Monochloroacetic Acid Market 2025–2034: Sustainable CMC Innovation, Agrochemical Expansion, and Feedstock Volatility Driving $2,045.4 Million Outlook

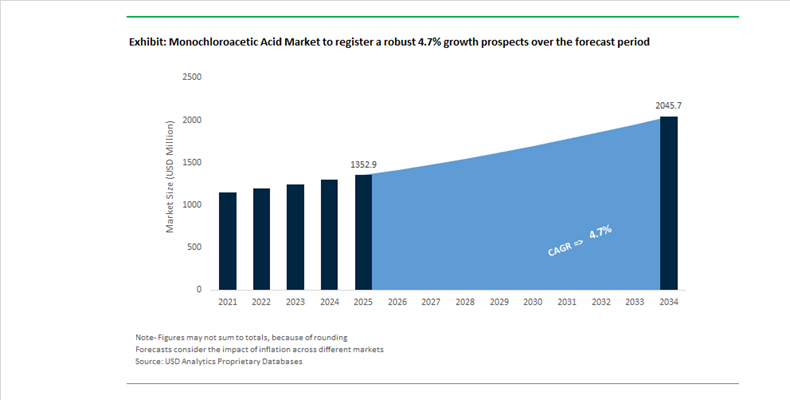

The Monochloroacetic Acid (MCAA) Market is projected to expand from $1,352.9 Million in 2025 to $2,045.4 Million by 2034, registering a CAGR of 4.7%. Growth is anchored in three structural demand streams: carboxymethylcellulose (CMC) for detergents and food applications, agrochemical intermediates such as 2,4-D and glyphosate, and thioglycolic acid (TGA) derivatives for PVC stabilizers. MCAA remains a critical chlorinated intermediate produced via chlorination of acetic acid, and its value chain is closely linked to chlorine, caustic soda, and ethylene economics. Over the 2024–2026 period, regulatory tightening, sustainability certifications, and process modernization have reshaped competitive positioning across major producing regions including Europe, North America, India, and Japan.

Sustainability has become a decisive differentiator. In June 2024, Nouryon secured ISCC PLUS certification for green MCAA production at its Delfzijl facility in the Netherlands, verifying the use of bio-based or recycled feedstocks. This foundation enabled the February 2026 launch of FinnFix® PB MAX, the first 100% bio-based and biodegradable CMC for detergents, derived from ISCC PLUS-certified MCAA. The innovation strengthens supply to consumer brands seeking lower Scope 3 emissions and reduced carbon intensity in homecare formulations. In February 2026, Nouryon received a Sustainability Award from Henkel, recognizing advancements in degradable MCAA-based detergent solutions that optimize water hardness and improve washing efficiency.

Capacity and technology investments have also intensified. In January 2024, Daicel Corporation committed $18 million to expand Japanese MCAA capacity by 20%, targeting tight supply in high-purity crystalline grades for textiles and agrochemicals. Throughout 2025, producers including CABB Group and PCC SE accelerated the shift toward continuous flow chlorination systems, replacing batch reactors to enhance energy efficiency, reduce dichloroacetic acid (DCAA) formation, and improve occupational safety. Regulatory compliance has required parallel capital allocation; in April 2024, the U.S. EPA finalized updated HON and RMP rules mandating stricter fenceline monitoring and emergency preparedness, compelling American manufacturers to invest in closed-loop chlorination and emissions control systems ahead of 2025–2026 deadlines.

India has emerged as a central agrochemical hub. By mid-2025, joint venture operations such as Anaven, formed between Nouryon and Atul Ltd, increased domestic supply of MCAA derivatives to serve rising pesticide demand across Asia. The FAO’s long-term pesticide usage data from 1990–2023 underscores sustained growth in herbicide intermediates, positioning India as a strategic export platform. Upstream integration remains critical; in February 2026, BASF SE was named Nouryon’s Supplier of the Year for Chemical Intermediates, highlighting the importance of secure ethylene and oxygenated solvent feedstocks for MCAA derivative production.

Market volatility has been pronounced. In late 2025 and early 2026, North American MCAA prices rose approximately 15.5% following chlor-alkali shutdowns that constrained chlorine availability, prompting producers such as OxyChem and Olin to pass through higher costs. Simultaneously, 2024 saw increased demand for high-purity TGA—an MCAA derivative—after European regulatory scrutiny of PVC additives encouraged stabilizer manufacturers to shift toward cleaner, MCAA-route chemistries to improve thermal stability in construction plastics. The interplay of sustainability certification, regulatory enforcement, feedstock availability, and agrochemical expansion continues to define the competitive trajectory of the global monochloroacetic acid market.

Monochloroacetic Acid Market Trends and Opportunities

Trend: Strategic Verticalization for High-Purity MCAA in CMC Production

The monochloroacetic acid market is undergoing a structural shift toward vertical integration as demand for carboxymethyl cellulose accelerates across energy, industrial, and advanced materials applications. CMC has evolved from a commodity thickener into a critical rheology modifier for shale oil recovery fluids, lithium-ion battery binders, and high-performance personal care formulations. This evolution is compelling producers to secure captive supplies of high-purity MCAA rather than rely on merchant sourcing, particularly for high-viscosity and specialty CMC grades where impurity control directly impacts end-use performance.

Between 2024 and 2025, leading manufacturers such as Nouryon and CABB Group executed targeted capacity expansions to address a 25–30% rise in CMC-grade MCAA demand. A notable milestone was the completion of a 25% capacity increase at Nouryon’s chlorinated intermediates assets, designed to support growth in Asia-Pacific and North America. Oilfield services remain a major demand anchor, as CMC is a non-substitutable fluid-loss additive in drilling operations. With global upstream oil and gas capital expenditure projected to reach approximately $570 billion in 2025, technical-grade crystalline MCAA continues to dominate volume demand due to its handling stability and compatibility with high-throughput formulations.

Technological upgrading is reinforcing this verticalization trend. By 2025, nearly one-fifth of global MCAA production lines had adopted advanced catalytic chlorination routes that reduce byproduct formation, particularly dichloroacetic acid. These eco-efficient processes deliver 10–12% energy savings while improving purity consistency, a prerequisite for specialty CMC applications in batteries and high-end industrial fluids. As a result, MCAA is increasingly treated as a strategic intermediate rather than a standalone commodity.

Trend: Regulatory-Driven Substitution and Green Herbicide Formulation

Regulatory pressure is reshaping the agrochemical segment, historically the largest outlet for MCAA consumption. In the European Union and North America, scrutiny of legacy phenoxy herbicides is accelerating the transition toward newer chloroacetamide-based actives that offer improved environmental and toxicological profiles. This shift is elevating the importance of ultra-high-purity MCAA, as trace impurities can propagate into final formulations and jeopardize compliance with tightening residue limits.

The implementation of Regulation (EU) 2025/854 in May 2025 intensified residue monitoring across the bloc, reinforcing the move away from older MCAA-derived actives such as 2,4-D and MCPA. In response, agrochemical leaders including FMC Corporation and Dow relaunched advanced herbicide platforms in high-growth markets such as India and Latin America. These products retain MCAA as a core building block but are engineered to meet stricter 2026 maximum residue level thresholds, driving a strong preference for MCAA with a low-dichloroacetic-acid profile.

Asia-Pacific remains the epicenter of agrochemical demand, with China and India jointly accounting for more than one-third of global MCAA consumption. However, the emphasis has shifted toward automated process control and export-grade consistency. In September 2025, Daicel Corporation expanded its MCAA capacity using advanced automation protocols to ensure uniform quality for specialty herbicide exports. This regulatory-driven evolution is redefining MCAA demand from volume-centric to quality-led growth.

Opportunity: Decarbonizing Supply Chains Through Bio-Based MCAA

Decarbonization mandates and Scope 3 emission targets are creating a structural opportunity for bio-based MCAA. By utilizing renewable acetic acid and green chlorine produced via renewable-powered electrolysis, producers are positioning MCAA as a low-carbon, drop-in intermediate for surfactants, detergents, and cellulose derivatives. This transition allows downstream brands to decarbonize supply chains without reformulating end products.

A key commercialization milestone occurred in December 2025, when Nouryon partnered with Galaxy Surfactants to integrate ISCC PLUS-certified green MCAA into cocamidopropyl betaine production. The initiative enables personal care brands to achieve measurable carbon footprint reductions while maintaining identical functional performance. In parallel, Nouryon Japan became the first supplier to launch ISCC PLUS-certified green MCAA in Asia-Pacific, aligning with the Japan 2030 decarbonization roadmap and signaling broader regional adoption.

Upstream innovation is also gaining momentum. In August 2025, BASF initiated collaborations with U.S. biotechnology firms to develop renewable feedstock pathways that decouple MCAA synthesis from fossil-derived chlorine. These developments position bio-based MCAA as a premium ingredient for CMC and detergent applications, where sustainability credentials are becoming procurement qualifiers rather than differentiators.

Opportunity: High-Purity Intermediates for Oncology and HPAPI Manufacturing

The rapid expansion of the high-potency active pharmaceutical ingredient market is unlocking a high-margin niche for MCAA as a precursor to chloroacetyl chloride and other complex intermediates. With oncology therapies accounting for more than 70% of HPAPI demand and a growing share of new molecular entities classified as highly potent, pharmaceutical manufacturers require intermediates that meet stringent purity and traceability standards.

This demand is driving targeted investment in pharma-grade MCAA capacity. In October 2025, Niacet Corporation, a subsidiary of Kerry, announced an expansion of its U.S. MCAA assets to serve oncology and chronic disease drug pipelines. The project emphasizes ultra-low impurity thresholds suitable for highly potent synthesis routes. Concurrently, contract development and manufacturing organizations are deepening integration with high-grade MCAA suppliers. Aarti Pharmalabs commercialized more than 50 APIs during the 2024–2025 fiscal year, underscoring the sector’s growing capability to manage hazardous MCAA-based transformations.

As HPAPI pipelines expand and regulatory scrutiny intensifies, reliable access to pharma-grade MCAA is emerging as a strategic enabler for oncology innovation. This positions the MCAA market at the intersection of specialty chemicals and advanced pharmaceutical manufacturing, with sustained upside driven by long-term healthcare demand rather than cyclical industrial trends.

Monochloroacetic Acid Market Share and Segmentation Insights

Solid Monochloroacetic Acid Leads Market with High Purity, Storage Efficiency, and Cost Advantages

Solid monochloroacetic acid accounted for 58.60% of the Monochloroacetic Acid Market by form in 2025, driven by its higher concentration, extended shelf life, and cost efficient transportation compared to liquid MCA. Typically supplied as flakes or pellets, solid MCA is preferred by large scale chemical manufacturers for producing key derivatives such as carboxymethyl cellulose (CMC), thioglycolic acid, and phenoxyacetic acid. Its stable physical form supports easier storage and handling across industrial supply chains. In 2025, dust suppressed and granular MCA formats are gaining adoption, improving occupational safety by reducing airborne particulates while maintaining reactivity and purity required for high performance chemical synthesis processes.

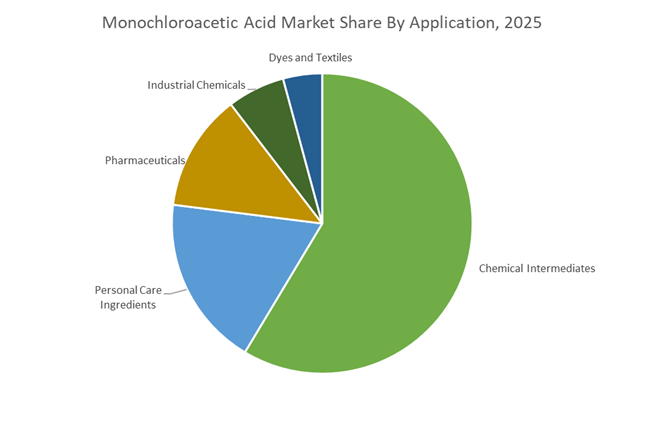

Chemical Intermediates Segment Drives MCA Demand Across CMC, Agrochemicals, and Specialty Chemicals

Chemical intermediates accounted for 58.60% of the Monochloroacetic Acid Market by application in 2025, reflecting MCA’s critical role as a building block in multiple downstream chemical value chains. It is extensively used in the production of carboxymethyl cellulose for food, pharmaceuticals, detergents, and oilfield applications, as well as thioglycolic acid for personal care and phenoxyacetic acid derivatives for agrochemicals such as 2,4-D herbicides. The broad applicability of MCA derivatives supports consistent industrial demand across sectors. In 2025, strong global demand for CMC continues to anchor MCA consumption, with expanding use in food stabilization, drilling fluids, and detergent formulations driving sustained growth in chemical intermediate applications.

Monochloroacetic Acid Market Competitive Landscape

The monochloroacetic acid (MCAA) market in 2026 is defined by ultra-low DCAA purity (<100 ppm), integrated chlorine-acetic acid value chains, and continuous flow manufacturing. Competitive differentiation centers on high-purity pharmaceutical grades, corrosion-resistant logistics, and energy-efficient production technologies.

Nouryon leads high-purity MCAA production with integrated global supply chains and bio-based derivative innovation

Nouryon remains the global benchmark in the monochloroacetic acid market, combining large-scale production with sustainability-driven innovation. Its recognition by Henkel underscores its leadership in supplying MCAA derivatives such as carboxymethyl cellulose (CMC) for biodegradable detergents. The company is advancing bio-based CMC solutions that comply with EU Ecolabel and EPA Safer Choice standards, strengthening its position in green surfactants. Through its Anaven joint venture with Atul Ltd, Nouryon operates a strategically integrated MCAA hub in India, serving high-growth APAC agrochemical and pharmaceutical markets. Its ISO-tank logistics network ensures safe molten MCAA transport across global markets. This integration across production and distribution secures its dominance in both volume and high-purity segments.

CABB sets industry benchmarks in high-purity MCAA logistics and digitalized fine chemical manufacturing

CABB Group GmbH differentiates itself through advanced logistics and precision manufacturing for high-specification monochloroacetic acid. Its titanium tank car innovation increases load capacity by 30% while improving corrosion resistance, addressing a critical challenge in molten MCAA transport. With production facilities in Germany and China, CABB ensures supply chain resilience for agrochemical and pharmaceutical clients. The company’s focus on custom manufacturing integrates MCAA into complex fine chemical synthesis for APIs and specialty dyes. Its digital monitoring systems capture over 5,000 data points per minute, reducing off-spec batches by 85% and ensuring consistent ultra-low impurity levels. CABB’s combination of logistics innovation and process control positions it as a premium supplier in high-purity markets.

PCC Group drives ultra-pure MCAA innovation with sub-100 ppm DCAA grades and integrated chlorine supply

PCC Group is emerging as a key disruptor in the monochloroacetic acid market through its ultra-pure (U-P MCAA) portfolio with DCAA levels below 90 ppm. Its Brzeg Dolny facility, with 42,000-ton capacity, is tightly integrated with PCC Rokita’s chlorine production, reducing feedstock volatility and logistics risks. The company is expanding into North America through planned chlor-alkali investments, strengthening its global footprint. PCC’s focus on pharmaceutical and food-grade CMC applications positions it in high-margin segments. Sustainability initiatives targeting net climate neutrality by 2050 and renewable energy integration further enhance its competitive positioning. Its emphasis on purity, integration, and green energy makes it a strong challenger in specialty MCAA.

Jubilant Ingrevia scales cost-efficient MCAA production to dominate agrochemical intermediate markets

Jubilant Ingrevia is a top global MCAA producer, leveraging cost-efficient manufacturing and vertical integration to serve high-volume agrochemical markets. As part of the top five players controlling nearly 48.8% market share, the company is a key supplier for herbicides such as glyphosate and 2,4-D. Its production base in India enables competitive pricing and strong export capabilities across ASEAN and Latin America. Jubilant is investing in cleaner chlorination technologies to align with global environmental regulations while maintaining cost leadership. The company’s expansion strategy focuses on regions with rising demand for crop protection chemicals driven by food security concerns. Its scale, cost advantage, and geographic reach solidify its position in volume-driven segments.

AkzoNobel strengthens MCAA derivative demand through chlorine integration and specialty chemicals investment

AkzoNobel N.V. is reinforcing its position in the monochloroacetic acid ecosystem through its chlorine-based operations and downstream specialty chemical applications. The company raised €1.1 billion in 2026 to expand its global chemical infrastructure and support high-margin growth areas. Its investments in aerospace coatings and specialty formulations increase internal demand for high-purity MCAA derivatives used as stabilizers and intermediates. AkzoNobel’s strategy focuses on margin expansion through portfolio optimization and divestment of non-core assets. Its expertise in halogenated chemistry supports applications in surfactants, pharmaceuticals, and industrial coatings. This integration across upstream chlorine and downstream specialty chemicals strengthens its competitive position in value-added MCAA segments.

China: Capacity Intensification, Semiconductor Purity, and Green Chlorination Mandates

China remains the most structurally dynamic geography in the monochloroacetic acid market, driven by capacity expansion, downstream polymer integration, and regulatory pressure on chlorination efficiency. In October 2025, Nouryon completed a major capacity expansion at its Jiaxing site, effectively doubling output of metal alkyls and essential co-catalysts that rely on MCAA-derived surfactants for polyolefin manufacturing. This investment strengthens China’s domestic supply chain for high-performance plastics while anchoring MCAA demand in value-added applications rather than commoditized outlets. Complementing this move, Nouryon also confirmed the launch of a dedicated Organic Peroxides Innovation Center in Tianjin, scheduled for 2026, which will further optimize MCAA utilization in localized polymer processing and advanced materials.

Policy-driven modernization is accelerating structural change. Under the Ministry of Industry and Information Technology 2026 Industrial Green Development Plan, chlorine-derivative producers are required to cut hazardous byproduct intensity by 15%. This mandate is forcing MCAA plants in Shandong and Jiangsu to migrate from batch to continuous chlorination, improving yield consistency and emission control. At the same time, 2025 industrial disclosures from the Yangtze River Delta highlight a clear shift toward ultra-pure MCAA grades, with impurity control tailored for chemical mechanical planarization slurries used in domestic 7 nm semiconductor fabrication. This convergence of green chemistry enforcement and electronics-grade purity is repositioning China from volume-centric production toward specification-driven MCAA supply.

India: Agrochemical Pull-Through, Feedstock Stability, and Transparency-Led Compliance

India’s monochloroacetic acid market is increasingly defined by agrochemical demand, feedstock stabilization, and sustainability-led operational upgrades. Gujarat Alkalies and Chemicals Limited reported accelerated progress on its “Ahvaan” sustainability project during November 2025, targeting higher capacity utilization and a greener power mix across its chlorine-derivative portfolio. These measures are aimed at lowering the carbon footprint of domestically produced MCAA while improving cost resilience. In parallel, GACL’s joint venture GACL-NALCO Alkalies & Chemicals achieved its first profit before tax in Q2 FY 2025–26, stabilizing regional chlorine feedstock availability for MCAA units in the Dahej industrial corridor.

Downstream agrochemicals continue to anchor demand fundamentals. FMC Corporation expanded its crop protection manufacturing footprint in India across 2024–2025, directly increasing local consumption of MCAA as a core intermediate for glyphosate and 2,4-D herbicides. Looking ahead, the anticipated 2026 rollout of India’s updated Pesticides Management Bill is reshaping supplier behavior. MCAA producers are being compelled to provide granular impurity disclosures, particularly dichloroacetic acid levels, to meet stricter export compliance norms. This regulatory shift is pushing the Indian market toward higher-transparency, export-grade MCAA rather than purely domestic commodity supply.

Germany: Energy Cost Pressure, Ultra-Pure Compliance, and Hydrogen-Based Pathways

Germany’s monochloroacetic acid market reflects a balance between energy cost challenges, export discipline, and technological differentiation. Throughout 2025, CABB Group undertook financial restructuring initiatives to stabilize operations amid elevated electricity and gas prices. Despite these headwinds, German export volumes remained stable at approximately 4,043 metric tons as of October 2025, underscoring the strategic importance of German-origin MCAA in pharmaceutical and specialty chemical supply chains. Pricing dynamics mirrored this tension, with an 11.9% surge recorded in September 2025 driven by capacity hedging and pharma-sector demand, followed by normalization in Q4 as buyers recalibrated procurement for 2026.

Regulatory and process innovation are reinforcing Germany’s positioning in ultra-pure grades. As of January 2026, new reporting obligations under European Chemicals Agency REACH Annex XVII came into effect, tightening oversight on persistent organic pollutants. German producers have responded by deploying AI-enabled real-time analytics to ensure dichloroacetic acid impurities remain below the 90 ppm threshold required for high-specification applications. Beyond compliance, forward-looking decarbonization is emerging. A 2025 pilot at the Leuna Chemical Complex is testing green hydrogen-derived acetic acid as a feedstock for MCAA synthesis, with the stated objective of achieving the first zero-carbon MCAA production route by 2027.

United States: Yield Optimization, Trade Facilitation, and Pharma Intermediates Reshoring

The United States monochloroacetic acid market is increasingly shaped by operational efficiency, cross-border trade frameworks, and pharmaceutical reshoring incentives. In mid-2025, Dow Chemical announced the deployment of advanced control systems across its domestic chlorine-derivative assets. These digital upgrades are designed to lift MCAA yields by 4% while cutting energy intensity by 12% per ton, reinforcing competitiveness amid tightening environmental scrutiny. On the policy front, a July 2025 executive order on regulatory relief eased select emission controls for high-efficiency chemical plants, while the USMCA framework continues to support frictionless trade of MCAA into Canadian mining and U.S. detergent value chains.

End-use diversification is providing structural demand support. In 2025, the U.S. oil and gas sector expanded its use of high-viscosity carboxymethyl cellulose for hydraulic fracturing, an application that now absorbs roughly one quarter of MCAA output in the Permian Basin. Simultaneously, federal incentives aimed at reducing reliance on imported active pharmaceutical ingredient intermediates have prompted U.S. specialty chemical firms to increase domestic synthesis of ibuprofen and naproxen, both of which depend on MCAA in key reaction steps. This pharma-focused pivot is elevating the strategic importance of consistent, pharmaceutical-grade MCAA supply within the United States.

Comparative Snapshot: Country-Level Strategic Positioning in the Monochloroacetic Acid Market

Monochloroacetic Acid Market County Level Snapshot

|

Country

|

Core Strategic Driver

|

Primary End-Use Pull

|

Technology or Policy Lever

|

Market Positioning Outcome

|

|

China

|

Capacity scale and green chemistry

|

Polyolefins, semiconductors

|

Continuous chlorination, purity upgrades

|

Shift toward spec-driven supply

|

|

India

|

Agrochemical growth and sustainability

|

Herbicides, exports

|

Feedstock stabilization, impurity disclosure

|

Export-ready, compliant MCAA

|

|

Germany

|

Ultra-pure compliance and decarbonization

|

Pharma intermediates

|

AI monitoring, green hydrogen pilots

|

High-spec, premium-grade supplier

|

|

United States

|

Efficiency and reshoring

|

Oil and gas, pharmaceuticals

|

Advanced process control, USMCA

|

Resilient domestic value chains

|

Monochloroacetic Acid Market Report Scope

Monochloroacetic Acid Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1352.9 Million

|

|

Market Size (2034)

|

$2045.4 Million

|

|

Market Growth Rate

|

4.7%

|

|

Segments

|

By Form (Solid, Liquid), By Production Process (Chlorination of Acetic Acid, Alternative Chemical Processes), By Grade (Technical Grade, High-Purity Grade, Ultra-Pure Grade), By Application (Chemical Intermediates, Personal Care Ingredients, Pharmaceuticals, Dyes and Textiles, Industrial Chemicals), By End-User Industry (Agriculture, Food and Beverage, Pharmaceuticals and Healthcare, Cosmetics and Personal Care, Oil and Gas, Textiles and Leather)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Nouryon, CABB Group, Archroma, PCC Group, Gujarat Alkalies and Chemicals, Dow, Shandong Minji Chemical, Niacet, International Flavors and Fragrances, Hebei Jihua Chemical, Denka, MCAA, Shijiazhuang Donghua Jinlong Chemical, Anugrah Kumar, Xuchang Dongfang Chemical

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Monochloroacetic Acid Market Segmentation

By Form

By Production Process

- Chlorination of Acetic Acid

- Alternative Chemical Processes

By Grade

- Technical Grade

- High-Purity Grade

- Ultra-Pure Grade

By Application

- Chemical Intermediates

- Personal Care Ingredients

- Pharmaceuticals

- Dyes and Textiles

- Industrial Chemicals

By End-User Industry

- Agriculture

- Food and Beverage

- Pharmaceuticals and Healthcare

- Cosmetics and Personal Care

- Oil and Gas

- Textiles and Leather

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Monochloroacetic Acid Market

- Nouryon

- CABB Group

- Archroma

- PCC Group

- Gujarat Alkalies and Chemicals

- Dow

- Shandong Minji Chemical

- Niacet

- International Flavors and Fragrances

- Hebei Jihua Chemical

- Denka

- MCAA

- Shijiazhuang Donghua Jinlong Chemical

- Anugrah Kumar

- Xuchang Dongfang Chemical

*- List not Exhaustive