Surface Treatment Chemicals Market 2025–2034: $16.6 Billion to $34.6 Billion at 8.5% CAGR Driven by EV Battery Coatings, Low-Temperature Degreasing, and Aerospace-Grade Surface Technologies

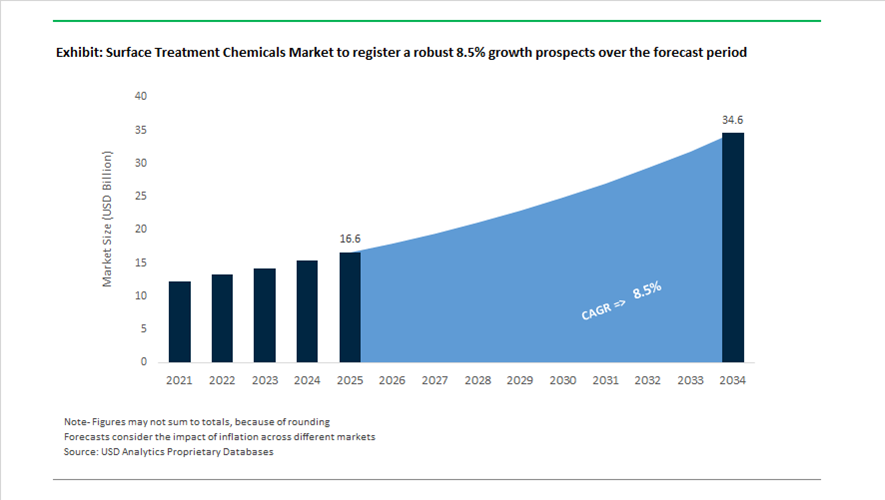

The global surface treatment chemicals market is valued at $16.6 billion in 2025 and is projected to reach $34.6 billion by 2034, expanding at a CAGR of 8.5%. Growth is being driven by rising demand for corrosion protection chemicals, metal pretreatment solutions, passivation coatings, electroplating chemistries, anodizing agents, industrial degreasers, and advanced functional coatings across automotive, EV battery manufacturing, aerospace, industrial MRO, and electronics sectors. Regulatory pressure around chromium-free technologies, fluorine-free passivation, low-VOC formulations, and energy-efficient cleaning processes is reshaping product portfolios. Manufacturers are increasingly adopting low-temperature surfactants, renewable energy-powered production, and carbon-optimized coating platforms to align with global decarbonization mandates and advanced materials performance requirements.

Strategic acquisitions and portfolio consolidation accelerated in 2025. In April 2025, Quaker Houghton completed the acquisition of Dipsol Chemicals for approximately $155 million, integrating advanced plating and metal surface treatment technologies into its global metalworking fluids platform. In May 2025, Chemetall transitioned its Langelsheim, Germany facility to 100% renewable electricity, strengthening BASF’s decarbonization roadmap and supporting the production of corrosion protection agents and aerospace sealants. In September 2025, Chemetall received the Airbus SQIP 2025 Award for the tenth consecutive year, reinforcing its leadership in aerospace-grade surface treatment solutions. In October 2025, Chemetall introduced Gardolene D, a chromium- and fluoride-free passivation technology for copper foils used in EV batteries. The solution enhances battery lifespan by up to 6% and aligns with the EU 2023/1542 Battery Regulation scheduled for enforcement in 2027. In November 2025, Oerlikon Balzers unveiled the INSPIRA carbon platform integrating S3p coating technology, improving wear resistance and productivity for precision tools and industrial components.

Transformation intensified in early 2026 with large-scale structural moves and process innovations. In February 2026, Henkel announced a €2.1 billion agreement to acquire Stahl Group, adding approximately €725 million in annual sales and significantly expanding its specialty surface treatment and flexible substrate coatings portfolio for automotive and packaging applications. In February 2026, Henkel launched Bonderite C-AD 20202, a low-temperature dip degreaser operating at 35–40°C, enabling manufacturers to reduce energy consumption by up to 35% compared to conventional 65°C cleaning systems. In November 2025, Solvay initiated a €25 million investment to convert its Bad Wimpfen site into a global Nocolok Paste & Paint hub, discontinuing legacy TFA production by early 2026 to prioritize automotive brazing surface technologies. In January 2026, Oerlikon finalized the divestment of Barmag to sharpen its focus as a pure-play surface technologies provider, while simultaneously strengthening its Michigan operations for future aerospace and energy demand expansion. In January 2026, Nippon Paint positioned its MRO segment as a strategic growth engine, emphasizing industrial surface treatment chemicals for renovation and infrastructure durability. These mergers, renewable energy transitions, chromium-free EV chemistries, and low-temperature process innovations are structurally reinforcing high-value growth across the surface treatment chemicals market through 2034.

Structural Trends and High-Value Opportunities in the Surface Treatment Chemicals Market

Mandatory Transition to Trivalent Chromium and Zirconium-Based Pretreatments

Global environmental regulation has moved decisively from guidance to enforcement, making the elimination of hexavalent chromium a non-negotiable requirement across automotive, industrial equipment, and coated metals supply chains. EU REACH restrictions and the End-of-Life Vehicles Directive are forcing OEMs and Tier 1 suppliers to re-engineer pretreatment lines around trivalent chromium and zirconium-oxide conversion coatings that eliminate carcinogenic exposure while simplifying wastewater management.

OEM-led directives are accelerating this transition. In February 2025, ZF Lifetech confirmed upgrades to its galvanizing operations using advanced Cr3+ technologies, reflecting a broader push by global automakers to align surface treatment processes with Cradle to Cradle Certified material health criteria. These requirements are now embedded in long-term sourcing contracts, effectively locking in compliant chemistries across multi-plant footprints.

From an operational standpoint, zirconium-based thin-film systems have emerged as the preferred alternative to zinc phosphating. Ambient-temperature operation reduces energy consumption by up to 30%, while near-zero sludge generation cuts hazardous waste disposal costs by 20 to 40% annually. Commercial platforms such as BONDERITE and Oxsilan, developed by Henkel and Chemetall respectively, illustrate how compliance-driven reformulation is simultaneously delivering measurable cost and sustainability advantages, reinforcing the long-term viability of these chemistries.

Convergence of Dry Surface Treatments and Integrated Chemical Service Models

The increasing use of lightweight composites, advanced polymers, and high-value electronics is exposing the limitations of conventional wet chemical etching. In response, manufacturers are adopting atmospheric plasma and laser ablation technologies to activate surfaces without liquid chemicals, reshaping the surface treatment chemicals market toward integrated equipment-plus-chemistry service offerings.

Capital investment in plasma surface treatment systems accelerated through 2025, with Europe leading adoption at a 6.3% regional growth rate. These systems now represent over a quarter of surface treatment applications in semiconductor and electronics manufacturing, where atomically clean, contamination-free surfaces are essential for yield control. The shift reflects a structural change, not a niche trend, as dry pretreatments become standard in high-reliability production environments.

Sustainability metrics are reinforcing adoption. Industry briefings released in January 2025 highlighted that dry pretreatment workflows can reduce Chemical Oxygen Demand in effluent streams by as much as 80% by eliminating secondary cleaning stages. This has catalyzed the rise of outcome-based service contracts in which providers such as MacDermid Enventure manage plasma activation, chemistry selection, and performance monitoring as a single responsibility. For customers, this model reduces regulatory risk and capital burden, while for suppliers it creates sticky, higher-margin recurring revenue streams.

All-in-One Conversion Coatings for Multi-Metal EV Battery Enclosures

The shift to 800V electric vehicle architectures is driving a redesign of battery enclosures that increasingly combine aluminum, galvanized steel, copper, and magnesium. Preventing galvanic corrosion across these dissimilar substrates has created a high-margin opportunity for single-step, multi-metal conversion coatings that simplify production while meeting aggressive durability standards.

Advanced passivation technologies are moving rapidly from pilot to production. In October 2025, BASF, through its Chemetall portfolio, launched Gardolene D, a chromium- and fluoride-free passivation solution for copper foils used in EV battery packs. Beyond corrosion protection, the chemistry improves surface energy for anode adhesion and has been shown to extend battery life by up to 6% after 1,000 charge cycles, linking surface treatment directly to cell performance and warranty economics.

Performance requirements for these coatings continue to rise. Systems introduced in mid-2025 by MKS Atotech and Axalta are engineered to pass ASTM G85 A5 cyclic corrosion testing for more than 120 cycles while delivering dielectric strengths up to 6 kV. As OEMs push toward standardized global battery platforms, suppliers capable of delivering robust, multi-metal pretreatments at scale are positioned to capture disproportionate value.

High-Performance Bio-Based Cleaners for Precision Manufacturing

Regulatory bans on chlorinated solvents such as trichloroethylene and n-propyl bromide are creating a structural gap in precision cleaning applications across aerospace, medical devices, and high-end machining. This has opened a significant opportunity for bio-based aqueous cleaners derived from plant oils and terpenes that can remove synthetic lubricants without residue or substrate damage.

Green chemistry adoption accelerated in 2025 with multiple commercial launches. USDA-certified formulations such as Renewable Lubricants’ GreenStrip Bio and aerospace-focused solutions like AQUANOX A4615 from Kyzen Corporation are gaining qualification for titanium composites and aluminum-lithium alloys used in next-generation aircraft. These products demonstrate that bio-based systems can meet stringent cleanliness and corrosion requirements previously associated only with solvent-based cleaners.

Precision requirements are driving volume as well as value. In commercial aviation maintenance, wide-body aircraft checks can consume 150 to 200 liters of specialized cleaners per event, with more than 40,000 heavy maintenance checks conducted annually worldwide. As operators transition to sustainable, pH-balanced formulations to maintain regulatory compliance and worker safety, bio-based surface treatment cleaners are evolving from niche alternatives into a multi-billion dollar growth engine within the surface treatment chemicals market.

Surface Treatment Chemicals Market Share and Segmentation Insights

Cleaners and Degreasers Lead Due to Critical Role in Surface Preparation Across Industries

Cleaners and degreasers accounted for 32.80% of the surface treatment chemicals market in 2025, reflecting their essential role in surface preparation processes across metals, plastics, and electronic substrates. These chemicals remove oils, greases, oxides, and contaminants, enabling effective adhesion of coatings, plating, and conversion layers. Their widespread use across automotive, aerospace, industrial manufacturing, and electronics drives high-volume consumption. The 2025 trend centers on the shift toward aqueous cleaning systems, where advanced surfactant formulations, controlled pH systems, and environmentally compliant chemistries replace solvent-based cleaners, balancing cleaning efficiency with regulatory compliance and worker safety requirements.

Corrosion Protection Drives High Consumption of Surface Treatment Chemicals Across Industrial Applications

Corrosion protection accounted for 38.60% of surface treatment chemicals market demand in 2025, making it the dominant application due to the critical need to extend the lifespan of metal components and infrastructure. Technologies including conversion coatings, plating systems, and corrosion inhibitors are widely used across automotive, construction, aerospace, and industrial sectors. Increasing complexity in material usage has intensified demand for advanced solutions. The 2025 market trend focuses on multi-metal corrosion protection systems, where treatment chemistries are designed to protect steel, aluminum, magnesium, and composite assemblies simultaneously, ensuring compatibility with coatings while minimizing galvanic corrosion risks in modern engineered systems.

Surface Treatment Chemicals Market Competitive Landscape

The surface treatment chemicals market in 2026 is defined by operational decarbonization, low-PCF formulations, and digital transparency tools. Competition centers on EV battery coatings, aerospace-grade corrosion protection, and electronics manufacturing, with localized production hubs and IoT-enabled performance monitoring driving next-generation surface engineering solutions.

Henkel Expands Digital PCF Modeling and Electronics-Focused Surface Solutions Through Bengaluru Innovation Hub

Henkel is leading the surface treatment chemicals market through its "Purposeful Growth" strategy, combining sustainability with digital innovation. Its Adhesive Technologies division generated €10.67 billion in 2025, driven by mobility and electronics demand. The expanded HEART platform now enables use-phase emission modeling, helping customers reduce energy consumption by up to 75%. The Bengaluru Customer Application Center supports co-development of thermal management and advanced surface solutions for electronics manufacturing. Henkel has audited its entire portfolio against Responsible Chemistry standards, ensuring compliance with global ESG regulations. Its integration of digital tools and sustainable chemistries strengthens its leadership in high-value industrial coatings.

BASF Chemetall Leads EV Battery and Aerospace Surface Treatments with Chromium-Free Technologies

BASF’s Chemetall division is setting industry benchmarks in aerospace coatings and EV battery surface treatment chemicals. The company received the Airbus SQIP Award for the tenth consecutive year, highlighting its leadership in corrosion protection technologies like Naftoseal® and Ardrox®. Its Gardolene® D platform introduces chromium- and fluoride-free passivation for copper foils, critical for EV battery efficiency and regulatory compliance. BASF is expanding its Southeast Asian footprint through Azelis partnerships and a new Ho Chi Minh City lab for localized testing. Its integration into the broader Green Transformation strategy focuses on reducing CO2 emissions across production sites. Chemetall’s advanced coatings support high-performance, low-PCF industrial applications.

PPG Delivers High-Durability Powder Coatings and Low-VOC Primers for Infrastructure and Marine Applications

PPG is advancing surface treatment technologies through durable powder coatings and sustainable water-based primers. Its Coraflon® Platinum coatings demonstrate 20x superior color retention over five years, ensuring long-term performance in architectural applications. The AQUACRON® WSP shop primer, launched in 2026, provides rapid drying and corrosion resistance for structural steel. PPG’s innovation strategy focuses on low-VOC, all-in-one coating systems that combine adhesion, protection, and sustainability. Its electrostatic application technology enhances transfer efficiency and reduces chemical waste in marine coatings. With over 200 dry docking projects completed, PPG maintains strong leadership in industrial and infrastructure coatings.

Quaker Houghton Expands Metalworking and Plating Solutions Through Strategic Acquisitions and Asia Growth

Quaker Houghton is strengthening its position in industrial surface treatment chemicals through targeted acquisitions and portfolio diversification. The $155 million acquisition of Dipsol Chemicals, along with Natech and CSI, enhances its plating and advanced solutions capabilities. The company reported Q4 2025 sales of $468.5 million, with Asia-Pacific volumes growing by 8% due to demand from electronics and automotive sectors. Its restructuring plan targets $20 million in cost savings by 2026, enabling reinvestment into R&D. Quaker Houghton’s ESG performance has been recognized for three consecutive years, reinforcing its sustainability credentials. Its integrated process fluids and surface treatment solutions support high-efficiency manufacturing systems.

SurTec Drives PFAS-Free Electroplating and Trivalent Chromium Technologies for EV and Fastener Applications

SurTec is leading innovation in environmentally compliant surface treatment chemicals, focusing on PFAS-free and trivalent chromium technologies. Its Precote® 85 PFAS-free solution addresses regulatory requirements for EV fasteners and automotive components. Collaboration with AVL enables early-stage integration of surface engineering into EV system design. The SurTec 717 Zn/Ni process delivers high deposition rates and stable long-cycle performance using advanced membrane anode technology. Its SurTec 883 XT trivalent chromium solution replicates hexavalent aesthetics while meeting EU REACH standards. SurTec’s specialization in electroplating and functional coatings positions it as a key supplier in automotive and industrial value chains.

China Surface Treatment Chemicals Market Anchored in Localization and Advanced Application Methods

China’s surface treatment chemicals industry is being reshaped by coordinated industrial policy and accelerated downstream sophistication. Under the Petrochemical and Chemical Industry Growth Plan for 2025–2026, seven ministries led by the Ministry of Industry and Information Technology established a clear mandate to prioritize high-end specialty surfactants, dispersants, and adhesives used in surface activation. This policy framework has shifted capital allocation away from bulk chemistries toward precision surface treatment formulations for automotive coatings, electronics, and engineered substrates. A concrete manifestation of this shift was the commissioning of a high-performance dispersant line by BASF at the Jiangbei New Material Technology Park in Nanjing in November 2025, using Controlled Free Radical Polymerization technology to support demanding industrial and automotive coating systems.

Semiconductor and sustainability requirements are reinforcing this structural upgrade. Beijing’s 2026 Supply Chain Resilience mandate targets domestic self-sufficiency of over 90% for semiconductor-grade surface cleaning chemicals, intensifying demand for ultra-pure etchants, cleaners, and plating additives compatible with advanced packaging. Fabrication hubs are increasingly aligning with Japanese-led JOINT3 standards for 2.1D and 3D panel-level packaging, which require highly controlled chemical etching and metallization chemistries. In parallel, new environmental mandates in the Pearl River Delta are subsidizing closed-loop zero-liquid discharge systems, accelerating the replacement of legacy phosphorus-based degreasers with advanced phosphorus-free alternatives. Emerging use cases such as drone-applied heat-shielding surface treatments further illustrate how application innovation is lowering labor intensity while expanding the functional scope of surface treatment chemicals.

United States Surface Treatment Chemicals Market Driven by Semiconductor Purity and Integrated Finishing Systems

In the United States, surface treatment chemicals demand is increasingly tied to semiconductor reshoring and advanced manufacturing integration. Funding cycles under the CHIPS and Science Act in 2025 have catalyzed domestic production of ultra-high-purity phosphoric acid and specialty solvents required for 2nm wafer-level cleaning, elevating purity standards to 99.999%. At the same time, sustainability considerations are shaping formulation strategies. BASF announced that its Cincinnati Alkyl Polyglucosides production line is scheduled for full start-up in 2026, positioning bio-based surfactants as core inputs for green-tier industrial surface cleaning across manufacturing and maintenance environments.

Regulatory convergence with Europe is also influencing U.S. practices. Aerospace supply chains are proactively transitioning away from DMAC and NEP solvents in surface primers ahead of the EU REACH prohibition deadline, driving demand for compliant alternative cleaners and pretreatment chemistries. On the integration front, Tyrolit’s post-acquisition synergy with Acme Holding has expanded the availability of combined chemical-mechanical polishing solutions for the electric vehicle market, while 3M introduced re-engineered Cubitron technology designed to work in tandem with specialized cooling and anti-loading chemical treatments. This convergence of abrasives and surface chemistry underscores a broader U.S. trend toward system-level performance optimization rather than standalone chemical supply.

India Surface Treatment Chemicals Market Accelerated by Automotive, Pharma, and Steel Localization

India’s surface treatment chemicals sector is benefiting from policy-driven localization across multiple industrial verticals. Henkel’s completion of Phase III at its LEED Gold Kurkumbh facility has positioned the site as a central hub for supplying high-performance surface treatment products to the automotive maintenance and overhaul ecosystem. This aligns with the Production Linked Incentive framework for advanced automotive technology, which by mid-2025 had catalyzed significant investment into localized manufacturing of components that require corrosion protection, chemical conversion coatings, and advanced pretreatments.

Pharmaceutical and infrastructure developments are creating additional demand layers. The government’s bulk drug park initiative has generated a secondary market for pharmaceutical-grade stainless steel passivation chemicals, essential for preventing cross-contamination in active ingredient reactors. Concurrently, India’s push under PLI 2.0 for specialty steel is driving localized development of zinc-rich primers and phosphate-based surface treatments for high-strength infrastructure components. These trends collectively indicate a transition from import dependence toward domestically engineered surface treatment chemistries tailored to Indian operating conditions.

Germany Surface Treatment Chemicals Market Shaped by REACH Simplification and PFAS Substitution

Germany remains a regulatory bellwether for surface treatment chemicals in Europe, with the upcoming Chemicals Industry Package introducing targeted revisions to REACH in 2025–2026. These revisions aim to simplify authorization for surface treatment chemicals deemed essential for green technologies, offering regulatory clarity for suppliers serving renewable energy, electrification, and lightweight mobility sectors. At the same time, German industry associations have issued detailed transition guidelines to navigate impending PFAS restrictions, accelerating the shift toward fluorine-free coatings for heat-exposed automotive components.

Industrial leadership is evident in bio-based and chromium-free solutions. BASF’s Düsseldorf care chemicals hub continues to supply the European market with bio-based degreasers aligned with the Clean Industrial Deal objectives. German automotive manufacturers have also finalized the phase-out of hexavalent chromium for 2026 model-year components, completing the transition to trivalent and chromium-free passivation systems. These shifts are reinforcing Germany’s position as a reference market for compliant, high-performance surface treatment technologies.

Japan Surface Treatment Chemicals Market Focused on Semiconductor Packaging and Functional Coatings

Japan’s surface treatment chemicals industry is closely linked to its advanced electronics and materials ecosystem. The Resonac-led JOINT3 consortium, launched in 2025, is developing next-generation panel-level semiconductor packaging at the Advanced Panel Level Interposer Center, which is expected to begin full operations in 2026. This initiative is driving demand for highly specialized chemical etching and surface preparation chemistries capable of meeting stringent dimensional and reliability requirements.

Beyond electronics, application-driven innovation is expanding into agriculture and public health. Nippon Paint Group’s participation in the Aichi Prefectural initiative to develop light-transmitting, heat-shielding coatings highlights the growing role of surface treatments in climate-resilient agriculture, with drone-applicable formulations targeted for greenhouse deployment. In parallel, the Tokyo Innovation Center established by Nippon Paint Holdings has become a focal point for antiviral and antibacterial surface treatment research, reinforcing Japan’s emphasis on multifunctional, high-value surface chemistries.

Comparative Snapshot: Surface Treatment Chemicals Industry by Country

Surface Treatment Chemicals Market County Level Snapshot

|

Country

|

Primary Policy Driver

|

Key Application Focus

|

Structural Differentiator

|

|

China

|

MIIT growth plan and localization mandates

|

Semiconductors, automotive coatings, drone application

|

Scale plus rapid adoption of advanced application methods

|

|

United States

|

CHIPS Act and sustainability transition

|

Semiconductor cleaning, EV polishing systems

|

Integrated chemical-mechanical solutions

|

|

India

|

PLI schemes and industrial localization

|

Automotive MRO, pharma reactors, specialty steel

|

Demand diversification across sectors

|

|

Germany

|

REACH revision and PFAS restrictions

|

Green tech and automotive compliance

|

Regulatory leadership and bio-based substitution

|

|

Japan

|

JOINT3 semiconductor initiative

|

Advanced packaging and functional coatings

|

Precision chemistry tied to electronics leadership

|

Surface Treatment Chemicals Market Report Scope

Surface Treatment Chemicals Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$16.6 Billion

|

|

Market Size (2034)

|

$34.6 Billion

|

|

Market Growth Rate

|

8.5%

|

|

Segments

|

By Chemical Type (Cleaners and Degreasers, Conversion Coatings, Plating Chemicals, Corrosion Inhibitors, Adhesion Promoters, Etchants and Desmutters), By Base Material (Metals, Plastics and Polymers, Wood and Composites, Electronic Substrates), By Application (Corrosion Protection, Decorative and Aesthetic Finishing, Functional and Performance Enhancement, Adhesion Promotion, Semiconductor Fabrication)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, BASF SE, PPG Industries, Inc., Nippon Paint Holdings Co., Ltd., Oerlikon Balzers, Sherwin-Williams Company, Quaker Houghton, Atotech, Nihon Parkerizing Co., Ltd., A Brite Company, Inc., Elementis PLC, Resonac Holdings Corporation, Solvay S.A., Kansai Paint Co., Ltd., Akzo Nobel N.V.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Surface Treatment Chemicals Market Segmentation

By Chemical Type

- Cleaners and Degreasers

- Conversion Coatings

- Plating Chemicals

- Corrosion Inhibitors

- Adhesion Promoters

- Etchants and Desmutters

By Base Material

- Metals

- Plastics and Polymers

- Wood and Composites

- Electronic Substrates

By Application

- Corrosion Protection

- Decorative and Aesthetic Finishing

- Functional and Performance Enhancement

- Adhesion Promotion

- Semiconductor Fabrication

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Surface Treatment Chemicals Industry

- Henkel AG & Co. KGaA

- BASF SE

- PPG Industries, Inc.

- Nippon Paint Holdings Co., Ltd.

- Oerlikon Balzers

- Sherwin-Williams Company

- Quaker Houghton

- Atotech

- Nihon Parkerizing Co., Ltd.

- A Brite Company, Inc.

- Elementis PLC

- Resonac Holdings Corporation

- Solvay S.A.

- Kansai Paint Co., Ltd.

- Akzo Nobel N.V.

*- List not Exhaustive