MOFs Market Overview: Scale-Up, Decarbonization Use-Cases, and Commercialization Pathways

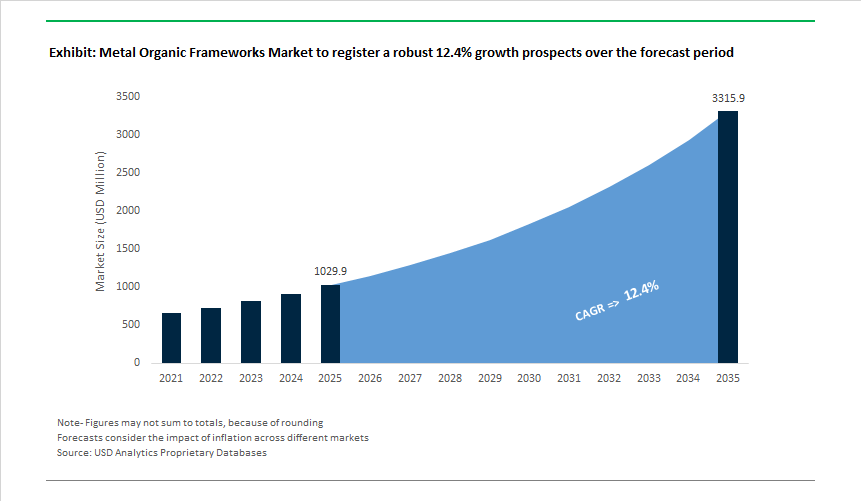

The Global Metal Organic Frameworks (MOFs) Market is valued at USD 1.03 billion in 2025 and is projected to reach USD 3.31 billion by 2035, expanding at a 12.4% CAGR as MOFs transition from a predominantly research-driven materials class into commercially deployable industrial platforms. The market’s momentum is no longer anchored in laboratory novelty; it is being driven by clear economic use cases in decarbonization, resource efficiency, and precision healthcare-areas where incremental performance gains translate directly into operating cost savings or regulatory compliance.

At a strategic level, MOFs are gaining relevance because they address structural inefficiencies in existing industrial processes. Energy-intensive separations, carbon capture systems with high regeneration costs, and bulky adsorption technologies are becoming increasingly misaligned with climate targets and cost pressures. MOFs offer a fundamentally different value proposition: higher selectivity, lower energy penalties, and smaller system footprints, enabling operators to redesign processes rather than optimize legacy ones. This shift is particularly attractive in sectors such as industrial gas separation, hydrogen infrastructure, and chemical processing, where energy costs and emissions exposure are rising simultaneously.

The strongest near-term commercial pull comes from decarbonization and gas separation. Industrial emitters and infrastructure operators are under pressure to reduce CO₂ intensity without sacrificing throughput or reliability. MOF-based systems are increasingly viewed as next-generation sorbents that can reduce capture energy demand and improve process economics at point sources. Importantly, these applications are supported by long-duration policy frameworks and capital programs, creating demand visibility that is rare for emerging materials.

A second growth engine is resource access and environmental resilience, particularly in water and air management. Atmospheric water harvesting, VOC control, and air purification are moving from pilot projects to deployment in infrastructure, defense, and remote industrial settings. These applications favor materials that deliver high performance per unit mass and modular deployment, making MOFs attractive for decentralized solutions where traditional infrastructure is impractical.

Healthcare and life sciences provide a third, higher-margin-but more selective-growth pathway. In drug delivery and diagnostics, MOFs are being evaluated as functional carriers rather than bulk materials, supporting controlled release, higher payload efficiency, and improved targeting. While volumes are smaller, qualification barriers and regulatory lock-in create defensible, long-term revenue streams once adoption occurs.

Market Analysis: Commercial Scaling, Flexible MOF Technologies, and Global Decarbonization Projects

Industry developments reveal a decisive pivot toward commercialization, scale, and integration of MOFs in high-impact decarbonization and separation technologies. The market gained strong momentum in November 2024, when NuMat Technologies announced the development of the world’s first industrial-scale MOF manufacturing facility in Chicago, enabling structured MOF-based solutions for specialty gas purification and carbon capture. This scaling trend intensified as May 2025 saw Svante inaugurate a dedicated Carbon Capture Gigafactory in North America to produce structured adsorbent filters-widely recognized as leveraging MOF-enabled sorbent technologies. These milestones indicate that MOFs have entered a phase of industrial readiness rather than academic novelty.

Parallel R&D advancements strengthened this commercial trajectory. In February 2025, a Horizon Europe-funded consortium published groundbreaking work on a flexible MOF (F-MOF) capable of dynamically adjusting pore size during pressure swing operations, potentially reducing propylene/propane separation energy costs by 15%-a major efficiency gain for petrochemical processors. Similarly, in September 2024, KAUST researchers demonstrated a titanium-based photocatalyst MOF that achieved 2.5× higher hydrogen production efficiency under visible light versus TiO₂, showing strong promise for hydrogen generation. Other breakthroughs emerged across applications: April 2024 pilot trials by UniSieve showcased MOF-based membranes achieving 99.5%+ hydrocarbon separation, while March 2024 DOE funding accelerated MOF-derived solid-state electrolyte research for next-gen Li-ion batteries.

Commercial product diversification also expanded significantly. June 2024 saw CD Bioparticles launch new iron-, nickel-, and titanium-based MOFs to support catalysis and biomedical innovation. On the other hand, March 2025 saw Promethean Particles invest heavily in equipment to shift from batch to continuous MOF manufacturing-addressing one of the industry’s largest historical bottlenecks: scalability.

Metal Organic Frameworks Market Trends and Opportunities

Trend 1: Commercial Pilot-Scale MOF-Based Systems for Hydrogen Storage

The hydrogen economy is moving beyond high-pressure compression toward MOF-enabled solid-state storage systems that prioritize safety, energy efficiency, and volumetric optimization. In 2025, this transition crossed a critical threshold as MOFs demonstrated hydrogen storage performance that is no longer purely academic but commercially relevant. A landmark Nature Materials study highlighted MOF-808-Hf, a hafnium-based framework capable of achieving 7.5 wt% hydrogen storage at ambient temperatures and pressures near 100 bar—comfortably surpassing the U.S. DOE vehicular target of 5.5 wt%. This performance directly translates into system-level benefits, including an estimated 30% reduction in energy consumption compared to 700-bar compressed tanks, while mitigating safety risks associated with extreme pressures. Automotive OEMs are responding accordingly: by March 2025, Toyota confirmed pilot integration of MOF-enhanced tanks into next-generation fuel cell platforms, leveraging surface areas exceeding 5,000 m²/g to improve volumetric density without increasing tank size or vehicle mass. Equally important, the manufacturing bottleneck is easing. Startups such as Rux Energy, working with academic partners, have transitioned MOF synthesis from batch reactors to continuous-flow processes, enabling tonne-scale production suitable for heavy-duty vehicle and refueling-station demonstrations. Collectively, these developments indicate that MOFs are evolving into a practical hydrogen storage medium capable of reshaping fuel logistics across mobility, industrial hydrogen distribution, and decentralized energy systems.

Trend 2: Integration of MOFs in Direct Air Capture (DAC) Systems

MOFs are rapidly becoming the material of choice for next-generation direct air capture systems, particularly as the industry confronts the twin challenges of low CO₂ concentration (≈400 ppm) and high regeneration energy penalties. By 2025, industrial validation replaced theoretical promise, with MOFs recognized at the highest scientific level for their transformative role in carbon capture. Industrial deployments by major chemical players have shown that MOF-based adsorbents can operate at regeneration temperatures between 70°C and 120°C—dramatically lower than amine-based solvents—cutting energy intensity and improving plant economics. The performance leap is being accelerated by computational advances: the release of the ODAC25 dataset in 2025, encompassing nearly 70 million DFT calculations across 15,000 MOF structures, has enabled machine-learning-driven discovery of sorbents optimized for CO₂ selectivity under humid conditions, historically the Achilles’ heel of solid adsorbents. From an operational standpoint, amine-functionalized MOFs are now demonstrating stable CO₂ capacities of ~1.7 mmol/g at 50% relative humidity, supporting DAC regeneration energies as low as 5.76 GJ per tonne of CO₂. This combination of selectivity, moisture tolerance, and low thermal demand positions MOFs as the leading materials platform for scalable carbon removal infrastructure aligned with net-zero commitments and emerging carbon credit markets.

Opportunity 1: Onshoring of MOF Production for Defense and Semiconductor Supply Chains

Geopolitical risk and technology sovereignty concerns are creating a structural opportunity for domestic MOF production, particularly in defense, electronics, and advanced manufacturing ecosystems. In late 2025, U.S. federal funding initiatives allocated a portion of a $355 million critical materials program toward establishing domestic MOF manufacturing capabilities, reflecting their growing importance in national security applications. Defense use cases span chemical warfare filtration, selective gas separation, and high-sensitivity sensing, where MOFs’ tunable pore chemistry enables rapid detection and neutralization of hazardous agents. Parallel demand is emerging from the semiconductor sector, where sub-5 nm lithography requires ultra-pure specialty gases such as neon, argon, and xenon at parts-per-billion impurity levels. Under large-scale semiconductor industrialization programs in the U.S. and India, MOFs are being deployed as next-generation purification media that outperform traditional cryogenic and membrane-based systems in selectivity and footprint. Additionally, tightening methane-emission regulations are accelerating the integration of MOF-based sensors into oil, gas, and industrial facilities, offering detection sensitivities up to 10× higher than legacy electrochemical sensors. Together, these applications create a defensible, high-margin opportunity for localized MOF production insulated from commodity price volatility and aligned with long-term strategic procurement.

Opportunity 2: MOF-Based Indoor Air Quality (IAQ) and HVAC Systems

The global redefinition of “healthy buildings” is opening a fast-scaling opportunity for MOF-integrated air purification and HVAC solutions, particularly in dense urban and public infrastructure environments. Post-pandemic policy shifts have elevated indoor air quality from an operational consideration to a regulatory and reputational priority, driving adoption of advanced filtration technologies. In 2025, large-scale deployments—such as government-led installation of air purification systems in public schools—highlighted the limitations of conventional HEPA filters, including high pressure drop and energy penalties. MOF-based filters address these constraints by offering high VOC adsorption capacity and selective capture without impeding airflow. Advances in nanotechnology have further expanded applicability: electrospun nanofiber filters coated with MOFs are now capable of capturing particles down to 0.1 microns with order-of-magnitude efficiency improvements over legacy media. Beyond passive adsorption, titanium-based MOFs demonstrated in late 2025 can photocatalytically degrade formaldehyde and benzene under ambient indoor lighting, enabling continuous VOC removal without additional energy input. For commercial real estate operators, this translates into 10–30% energy savings through optimized ventilation rates while maintaining superior IAQ metrics. As ESG reporting increasingly incorporates occupant health indicators, MOF-enabled HVAC systems are emerging as a differentiated solution at the intersection of sustainability, energy efficiency, and public health.

Market Share Analysis: Metal-Organic Frameworks (MOFs) Market

Market Share by Product Type: Zirconium-Based MOFs as the Industrial Stability Benchmark

Zirconium-based MOFs, accounting for approximately 30% of the global MOFs market in 2025, have emerged as the dominant product class because they uniquely balance high porosity with industrial-grade chemical and thermal stability, a combination that competing Copper- or Zinc-based frameworks fail to deliver at scale. UiO-66 and UiO-67 structures have effectively become the commercial reference standard for buyers operating in harsh environments, as they retain structural integrity across a pH window of 1–10, enabling deployment in acidic flue gases, humid industrial exhausts, and aggressive semiconductor cleanroom conditions. This stability advantage directly underpins procurement decisions in high-liability industries, where material degradation equates to safety risk and operational downtime. On the supply side, the segment’s leadership is reinforced by manufacturing scale: NuMat Technologies has expanded U.S.-based production capacity to 300 tonnes annually, marking a decisive shift of Zirconium MOFs from pilot-scale synthesis to bulk industrial chemicals. Performance differentiation further strengthens share capture—Zr-MOFs demonstrate >95% selectivity in hazardous gas capture applications, enabling sub-atmospheric storage of Arsine and Phosphine for advanced semiconductor fabrication, a non-negotiable requirement for 2nm and below process nodes. The segment also benefits from strong innovation signaling: global recognition of Zr-MOF modularity in the 2025 Nobel Prize in Chemistry has catalyzed a measurable surge in corporate R&D spending, accelerating standardization around Zirconium frameworks and locking in their position as the most commercially bankable MOF chemistry.

Market Share by Product Type, 2025.png)

Market Share by Application: Gas Storage & Separation as the Highest-ROI Deployment Path

Gas storage and separation, holding around 35% of total MOF demand, represents the most economically compelling application segment because it directly attacks one of industry’s largest cost centers: energy-intensive molecular separation. In 2025, MOF-based systems have moved decisively beyond pilots, with over 40% of new gas separation installations incorporating MOF-enabled mixed matrix membranes (MMMs) that cut energy consumption by 30–50% versus cryogenic distillation. This efficiency gain is especially material for hydrogen purification, natural gas upgrading, and CO₂ capture, where operating costs dominate lifecycle economics. Within the segment, carbon capture alone accounts for nearly half of activity, supported by commercial-scale initiatives such as BASF’s multi-ton MOF sorbent production programs aimed at replacing liquid amine systems. The value proposition is quantifiable and highly marketable: next-generation MOF sorbents demonstrate capture rates equivalent to 20 kg of CO₂ per year from 200 g of material, delivering a compelling “material efficiency per ton of CO₂” metric for Net Zero investment cases. Field pilots further validate superiority—MOF-based adsorption beds have achieved 100% methane purity from raw gas streams, a threshold unattainable with conventional silica or activated carbon. As energy producers face rising carbon costs and tightening emissions regulation, gas separation remains the fastest path to monetization for MOFs, anchoring its position as the market’s leading application segment.

Competitive Landscape: Scaling, Device Integration, and Decarbonization Drive MOF Market Leadership

The competitive environment in the MOF market is characterized by material innovation, rapid scale-up, and vertical integration into functional systems rather than commodity powder sales. Leading companies differentiate through high-volume production capability, device-level engineering, and deep specialization in industrial applications such as carbon capture, specialty gas purification, petrochemical separations, and biomedical delivery systems.

BASF SE - Industrial-Scale MOF Manufacturer Supporting Global Decarbonization Initiatives

BASF’s Basolite® MOF product line positions the company among the few with multi-hundred-ton annual production capacity, achieved through optimized batch synthesis processes ensuring material consistency for industrial clients. Their portfolio, which includes widely used structures such as ZIF-8, supports large-scale catalysis, gas separation, and CO₂ capture systems. BASF’s strategic emphasis on long-term supply contracts for hard-to-abate industrial sectors aligns with the growing deployment of MOF-based decarbonization technologies. With MOFs offered in powders, pellets, and formed media for process integration, BASF remains the leading bridge between MOF chemistry and chemical industry deployment.

Numat Technologies - Pioneer in MOF-Device Engineering and Semiconductor-Grade Gas Purification

NuMat Technologies focuses on cutting-edge MOF systems for specialty gas purification, storage, and separation across electronics, defense, and clean energy segments. The company’s 300-tonne industrial MOF facility (announced Nov 2024) marks the first of its kind in the United States, enabling high-purity MOF deployment at commercial scale. NuMat’s unique strength lies in converting MOFs into integrated cartridges and purification modules, designed for ultra-high purity applications in semiconductors and advanced materials. Its specialization in engineering MOFs into functional devices differentiates it from conventional MOF powder suppliers.

Svante Inc. - Global Leader in MOF-Enabled Carbon Capture Systems For Hard-To-Abate Industries

Svante develops structured solid sorbent filters incorporating MOFs, such as CALF-20, to deliver high-efficiency CO₂ capture for cement, steel, lime, and refinery plants. Its May 2025 Gigafactory launch represents a major scale-up in the commercialization of MOF-enabled Vacuum Swing Adsorption (VSA) technology. With core competencies in system integration and industrial decarbonization engineering, Svante is positioned at the forefront of deploying MOF-based capture units for global climate mitigation efforts.

Promethean Particles Ltd. - Continuous-Flow MOF Manufacturing Specialist Addressing Scalability Constraints

Promethean Particles focuses on continuous-flow synthesis of MOFs, a key differentiator enabling cost-efficient, industrial-scale production. Their March 2025 equipment investments accelerate the commercialization of MOFs for carbon capture, gas separations, and catalyst markets. Known for its ability to replicate complex MOF architectures at scale while maintaining structural integrity, Promethean is instrumental in bridging the gap between laboratory MOF innovation and industrial adoption through cost-effective MOF production technologies.

Mosaic Materials - Developer of Ultra-Selective Mofs For CO₂ Removal and Direct Air Capture

Mosaic Materials specializes in highly selective MOF adsorbents engineered for removing CO₂ from flue gas and ambient air, supporting the growing Direct Air Capture (DAC) market. Their materials exhibit low-energy desorption characteristics, potentially reducing thermal energy penalties for gas separation processes. Mosaic’s ongoing pilot programs demonstrate long-term material stability in industrial conditions, confirming the readiness of their MOF chemistries for deployment in climate mitigation applications.

The United Kingdom has decisively positioned itself as the global scale-up leader in Metal Organic Frameworks, transitioning MOFs from laboratory powders into industrial monoliths and tonne-scale outputs. A landmark 2025 achievement came from Promethean Particles, which successfully manufactured and shipped four tonnes of MOFs in a single commercial order for an energy-efficient gas storage application. This milestone underscores the UK’s leadership in continuous-flow reactor technology, which eliminates batch-processing bottlenecks and enables consistent, high-purity MOF production suitable for regulated industrial markets.

Parallel innovation is occurring in MOF densification and system integration. Immaterial Ltd secured €15.4 million in Series A2 funding led by SLB, accelerating the development of monolithic MOFs (m-MOFs) optimized for intermittent hydrogen storage and industrial decarbonization. Additionally, Nuada expanded manufacturing at its Northern Ireland facility, scaling MOF-based carbon capture systems that deliver lower regeneration energy penalties than conventional amine scrubbing. Collectively, these developments anchor the UK as the benchmark geography for industrial MOF manufacturability.

United States – DOE-Backed MOFs for Extreme Environments and DAC

The United States MOF market is defined by federal funding intensity and application-driven deployment, particularly across Direct Air Capture (DAC), semiconductors, and defense filtration systems. A key industrial expansion was completed by Numat Technologies, which scaled its Wisconsin facility to support high-volume MOF production engineered for extreme chemical and thermal environments. These materials are increasingly embedded in semiconductor fabs for toxic gas containment and purification.

At the policy level, the U.S. Department of Energy prioritized MOFs across its 2025 DAC funding cycles, citing their ultra-high surface areas (up to ~7,000 m²/g) and superior selectivity under atmospheric conditions. Beyond clean energy, U.S. defense collaborations intensified as Framergy and Nanorh deepened partnerships to integrate MOF-based filtration systems into next-generation PPE. This dual-use trajectory positions the U.S. as the primary market for ruggedized, defense-grade MOF deployment.

Switzerland – Venture-Backed Carbon Removal and Compact MOF Systems

Switzerland has emerged as Europe’s venture capital hub for MOF-based carbon removal, focusing on cost reduction and spatial efficiency. In April 2025, novoMOF raised $5.4 million in Series B funding, led by GTT Strategic Ventures, to scale MOFs targeting sub-€100/ton CO₂ capture economics. The investment highlights the growing commercial credibility of MOFs as next-generation carbon removal substrates.

A notable strategic angle is maritime decarbonization. Swiss MOF developers are designing space-efficient sorbent architectures suitable for ships and heavy-duty transport—segments where bulky capture units are impractical. In parallel, Climeworks has reportedly evaluated second-generation MOF sorbents in 2025 to enhance the thermal efficiency of its DAC modules. These developments reinforce Switzerland’s role as a high-value innovation nucleus rather than a bulk manufacturing center.

Germany – Chemical Integration and Industrial-Grade MOFs

Germany’s MOF strategy is anchored in industrial integration, leveraging its global leadership in chemical engineering and process scale-up. A centerpiece of this approach is BASF’s continued collaboration with Svante, which in 2025 advanced mass production of CALF-20, a MOF specifically engineered to capture CO₂ from hot, humid industrial exhaust streams. This positions Germany as a leader in industrial exhaust decarbonization, beyond pilot-scale demonstrations.

Public-sector support complements private scaling. The Federal Ministry for Economic Affairs and Climate Action (BMWK) incorporated MOF-based sensors and materials into its 2025 Smart City and SuperLink innovation roadmap. Meanwhile, research institutions such as Karlsruhe Institute of Technology are advancing MOF-enhanced cryogenic insulation for hydrogen liquefaction, targeting meaningful reductions in storage energy intensity. Germany thus serves as Europe’s industrial validation platform for MOF technologies.

China – Resource Scale, Domestic Content, and Mass Deployment

China’s MOF market is driven by scale economics and domestic substitution, aligned with its Dual Carbon objectives. Under the 14th Five-Year Plan, the Ministry of Industry and Information Technology (MIIT) formally designated MOFs as Strategic New Materials, accelerating capacity build-out for zinc-based (ZIFs) and iron-based MOFs that benefit from abundant domestic feedstocks and lower costs.

Application-wise, China is the world’s largest consumer of MOFs for electronic specialty gas (ESG) storage, with 2025 subsidies supporting MOF-lined cylinders in semiconductor fabs across Jiangsu and Shaanxi. Beyond electronics, national pilots in arid western regions are deploying MOF-based atmospheric water harvesting (AWH) systems to secure water for remote industrial sites. These initiatives highlight China’s emphasis on broad, system-level deployment rather than niche specialization.

Canada – Advanced Adsorption Engineering and Clean-Tech Exports

Canada’s MOF ecosystem is characterized by precision engineering and export-oriented specialization, particularly in chemically robust zirconium-based frameworks. In 2025, ACSYNAM expanded exports of zirconium-based MOFs to European petrochemical customers, where long-term stability under harsh conditions is critical for gas separation and purification.

Canada’s global influence is further reinforced by Svante, headquartered in Vancouver. Svante’s large-scale R&D infrastructure is being used to validate MOF durability across thousands of adsorption–desorption cycles, providing the industrial proof points required by utilities and heavy industry. As a result, Canada functions as a clean-tech reliability and qualification hub within the global MOF value chain.

2025 Strategic Matrix: Metal Organic Frameworks (MOFs) National Benchmarking

Metal Organic Frameworks (MOFs) National Benchmarking

|

Country

|

Strategic Driver

|

2025 Key Milestone

|

Primary Application Focus

|

|

United Kingdom

|

Tonne-Scale Manufacturing

|

4-tonne MOF export (Promethean)

|

Gas storage, decarbonization

|

|

United States

|

Federal R&D & Defense

|

Numat Wisconsin expansion

|

Semiconductors, DAC, PPE

|

|

Switzerland

|

Carbon Tech Venture

|

novoMOF $5.4M Series B

|

Compact carbon capture

|

|

Germany

|

Chemical Integration

|

CALF-20 mass production (BASF)

|

Industrial exhaust separation

|

|

China

|

Resource Scale

|

MIIT strategic material status

|

Specialty gases, AWH

|

|

Canada

|

Adsorbent Engineering

|

Zirconium-MOF export growth

|

Petrochemical purification

|

Metal Organic Frameworks Market Report Scope

Metal Organic Frameworks Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1029.9 Million

|

|

Market Size (2035)

|

$3314.8 Million

|

|

Market Growth Rate

|

12.4%

|

|

Segments

|

By Product Type (Zinc-Based, Copper-Based, Iron-Based, Aluminum-Based, Magnesium-Based, Zirconium-Based, Others), By Organic Ligand (Carboxylate, Imidazolate, Azolate, Pyridyl), By Synthesis Method (Solvothermal/Hydrothermal, Microwave-Assisted, Mechanochemical [Ball Milling], Electrochemical, Ultrasonic/Sonochemical), By Application (Gas Storage, Gas & Liquid Adsorption/Separation, Water Harvesting & Purification, Catalysis, Biomedical & Healthcare, Energy Storage & Conversion, Sensing & Detection)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, NuMat Technologies Inc., Svante Technologies Inc., Nuada, Promethean Particles Ltd., Sumitomo Electric Industries Ltd., Kao Corporation, SyncMOF Inc., Strem Chemicals Inc., novoMOF, ACSYNAM, Immaterial, Framergy Inc., ProfMOF, EnergyX

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Metal-Organic Frameworks (MOFs) Market Segmentation

By Product Type

- Zinc-Based MOFs

- Copper-Based MOFs

- Iron-Based MOFs

- Aluminum-Based MOFs

- Magnesium-Based MOFs

- Zirconium-Based MOFs

- Others

By Organic Ligand

- Carboxylate Ligands

- Imidazolate Ligands

- Azolate Ligands

- Pyridyl Ligands

By Synthesis Method

- Solvothermal/Hydrothermal

- Microwave-Assisted Synthesis

- Mechanochemical (Ball Milling)

- Electrochemical Synthesis

- Ultrasonic/Sonochemical

By Application

- Gas Storage

- Gas & Liquid Adsorption/Separation

- Water Harvesting & Purification

- Catalysis

- Biomedical & Healthcare

- Energy Storage & Conversion

- Sensing & Detection

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Metal-Organic Frameworks (MOFs) Market

- BASF SE

- NuMat Technologies, Inc.

- Svante Technologies Inc

- Nuada

- Promethean Particles Ltd.

- Sumitomo Electric Industries, Ltd.

- Kao Corporation

- SyncMOF Inc.

- Strem Chemicals, Inc.

- novoMOF

- ACSYNAM

- Immaterial

- Framergy, Inc.

- ProfMOF

- EnergyX

*- List not Exhaustive