Microplastic Detection Market 2025–2034: Regulatory Mandates, Portable Spectroscopy, and Real-Time Sensing Technologies Driving $10.1 Billion Expansion

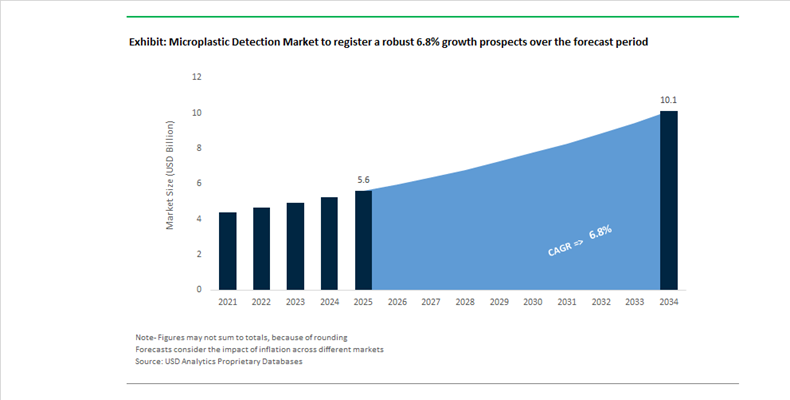

The Microplastic Detection Market is projected to grow from $5.6 billion in 2025 to $10.1 billion by 2034, reflecting a CAGR of 6.8%. Market expansion is being directly shaped by tightening environmental regulations, food safety surveillance initiatives, and technological advancements in trace-level polymer analytics. The regulatory environment is transitioning from exploratory research toward mandatory reporting frameworks, forcing industrial laboratories, water utilities, and food manufacturers to implement validated detection protocols. Analytical demand now spans microplastics (<5 mm) and increasingly nanoplastics (<1 µm), requiring highly sensitive spectroscopy, chromatography, and imaging platforms capable of differentiating polymer types in complex matrices.

In November 2025, the European Chemicals Agency opened its portal for annual microplastic emission reporting under updated EU REACH restrictions. Companies must submit emission data by May 31, 2026, triggering immediate investment in standardized quantification tools. In parallel, the U.S. Environmental Protection Agency initiated review procedures in June 2025 to potentially include microplastics under the forthcoming UCMR 6 framework—an action that would obligate nationwide water system monitoring. At the state level, the California Department of Toxic Substances Control proposed listing microplastics on its Candidate Chemicals List in mid-2025, setting the stage for mandatory alternative analyses of consumer products. In Asia, the Food Safety and Standards Authority of India launched “Project Microplastics” to establish validated national detection methods for salt, seafood, and sugar by 2026. These regulatory catalysts are structurally embedding detection technology into compliance workflows rather than voluntary research environments.

Instrumentation providers are responding with high-throughput and portable solutions. In 2024, Shimadzu Corporation and HORIBA Scientific launched upgraded mass spectrometry systems engineered for trace-level PTFE and fluoropolymer quantitation in food and water samples. In May 2025, Agilent Technologies enhanced its 8850 Gas Chromatograph with triple quadrupole compatibility to accelerate polymer fingerprinting in high-volume environmental labs. In February 2025, Bruker Corporation introduced a 3D X-ray microscope using microCT to provide non-destructive structural imaging of microplastics, reducing reliance on destructive FTIR sample preparation. Meanwhile, Waters Corporation expanded portable chromatography platforms to enable at-line food testing during manufacturing rather than post-production lab submission.

Emerging technologies are redefining field detection. Researchers at the University of British Columbia developed a smartphone-based fluorescence microscope capable of detecting particles down to 50 nanometers, offering a scalable solution for low-resource environments. In early 2026, academic teams introduced aggregation-induced emission polymers that enable glow-in-the-dark tracking of microplastics within biological tissues—eliminating dye leakage and enabling real-time in vivo monitoring. Concurrently, advancements in Surface Acoustic Wave (SAW) sensors demonstrated reagent-free, piezoelectric-based particle detection in beverages, opening pathways for compact, continuous monitoring devices. Collectively, the convergence of regulatory mandates, spectroscopic precision, and portable sensor innovation is transitioning the microplastic detection market from laboratory-based analysis toward integrated, real-time environmental surveillance systems.

Microplastic Detection Market Trends and Opportunities

Trend: Regulatory Mandates Driving Standardized Microplastic Monitoring in Drinking Water

The microplastic detection market is entering a regulatory-driven expansion phase as public authorities move from exploratory research toward enforceable monitoring regimes. Following the regulatory trajectory of PFAS, microplastics are increasingly viewed as an emerging contaminant class that requires standardized, nationwide surveillance. In December 2025, a coalition of governors from seven U.S. states formally petitioned the U.S. Environmental Protection Agency to include microplastics in the upcoming Unregulated Contaminant Monitoring Rule (UCMR 6) scheduled for 2027. If adopted, this would mandate high-frequency testing across thousands of public water systems, triggering a large-scale procurement cycle for advanced analytical instrumentation such as Raman spectroscopy, micro-FTIR, and pyrolysis-GC-MS.

California continues to function as the regulatory bellwether. The California State Water Resources Control Board finalized detailed standard operating procedures for Raman and infrared spectroscopy during 2024–2025, requiring four consecutive years of testing and public disclosure. These protocols have effectively set detection benchmarks that municipal laboratories in other states are now compelled to emulate to avoid future compliance gaps. Importantly, public health agencies are also evaluating the co-removal efficiency of existing PFAS treatment infrastructure. Audits conducted in late 2025 revealed that reverse osmosis and granular activated carbon systems installed for PFAS mitigation can simultaneously capture microplastics down to extremely small size fractions, creating a dual-utility justification for upgrading both detection and filtration systems. This convergence is accelerating capital investment into integrated monitoring platforms that combine chemical and particulate analysis.

Trend: Strategic CPG Supply Chain Auditing and Brand Risk Mitigation

Beyond public utilities, global consumer packaged goods companies are emerging as a powerful demand driver for microplastic detection technologies. Food and beverage brands are embedding microplastic analytics into ESG reporting, supplier qualification, and quality assurance programs to protect brand equity and pre-empt regulatory enforcement. During 2024–2025, Danone accelerated the deployment of advanced product footprinting tools that integrate microplastic leakage metrics into dynamic life cycle assessments. As a result, more than 99% of its production sites now operate under structured water filtration and reclamation frameworks that explicitly consider particulate contamination risks.

Scientific evidence has amplified this urgency. Peer-reviewed studies published in 2024 reported microplastic presence in over 80% of global tap water samples and in nearly all tested commercial sea salt brands. In response, premium and “free-from” product lines are increasingly investing in micro-FTIR imaging and Raman mapping to certify products as plastic-minimized. This analytical certification is becoming a commercial differentiator in high-value European fresh and packaged food markets. Regulatory signaling is reinforcing this shift. In July 2024, the U.S. Food and Drug Administration confirmed that it is actively validating analytical methods for microplastic detection, signaling to manufacturers that voluntary compliance today will likely translate into mandatory compliance under future food safety frameworks. As a result, detection capabilities are moving upstream into raw material sourcing and bottling operations rather than remaining confined to end-product testing.

Opportunity: Rapid AI-Enabled Sensors for Wastewater Compliance and Source Control

Wastewater treatment plants represent the most critical intervention point for preventing microplastic leakage into rivers and oceans. The primary growth opportunity lies in transitioning from slow, laboratory-based analytical workflows to AI-enabled, real-time detection systems that operate directly within treatment processes. In January 2024, researchers introduced PlasticNet, a machine learning model capable of classifying 11 common polymer types with accuracy exceeding 95% while delivering results roughly 50% faster than traditional spectroscopic interpretation. Such tools allow operators to dynamically adjust filtration and separation parameters based on the specific polymer profile detected in influent streams.

Field-deployable optics are further expanding addressable markets. Academic and municipal pilots supported by EU-funded initiatives in 2025 demonstrated that compact optical sensors using blue-light excitation and smartphone-integrated analysis can identify pollution hotspots in urban runoff without centralized laboratories. These solutions dramatically reduce response times from days to minutes, enabling preventive interventions upstream of wastewater plants. At the same time, next-generation filtration technologies are creating a feedback-driven market for smart detection. The rise of metal-organic framework membranes and advanced nanofiltration systems in 2025 has increased demand for embedded sensors that can detect micro- and nanoplastics in real time, optimizing energy use while maintaining sub-micron capture efficiency. This sensor–filtration convergence positions AI-enabled detection as a core infrastructure layer rather than a standalone analytical service.

Opportunity: Ambient Air Monitoring for Occupational and Urban Microplastic Exposure

Airborne microplastics are rapidly emerging as a new regulatory and public health frontier, opening a parallel growth avenue for the microplastic detection market. Evidence from occupational studies in late 2025 confirmed the presence of respirable microplastic particles, often around 10 microns, in textile and synthetic fiber manufacturing environments. These findings are driving demand for continuous, stationary air monitoring systems capable of coupling high-volume air sampling with Raman or SEM-based polymer identification to meet evolving occupational health and safety requirements.

Urban monitoring represents an even broader opportunity. Smart city programs are already deploying dense networks of multi-pollutant sensors to generate hyperlocal air quality heatmaps. In 2025, these networks began integrating microplastic-specific spectral triggers, allowing municipalities to correlate airborne plastic concentrations with traffic density, construction activity, and industrial zoning. This capability supports data-driven urban planning while addressing citizen concerns around chronic exposure. Longer term, the greatest R&D focus is shifting toward nanoplastics below one micron. With global plastic use projected to nearly triple by 2060, the ability of nanoplastics to cross biological membranes has elevated nanoparticle tracking analysis and dynamic light scattering tools to priority status for government-funded research. Vendors capable of bridging laboratory-grade nanoplastic detection with scalable environmental monitoring are positioned to capture the next wave of growth in the microplastic detection market.

Microplastic Detection Market Share and Segmentation Insights

Spectroscopy-Based Analytical Technologies Lead Microplastic Detection Market

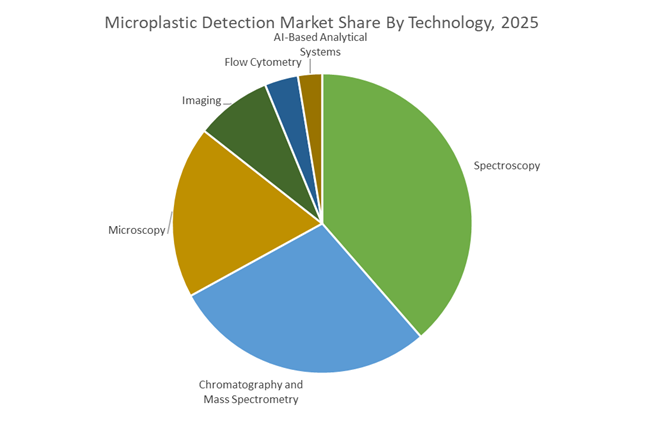

Spectroscopy technologies accounted for 38.60% of the Microplastic Detection Market share in 2025, establishing them as the most widely used analytical tools for identifying and characterizing microplastic particles in environmental and industrial samples. Techniques such as Fourier Transform Infrared (FTIR) spectroscopy, Raman spectroscopy, and Near Infrared (NIR) spectroscopy enable precise polymer identification by analyzing the molecular vibration patterns unique to different plastic materials. These analytical platforms allow researchers and laboratories to detect common microplastics such as polyethylene (PE), polypropylene (PP), polyethylene terephthalate (PET), and polystyrene (PS) in water, soil, air, and biological samples. FTIR microscopy remains the most widely adopted technique for laboratory-based polymer identification, while portable Raman spectroscopy systems support in-field microplastic detection and environmental monitoring. In 2025, the integration of automated particle recognition software and artificial intelligence–assisted spectral libraries has significantly improved detection efficiency, enabling spectroscopy platforms to automatically identify, classify, and quantify thousands of microplastic particles within a single sample while reducing manual analysis time and improving analytical consistency.

Research and Academic Institutions Drive Global Demand for Microplastic Detection Technologies

Research and academic institutions accounted for 38.60% of the Microplastic Detection Market share in 2025, making universities and environmental research laboratories the largest users of microplastic analysis technologies. The rapid rise in scientific studies examining the occurrence, environmental distribution, ecological impacts, and human health implications of microplastics has driven extensive demand for advanced analytical instruments capable of identifying microscopic polymer particles in complex environmental samples. Academic laboratories conduct large volumes of microplastic research across disciplines including environmental science, marine biology, toxicology, and materials science, generating critical datasets on microplastic contamination in oceans, freshwater systems, soils, and food chains. In 2025, the global research community is increasingly focused on developing standardized analytical protocols for microplastic detection, as variations in sampling, extraction, and identification methods have historically limited cross-study comparability. International organizations such as ISO and ASTM are actively developing standardized testing frameworks that build upon methodologies established by academic researchers, enabling more consistent measurement of microplastic contamination and facilitating broader adoption of detection technologies by regulatory agencies and industrial stakeholders.

Microplastic Detection Market Competitive Landscape

The microplastic detection market in 2026 is driven by AI-integrated analytical workflows, hyphenated techniques (TGA-FTIR-GC/MS), and automated “load-and-go” sample preparation. Competitive advantage lies in sub-micron detection, nanoplastic identification, and high-throughput systems for regulatory-driven testing across water, air, and food matrices.

Shimadzu pioneers automated microplastic mass quantification with dual-spectroscopy integration

Shimadzu Corporation is leading the microplastic detection market through advanced automation and AI-powered analytical platforms. Its AMsolution-enabled Particle Analysis System is the first to automatically quantify microplastic mass and volume, significantly improving analytical accuracy. The AIRsight™ IR/Raman microscope enables simultaneous dual-spectroscopy, allowing precise identification of polymers and inorganic additives in a single workflow. LabSolutions Detect enhances anomaly detection in chromatographic systems, improving reliability in complex environmental samples. The company’s expansion into India strengthens its presence in high-growth APAC environmental monitoring markets. Shimadzu’s focus on automation, precision, and integrated spectroscopy positions it at the forefront of next-generation microplastic analysis.

Agilent accelerates microplastic detection speed with QCL-based chemical imaging and automated workflows

Agilent Technologies is dominating high-throughput microplastic analysis through its 8700 LDIR Chemical Imaging System powered by quantum cascade laser (QCL) technology. This system enables rapid spectral acquisition in under one second, dramatically reducing analysis time from days to minutes. Its automated workflows can detect particles as small as 2 µm, addressing critical sub-10 micron detection requirements. Agilent’s GC/MSD systems combined with pyrolysis and thermal desorption remain industry benchmarks for mass-based quantification. The company is also positioning its analytical tools within global regulatory frameworks, supporting nanoplastic toxicity research. Its emphasis on speed, sensitivity, and regulatory alignment strengthens its leadership in analytical instrumentation.

Thermo Fisher delivers end-to-end microplastic analysis with high-resolution spectroscopy and mass quantification

Thermo Fisher Scientific provides comprehensive “sample-to-insight” solutions, integrating Raman spectroscopy, FT-IR, and pyrolysis-GC-MS technologies. Its DXR3 Raman microscope and Nicolet iS50 FT-IR systems enable precise polymer identification and morphological characterization. The company is advancing total mass quantification approaches using pyrolysis-GC-MS to meet evolving regulatory reporting standards. New software innovations simplify detection of particles below 10 µm, addressing key technological limitations in microplastic analysis. Thermo Fisher is also a leader in nanoplastic research, leveraging high-sensitivity mass spectrometry for trace-level detection. Its integrated ecosystem and analytical depth position it as a key player in environmental and pharmaceutical testing markets.

PerkinElmer advances AI-driven FTIR microscopy with hyphenated analytical workflows for regulatory compliance

PerkinElmer is strengthening its position in the microplastic detection market through AI-powered digital ecosystems and high-performance FTIR microscopy. The Spotlight Aurora platform delivers enhanced speed and clarity, enabling laboratories to meet stringent regulatory requirements for food and water testing. Its unified AI software ecosystem connects instruments and workflows, improving productivity and anomaly detection in industrial QA/QC environments. PerkinElmer’s leadership in TGA-FTIR-GC/MS technologies enables advanced identification of microplastics and associated organic contaminants. With operations across 168 countries, the company has a strong global footprint in environmental monitoring. Its focus on AI integration and hyphenated techniques supports high-confidence analytical outcomes.

Waters expands bio-environmental microplastic analysis with high-sensitivity LC-MS and diagnostic integration

Waters Corporation is leveraging its LC-MS expertise and strategic acquisitions to expand into bio-environmental microplastic analysis. Its next-generation Microflow LC columns with MaxPeak HPS technology deliver enhanced sensitivity for detecting trace-level plastic additives. The acquisition of BD’s Biosciences & Diagnostic Solutions business strengthens its capabilities in studying biological impacts of microplastics. With $3.165 billion in 2025 sales, growth is driven by increasing demand for high-precision analytical instruments. Waters is targeting ESG-driven laboratory upgrades through low-solvent, high-sensitivity systems. Its integration of analytical chemistry with life sciences positions it uniquely in the evolving microplastic detection ecosystem.

European Union (Germany & France): From Compliance Deadlines to Instrument Standardization

The European Union represents the most regulation-driven demand center for microplastic detection technologies, with Germany and France at the forefront of enforcement and implementation. Under Regulation (EU) 2023/2055, the October 17, 2025 deadline marked the first binding requirement for suppliers of synthetic polymer microparticles to provide technical instructions for preventing environmental release. This obligation has materially increased procurement of localized detection systems capable of quantifying microplastic losses at production sites, compounding facilities, and downstream industrial users. The December 2025 entry into force of the Plastic Pellets Loss Regulation further tightened controls, as operators handling more than five tonnes of pellets annually must now deploy verifiable containment and monitoring systems, driving demand for high-throughput, inline detection platforms in logistics yards, silos, and effluent discharge points.

Regulatory pressure escalates further in 2026. From May 31, 2026, annual reporting to European Chemicals Agency becomes mandatory, requiring quantified disclosure of microplastic releases for the 2025 calendar year. This has accelerated investment in automated FTIR and Raman spectroscopy within municipal wastewater treatment plants to support the EU Zero Pollution Action Plan, which targets a 30% reduction in microplastic emissions by 2030. Looking ahead, the European Commission’s plan to request harmonized standards by December 17, 2026 is formalizing instrument performance benchmarks across the Single Market, effectively transforming detection systems from optional compliance tools into regulated infrastructure.

United States: State-Led Regulation and Infrastructure-Driven Monitoring

In the United States, microplastic detection demand is being shaped less by a single federal mandate and more by state-level rulemaking and infrastructure initiatives. California’s June 2025 decision to initiate rulemaking to list microplastics under the Safer Consumer Products Candidate Chemicals List positions the California Department of Toxic Substances Control to regulate priority products that contain or generate microplastics, including electronics, paints, and textiles. Anticipated finalization in 2026 is prompting early adoption of laboratory-grade imaging and spectroscopic systems by manufacturers seeking to pre-empt product restrictions.

Parallel initiatives are unfolding across water systems. Great Lakes states, led by Michigan, are developing groundwater sampling methodologies to establish baseline microplastic concentrations, while coastal states such as Rhode Island have mandated bi-annual characterization of microplastic loads in state waters. These programs are prioritizing automated computer vision and rapid particle counting platforms to manage scale. Additional momentum comes from proposed microfiber filtration mandates for washing machines, which are expected to require standardized detection protocols to verify filtration efficacy. At the federal level, the U.S. Food and Drug Administration has included microplastics in its FY 2025–2026 food safety research priorities, driving procurement of ultra-high-resolution imaging systems for toxicological studies across federal laboratories.

China: Centralized Monitoring and AI-Integrated Detection

China’s microplastic detection market is being structured through centralized environmental governance and digital industrial policy. The Regulation on Ecological Environment Monitoring, effective January 1, 2026, strengthens national control over data quality and explicitly encourages the deployment of AI-integrated spectroscopic methods for trace pollutant identification in soil and water. This regulatory framework is being reinforced by the Ministry of Industry and Information Technology Green Manufacturing roadmap, which promotes zero-waste industrial parks and requires continuous monitoring of micro-debris in effluent streams using online laser diffraction and optical sensing technologies.

Scientific advancement is supporting this policy push. In March 2025, research from the Shaanxi Key Laboratory demonstrated the application of machine learning to FTIR and Raman datasets, significantly improving detection accuracy in complex biological matrices. Beyond terrestrial monitoring, China expanded its maritime surveillance network in 2025 by deploying autonomous underwater vehicles equipped with fluorescence sensors in the South China Sea. This combination of centralized regulation, AI-driven analytics, and marine monitoring positions China as a scale-driven adopter of next-generation microplastic detection systems.

Japan: Maritime Recovery and High-Resolution Coastal Mapping

Japan’s approach to microplastic detection is anchored in maritime recovery and precision coastal monitoring. In 2025, the government highlighted the second-generation onboard microplastic recovery system developed by Mitsui O.S.K. Lines in collaboration with Miura Co., which uses cyclone separation to isolate microplastics from engine-cooling seawater during voyages. This operational integration of detection and capture reflects Japan’s emphasis on source-level intervention.

Onshore, the Ministry of the Environment is reinforcing detection through fixed-point coastal monitoring stations deployed in 2025–2026, using advanced FTIR microscopy to generate high-resolution spatial maps of microplastic distribution. These efforts align with Japan’s Plastic Resource Circulation Strategy, which targets a 25% reduction in single-use plastics by 2030 and includes funding for blockchain-based tracking systems to prevent fragmentation during recycling. Detection technologies are therefore embedded not only in monitoring but also in lifecycle governance.

South Korea: Legislative Frameworks and Predictive Risk Modeling

South Korea is developing one of the most structured legislative frameworks for microplastic detection. The proposed Special Law on the Reduction and Management of Microplastics, deliberated during 2024–2025, seeks to establish enforceable standards for intentionally added microplastics in household appliances and office equipment. This anticipated regulation is driving early investment in detection systems capable of verifying compliance at the product and component level.

Maritime monitoring is advancing in parallel. The Ministry of Oceans and Fisheries plans to implement a one-stop onboard treatment system by December 31, 2026, integrating real-time detection technologies to quantify microplastics recovered from marine debris. Complementing physical monitoring, South Korea is developing a biochemical behavior forecasting model scheduled for completion in late 2026. This tool will correlate particle size, polymer type, and surface chemistry with environmental and biological behavior, elevating detection data into a predictive risk assessment framework.

Comparative Snapshot: Country-Level Positioning in the Microplastic Detection Market

Microplastic Detection Market County Level Snapshot

|

Region / Country

|

Primary Regulatory Driver

|

Detection Technology Focus

|

Core Monitoring Environment

|

Strategic Outcome

|

|

European Union (DE, FR)

|

REACH Annex XVII and pellet loss regulation

|

Automated FTIR and Raman spectroscopy

|

Industrial sites and wastewater plants

|

Standardized, compliance-led deployment

|

|

United States

|

State-level SCP and water policies

|

Imaging, computer vision, filtration verification

|

Consumer products and freshwater systems

|

Decentralized, infrastructure-driven adoption

|

|

China

|

Ecological monitoring regulation 2026

|

AI-integrated spectroscopy and laser sensors

|

Industrial parks and marine zones

|

Centralized, scale-oriented monitoring

|

|

Japan

|

Plastic resource circulation strategy

|

FTIR microscopy and onboard recovery systems

|

Coastal and maritime environments

|

Precision mapping and source capture

|

|

South Korea

|

Special microplastics management law

|

Real-time detection and predictive modeling

|

Marine and product-level systems

|

Risk-based regulatory enforcement

|

Microplastic Detection Market Report Scope

Microplastic Detection Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.6 Billion

|

|

Market Size (2034)

|

$10.1 Billion

|

|

Market Growth Rate

|

6.8%

|

|

Segments

|

By Technology (Spectroscopy, Microscopy, Chromatography and Mass Spectrometry, Imaging, Flow Cytometry, AI-Based Analytical Systems), By Medium (Water, Soil and Sediment, Air, Biological Samples, Consumer Products), By Particle Size (Below 100 Microns, 100 Microns to 1 Millimeter, 1 to 5 Millimeters), By End User (Regulatory and Government Bodies, Research and Academic Institutions, Industrial Facilities, Water Treatment Facilities, Food and Beverage Manufacturers)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Thermo Fisher Scientific, Agilent Technologies, Bruker, Shimadzu, PerkinElmer, HORIBA, JEOL, Waters, Danaher, Oxford Instruments, Renishaw, ZEISS, Endress+Hauser, JASCO, Mettler Toledo

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Microplastic Detection Market Segmentation

By Technology

- Spectroscopy

- Microscopy

- Chromatography and Mass Spectrometry

- Imaging

- Flow Cytometry

- AI-Based Analytical Systems

By Medium

- Water

- Soil and Sediment

- Air

- Biological Samples

- Consumer Products

By Particle Size

- Below 100 Microns

- 100 Microns to 1 Millimeter

- 1 to 5 Millimeters

By End User

- Regulatory and Government Bodies

- Research and Academic Institutions

- Industrial Facilities

- Water Treatment Facilities

- Food and Beverage Manufacturers

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Microplastic Detection Market

- Thermo Fisher Scientific

- Agilent Technologies

- Bruker

- Shimadzu

- PerkinElmer

- HORIBA

- JEOL

- Waters

- Danaher

- Oxford Instruments

- Renishaw

- ZEISS

- Endress+Hauser

- JASCO

- Mettler Toledo

*- List not Exhaustive