Market Overview: Advanced Lightweighting Metrics and High-Strength Composite Performance Propel Metallic Microspheres Market Expansion

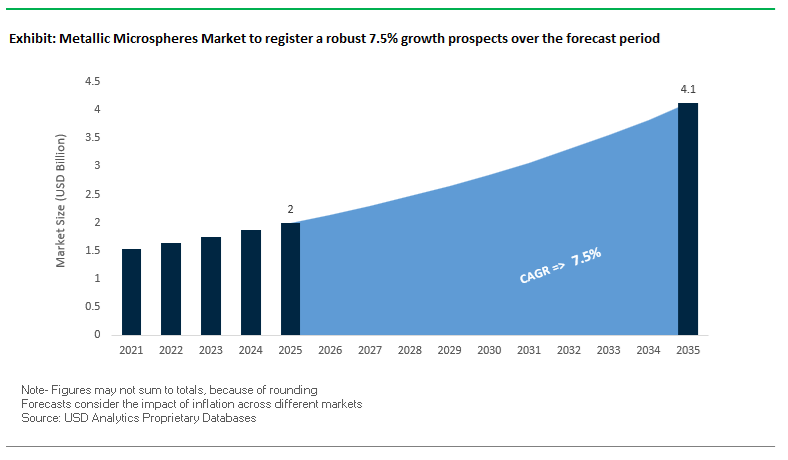

The Metallic Microspheres Market is projected to grow from USD 2.0 billion in 2025 to USD 4.1 billion by 2035, demonstrating a robust CAGR of 7.5%. The industry is accelerating due to the increasing integration of hollow metallic microspheres into syntactic foams, additive manufacturing (AM) materials, aerospace structures, automotive crash systems, and lightweight thermal management components. Manufacturers are prioritizing precise wall-thickness-to-diameter ratios, improved high-temperature performance, and optimized shock-absorption characteristics, enabling microsphere-reinforced materials to meet stringent mechanical requirements in high-performance engineering applications.

A key differentiator for vendors is the ability to supply uniform, highly spherical metallic microspheres—especially aluminum and titanium grades—engineered with a 10% wall-to-diameter ratio, a critical benchmark for maintaining compressive strength while achieving major density reductions. In aerospace, titanium syntactic foams can reduce composite density by up to 50%, reaching 0.7 g/cm³, significantly outperforming conventional metal matrices. The automotive and rail sectors are rapidly adopting Metallic Hollow Sphere Structures (MHSS), which withstand high-velocity impact loads (e.g., 5 m/s) while maintaining structural integrity. The shift from polymer fillers to metallic microspheres in high-temperature environments, such as engine components, further strengthens market adoption.

Key Insights for Material Scientists, Composite Engineers & OEM Suppliers

- 10% wall thickness ratio is now a standard engineering requirement for structural-grade hollow metallic microspheres.

- Syntactic foams achieve ~50% density reduction, enabling aerospace lightweighting targets impossible with conventional metals.

- MHSS support high-energy absorption, making them critical for crash systems, industrial safety structures, and protective enclosures.

- Metal-reinforced composites outperform polymers at high temperatures, supporting applications in aircraft engines and advanced thermal systems.

Market Analysis: AM Adoption, AI-Driven Composite Optimization & Lightweighting Investments Reshape the Metallic Microspheres Industry Landscape

The Metallic Microspheres Market is experiencing accelerated transformation driven by additive manufacturing advancements, AI-enhanced composite design, and large-scale investments in lightweight metal systems. In November 2025, Ball Corporation announced a USD 60 million expansion of its Sri City facility, indirectly boosting demand for high-purity aluminum powders, which serve as base feedstocks for both microsphere production and metal composites used in lightweight packaging and industrial applications. This aligns with the broader shift toward sustainable, lightweight materials for transportation, packaging, and next-generation electronics.

In September 2025, Materion Corporation highlighted its strategic emphasis on advanced materials for AM, EV battery systems, and semiconductor applications, reinforcing its role as a critical supplier of high-purity metal powders and metal matrix composites. The market also saw strengthening commercial viability for high-performance microsphere solutions in August 2025, when Hollomet promoted its globomet® and globocer® hollow spheres for industrial crash absorbers and thermal insulation systems. These innovations confirm growing demand for Metallic Hollow Sphere Structures (MHSS) in both high-energy impact settings and heat-management applications.

Additive manufacturing is a major catalyst, with April 2025 reports highlighting a USD 14 million expansion by Collins Aerospace, driving the need for high-sphericity metal powders essential for consistent 3D-printed structural parts. Industrywide, the integration of Artificial Intelligence (AI) with AM workflows, reported in March 2025, is enabling unprecedented precision in designing microsphere-reinforced composite architectures. AI-driven models now simulate material behavior, optimize microsphere dispersion, and enhance overall structural performance—reducing prototyping cycles and improving reliability.

R&D breakthroughs are also redefining performance benchmarks. In October 2024, researchers successfully tested aluminum syntactic foams achieving plateau strengths up to 87.71 MPa after heat treatment, pushing metallic microsphere composites into new categories of structural and crash-resistant materials. Meanwhile, strategic acquisitions in October 2025 signaled rapid consolidation within the metal matrix composite and lightweighting ecosystem, as companies race to secure technologies necessary for aerospace, defense, and automotive electrification. Additional market traction came in January 2025, when new thermal management systems in electronics adopted aluminum composite materials reinforced with conductive microspheres to enable high heat-flux dissipation in densely packed power modules.

Breakthrough Trends and Emerging Opportunities Positioning Metallic Microspheres at the Core of High-Strength Foams, Conductive Adhesives, Targeted Therapies, and Propulsion Technologies

Market Trend 1: Shift Toward Monodisperse Hollow Stainless Steel and Titanium Microspheres for High-Strength Aerospace and Marine Syntactic Foams

A defining trend in the metallic microspheres market is the rapid adoption of monodisperse hollow metallic spheres—particularly stainless steel and titanium—for next-generation metal matrix syntactic foams used across aerospace, marine, and defense platforms. These advanced MMSFs demonstrate exceptional structural performance, with Al7075-based syntactic foams achieving compressive strengths up to 230 MPa, while stainless steel MMSFs deliver around 65 MPa, enabling lightweight structural components with unprecedented load-bearing capability. Their energy absorption capacity of 67.8 MJ/m³ at densification in steel-steel composite metal foams underscores their relevance for crashworthy structures, impact-resistant panels, and blast-mitigation systems.

A key material science driver is monodispersity—narrow size distributions eliminate microstructural voids and stress concentrations, increasing compressive strength compared to polydisperse spheres. The fire performance profile of MMSFs further enhances their technical attractiveness: even with an approximate 30% drop in compressive strength at elevated temperatures, they retain structural integrity, whereas polymer foams typically undergo catastrophic thermal failure. This positions hollow metallic microspheres as critical fillers for high-temperature, high-stiffness, and high-resilience syntactic foam systems engineered for hostile environments.

Market Trend 2: Surge in Silver-Coated and Nickel Microspheres for Isotropic Conductive Adhesives in Miniaturized Electronics and EMI-Shielded Systems

Electronics miniaturization is accelerating the integration of silver-coated and nickel conductive microspheres into isotropic conductive adhesives (ICAs), replacing traditional silver flakes to achieve fine-pitch deposition, lower curing temperatures, and superior reliability. The economic advantage is substantial: silver-coated microspheres reduce the required conductive phase to 1–3% by volume, compared to 25–30% silver loading in conventional ICAs, drastically lowering precious metal consumption.

These microspheres, typically 5–30 µm in diameter with 50–250 nm silver coating layers, enable high-resolution interconnects essential for micro-LEDs, smartphone modules, and automotive sensors. Their ability to deliver EMI shielding effectiveness of 80–110 dB at ~20% filler loading supports rapidly growing demand for interference-hardened electronic architectures. Equally important is the material processing benefit—ICAs cure between 180°C and 260°C, avoiding the substrate cracking risks associated with solder reflow. As OEMs push toward ultra-compact device architectures, monodisperse metallic microspheres become indispensable to the next generation of electronic packaging and high-density circuit assemblies.

Market Opportunity 1: Magnetic Iron and Cobalt Microspheres for Contrast Enhancement, Drug Delivery, and Hyperthermia in Targeted Biomedical Therapies

A high-value opportunity emerges from the development of magnetic metallic microspheres—particularly iron oxide-based—for theranostics, MRI contrast enhancement, targeted drug delivery, and cancer hyperthermia. Biomedical performance is driven by particle size engineering: superparamagnetism is achieved below ~20 nm, enabling strong temporary magnetization under 0.2–0.5 Tesla fields without residual magnetism, preventing aggregation and ensuring circulation stability.

Biological clearance dynamics define size selection:

- <10 nm particles undergo rapid renal clearance.

- >200 nm particles are prematurely removed by the RES.

Thus, the optimal range 100–500 nm maximizes bloodstream residency and therapeutic index.

Magnetic microspheres demonstrate highly effective hyperthermia capabilities, generating heat through AMF exposure to reach 42–46°C, the therapeutic zone for tumor ablation. Their drug-loading performance is equally compelling, with nanosystems achieving 93% Doxorubicin encapsulation and pH-responsive release profiles—releasing 70% of the drug at pH 5.5 versus 10% at pH 7.4. This differential targeting supports precision oncology, making magnetic microspheres a platform material for next-generation biomedical treatments combining imaging, targeting, and therapy in a single carrier.

Market Opportunity 2: Aluminum and Copper Microspheres as Energetic Additives for Solid Rocket Propellants and Advanced Pyrotechnics

The energetic materials segment presents another strong opportunity, driven by the integration of aluminum and copper microspheres into composite solid propellants and pyrotechnic formulations. Ultrafine spherical aluminum significantly increases propellant combustion efficiency—raising the linear burn rate by 1.6–2× compared with propellants containing micron-scale aluminum or no metallic fuel. Aluminum’s high combustion enthalpy elevates specific impulse (Isp) and overall energy density, making it a cornerstone additive for defense and space propulsion systems.

Microsphere morphology directly influences ignition behavior. While traditional micron-size aluminum ignites at 2,000–2,300 K, specialized microspheres exhibit earlier ignition nearer to the ≈800 K propellant surface temperature, improving heat feedback to the decomposition zone and enabling faster, more stable combustion.

Loading levels of 14–20 wt% aluminum are standard in composite propellants, and spherical microspheres offer rheological advantages by improving slurry flow uniformity before curing. Copper microspheres similarly enhance burn profiles and energy release in pyrotechnics. These performance characteristics position metallic microspheres as critical additives in high-precision, high-energy, and high-density solid propulsion systems aligned with next-generation aerospace and defense requirements.

Metallic Microspheres Market Share Analysis

Market Share by Core Structure: Hollow Metallic Microspheres Lead Due to Lightweighting, Thermal Insulation, and Processing Advantages

Hollow Microspheres dominate the global metallic microspheres market with an estimated 60% share, driven by their unique ability to deliver dramatic weight reduction and enhanced functional performance across high-value industries. Their hollow internal core—often filled with air or inert gas—reduces density to a fraction of traditional fillers, allowing composite materials to achieve 10–30% weight savings without sacrificing mechanical strength. This lightweighting capability directly aligns with the strategic priorities of automotive, aerospace, energy, and industrial manufacturers seeking improved fuel efficiency, reduced emissions, and enhanced system performance. Additionally, hollow microspheres provide exceptional thermal insulation, making them indispensable in subsea oil & gas insulation coatings, aerospace thermal protection structures, and high-performance construction materials. Their uniformly spherical geometry improves rheology and flowability, enabling higher filler loading, reduced shrinkage, and superior surface finish in paints, coatings, adhesives, and molded parts. Such processing benefits lower manufacturing costs and improve consistency in mass production environments. The combination of structural efficiency, enhanced functionality, and manufacturing optimization places hollow metallic microspheres at the center of material innovation, securing their leadership position in the global market.

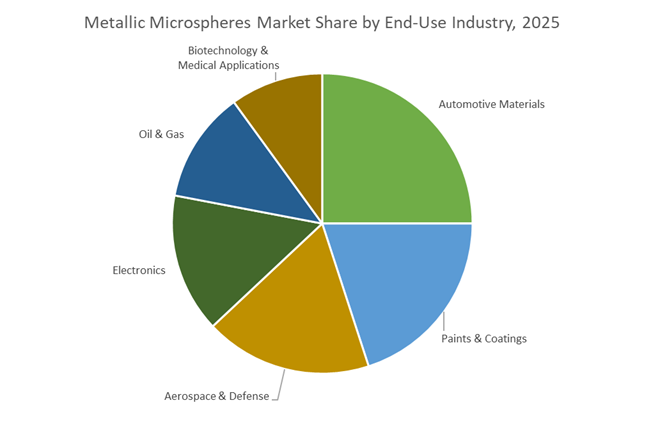

Market Share by End-Use: Automotive Materials Lead Through Lightweighting Imperatives and Electrification Trends

The Automotive Materials sector holds the largest share of the metallic microspheres market—approximately 25%—because vehicle manufacturers increasingly rely on advanced lightweight composites to meet stringent global fuel economy standards and accelerate electric vehicle (EV) adoption. Metallic microspheres, particularly metal-coated hollow spheres, are integrated into polymer matrices, composite body panels, battery housings, and structural brackets to reduce weight while retaining the mechanical strength needed for crash performance and durability. In EVs, every kilogram saved directly contributes to extended driving range, improved energy efficiency, and enhanced thermal management—making microsphere-filled materials strategically valuable. Their conductive and shielding properties (especially in nickel- and silver-coated variants) are mission-critical for EMI shielding in high-voltage battery systems, onboard electronics, and autonomous driving sensors. Beyond structural and electrical functions, hollow microspheres enable superior acoustic damping and thermal insulation in cabins, elevating passenger comfort and supporting the shift toward premium EV platforms. As automakers globally expand production volumes and transition to composite-intensive vehicle architectures, the automotive sector continues to serve as the primary growth engine for metallic microsphere demand, reinforcing its dominant market share.

Country Analysis: Strategic National Accelerators Defining the Global Metallic Microspheres Market

United States: Cold-Plasma Manufacturing Breakthroughs and Expanding Aerospace–Medical Demand

The United States remains a global innovation hub for metallic microspheres used in aerospace composites, defense-grade lightweighting materials, and precision radiotherapy applications, driven by strong government, academic, and private-sector investment. A major technological milestone came in February 2024, when U.S. university researchers demonstrated a pulsed DC cold plasma technique enabling low-cost, continuous open-air production of aluminum metallic microspheres. This development is particularly significant for manufacturers aiming to scale lightweight filler production for next-generation aerospace structures and high-performance polymer composites. Complementing these advances is the U.S. Department of Defense (DoD), which continues to sponsor R&D on metal-coated hollow ceramic microspheres for high-strength armor systems, missile platforms, and lightweight airframe components where low density and high compressive strength are mission-critical.

In parallel, the medical sector is emerging as a substantial growth engine, highlighted by ABK Biomedical securing $30 million in late 2022 to fund IDE approval for Eye90 microspheres—an advanced radiotherapeutic used in liver cancer brachytherapy. This positions the U.S. as a leading market for biologically compatible metallic microspheres designed for precision oncology. Together, these initiatives reinforce the United States’ continued dominance in high-value metallic microspheres across aerospace, defense, medical, and advanced manufacturing ecosystems.

China: High-Volume Microsphere Manufacturing and Expansion of EMI Shielding & Automotive Composite Applications

China’s position as the world's largest automotive production base and a central electronics manufacturing hub directly accelerates demand for metallic microspheres used in lightweight composites, conductive fillers, and EMI-shielding systems. As the New Energy Vehicle (NEV) segment expands, Chinese OEMs increasingly integrate metallic microspheres into polymer matrices to reduce component weight, improve thermal stability, and extend vehicle battery range—critical performance metrics in China’s competitive EV landscape. These microsphere-enabled lightweight composites are rapidly being adopted in structural parts, engine covers, interior modules, and high-voltage insulation components.

In the electronics and 5G/6G communication sector, Chinese manufacturers have shifted focus toward silver-coated microspheres that offer exceptional electrical conductivity and stable dielectric properties. These materials are essential for high-frequency electronic packaging, EMI/RFI shielding films, and conductive adhesives used in smartphones, routers, and IoT hardware. Supported by large-scale industrial policy, China continues to strengthen its supply chain in precision coating, microsphere metallurgy, and composite integration, cementing its leadership in high-volume metallic microsphere production for automotive and electronics applications.

India: Defense Manufacturing Corridors and A&D Localization Fueling Metallic Microsphere Demand

India’s Metallic Microspheres Market is gaining momentum through aggressive national policies targeted at building a self-reliant Aerospace & Defence (A&D) manufacturing ecosystem. The Department of Defence Production’s 2025 Aerospace & Defence Policy Compendium—featuring state-level policies such as the Andhra Pradesh Aerospace and Defence Policy 4.0 (2025–2030)—aims to attract ₹1 lakh crore in investment, directly bolstering domestic production of high-performance composites and specialized metallurgical components. These policies significantly expand the market for metal microspheres used in lightweight aircraft structures, ballistic-resistant composites, radomes, UAV components, and thermal shielding materials.

The launch of AeroDefCon’25 in Tamil Nadu, with a long-term target of securing ₹75,000 crore in investments, further strengthens India’s ambition to become a global defense manufacturing hub. Localization mandates and incentives for indigenous component manufacturing push Indian companies to adopt advanced microsphere synthesis technologies to meet aerospace-grade specifications. As India accelerates the development of fighter aircraft, missile systems, unmanned platforms, and defense electronics, demand for metallic microspheres—both hollow and solid, coated and uncoated—continues to rise sharply.

Germany & the European Union: Automotive Lightweighting Mandates and Next-Generation Composite Engineering

Germany and the broader EU remain at the forefront of automotive lightweighting and environmentally compliant composite development, making the region a critical hotspot for metallic microspheres. EU emission standards and circular economy regulations have forced automotive manufacturers to adopt innovative materials that reduce vehicle mass while maintaining structural strength. This is driving the integration of hollow metallic microspheres, including nickel-coated variants, into structural foams, underbody shields, and battery enclosure components, enabling weight reductions without sacrificing crash performance or thermal stability.

European material science companies are also pioneering advanced coating technologies, particularly Physical Vapor Deposition (PVD), to enhance coating uniformity, adhesion strength, and electrical performance of metal-coated ceramic microspheres. These developments are crucial for e-mobility applications, conductive adhesives, and power electronics packaging used in EVs. Meanwhile, EU-funded research programs continue to support innovations in multi-functional composites, corrosion-resistant microsphere alloys, and thermally conductive lightweight fillers—solidifying Europe’s position as a leader in high-performance, regulation-compliant metallic microsphere technology.

Japan: Precision Metallic Microsphere Engineering and Ultra-Pure Coating Technologies

Japan is a global specialist in ultra-fine metallic microspheres, excelling in tight particle size distribution and high-purity coatings essential for microelectronics, sensor modules, and advanced display technologies. Japanese companies have perfected the production of monodisperse microspheres, including nanometer-scale spheres tailored for anisotropic conductive adhesives (ACAs) used in semiconductor bonding, LCD/FPD panel assembly, and miniaturized electronic modules. These ultra-fine particles enable high-density interconnections with superior thermal and electrical stability—capabilities unmatched in many other markets.

In addition, Japan’s expertise in high-purity silver, nickel, and gold coatings ensures conductivity consistency and corrosion resistance critical for high-frequency, high-reliability electronics. This precision aligns with Japan’s strong semiconductor, robotics, and automotive electronics sectors, where microsphere uniformity and purity directly impact product performance. With continuous investment in particle synthesis, nano-coating technologies, and micro-electronic integration, Japan remains one of the highest-value markets for premium metallic microspheres.

South Korea: High-Power Electronics, EV Battery Innovation, and Demand for Conductive Microsphere Fillers

South Korea’s global strength in consumer electronics, electric vehicles, and battery technologies shapes its growing demand for metallic microspheres, particularly those used as conductive fillers and thermal management materials. Korean electronics manufacturers increasingly rely on silver-coated microspheres for EMI shielding, compact PCB architectures, and high-frequency device packaging. These materials support the country’s leadership in mobile devices, 5G infrastructure, and display technologies.

In the EV sector, South Korean OEMs advancing 800V EV architectures require materials that can withstand higher voltages, temperatures, and switching frequencies. Metallic microspheres are being integrated into battery thermal interface materials (TIMs), conductive adhesives, and lightweight structural composites for high-performance motors. Ongoing R&D into next-generation battery technologies—including silicon anodes and solid-state batteries—further expands the application of metallic microspheres in reinforcement structures, insulation layers, and high-durability conductive pathways. This positions South Korea as a dynamic, innovation-driven market for high-spec microsphere solutions.

Competitive Landscape: High-Purity Metals, Syntactic Foam Leadership & Additive Manufacturing Integration Define Market Positioning

The competitive landscape of the Metallic Microspheres Market is shaped by companies advancing lightweight metal foams, hollow metallic spheres, additive manufacturing powders, energy-absorbing structures, and high-purity metal feedstocks. Vendors that integrate materials R&D, AM-ready powder production, and proprietary composite solutions are gaining share as aerospace and automotive OEMs demand stronger, lighter, and more thermally stable materials.

Materion Corporation – Materion strengthens specialty materials leadership through aerospace and semiconductor focus

Materion remains a global leader in high-value engineered materials, supplying beryllium-based systems, advanced coatings, and metal matrix composites essential for defense and semiconductor applications. Its strategic focus aligns with megatrends such as EV electrification and clean-energy systems, industries that rely on lightweight, thermally conductive composites enhanced with metallic microspheres. Materion’s investment toward next-generation AM materials supports demand for highly spherical metal powders, ensuring consistent structural performance in aerospace-grade syntactic foams and impact-resistant components. With aerospace representing 19% and semiconductors 24% of FY24 revenue, the company continues to reinforce its position in the high-growth, high-purity materials ecosystem.

Sandvik AB (Additive Manufacturing) – Sandvik drives integrated metal powder solutions for AM-optimized composites

Sandvik leverages deep metallurgical expertise to deliver titanium, nickel, and stainless steel powders optimized for laser powder bed fusion (LPBF) and other advanced manufacturing processes. Its CoroPlus® Additive platform integrates design, materials, and production, enabling customers to develop lightweight components reinforced with metallic microspheres or hybrid structures. Strategic acquisitions have strengthened its footprint in the United States, allowing Sandvik to support regional supply chains with AM-ready powders for aerospace, energy, and medical applications. The company’s vertically integrated AM strategy provides a strong foundation for producing microsphere-reinforced metal components with superior precision.

Hollomet GmbH – Hollomet leads in metallic hollow spheres and energy-absorbing cellular metals

Hollomet specializes in globomet® metallic hollow spheres, globocer® ceramic spheres, and foamet® metal foams, differentiating itself as a pioneer in engineered cellular metals. Its microsphere structures are widely adopted in impact absorbers, crash barriers, and protective enclosures, leveraging their ability to dissipate kinetic energy without structural failure. Hollomet’s products also support high-temperature insulation applications, giving it a strong foothold in aerospace, industrial safety, and thermal engineering sectors. Continued commercial adoption of Hollow Sphere Structures (MHSS) reinforces Hollomet’s strategic role in next-generation lightweighting solutions.

Hoganas AB – Hoganas dominates the atomized metal powder supply chain for large-scale composite applications

Hoganas is the world’s largest producer of atomized metal powders, serving automotive, industrial, and additive manufacturing segments. Its powders are critical feedstocks for press-and-sinter components, which account for over 89% of traditional metal powder consumption. With the automotive industry representing ~64.9% of its metal powder demand, Hoganas plays a central role in supplying iron, nickel, and copper-based powders used to produce microsphere-enhanced structural and thermal components. Its scale, global distribution, and technical expertise position Hoganas as a foundational supplier for syntactic foam and metal matrix composite manufacturers.

Tongling Jingda Special Magnet Wire Co., Ltd. – Tongling supports low-cost, high-volume copper feedstocks for composite microsphere applications

Tongling Jingda is a major producer of enameled copper and aluminum wire, but its extensive copper-processing capabilities indirectly support the metallic microspheres market by providing access to high-purity copper powders and related feedstocks used in certain solid microsphere and composite formulations. The company’s dominant position in automotive and appliance motor materials ensures stable demand for copper-based metallic materials, enabling economies of scale. Its broad product portfolio and manufacturing capacity contribute to cost-effective sourcing for composite manufacturers developing copper-infused microspheres or hybrid metal matrix composites.

Metallic Microspheres Market Report Scope

Metallic Microspheres Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2 Billion

|

|

Market Size (2035)

|

$4.1 Billion

|

|

Market Growth Rate

|

7.5%

|

|

Segments

|

By Core Structure (Hollow Microspheres, Solid Microspheres), By Base Material (Aluminum, Silver, Copper, Nickel, Gold/Platinum Microspheres), By Coating Material (Silver-Coated, Nickel-Coated, Copper-Coated Microspheres), By End-Use Application (Automotive Materials, Aerospace & Defense, Electronics, Biotechnology & Medical Applications, Paints & Coatings, Oil & Gas)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M, Trelleborg, Momentive, Potters Industries, Cospheric, Sinosteel, ABK Biomedical, Mo-Sci Corporation, Sigmund Lindner, AkzoNobel, Matsumoto Yushi-Seiyaku, Accumet Materials, Reade Advanced Materials, Novum Glass, Induchem Holding

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Metallic Microspheres Market Segmentation

By Core Structure

- Hollow Microspheres

- Solid Microspheres

By Base Material

- Aluminum Microspheres

- Silver Microspheres

- Copper Microspheres

- Nickel Microspheres

- Gold / Platinum Microspheres

By Coating Material

- Silver-Coated Microspheres

- Nickel-Coated Microspheres

- Copper-Coated Microspheres

By End-Use Industry

- Automotive Materials

- Aerospace & Defense

- Electronics

- Biotechnology & Medical Applications

- Paints & Coatings

- Oil & Gas

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Metallic Microspheres Market

- 3M

- Trelleborg

- Momentive

- Potters Industries

- Cospheric

- Sinosteel

- ABK Biomedical

- Mo-Sci Corporation

- Sigmund Lindner

- AkzoNobel

- Matsumoto Yushi-Seiyaku

- Accumet Materials

- Reade Advanced Materials

- Novum Glass

- Induchem Holding.

*- List not Exhaustive

Research Coverage: Metallic Microspheres Market

The latest USDAnalytics study on the Metallic Microspheres Market investigates how hollow and solid metal spheres are redefining lightweight structural design, crash energy management, and thermally stable composites across automotive, aerospace, electronics, biotechnology, and energy applications. This report investigates the evolution of metallic microsphere engineering—from monodisperse stainless-steel and titanium grades for high-strength syntactic foams to silver- and nickel-based spheres tailored for conductive adhesives, EMI shielding, and high-density electronic packaging. It examines breakthroughs in cold-plasma manufacturing, additive-manufacturing-ready powders, magnetic microsphere therapeutics, and energetic formulations for advanced propulsion systems. In-depth analysis reviews cover demand inflection points created by EV lightweighting, defense armor programs, medical radiotherapy platforms, and high-power electronics thermal management. The study highlights how OEMs and material innovators are using microsphere-filled metal, polymer, and hybrid matrices to meet aggressive performance, weight, and sustainability metrics while optimizing rheology and processing economics. With rigorous coverage of competitive strategies, technology roadmaps, and country-level policy catalysts, this report is an essential resource for material scientists, composite designers, procurement leaders, and strategy teams seeking data-backed insights into the future trajectory of the global metallic microspheres ecosystem.

Scope Highlights

- Segmentation By Core Structure – Hollow Microspheres; Solid Microspheres

- Segmentation By Base Material – Aluminum Microspheres; Silver Microspheres; Copper Microspheres; Nickel Microspheres; Gold / Platinum Microspheres

- Segmentation By Coating Material – Silver-Coated Microspheres; Nickel-Coated Microspheres; Copper-Coated Microspheres

•By End-Use Industry – Automotive Materials; Aerospace & Defense; Electronics; Biotechnology & Medical Applications; Paints & Coatings; Oil & Gas

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, capturing regional regulations, industrial clusters, and OEM localization strategies influencing metallic microsphere adoption.

- Timeframe Coverage: Includes historic data from 2021–2025 and forecast assessments for 2026–2034, enabling long-term planning around lightweighting programs, composite platform launches, and AM-centric manufacturing investments.

- Companies: Covers analysis and profiles of 15+ key players, encompassing hollow-sphere specialists, AM-powder producers, medical microsphere innovators, and specialty chemical firms shaping the global Metallic Microspheres Market value chain.