Metal Finishing Chemicals Market 2025–2034: Cr(VI)-Free Plating, PFAS Regulation, and EV Battery Surface Technologies Driving $44.7 Billion Outlook at 6.2% CAGR

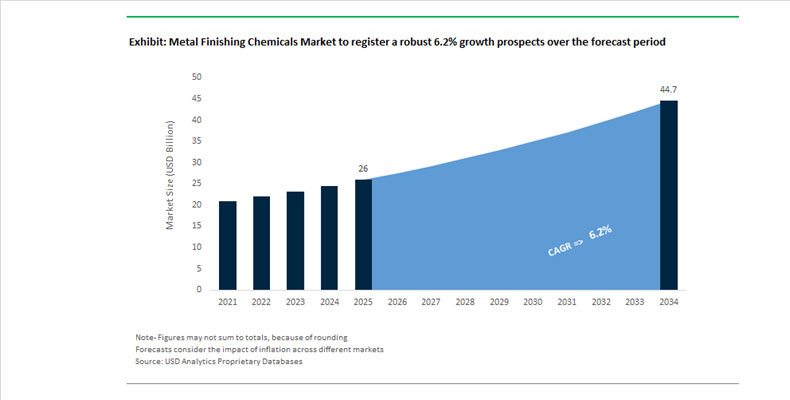

The Metal Finishing Chemicals Market is projected to expand from $26 billion in 2025 to $44.7 billion by 2034, registering a CAGR of 6.2%. Growth is being propelled by rising demand for advanced surface treatment chemicals, electroplating solutions, conversion coatings, passivation systems, and specialty cleaners across automotive, EV battery manufacturing, aerospace, electronics, and industrial fasteners. Increasing regulatory pressure to eliminate hexavalent chromium, PFAS-containing fume suppressants, and cyanide-based plating baths is accelerating innovation in trivalent chromium systems, non-cyanide silver plating, fluorine-free wetting agents, and energy-efficient bath chemistries. Simultaneously, OEMs are demanding improved corrosion resistance, conductivity, and lightweight compatibility for aluminum and high-strength steel components.

In January 2024, MacDermid Enthone acquired All-Star Chemical Company to strengthen its surface finishing footprint in the U.S. automotive and EV corridor. Effective January 1, 2024, SurTec integrated the bonded coatings business of OKS Spezialschmierstoffe, consolidating fastener-focused surface technologies. In April 2025, MacDermid Alpha commercialized EcoBond 3000, a non-cyanide, low-temperature silver plating solution targeting EV connectors and aerospace electrical systems while reducing hazardous waste and energy consumption. In May 2025, Chemetall deployed its Gardo SmartTrack cloud-based system across European OEM lines, enabling predictive bath maintenance and automated dosing to reduce chemical waste and enhance process stability. During the same month, Chemetall transitioned its Langelsheim production site to 100% renewable electricity, reducing indirect CO₂ emissions by approximately 620 tons annually. In September 2025, Azelis and Chemetall expanded their Southeast Asia distribution partnership, adding Thailand and the Philippines and announcing a new application lab in Vietnam to support aluminum finishing and automotive customers.

Regulatory shifts and strategic consolidation intensified through late 2025 and early 2026. In November 2025, the U.S. EPA proposed revised metal finishing effluent guidelines targeting PFAS discharges in chromium electroplating wastewater, accelerating development of fluorine-free process chemistries. Throughout 2025, MKS’ Atotech showcased next-generation zinc-nickel alloys and membrane technologies for EV battery housings and busbars at major battery expos. In November 2025, SurTec and Chem-Trend launched integrated aluminum die-casting process solutions combining release agents, cleaners, and passivations for automotive manufacturing. At the India Surface Finishing 2026 conference in February, Atotech highlighted Cr(VI)-free decorative chrome systems and non-PFAS coatings including Covertron 600 and the TriChrome family. In February 2026, Henkel announced a €2.1 billion agreement to acquire Stahl Group following its January 2026 acquisition of ATP Adhesive Systems, adding nearly €1 billion in annual sales and strengthening specialty coatings integration. In January 2026, BASF announced the opening of a global Digital Hub in Hyderabad to standardize digital services across business units, including surface treatment operations, advancing manufacturing digitalization and supply chain optimization within the global metal finishing chemicals value chain.

Metal Finishing Chemicals Market Trends and Opportunities

Trend: Accelerated Shift to Trivalent Chromium and Chrome-Free Pretreatment Technologies

The Metal Finishing Chemicals Market is entering a decisive regulatory inflection point as global authorities move from conditional authorization to outright restriction of hexavalent chromium. Classified as a proven carcinogen, Cr(VI) is no longer considered a manageable compliance risk but a material that must be structurally eliminated from automotive, aerospace, and industrial finishing processes. In June 2025, European Chemicals Agency initiated a six-month public consultation to restrict 13 hexavalent chromium compounds under REACH, a move expected to be adopted by 2027. Regulatory impact assessments indicate this action could prevent up to 17 tonnes of annual Cr(VI) releases and avoid as many as 195 cancer cases per year, fundamentally redefining acceptable surface treatment chemistries in Europe and influencing global supply chains.

Performance parity has emerged as the key enabler of adoption. In late 2024, MacDermid Enthone commercialized an advanced trivalent chromium passivation system for automotive components that delivers neutral salt spray resistance comparable to, and in some cases exceeding, legacy hexavalent systems. This breakthrough removes the last technical barrier for OEMs phasing out Cr(VI) in safety-critical applications such as braking and powertrain assemblies. While ECHA estimates the societal transition cost at €314 million to €3.23 billion, monetized health benefits of €331 million to €1.07 billion over 20 years provide a compelling macroeconomic rationale. As a result, zirconium- and titanium-based chrome-free pretreatments are rapidly becoming the default specification in new vehicle platforms and aerospace qualification programs.

Trend: Onshoring and Strategic Stockpiling of Critical Plating Chemistries

Geopolitical fragmentation and semiconductor industrial policy are reshaping sourcing strategies for metal finishing chemicals, particularly high-purity nickel, gold, palladium, and copper compounds used in electroplating. The CHIPS and Science Act era has accelerated the shift from just-in-time procurement to buffer inventory and localized production. In late 2024, the U.S. Department of Commerce awarded USD 1.5 billion in funding to GlobalFoundries, part of a broader USD 185 billion semiconductor capital cycle in 2025 that includes upstream investments in plating chemicals and process consumables required for wafer fabrication.

Supply-chain de-risking is now a board-level priority. Industry data released in November 2025 shows over 70% of semiconductor manufacturers have implemented dual sourcing strategies, while 60% are actively regionalizing chemical supply. Despite this, the U.S. still faces an estimated USD 9 billion gap in domestic specialty chemical capacity for front-end semiconductor manufacturing. Parallel momentum is visible in Asia. India raised its 2025 semiconductor budget by 83% to INR 7,000 crores, targeting USD 10 billion in fabrication investments. The launch of CG Semi’s OSAT facility in Gujarat in August 2025 exemplifies this push, with localized demand emerging for advanced plating additives and packaging chemistries that previously relied on imports.

Opportunity: High-Throw Plating Chemistry for 3D Semiconductor Packaging

The transition toward chiplets, Through-Silicon Vias, and High-Bandwidth Memory is creating a high-growth, high-margin opportunity for precision metal finishing chemicals. TSV architectures with aspect ratios exceeding 10:1 demand copper and nickel plating chemistries capable of void-free filling, uniform grain structure, and extreme throwing power. The commercialization of HBM3E and early HBM4 platforms in 2025 has accelerated the adoption of vertically stacked DRAM, making advanced electroplating additives a mission-critical input rather than a commoditized consumable.

China has already localized over 60% of its mainstream packaging toolchain capacity by 2024, intensifying competition on chemistry performance rather than cost. To support this demand, Moses Lake Industries opened a USD 100 million R&D facility in Arizona in 2025 focused on ultra-pure copper plating solutions. These formulations are designed to meet the stringent defect density requirements of nearby advanced packaging ecosystems anchored by TSMC and Amkor Technology, positioning high-throw plating chemistry as a strategic growth lever tied directly to AI and high-performance computing demand.

Opportunity: Closed-Loop Zero-Liquid-Discharge Systems for Metal Recovery

Environmental compliance in metal finishing is rapidly evolving from effluent minimization to full resource recovery. Stricter limits on PFAS and dissolved metals such as copper, nickel, and zinc are pushing wastewater treatment into the core process design. In October 2025, updated guidance linked to the U.S. EPA’s planned revision of Metal Finishing Effluent Limitation Guidelines signaled parts-per-trillion PFAS thresholds, with a formal rulemaking expected by mid-2026. This regulatory trajectory is transforming Zero-Liquid-Discharge systems from optional sustainability upgrades into permit-level requirements.

Water-stressed economies are leading adoption. In India, where industrial users operate under acute water scarcity, ZLD systems are now legally mandated for many chemical and textile facilities. These integrated systems enable up to 90% water reuse through thermal evaporation and crystallization, converting dissolved metals into recoverable solid residues. The 2025 technology frontier combines advanced membrane filtration with AI-driven predictive maintenance, reducing downtime and improving metal recovery yields. For metal finishing chemical suppliers, this creates a dual opportunity: supplying process-compatible chemistries optimized for closed-loop operation and participating in the monetization of recovered metals, effectively converting compliance spend into a circular value stream.

Metal Finishing Chemicals Market Share and Segmentation Insights

Plating Chemicals Lead Metal Finishing Chemicals Market with High Demand from Electroplating Processes

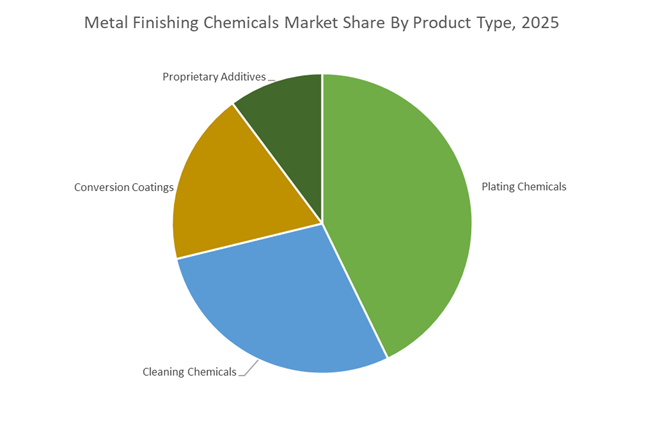

Plating chemicals accounted for 42.80% of the Metal Finishing Chemicals Market share in 2025, making them the largest product segment used in industrial surface treatment processes. These chemicals are essential in electroplating and electroless plating operations, where thin metallic coatings are deposited onto substrates to improve corrosion resistance, wear protection, electrical conductivity, and decorative appearance. Plating processes are widely applied in automotive components, electronic connectors, industrial machinery parts, and consumer goods, ensuring both functional performance and aesthetic quality. Common plating chemistries involve nickel, copper, chromium, zinc, and precious metal coatings, each providing specific surface properties required for different industrial applications. In 2025, regulatory pressure on hexavalent chromium compounds has significantly influenced plating chemistry development. Manufacturers are increasingly transitioning to trivalent chromium plating systems and alternative metal finishing technologies that maintain corrosion resistance and decorative quality while complying with environmental and occupational safety regulations in global manufacturing industries.

Automotive Sector Drives the Largest Demand for Metal Finishing Chemicals

Automotive applications accounted for 38.60% of the Metal Finishing Chemicals Market share in 2025, positioning the automotive manufacturing sector as the largest consumer of metal surface treatment solutions. Modern vehicles contain thousands of metal components requiring protective and decorative surface finishing, including fasteners, engine components, suspension parts, electrical connectors, trim elements, and structural assemblies. Metal finishing processes provide corrosion protection, improved mechanical durability, electrical conductivity, and enhanced appearance, which are essential for long-term vehicle reliability and product aesthetics. The large global production volume of passenger vehicles, commercial trucks, and specialty vehicles ensures continuous demand for plating and surface treatment chemicals across automotive supply chains. In 2025, the rapid transition toward electric vehicle (EV) manufacturing has introduced new requirements for metal finishing processes. EV platforms require specialized finishing solutions for battery housings, copper busbars, aluminum components, and electronic control systems, along with surface treatments that support electromagnetic interference (EMI) shielding and thermal management, expanding the role of advanced metal finishing chemistries in next-generation automotive production.

Metal Finishing Chemicals Market Competitive Landscape

The metal finishing chemicals market in 2026 is driven by Cr(VI) phase-out, trivalent chromium (Cr III) adoption, PFAS-free chemistries, and closed-loop plating systems. Advanced surface engineering, AI-driven bath monitoring, and ZLD technologies are enabling compliance while meeting EV, aerospace, and high-performance industrial standards.

Atotech leads closed-loop Cr III plating and PFAS-free systems for next-gen surface finishing

MKS Instruments (Atotech) is setting the benchmark in sustainable metal finishing through integrated chemical-equipment solutions and closed-loop chemistry. Its CMA (Compact Membrane Anode) systems enable near-zero liquid discharge (ZLD), significantly reducing wastewater and operational costs. The launch of Covertron® 600 enables fully Cr-free plating-on-plastics using trivalent chromium and PFAS-free agents, aligning with REACH mandates. Expansion in Spain and strong presence in India reinforce its regional service capabilities. Atotech’s non-PFAS zinc flake and phosphate-free technologies position it as a key enabler for EV and automotive surface finishing transformation.

MacDermid Enthone accelerates REACH-compliant Cr(VI)-free plating with recycled material systems

MacDermid Enthone (Element Solutions) is driving industry transition through its Sustainable Solutions roadmap focused on Cr(VI)-free decorative and functional plating. Its AluKlad Construct system supports recycled aluminum processing, delivering up to 95% energy savings, critical for EV and architectural applications. The NiKlad™ ECO MP process reduces nickel discharge through advanced ion control, addressing tightening environmental regulations. Innovations like CUPROSTAR 800 support high-density PCB manufacturing for 5G and AI applications. With strong emphasis on maintaining premium aesthetics and compliance, MacDermid is a leader in next-generation plating chemistries.

DuPont strengthens metal finishing through water treatment integration and high-performance bonding chemicals

DuPont is repositioning its metal finishing chemicals portfolio toward high-value industrial applications following its electronics business spin-off. Its investment in the Spruance facility enhances production of advanced materials requiring specialized metal-to-polymer bonding chemistries. The company’s leadership in ion-exchange resins and membrane technologies supports efficient recovery of metals and treatment of hazardous effluents in plating operations. With a focus on EBITDA margin expansion and operational efficiency, DuPont is aligning its finishing solutions with sustainability and circular water management. Its integration of water technologies provides a critical advantage in ZLD and regulatory compliance.

Quaker Houghton expands global plating footprint through acquisitions and EV-focused finishing solutions

Quaker Houghton is rapidly scaling its presence in metal finishing chemicals through strategic acquisitions, including Dipsol Chemicals, Natech, and CSI. These integrations enable a comprehensive portfolio spanning cleaning, conversion coating, and finishing solutions for EV battery trays and lightweight structures. The company’s expansion into Africa and Asia-Pacific strengthens its global footprint in high-growth industrial markets. Strong revenue growth reflects successful integration and new business wins. By offering single-source solutions, Quaker Houghton is enhancing operational efficiency for manufacturers while targeting high-performance, corrosion-resistant applications.

BASF Chemetall pioneers chrome-free pretreatment and low-energy thin-film technologies

BASF’s Chemetall division is leading sustainable surface treatment with its Oxsilan® thin-film technology, eliminating traditional phosphating while reducing sludge and energy consumption by up to 90%. Its transition to 100% renewable electricity at key production sites supports carbon-neutral manufacturing goals. Chemetall’s chrome-free primers and Naftoseal aerospace solutions align with strict 2026 aviation and REACH regulations. The company’s integration within BASF’s global Verbund network ensures scalability and innovation. With strong positioning in automotive and aerospace MRO, Chemetall is driving the shift toward eco-efficient, high-performance metal finishing systems.

Germany: Hybrid Coatings, Battery Compliance, and Circular Processing Leadership

Germany continues to set the technical and regulatory benchmark for the metal finishing chemicals market through material efficiency, circularity, and low-emission process design. In December 2025, Henkel expanded its Thin Organic Coating portfolio with new color variants, including a pilot golden finish tailored for coil-coating in construction applications. These TOC systems integrate passivation with organic polymers at film thicknesses of 1 to 2 microns, enabling corrosion protection with significantly reduced material consumption and downstream waste. This innovation aligns with demand from architectural steel and aluminum processors seeking thinner, multifunctional coatings without compromising durability.

Regulatory alignment is further reshaping formulation priorities. The EU Battery Regulation entering full effect from August 2025 is tightening registration and extended producer responsibility requirements across device, starter, and electric vehicle batteries. German finishing chemical suppliers are adapting surface treatments for battery housings and current collectors to meet traceability and recyclability criteria. Parallel pressure from Germany’s updated Packaging Act is accelerating investment in optical sorting and recovery systems capable of achieving metal residue recovery rates approaching 99.99% from mixed waste streams. Process-side efficiency is also advancing through low-temperature chemistry. German R&D teams successfully piloted the UniClean A101 system operating at 35 degrees Celsius, delivering effective oil degradation, extended bath life, and materially lower carbon emissions compared with conventional high-heat alkaline cleaners.

China: Recycled Metals, AI-Enabled Carbon Tracking, and Precision Plating

China’s metal finishing chemicals market is evolving under strong policy direction focused on non-ferrous metals, recycling, and digital oversight. The Ministry of Industry and Information Technology issued a 2025–2026 growth directive targeting 5% annual industrial value growth in non-ferrous metals, with emphasis on ultra-high purity materials and corrosion-resistant aluminum alloys for new energy vehicles and information technology hardware. These requirements are driving demand for advanced plating baths, brighteners, and inhibitors capable of delivering uniform finishes on high-spec aluminum substrates.

Secondary metal utilization is a central driver. China aims to lift annual production of recycled metals beyond 20 million metric tons by 2026, increasing the need for specialized purification chemicals, de-smutting agents, and stabilizers designed for variable scrap chemistries. Under the AI plus Non-Ferrous Metals initiative launched in 2025, producers are deploying digital models to track carbon intensity from smelting through chemical finishing, integrating emissions accounting directly into surface treatment workflows. Capacity expansion by global suppliers such as Arkema and Nouryon at the Nansha site is reinforcing China’s role as a hub for high-precision plating chemicals used in integrated circuits and emerging humanoid robotics supply chains.

India: Energy-Efficient Pretreatment and Domestic Plating Ecosystems

India’s metal finishing chemicals market is being reshaped by fiscal reform, mineral security initiatives, and rapid adoption of energy-efficient surface treatments. Under GST 2.0 Green Growth reforms in 2025, the reduction of tax rates on effluent treatment plants and renewable energy equipment from 12% to 5% has materially improved the return on investment for advanced wastewater management and zero-liquid-discharge chemical systems. This policy has accelerated uptake of closed-loop pretreatment and rinsing chemistries among automotive and industrial finishers.

Resource strategy is also influencing formulation demand. The National Critical Mineral Mission launched in 2025 focuses on securing domestic supplies of nickel, cobalt, and lithium, directly supporting local production of zinc-nickel plating chemicals required for corrosion-resistant automotive components destined for export markets. Technology adoption is accelerating through industry platforms. At Surface and Coating Expo 2025 in Chennai, Compact Membrane Anodes were introduced for alkaline zinc-nickel electroplating, significantly reducing waste generation and chemical drag-out. In parallel, Indian automotive corridors are rapidly replacing iron phosphate pretreatments with zirconium-based conversion coatings, cutting energy consumption in paint shops while maintaining adhesion and corrosion resistance.

United States: Aerospace-Led Innovation and Safer Chemistry Transition

The United States metal finishing chemicals market is being driven by aerospace lightweighting, advanced materials, and regulatory pressure toward safer chemistries. In 2025, MacDermid Enthone launched evolve Chrome-Free Etch, a sustainable alternative to PFAS-containing hexavalent chromium systems. This technology enables reliable plating on high-performance engineered plastics such as PEEK and ULTEM used in 3D-printed aerospace components, delivering weight reductions that translate into significant lifecycle fuel savings.

Electromagnetic interference shielding remains another high-value application. U.S. suppliers are advancing mid-phosphorus electroless nickel systems that protect composite connectors against lightning strikes up to 200 kiloamperes while preserving structural integrity under extreme conditions. Regulatory momentum is reinforcing reformulation. The EPA Safer Choice expansion expected through 2026 is pushing finishing laboratories to replace hard-chelating agents with biodegradable alternatives such as GLDA and MGDA in industrial cleaning and pretreatment formulations. This transition is positioning U.S. suppliers toward compliant, aerospace-grade, and environmentally aligned finishing chemistries.

Country-Level Strategic Positioning in the Metal Finishing Chemicals Market

Metal Finishing Chemicals Market County Level Snapshot

|

Country

|

Strategic Focus

|

Key Technology or Chemistry

|

Regulatory or Policy Driver

|

Competitive Differentiation

|

|

Germany

|

Hybrid coatings and circular processing

|

Thin Organic Coatings, low-temp cleaners

|

EU Battery Regulation, Packaging Act

|

Material efficiency and recycling leadership

|

|

China

|

Recycled metals and digital control

|

De-smutting agents, AI-tracked finishing

|

MIIT non-ferrous growth plan

|

Scale with carbon transparency

|

|

India

|

Energy-efficient pretreatment

|

Zirconium conversion, zinc-nickel plating

|

GST reforms, Critical Mineral Mission

|

Cost-efficient sustainability adoption

|

|

United States

|

Aerospace and safer chemistries

|

Chrome-free etch, electroless nickel

|

EPA Safer Choice expansion

|

High-performance regulatory compliance

|

Metal Finishing Chemicals Market Report Scope

Metal Finishing Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$26 Billion

|

|

Market Size (2034)

|

$44.7 Billion

|

|

Market Growth Rate

|

6.2%

|

|

Segments

|

By Product Type (Plating Chemicals, Cleaning Chemicals, Conversion Coatings, Proprietary Additives), By Process (Electroplating, Electroless Plating, Chemical Conversion, Anodizing and Electropolishing), By Material Substrate (Steel and Iron, Aluminum and Light Alloys, Copper and Brass, Plastics and Composites), By End-Use Industry (Automotive, Electrical and Electronics, Aerospace and Defense, Industrial Machinery, Construction)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Atotech, MacDermid Enthone, Henkel, BASF, Dow, DuPont, Quaker Houghton, Nippon Paint Holdings, Uyemura, Grauer and Weil, Elementis, NOF Corporation, Technic

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Metal Finishing Chemicals Market Segmentation

By Product Type

- Plating Chemicals

- Cleaning Chemicals

- Conversion Coatings

- Proprietary Additives

By Process

- Electroplating

- Electroless Plating

- Chemical Conversion

- Anodizing and Electropolishing

By Material Substrate

- Steel and Iron

- Aluminum and Light Alloys

- Copper and Brass

- Plastics and Composites

By End-Use Industry

- Automotive

- Electrical and Electronics

- Aerospace and Defense

- Industrial Machinery

- Construction

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Metal Finishing Chemicals Market

- Atotech

- MacDermid Enthone

- Henkel

- BASF

- Dow

- DuPont

- Quaker Houghton

- Nippon Paint Holdings

- Uyemura

- Grauer and Weil

- Elementis

- NOF Corporation

- Technic

*- List not Exhaustive