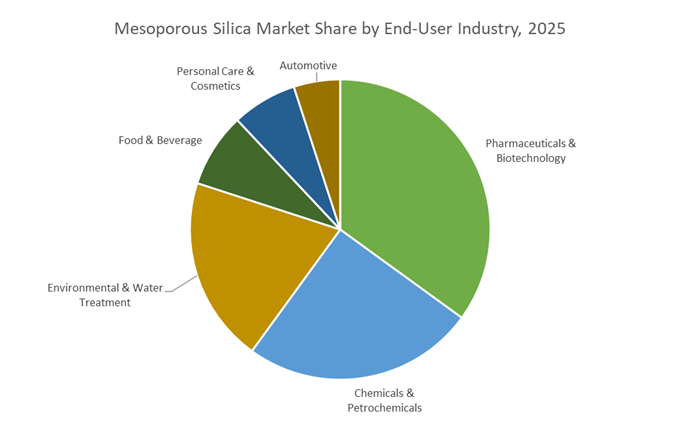

Market Share by End-User Industry: Pharmaceuticals & Biotechnology Lead Market Demand

The Pharmaceuticals & Biotechnology sector commands the largest end-user share—approximately 35% in 2025—driven by its intensive reliance on mesoporous silica nanoparticles (MSNs) for advanced drug delivery systems, targeted therapeutics, and nanomedicine research. The segment’s influence is propelled by mesoporous silica’s uniquely high surface area, large pore volume, and exceptional tunability, enabling pharmaceutical developers to design controlled-release formulations, improve solubility of poorly water-soluble drugs, and achieve targeted delivery to diseased tissues. As the industry accelerates toward precision medicine, oncology-focused nanocarriers, and biologics encapsulation, MSNs provide the structural and chemical versatility required for high drug loading and stimuli-responsive release mechanisms. Their biocompatibility and degradability further enable safe therapeutic deployment, contributing to widespread adoption across clinical research pipelines. Additionally, rapid advancements in theranostics—integrated therapeutic and diagnostic platforms—continue to elevate demand for mesoporous silica constructs capable of carrying imaging agents alongside active pharmaceutical ingredients. With North America, Europe, and emerging Asian R&D hubs expanding investments in nanotechnology and biologics manufacturing, pharmaceuticals and biotechnology remain the dominant growth engine, sustaining the segment’s leading market share and shaping the future direction of mesoporous silica innovation.

Country Analysis: Key Drivers in the Mesoporous Silica Ecosystem

China: Nanomaterials Commercialization Momentum and Industrial-Scale Mesoporous Silica Deployment

China continues to be the most influential geography in the global Mesoporous Silica Market, driven by its expanding nanotechnology research base, state-backed innovation programs, and large-scale chemical manufacturing infrastructure. In 2024, leading Chinese research institutions published breakthrough findings on functionalized Mesoporous Silica Nanoparticles (MSNs) for advanced wastewater treatment, demonstrating exceptional efficiency in removing heavy metals such as chromium and cadmium. This directly aligns with China’s increasingly stringent environmental remediation mandates, making mesoporous silica a strategic material for nationwide sustainability initiatives. Parallel growth is evident in biomedical applications as domestic biopharma startups scale the production of MSN-based drug delivery vectors designed for improved bioavailability of poorly soluble APIs and controlled-release therapeutics.

The country's strong petrochemical and fine chemical sectors also drive adoption of advanced mesoporous materials like SBA-15 and MCM-41 as high-performance catalyst supports, improving yield optimization and reducing energy consumption in large-scale industrial reactions. Additionally, China’s renewable energy push is increasingly supported by government-backed research aimed at integrating mesoporous silica in next-generation lithium-ion batteries and supercapacitors, particularly as a solid-state electrolyte component. This combination of environmental, industrial, biomedical, and energy-centric innovation firmly establishes China as a central catalyst for future mesoporous silica commercialization.

United States: Frontier Research in Drug Delivery, Diagnostics, and High-Value Silica Engineering

The United States remains a global powerhouse in premium-grade mesoporous silica applications, particularly in precision medicine, drug delivery, and specialty chemicals. Following Fortis Life Sciences’ acquisition of NanoComposix, U.S. biotech firms gained expanded access to highly functionalized Mesoporous Silica Nanoparticles used in in vitro diagnostics and complex assay development. This aligns with increasing NIH/NSF-funded research, including a 2024 study demonstrating drug-free Mesoporous Silica Nanoparticles successfully suppressing cancer metastasis in vivo, opening new pathways in theranostics and immune modulation platforms.

Industrial demand further strengthens the U.S. market, with W.R. Grace & Co. leveraging its expertise in silica materials to produce specialty catalyst carriers and adsorbents tailored to petrochemical upgrading processes that rely on controlled pore-size distributions. In advanced energy systems, U.S. DOE-funded researchers are exploring mesoporous silica frameworks for thermal energy storage and solid-state battery optimization, aiming to improve energy density and thermal stability for grid-scale and electric vehicle applications. Together, a combination of frontier biomedical research, high-value industrial materials engineering, and energy storage innovations positions the United States as a leading hub for high-purity mesoporous silica specialization.

Germany: Industrial Catalysis Leadership and High-Purity Mesoporous Silica for Specialty Chemical Advancement

Germany remains a core innovation center in the Mesoporous Silica Market, supported by its robust specialty chemical industry and long-standing leadership in technical materials for industrial catalysis. Evonik Industries AG continues to strengthen its silica product portfolio, focusing on functionalized mesoporous materials engineered for green tire manufacturing and advanced catalytic reactions. These innovations enable improved surface interactions, higher selectivity, and greater efficiency in industrial-scale chemical transformations. Germany’s emphasis on precision materials is further reinforced by Merck KGaA (MilliporeSigma), which supplies research-grade mesoporous silica optimized for biomedical testing, surface modification trials, and next-generation chromatography workflows.

Complementing commercial innovation, academic-industry collaborations in 2024 achieved significant milestones by developing mesoporous silica-coated silver nanoparticles that delivered enhanced antimicrobial activity against drug-resistant bacteria. Such advancements highlight Germany’s focus on medical-grade nanomaterials and potential applications in device coatings and infection-resistant clinical surfaces. EU-backed sustainability initiatives also drive the adoption of mesoporous silica-supported catalysts designed to minimize waste generation and energy consumption in industrial chemistry, reinforcing Germany’s commitment to green process innovation.

Japan: High-Precision Mesoporous Silica Engineering for Chromatography, Cosmetics, and Semiconductor Manufacturing

Japan maintains a highly specialized position in the global Mesoporous Silica Market, owing to its expertise in precision materials science and controlled-release technologies. Leading Japanese firms such as Taiyo Kagaku and Fuji Silysia Chemical continue to utilize mesoporous silica in high-performance cosmetics and skincare formulations, where pore-engineered silica improves oil absorption, enhances texture, and enables controlled release of active compounds. This capability supports Japan’s premium beauty segment, which demands advanced material engineering for superior product performance.

The country's scientific rigor extends to chromatography, with Japanese manufacturers producing highly uniform spherical mesoporous silica particles essential for protein purification, biomolecule separation, and pharmaceutical-grade analytics. Additionally, Japanese researchers are pushing the boundaries of electronic materials by exploring ultra-fine mesoporous silica abrasives for CMP (Chemical Mechanical Planarization), a critical step in semiconductor wafer finishing that requires atomically smooth surfaces. Mesoporous silica is also gaining traction in food and beverage purification processes, where selective adsorption capabilities allow removal of unwanted contaminants without impacting product quality. These diversified, high-value applications underscore Japan’s leadership in precision-engineered mesoporous materials.

South Korea: Accelerated Development of Therapeutic Nanocarriers and Advanced Diagnostic Silica Platforms

South Korea is rapidly becoming a key growth node in the Mesoporous Silica Market, supported by the nation’s strong biotechnology ecosystem and high adoption of advanced medical technologies. Research institutions collaborating with Nano Targeting & Therapy Biopharma Inc. are developing increasingly sophisticated MSN-based drug delivery frameworks, integrating targeted ligands and responsive release mechanisms optimized for personalized nanomedicine. These platforms support tailored cancer therapies, gene delivery modules, and next-generation therapeutic formulations designed for high drug-loading efficiency.

South Korea’s innovation also extends into diagnostic technologies, where mesoporous silica films are being engineered for use in ultrasensitive biosensors capable of enzyme immobilization and enhanced molecular detection. Corporate R&D teams are simultaneously scaling production of Hollow Mesoporous Silica Nanoparticles (HMSNs), prized for their tunable shell permeability and their ability to carry high payloads of anticancer drugs. The convergence of diagnostic and therapeutic innovation positions South Korea as a rising leader in medical-grade mesoporous silica applications.

Competitive Landscape: Leading Players Advancing Mesoporous Silica Innovation and Supply Chain Strength

The competitive landscape of the Mesoporous Silica Market is shaped by companies specializing in high-purity silica production, nanomaterials synthesis, pharmaceutical excipients, advanced catalyst supports, and nanoscale characterization. Vendors are intensifying investments in surface engineering, pore-size design, continuous-flow manufacturing, regulatory compliance, and biomedical-grade materials to address the expanding spectrum of high-value applications. Collaboration, mergers, and IP expansion remain central strategies for strengthening market presence and accelerating commercialization.

Evonik Industries: Integrating Silica and Silanes for Advanced Materials Solutions

Evonik maintains a dominant position in high-performance silica through its extensive precipitated and fumed silica portfolio and its expanded Smart Effects business line. The company announced in January 2025 the strategic merger of its Silica and Silanes divisions, allowing it to combine advanced particle design with molecular silane chemistry for high-functionality applications. Evonik is especially active in developing CO₂ capture adsorbents, leveraging mesoporous silica carriers modified with amino silanes. Its integrated business structure enhances its ability to serve emerging markets in green technologies, semiconductor coatings, and high-purity silica for lithium-ion batteries.

W. R. Grace & Co.: Engineering High-Performance Catalyst Supports and Adsorbents

W. R. Grace remains a global leader in engineered materials and catalyst carriers, with expertise in tailoring pore structures and surface chemistry for high-performance applications. The company supplies custom mesoporous silica materials suited for chromatography, refinery processes, and chemical purification. Its strength lies in mastering pore structure control, enabling catalytic materials with consistent reaction efficiency. Grace is heavily focused on batch-to-batch consistency and stringent quality control, serving tightly regulated industries such as pharmaceuticals, petrochemicals, and food processing.

Merck KGaA: Advancing High-Purity Mesoporous Silica for Life Science Applications

Merck is a major supplier of research-grade SBA-15 and MCM-41 mesoporous silica materials, widely used in drug formulation studies, chromatographic applications, and biopharmaceutical R&D. The company’s strong emphasis on drug-delivery systems, nanomedicine, and separation science positions it as a preferred partner for academic and industrial research labs. Merck’s broad portfolio in purification and chromatography allows it to integrate mesoporous silica into high-resolution filtration and bioseparation solutions, supporting the development of next-generation targeted therapeutics.

Taiyo Kogyo Corporation: Scaling Pharmaceutical-Grade Mesoporous Silica Manufacturing

Taiyo Kogyo specializes in pharmaceutical-grade silica excipients and custom-designed porous materials for drug formulation. Its expansion of the Osaka production facility in 2023, increasing capacity by 18%, reinforces its leadership in high-volume supply for oral solid dosage forms. The company’s proprietary synthesis and drying processes allow fine control over pore volume, particle morphology, and dissolution properties, making Taiyo Kogyo a major contributor to the pharmaceutical excipients market. Its mesoporous silica grades are widely used as flow aids, anti-caking agents, and stabilization carriers.

nanoComposix (Fortis Life Sciences): Precision Nanomaterials for Diagnostics and Research

nanoComposix, now operating under Fortis Life Sciences after its July 2021 acquisition, specializes in producing highly characterized mesoporous silica nanoparticles for diagnostics, imaging, and advanced biomedical research. Its expertise in achieving tight particle-size control (as precise as ±5 nm) and customizable surface chemistry makes it a top supplier for assay developers and research institutions. The brand continues to lead in high-value niche markets where reproducibility and nanoparticle precision are critical, including contrast agents, point-of-care diagnostics, and analytical kits.

Mesoporous Silica Market Report Scope

Mesoporous Silica market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$217 Million

|

|

Market Size (2035)

|

$578.4 Million

|

|

Market Growth Rate

|

10.3%

|

|

Segments

|

By Structure (MCM-41, SBA-15, MCM-48, Hollow Mesoporous Silica Nanoparticles, KCC-1/KIT-6, Others), By Pore Size (Ultra-Mesoporous, Large-Mesoporous, Macroporous/Hierarchical), By Application (Drug Delivery & Theranostics, Catalyst Supports, Adsorbents & Separation Media, Environmental Remediation, Coatings & Additives, Energy Storage Materials, Cosmetics & Personal Care), By End-User Industry (Pharmaceuticals & Biotechnology, Chemicals & Petrochemicals, Environmental & Water Treatment, Food & Beverage, Personal Care & Cosmetics, Automotive)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Evonik Industries, Merck KGaA, W. R. Grace & Co., BASF SE, Fuji Silysia Chemical, Taiyo Kagaku, AGC Chemicals, Solvay, PQ Corporation, Taiyo International, Mitsubishi Chemical, nanoComposix/Fortis Life Sciences, Anten Chemical, Tosoh Silica Corporation, Nanomakers

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Mesoporous Silica Market Segmentation

By Structure

- MCM-41

- SBA-15

- MCM-48

- Hollow Mesoporous Silica Nanoparticles

- KCC-1 and KIT-6

- Others

By Pore Size

- Ultra-Mesoporous (2–6 nm)

- Large-Mesoporous (6–50 nm)

- Macroporous / Hierarchical

By Application

- Drug Delivery and Theranostics

- Catalyst Supports

- Adsorbents & Separation Media

- Environmental Remediation

- Coatings and Additives

- Energy Storage Materials

- Cosmetics and Personal Care

By End-User Industry

- Pharmaceuticals & Biotechnology

- Chemicals & Petrochemicals

- Environmental & Water Treatment

- Food & Beverage

- Personal Care & Cosmetics

- Automotive

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Mesoporous Silica Market

- Evonik Industries

- Merck KGaA

- W. R. Grace & Co.

- BASF SE

- Fuji Silysia Chemical

- Taiyo Kagaku

- AGC Chemicals

- Solvay

- PQ Corporation

- Taiyo International

- Mitsubishi Chemical

- nanoComposix / Fortis Life Sciences

- Anten Chemical

- Tosoh Silica Corporation

- Nanomakers

*- List not Exhaustive

Research Coverage: Mesoporous Silica Market

This USDAnalytics report investigates the global Mesoporous Silica Market across its full technology, application, and end-user spectrum, mapping how engineered structures such as MCM-41, SBA-15, hollow mesoporous silica nanoparticles, and hierarchical frameworks are reshaping pharmaceuticals, catalysis, environmental remediation, energy storage, and personal care systems. It examines the latest breakthroughs in pore-size control, surface functionalization, and continuous-flow synthesis, while its analysis reviews strategic moves including mergers, capacity expansions, IP development, and government-backed nanotechnology funding. The study highlights performance benchmarks such as high drug-loading efficiencies, ultra-uniform pore distributions, and regenerable CO₂ sorbent capabilities, linking these material attributes to commercial use cases in drug delivery, DAC, smart agriculture, and advanced formulations. With deep coverage of structural variants, pore classes, application clusters, and vertical-specific adoption curves, this report is an essential resource for R&D leaders, business development teams, nanomaterials strategists, and investors seeking to understand where value will accrue in next-generation mesoporous silica platforms and how competitive positioning is evolving along the global supply chain.

Scope Highlights

- Segmentation:

By Structure – MCM-41, SBA-15, MCM-48, Hollow Mesoporous Silica Nanoparticles, KCC-1 and KIT-6, Others

By Pore Size – Ultra-Mesoporous (2–6 nm), Large-Mesoporous (6–50 nm), Macroporous / Hierarchical

By Application – Drug Delivery and Theranostics, Catalyst Supports, Adsorbents & Separation Media, Environmental Remediation, Coatings and Additives, Energy Storage Materials, Cosmetics and Personal Care

By End-User Industry – Pharmaceuticals & Biotechnology, Chemicals & Petrochemicals, Environmental & Water Treatment, Food & Beverage, Personal Care & Cosmetics, Automotive

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Time Horizon: Historic data from 2021 to 2024 with detailed market forecasts from 2025 to 2034.

- Company Coverage: Competitive profiling and strategic assessment of 15+ leading players, including innovators in mesoporous silica nanoparticles, catalyst supports, pharmaceutical excipients, and specialty nanomaterials.