Thioglycolic Acid Market Overview 2025–2034: $148.6 Million to $257.5 Million at 6.3% CAGR Driven by Regulatory Reformulation, High-Purity Electronics Demand, and Low-Carbon Thiochemical Integration

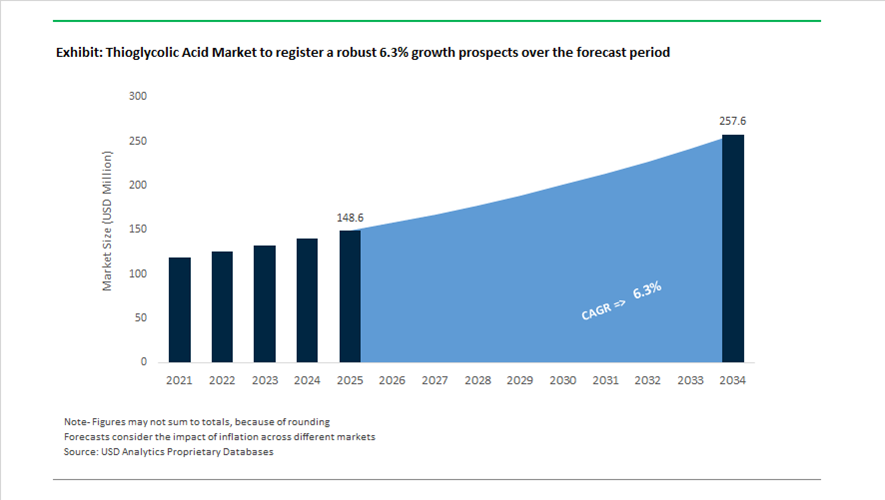

The global Thioglycolic Acid (TGA) market is valued at $148.6 million in 2025 and is projected to reach $257.5 million by 2034, expanding at a CAGR of 6.3%. Thioglycolic acid, a core sulfur-based specialty chemical, is widely used in depilatory creams, hair waving formulations, PVC stabilizers, oilfield corrosion inhibitors, and advanced electronic materials. Market growth is being reshaped by regulatory tightening in cosmetics, increasing demand for high-purity thiochemicals in opto-electronics, and decarbonization initiatives across sulfur-intermediate supply chains. The industry is transitioning from commodity-grade TGA toward application-specific, compliant, and high-performance derivatives targeting premium personal care, laboratory reagents, and semiconductor materials.

Regulatory scrutiny intensified across major markets beginning in 2024. Throughout 2024, the EU Scientific Committee on Consumer Safety continued safety evaluations of thioglycolic acid in eyelash-waving and professional salon products, prompting manufacturers to reformulate with lower concentrations and pH-balanced systems to comply with strict EU caps. In February 2025, Health Canada updated its Cosmetic Ingredient Hotlist to include tighter restrictions on certain thioglycolic acid esters. This regulatory revision mandates reformulation of select depilatory and hair-care products by 2026, accelerating demand for safer TGA derivatives with improved dermal compatibility. In response to these pressures, Arkema introduced a new range of TGA-based personal care derivatives in 2024 focused on reduced irritation and enhanced skin tolerance for sensitive applications. During mid-2024 and into 2025, producers such as Bruno Bock showcased low-odor TGA salt innovations utilizing advanced masking technologies to address one of the key commercial limitations of thiochemicals in premium at-home depilatory products.

Structural shifts in upstream production and portfolio strategy further define the market landscape. In April 2024, Thermo Fisher Scientific implemented sustainability upgrades across its reagent manufacturing lines, incorporating eco-efficient methods for high-purity thioglycolic acid used in pharmaceutical and laboratory synthesis. In January 2024, the merger of Novozymes and Chr. Hansen to form Novonesis indirectly influenced the TGA market by accelerating development of enzymatic alternatives to chemical reductants in textile and hair processing, intensifying competition in certain end-use segments. In November 2025, Lotte Chemical finalized the divestment of its Pakistani chemical stake as part of a broader strategic exit from legacy commodity intermediates, reflecting global realignment toward high-performance materials. During late 2025, Sinopec integrated green hydrogen production from its Xinjiang project into sulfur-intermediate manufacturing chains, supporting lower-carbon synthesis of TGA precursors aligned with China’s 2026 ESG objectives. Arkema announced in late 2025 a strategic cost-reduction plan targeting €600 million in 2026 capital expenditure, prioritizing investment in high-growth thiochemical derivatives for battery and healthcare applications.

High-value specialty applications are expanding beyond traditional cosmetics. In 2025, specialty chemical producers introduced high-purity thioglycolic acid with purity levels exceeding 99.5% for quantum-dot passivation in next-generation display technologies, where TGA acts as a capping and surface-stabilizing ligand in nanocrystal synthesis. During 2025, new TGA-derived corrosion inhibitor systems were commercialized for oil and gas well acidizing, functioning as mercaptide-based passivating agents to protect metal infrastructure from sour gas and catalytic cracking environments.

Structural Shifts and High-Value Adjacencies in the Thioglycolic Acid (TGA) Market

Supply Chain Localization Accelerates Demand for High-Purity Thioglycolic Acid in Pharmaceutical Synthesis

The Thioglycolic Acid market is undergoing a decisive structural bifurcation, with high-purity pharmaceutical-grade TGA consolidating its dominance as drug manufacturers tighten impurity thresholds across sulfur-containing API pathways. TGA is a non-substitutable intermediate in cephalosporin antibiotics, thiol-functionalized oncology drugs, and emerging targeted therapies where trace metal contamination or side-product formation directly compromises yield and regulatory acceptance. As of late 2024, high-purity grades accounted for the largest share of global demand, reflecting the growing intolerance for technical or cosmetic-grade material in regulated synthesis environments.

This shift is reinforced by geographic supply chain realignment. India’s chemical manufacturing ecosystem is expanding domestic TGA capacity under the Production-Linked Incentive scheme and the broader Aatmanirbhar Bharat framework, targeting reduced reliance on imports from East Asia. With the Indian chemical sector contributing approximately 7% to national GDP and supplying over 80,000 downstream products, local availability of high-purity TGA is becoming a strategic enabler for pharmaceutical CDMOs. For buyers, localization reduces lead-time volatility, mitigates geopolitical risk, and improves auditability under cGMP and ICH Q7 standards. For producers, this trend elevates the value of process control, sulfur feedstock purity, and advanced distillation capabilities over sheer volume expansion.

Clean Beauty Reformulation Drives Odor-Controlled and Salt-Based TGA Derivatives

In personal care, Thioglycolic Acid is experiencing a parallel transformation driven by clean beauty positioning and regulatory scrutiny rather than cost optimization. Traditional free-acid TGA, long criticized for its pungent odor and irritation potential, is increasingly being replaced by ammonium and calcium thioglycolate salts that offer controlled reactivity and improved sensory profiles. This transition is being accelerated by regulatory tightening. In February 2025, Health Canada updated its Cosmetic Ingredient Hotlist, banning specific thioglycolic esters and imposing stricter limits on TGA-based actives in depilatory and hair-perm formulations.

These regulatory moves are reshaping formulation strategies across North America and influencing global brand standards. Product launches now emphasize rapid efficacy with reduced skin aggressiveness, as demonstrated by natural-focus depilatory creams introduced in 2024–2025 that achieve effective hair removal in under three minutes while minimizing irritation. For TGA producers, this trend shifts competitive advantage toward derivative chemistry, deodorization techniques, and formulation-grade consistency rather than commodity acid production. Suppliers capable of delivering low-odor, tightly specified thioglycolate salts are increasingly preferred partners for multinational cosmetics brands seeking regulatory resilience and consumer trust.

TGA-Based Lixiviants Enable Low-Carbon Precious Metal Recovery from E-Waste

One of the most structurally attractive growth opportunities for Thioglycolic Acid lies in sustainable hydrometallurgy for electronic waste recycling. With global e-waste volumes growing at roughly 5% annually and urban mining economics becoming increasingly compelling, TGA is gaining attention as a selective, low-toxicity lixiviant for gold and copper recovery from printed circuit boards and ceramic capacitors. Peer-reviewed research published in 2025 demonstrates that thiol-containing organic acids can achieve gold extraction efficiencies exceeding 90% under optimized acidic oxidant conditions, while significantly reducing co-dissolution of base metals.

The economic rationale is strong. One metric ton of discarded smartphones contains up to 100 times more gold than a ton of primary ore, yet traditional cyanide-based leaching faces mounting regulatory and social resistance. TGA-based systems offer lower energy intensity, reduced CO2 emissions, and improved occupational safety compared to pyrometallurgical routes. As extended producer responsibility regulations and circular economy mandates tighten across the EU and parts of Asia, demand for green lixiviants positions TGA as a strategic input into next-generation urban mining infrastructure rather than a niche laboratory reagent.

High-Performance TGA Derivatives Gain Traction as Green Corrosion Inhibitors in Oil and Gas

The expansion of deepwater exploration, sour gas production, and high-pressure reservoirs is opening a specialized, high-margin application window for Thioglycolic Acid derivatives as corrosion inhibitors. In CO2-rich and moderately high-temperature environments, TGA-based compounds exhibit strong electron-donating characteristics that promote the formation of stable protective films on steel surfaces. This makes them particularly effective in mitigating localized corrosion and scaling in produced water systems where traditional nitrogen-based inhibitors struggle with toxicity and biodegradability constraints.

Sustainability pressures are amplifying this opportunity. Nearly one-third of offshore operators report challenges complying with marine discharge regulations for conventional corrosion inhibitors. TGA-derived formulations, which demonstrate higher biodegradability and lower aquatic toxicity, align more closely with offshore environmental permitting requirements. As oilfield chemistry shifts from brute-force inhibition toward performance-optimized, environmentally acceptable formulations, TGA’s role is evolving from a specialty additive to a core component of green corrosion management strategies in offshore and subsea operations.

Thioglycolic Acid Market Share and Segmentation Insights

Purity Grade Market Share: Technical Grade Dominates with Mining and Industrial Processing Demand

Technical grade thioglycolic acid holds the largest share at 48.60% in 2025, supported by its extensive use in mining and metallurgy, oil and gas processing, and polymer additive applications. Its cost-effectiveness and reliable performance make it the preferred choice for large-scale industrial operations. High purity, pharmaceutical, and electronic grades serve more specialized applications requiring stricter quality standards. A key market driver is the strong linkage to mining industry demand, particularly in copper and molybdenum extraction, where thioglycolic acid is used as a depressant in sulfide ore flotation, ensuring efficient mineral separation and consistent operational performance.

Application Market Share: Cosmetics and Personal Care Leads with Strong Hair Treatment Demand

Cosmetics and personal care accounts for 32.80% of the thioglycolic acid market in 2025, driven by its critical role in permanent hair waving and depilatory formulations. Its ability to break disulfide bonds in keratin enables effective hair reshaping and removal, making it indispensable in hair care chemistry. Mining and metallurgy, oil and gas, polymer and plastic additives, and pharmaceuticals represent additional application areas. A significant trend is the continued demand from professional salon services, where thioglycolic acid-based formulations are optimized for controlled performance, reduced odor, and improved hair protection, supporting consistent results in permanent hair treatments.

Thioglycolic Acid Market Competitive Landscape

The thioglycolic acid (TGA) market in 2026 is shaped by feedstock integration and regionalized production near sulfur and natural gas hubs. Industry leaders are advancing odor-masking technologies, low-sensitization derivatives, and bio-based synthesis routes to comply with ECHA regulations while improving safety, stability, and performance across cosmetics, polymers, and industrial applications.

Arkema Strengthens Global Leadership with Integrated Thiochemicals and Low-Odor TGA Innovations

Arkema dominates the thioglycolic acid market with the world’s largest production capacity and vertically integrated sulfur derivatives platform. Expansion of its Kerteh, Malaysia facility strengthens methyl mercaptan supply, ensuring feedstock security for TGA production. Its low-odor TGA derivatives are gaining traction in premium personal care formulations, addressing regulatory and consumer-driven requirements. Arkema’s mercaptide chemistry plays a critical role in refinery catalyst protection and PVC stabilization. Integration across Beaumont and Lacq sites ensures cost efficiency and consistent product quality. The company continues to lead in high-purity thiochemical intermediates for global industrial and cosmetic applications.

Bruno Bock Advances High-Purity Thioglycolates for Polymer Control and Semiconductor Applications

Bruno Bock is a benchmark in high-performance sulfur chemistry, focusing on ultra-pure thioglycolic acid derivatives for specialty applications. Its TGA-based chain transfer agents enable precise molecular weight control in acrylic polymer synthesis. The company has successfully navigated REACH regulations by developing low-sensitization, compliant derivatives aligned with Annex III standards. Ammonium and calcium thioglycolates remain essential in cold wave hair formulations and are expanding into metal recovery processes. Through its EVANS® division, Bruno Bock is scaling custom thiochemicals for semiconductor and photoresist applications. Its specialization in high-purity, high-value TGA segments ensures strong positioning in regulated markets.

Daicel Accelerates Bio-Based Thiochemical Development Through Portfolio Transformation Strategy

Daicel is repositioning its chemical portfolio toward high-value intermediates under its Accelerate 2025 strategy. The 2026 reorganization and divestment of non-core assets enable increased focus on biomass-derived thiochemicals and advanced synthesis technologies. Its EcoVadis Gold certification reflects strong ESG performance and sustainable manufacturing practices. The company is leveraging internal carbon pricing to drive low-emission TGA production innovations. Strategic capital reallocation supports expansion in automotive and specialty chemical applications across Asia. Daicel’s focus on carbon-accountable intermediates aligns with growing demand for sustainable thioglycolic acid derivatives.

Merck Targets High-Purity TGA Demand in Biopharma, Semiconductor, and Analytical Applications

Merck KGaA leads the analytical-grade thioglycolic acid segment through its Life Science division, supplying high-purity reagents for pharmaceutical and semiconductor industries. Its TGA is widely used in peptide synthesis, metal ion analysis, and stabilization of sensitive intermediates. The 2026 restructuring prioritizes Process Solutions, strengthening its position in bioprocessing and advanced materials. Supelco-grade TGA ensures regulatory compliance for global QC laboratories and research institutions. Divestment of Surface Solutions enhances focus on high-growth sectors including semiconductors and rare diseases. Merck’s precision chemical portfolio supports high-margin, low-volume applications requiring stringent purity standards.

Sasaki Chemical Expands Surface Treatment Applications with pH-Neutral TGA and EV Sector Focus

Sasaki Chemical specializes in functional thioglycolic acid applications for metal treatment, industrial cleaning, and leather processing. Its pH-neutral TGA formulations reduce corrosion risks while maintaining high solvency, making them ideal for aerospace and precision equipment maintenance. The company is targeting EV battery manufacturing, using TGA for copper foil cleaning and surface preparation. Its solutions support environmentally compliant leather processing as a safer alternative to sulfide-based unhairing agents. Expansion into Southeast Asia strengthens its presence in electronics manufacturing hubs. Sasaki’s niche focus on surface chemistry enables differentiation in high-value industrial applications.

Qingdao LNT Chemical Scales Cost-Competitive TGA Supply with Green Manufacturing Upgrades

Qingdao LNT Chemical represents the high-volume backbone of the global thioglycolic acid supply chain, producing ammonium and sodium thioglycolates at scale. Integration with chloroacetic acid and hydrogen sulfide feedstocks ensures cost competitiveness and supply stability. Investments in H2S recovery systems align with China’s MIIT green manufacturing guidelines, reducing emissions from traditional TGA processes. The company is a major exporter of flotation-grade TGA collectors used in gold, silver, and base metal recovery. Its technical-grade TGA supports global PVC stabilizer and hair care markets. LNT continues to enhance environmental compliance while maintaining pricing leadership in bulk thiochemical supply.

China Thioglycolic Acid Market Anchored in Integrated Feedstock Control and Export-Led Specialties

China’s thioglycolic acid market in 2025–2026 is structurally defined by deep upstream integration and regulatory-driven process optimization. Major chemical clusters in Zhejiang and Shandong have embedded thioglycolic acid production directly within maleic anhydride and acetic acid value chains, materially improving feedstock security and cost predictability. This integration is particularly critical for downstream organotin stabilizer manufacturing, where consistent thioglycolic acid quality is required for PVC vinyl siding and rigid construction profiles supplied to both domestic and export markets.

Regulatory shifts are widening the application base. Mining sector mandates issued in 2025 by the Ministry of Natural Resources are accelerating the replacement of sodium hydrosulfide with sodium thioglycolate in copper and molybdenum flotation, positioning thioglycolic acid derivatives as safer, lower-toxicity depressants. In parallel, industrial upgrading under the 2026 Industrial Modernization Blueprint is pushing producers such as Shanghai Sunwise Chemical toward AI-driven batch control systems capable of producing electronic-grade thioglycolic acid above 99.5% purity. Environmental compliance is also reshaping plant economics. New Yangtze River Delta standards effective January 2026 require advanced oxidative sulfur recovery to manage odor and VOC emissions from mercaptan synthesis, favoring capital-intensive producers with closed-loop recovery infrastructure. Export momentum remains strong, with China consolidating its role as the leading global supplier of thioglycolic acid-based intermediates for cephalosporin antibiotic synthesis, supporting rising shipments to India and Europe through the 2025 fiscal year.

Germany Thioglycolic Acid Market Driven by Specialty Leadership and Circular Chemistry

Germany occupies the premium end of the global thioglycolic acid market, defined by specialty performance, odor reduction, and decarbonization initiatives. The Bruno Bock Group continues to set technical benchmarks, unveiling new low-odor thioglycolic acid derivatives at the European Coatings Show 2025. These grades are tailored for UV-curable coatings and high-performance adhesives, where odor profile and formulation stability are decisive procurement criteria.

Sustainability is increasingly embedded at the asset level. Bruno Bock’s photovoltaic installation at its Marschacht site, commissioned in late 2024, is projected to cut the carbon footprint of energy-intensive distillation operations by approximately 15% by 2026. At the industry level, German producers are piloting bio-derived acetic acid as a precursor to thioglycolic acid to align with EU Green Deal objectives on renewable feedstocks. Circularity is also advancing beyond solvents and energy. In early 2026, BASF SE and regional partners formalized a Ruhr-based recovery loop for thioglycolic acid mercaptide passivators extracted from spent petroleum cracking catalysts, reducing hazardous waste while securing secondary raw material streams.

United States Thioglycolic Acid Market Shaped by Oilfield Demand and PFAS Substitution

In the United States, thioglycolic acid demand is increasingly tied to oilfield chemicals and regulatory-driven material substitution. Expansion of Permian Basin drilling activity through 2025–2026 has driven higher consumption of thioglycolic acid as a ferric ion sequestrant in well stimulation. Its superior performance at temperatures above 70°C has made it a preferred alternative to citric acid in preventing iron precipitation during acidizing operations, particularly in deep and high-temperature reservoirs.

Regulatory developments are opening new downstream channels. As multiple U.S. states tighten restrictions on fluorinated surfactants, thioglycolic acid-based mercapto-functional silanes are gaining adoption as intermediates for PFAS-free water-repellent textile finishes. Compliance obligations are also shaping producer behavior. Under TSCA Section 8(a), thioglycolic acid manufacturers are providing detailed usage and exposure data to regulators, particularly for personal care applications such as depilatories. From a supply chain perspective, 2025 trade realignments have prompted distributors to increase domestic inventories of ammonium thioglycolate to hedge against volatility in Asian logistics corridors.

Canada Thioglycolic Acid Market Defined by Cosmetic Regulation and Mining Applications

Canada’s thioglycolic acid market is undergoing rapid formulation and application realignment following regulatory action in the personal care sector. Health Canada’s August 2025 update to the Cosmetic Ingredient Hotlist imposed a maximum post-oxidation concentration limit of 3% for thioglycolic acid, forcing professional hair care brands and salons to re-engineer formulations within compressed timelines. This shift was reinforced by the progressive prohibition of certain thioglycolic acid esters, including glyceryl thioglycolate, in consumer-grade products due to sensitization risks.

Outside cosmetics, mining is emerging as a stabilizing demand pillar. Under the Critical Minerals Strategy, federal funding in 2025 supported new flotation pilot plants in Ontario that deploy thioglycolic acid-based depressants for nickel extraction. These applications prioritize selective metal separation and reduced environmental toxicity, aligning thioglycolic acid usage with Canada’s broader sustainable mining objectives.

India Thioglycolic Acid Market Accelerated by Import Standardization and Pharma Integration

India’s thioglycolic acid market is transitioning from import dependence toward controlled domestic scaling. The Directorate General of Foreign Trade’s Notification No. 44/2025-26 amended import policies for Chapter 29 chemicals, including mercaptans, with the explicit objective of standardizing thioglycolic acid quality for pharmaceutical and agrochemical use. This move is improving input consistency for downstream formulators while raising compliance thresholds for imported material.

Industrial policy is reinforcing localization. Under the PLI scheme for bulk drugs, Indian producers such as Triveni Chemicals have expanded thioglycolic acid-based pharmaceutical intermediate production to support generic drug manufacturing and reduce reliance on Chinese suppliers. Concurrently, domestic consumption is being lifted by the rapid expansion of the male grooming segment, which is driving localized demand for calcium thioglycolate in depilatory formulations. Together, these trends are positioning India as a structurally more balanced market, combining regulated imports with rising domestic synthesis capacity.

Comparative Snapshot: Thioglycolic Acid Market by Country

Thioglycolic Acid Market County Level Snapshot

|

Country

|

Primary Demand Driver

|

Regulatory or Policy Trigger

|

Structural Impact on TGA Market

|

|

China

|

Integrated PVC and pharma intermediates

|

Mining safety mandates, YRD emission standards

|

Scale-driven, export-oriented production with higher purity grades

|

|

Germany

|

Specialty coatings and adhesives

|

EU Green Deal, circular economy initiatives

|

Premium low-odor and bio-based TGA development

|

|

United States

|

Oilfield chemicals and PFAS substitution

|

TSCA reporting, state surfactant restrictions

|

Growth in high-temperature and PFAS-free applications

|

|

Canada

|

Cosmetics reformulation and mining

|

Cosmetic Ingredient Hotlist updates

|

Shift from consumer esters to regulated professional and mining uses

|

|

India

|

Pharma localization and personal care

|

DGFT import controls, PLI bulk drug policy

|

Expansion of standardized domestic intermediates

|

Thioglycolic Acid Market Report Scope

Thioglycolic Acid Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$148.6 Million

|

|

Market Size (2034)

|

$257.5 Million

|

|

Market Growth Rate

|

6.3%

|

|

Segments

|

By Purity Grade (Technical Grade, High Purity Grade, Pharmaceutical Grade, Electronic Grade), By Product Form (Thioglycolic Acid, Ammonium Thioglycolate, Sodium Thioglycolate, Calcium Thioglycolate, Potassium Thioglycolate, Thioglycolic Acid Esters), By Application (Cosmetics and Personal Care, Mining and Metallurgy, Oil and Gas, Polymer and Plastic Additives, Pharmaceuticals and Fine Chemicals, Other Industrial Applications)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Arkema Group, Bruno Bock Chemische Fabrik GmbH & Co. KG, Daicel Corporation, Merck KGaA, Sasaki Chemical Co., Ltd., Hebei Yanuo Bioscience Co., Ltd., HiMedia Laboratories Pvt. Ltd., Shanghai Sunwise Chemical Co., Ltd., Qingdao Ruchang Mining Industry Co., Ltd., Triveni Chemicals, Everlight Chemical Industrial Corp., Swan Chemical Inc., Qingdao LNT Chemical Co., Ltd., Quadrimex Chemical, Hubei Ge-Wu Chemical Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Thioglycolic Acid Market Segmentation

By Purity Grade

- Technical Grade

- High Purity Grade

- Pharmaceutical Grade

- Electronic Grade

By Product Form

- Thioglycolic Acid

- Ammonium Thioglycolate

- Sodium Thioglycolate

- Calcium Thioglycolate

- Potassium Thioglycolate

- Thioglycolic Acid Esters

By Application

- Cosmetics and Personal Care

- Mining and Metallurgy

- Oil and Gas

- Polymer and Plastic Additives

- Pharmaceuticals and Fine Chemicals

- Other Industrial Applications

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Thioglycolic Acid Market

- Arkema Group

- Bruno Bock Chemische Fabrik GmbH & Co. KG

- Daicel Corporation

- Merck KGaA

- Sasaki Chemical Co., Ltd.

- Hebei Yanuo Bioscience Co., Ltd.

- HiMedia Laboratories Pvt. Ltd.

- Shanghai Sunwise Chemical Co., Ltd.

- Qingdao Ruchang Mining Industry Co., Ltd.

- Triveni Chemicals

- Everlight Chemical Industrial Corp.

- Swan Chemical Inc.

- Qingdao LNT Chemical Co., Ltd.

- Quadrimex Chemical

- Hubei Ge-Wu Chemical Co., Ltd.

*- List not Exhaustive