Naphthenic Acid Market 2025–2034: High-TAN Crude Processing, Metal Naphthenate Expansion, and Energy-Transition Applications

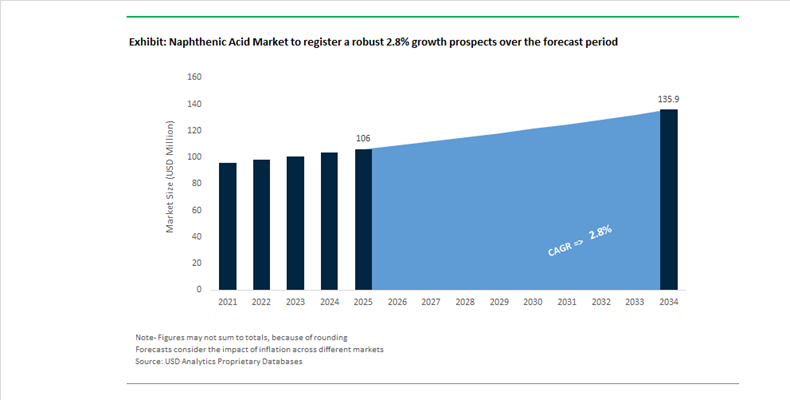

The Naphthenic Acid Market is projected to grow from $106 Million in 2025 to $135.9 Million by 2034, reflecting a moderate CAGR of 2.8%. Market performance is closely tied to global crude slate composition, refinery complexity upgrades, and downstream demand for metal naphthenates and specialty naphthenic oils. As refiners increasingly process high-TAN (Total Acid Number) crudes to optimize feedstock economics, the recovery and upgrading of naphthenic acids has shifted from a corrosion management issue to a value-extraction opportunity. The market today spans two core verticals: acid extraction technologies integrated into refinery systems, and downstream chemical derivatives such as metal naphthenates used in coatings, inks, catalysts, wood preservatives, and polymerization systems.

Technology-driven consolidation is reshaping upstream processing. In early 2024, Merichem Technologies expanded its acid and sulfur treatment capabilities through the acquisition of Chemical Products Industries. This move strengthened Merichem’s licensing position in high-TAN crude processing and acid removal systems. In parallel, Black Bay Energy Capital acquired Merichem’s Process Technologies & Catalyst business, enabling a sharper focus on proprietary systems such as NAPFINING™, widely deployed for removing naphthenic acids from jet fuel and diesel streams. At India Energy Week 2026, Merichem emphasized the “beneficial reuse” of recovered acids, signaling a structural shift: refineries are increasingly monetizing extracted naphthenic acids rather than treating them purely as contaminants.

Downstream, metal naphthenates remain central to coatings and polyester resin catalysis. In June 2024, Umicore expanded its metal naphthenate production capacity in Belgium to meet rising demand for high-performance driers and catalysts. These derivatives are essential in accelerating oxidative curing reactions in alkyd paints and improving crosslinking efficiency in resin systems. The expansion reflects sustained growth in architectural coatings, marine paints, and industrial inks, particularly in emerging economies. Regulatory scrutiny on heavy metals is, however, encouraging innovation in cobalt-free and low-toxicity alternatives, influencing formulation strategies across Europe and Japan.

Specialty oil producers are also repositioning around sustainability. In May 2024, Nynas achieved a monthly production record of 42,000 metric tons of naphthenic oils at its Nynäshamn refinery, underscoring its strategic pivot away from fuels toward high-margin specialty segments. In October 2025, Nynas secured an EcoVadis Platinum rating, reinforcing lifecycle transparency as a competitive differentiator. The company delivered nearly 700 metric tons of NYTRO® Lyra X transformer oil in January 2026 to Poland’s largest offshore wind project, demonstrating ongoing reliance on naphthenic-based dielectric fluids for renewable infrastructure. Simultaneously, the November 2025 commercialization of NYTRO® BIO 300X—a bio-based transformer fluid—illustrates a gradual transition toward renewable feedstocks while preserving the low pour point and high solvency characteristics typical of naphthenic derivatives.

Regulatory frameworks continue to influence regional supply. Japan’s 2026 chemical substance process, announced by METI in December 2025, introduces updated reporting obligations for specialized naphthenate derivatives used in electronics and medical devices. Meanwhile, Nynas’ February 2026 pilot for permanent CO₂ storage at Nynäshamn highlights the decarbonization imperative within hydrogen-intensive refining operations.

Through 2034, market growth will remain steady but constrained by substitution risks, bio-based transformer fluids, and tighter environmental oversight. However, the continued processing of high-acidity crudes, expansion of specialty coatings demand, and renewable energy grid investments will sustain structural demand for naphthenic acids and their derivatives.

Naphthenic Acid Market Trends and Opportunities

Trend: Capacity Expansion for Battery-Grade Naphthenic Acid in Advanced Lithium-Ion Chemistries

The naphthenic acid market is undergoing a structural upgrade as battery manufacturers push toward high-nickel and high-voltage lithium-ion chemistries. Lithium naphthenate is increasingly deployed as a functional electrolyte additive, where purity levels above 99% are critical to stabilizing the solid-electrolyte interphase and extending cycle life in electric vehicle battery systems. As EV OEMs transition to NMC 811 and other nickel-rich cathode formulations, electrolyte stability has become a decisive performance lever rather than a secondary formulation variable.

Late-2024 performance studies demonstrate that naphthenate-based additives can reduce initial impedance in high-nickel cathode systems by roughly 15 to 20%, directly mitigating resistive surface film formation during early charge cycles. This improvement addresses long-standing energy fade challenges associated with 4.5V and higher operating voltages. In the 2025 commercial landscape, refined naphthenic acid grades with low unsaponifiable content are increasingly dominant, particularly because lithium salts derived from these grades enhance low-temperature discharge performance by approximately 5 to 8% versus conventional electrolyte baselines.

To capture this demand, producers are investing in multi-stage distillation and proprietary purification technologies. Companies such as Merichem and Umicore have announced initiatives to integrate naphthenic acid derivatives directly into closed-loop cathode material supply chains. These moves are strategically aligned with the more than 700 GWh of lithium-ion battery capacity currently under construction across North America and Asia, where long-term feedstock security and trace impurity control are now procurement prerequisites rather than value adds.

Trend: Consolidation and Vertical Integration in Copper Naphthenate Wood Preservation

Regulatory pressure on legacy wood preservatives is reshaping demand dynamics for naphthenic acid in industrial treatment applications. As chromated copper arsenate, creosote, and pentachlorophenol face increasing restrictions for residential and sensitive-use scenarios, copper naphthenate has emerged as the preferred general-use preservative with a comparatively benign regulatory profile. This shift has tightened supply conditions and triggered consolidation across the wood preservation value chain.

Updated EPA reregistration decisions in August 2025 reaffirmed copper naphthenate as a non-restricted use pesticide, accelerating adoption by utilities and infrastructure operators. Major power companies have increasingly standardized copper naphthenate-treated poles, citing documented service lifetimes ranging from 35 to 80 years under proper treatment conditions. As a result, oil-borne copper naphthenate demand is projected to rise by 10 to 12% in regions enforcing stricter leaching and environmental compliance standards.

Vertical integration has become a defining competitive strategy. During 2024 and 2025, Koppers Inc. completed the acquisition of Brown Wood Preserving Company, reinforcing its position as a fully integrated producer of both wood treatment chemicals and treated products. This consolidation allows Koppers to secure captive naphthenic acid supply while controlling formulation consistency across utility poles, marine pilings, and industrial timber segments. Copper-based preservatives now account for roughly 45% of construction wood treatments and about 20% of marine applications, underscoring the structural nature of this demand shift.

Opportunity: Bio-Derived Naphthenic Acids for Environmentally Acceptable Lubricants

Maritime and offshore regulations are opening a high-value opportunity for bio-based naphthenic acid analogues in environmentally acceptable lubricants. Under U.S. Vessel General Permit and VIDA frameworks, as well as IMO-aligned international standards, lubricants used in stern tubes, thrusters, and deck machinery must meet strict biodegradability and aquatic toxicity thresholds. This has elevated demand for naphthenate-based rust inhibitors and emulsifiers that can deliver performance parity with petroleum-derived products.

To qualify as environmentally acceptable, lubricants must achieve more than 60% biodegradation within 28 days. In 2025, both startups and established marine lubricant suppliers began scaling enzymatically synthesized and bio-derived naphthenic acid alternatives that retain metal-binding efficiency while dramatically lowering aquatic toxicity. The economic incentive is significant: commercial vessels conduct over 1.7 million port visits annually, with stern tube leakage estimated at up to tens of millions of liters of oil per year. Environmental discharge penalties in monitored waters can exceed $50,000 per violation, making compliant lubricants a risk mitigation tool rather than a discretionary upgrade.

Beyond fluids, bio-synthetic naphthenates are also gaining traction in environmentally acceptable greases. These formulations demonstrate reliable extreme-pressure performance while meeting Green Seal and LEED-aligned procurement requirements for forestry, port equipment, and marine heavy machinery, positioning bio-derived naphthenic acids as a growth pillar within sustainable industrial lubrication.

Opportunity: Critical Mineral Extraction and E-Waste Recycling via Selective Chelation

Naphthenic acid is increasingly being evaluated as a selective solvent extraction agent in hydrometallurgical circuits supporting the circular economy. Its ability to chelate copper, cobalt, and nickel makes it particularly valuable for recovering metals from mine tailings and end-of-life electronics, where conventional smelting routes are energy-intensive and environmentally burdensome.

A February 2025 study published in Separations highlighted that optimized naphthenic acid-based leaching systems can achieve over 90% extraction efficiency for copper and nickel from reprocessed tailings. This capability is attracting attention as governments and mining companies reassess tailings as secondary resources rather than liabilities. In parallel, the U.S. International Trade Commission has emphasized the strategic importance of domestic recovery of rare earth elements from E-waste to reduce reliance on imports. Pilot extraction circuits using naphthenic acid are being tested to recover neodymium and dysprosium from shredded permanent magnets, offering a cleaner alternative to pyrometallurgical recovery.

Naphthenic Acid Market Share and Segmentation Insights

Refined Naphthenic Acid Leads the Market Through Balanced Purity and Industrial Performance

Refined naphthenic acid accounted for 52.80% of the Naphthenic Acid Market share in 2025, establishing it as the most widely used form of naphthenic acid across industrial chemical applications. Refined grades provide a balanced combination of consistent purity, stable chemical composition, and cost efficiency, making them suitable for large-scale manufacturing uses including paint driers, fuel additives, lubricant additives, rubber compounding agents, and metal treatment chemicals. Compared with crude naphthenic acid, refined grades offer improved color, reduced impurities, and more predictable chemical behavior, which are essential for formulation stability in industrial applications. However, they remain significantly more economical than high-purity grades designed for specialized uses. In 2025, many producers have shifted their strategy toward forward integration into higher-value naphthenate derivatives, including cobalt, manganese, zinc, and copper naphthenates used in coatings, catalysts, and corrosion inhibitors. This integration allows manufacturers to capture greater value across the supply chain while stabilizing demand for refined naphthenic acid as a key intermediate in metal-based chemical additives.

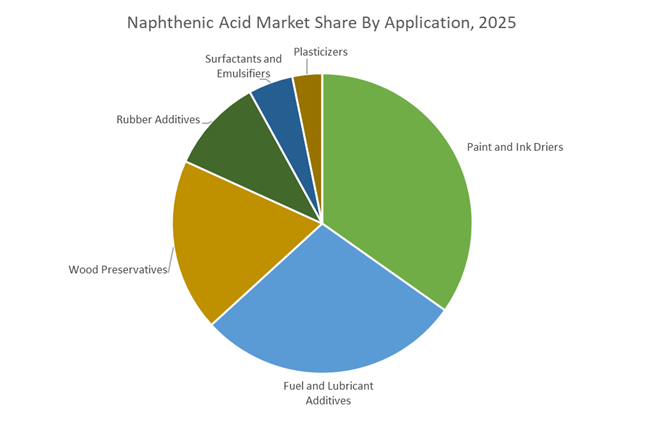

Paint and Ink Driers Drive the Largest Demand for Naphthenic Acid Derivatives

Paint and ink driers accounted for 34.80% of the Naphthenic Acid Market share in 2025, making the coatings and printing industries the largest consumers of naphthenic acid derivatives. Naphthenic acid is primarily converted into metal naphthenates such as cobalt naphthenate, manganese naphthenate, zirconium naphthenate, and calcium naphthenate, which function as catalytic drying agents in solvent-based alkyd coatings and printing inks. These metal driers accelerate oxidative polymerization reactions during coating curing, enabling faster drying times and improved film formation in paints used for architectural coatings, industrial equipment finishes, and printing applications. The global scale of the coatings industry continues to support strong demand for these additives across construction, automotive refinishing, and packaging printing sectors. In 2025, regulatory scrutiny surrounding cobalt-based drying catalysts has encouraged coatings manufacturers to explore alternative metal drier systems using manganese and iron naphthenates. Despite this shift, cobalt naphthenate continues to dominate in high-performance coatings due to its superior catalytic efficiency, while substitution efforts remain focused primarily on less demanding coating applications.

Naphthenic Acid Market Competitive Landscape

The naphthenic acid market in 2026 is driven by high-purity refined grades (Acid Number >240), PAH reduction, and circular recovery technologies. Competitive advantage centers on modular extraction systems, downstream metal naphthenates, and integration with high-TAN crude refining and specialty lubricant applications.

Merichem leads circular recovery and high-purity naphthenic acid extraction with modular refinery solutions

Merichem Technologies dominates the naphthenic acid market by combining technology licensing with merchant production of refined, low-PAH acids. Its skid-mounted caustic treatment systems enable on-site recovery of naphthenic acids from refinery waste streams, reducing logistics costs and enhancing circularity. At AFPM 2026, Merichem highlighted integrated H₂S removal and acid recovery systems that align with tightening sulfur emission regulations. Its “Renewables on the Rise” initiative extends its treating technologies into biofuel purification, expanding application scope. The company’s sustainability scorecard reinforces its position as a preferred partner for refinery decarbonization. Its expertise in modular systems and waste valorization secures leadership in high-purity segments.

Umicore drives value-added metal naphthenates for wood preservation and high-performance lubricant additives

Umicore leverages its downstream integration to convert naphthenic acid into high-value metal naphthenates, including copper, zinc, and bismuth variants. Copper naphthenate is widely adopted as a safer alternative to creosote in wood preservation, offering deep penetration and lower toxicity. The company is expanding bismuth-based additives for extreme pressure (EP) lubrication, replacing lead-based chemistries in industrial greases. Umicore emphasizes biodegradable sourcing, aligning with environmental standards across Europe and North America. Its integrated production model ensures consistent purity and performance for coatings, marine antifouling, and automotive driers. This focus on specialty derivatives positions Umicore in high-margin downstream applications.

ExxonMobil maximizes refinery integration to supply high-performance naphthenic fluids for energy and industrial systems

ExxonMobil Product Solutions utilizes its extensive refining infrastructure to produce high-purity naphthenic fluids for energy-grade applications. Its Univolt™ transformer oils deliver superior dielectric performance and thermal stability, supporting global grid modernization. The Escaid™ fluids portfolio is optimized for lithium-ion battery recycling and solvent extraction mining, leveraging naphthenic-rich compositions for safety and efficiency. ExxonMobil’s crude-to-chemicals strategy enhances yield optimization of specialty solvents and cycloparaffinic products. Strategic realignment toward Gulf Coast operations strengthens integration with high-TAN crude processing. Its scale, feedstock access, and advanced distillation capabilities reinforce leadership in energy and industrial applications.

Nichem develops niche naphthenic-based specialty chemicals for polymer performance and sustainable applications

Nichem Solutions is emerging as an innovation-driven player focused on niche, high-value applications of naphthenic chemistry. Its R&D-driven model enables the development of polymer additives with antimicrobial and anti-rodent properties for infrastructure protection. The company’s backward integration approach aligns chemical synthesis with application-specific performance requirements. With patented technologies and rapid expansion into global markets, Nichem is targeting sustainable polymer solutions and recycling-enhancing additives. Its portfolio emphasizes non-toxic, eco-friendly formulations for industrial coatings and water conservation. This specialization in customized chemistry differentiates Nichem in the specialty segment.

Sea-Land enhances naphthenic acid adoption through formulation expertise and specialty additive distribution

Sea-Land Chemical Company plays a strategic role as a formulation partner and distributor of naphthenic acid-based additives. Its Innovation Lab provides customized solutions for lubricants, metalworking fluids, and CASE applications, optimizing dosage and performance characteristics. The company is guiding customers through PFAS replacement strategies, positioning naphthenic intermediates as low-VOC alternatives in industrial formulations. Its portfolio includes natural sodium sulfonates and dispersants tailored for coatings and adhesives. Sea-Land’s technical specialists collaborate directly with manufacturers to solve complex formulation challenges. This customer-centric, solution-based approach strengthens its position in mid-market and specialty chemical distribution.

China: Refinery Consolidation, Purity Uplift, and Export-Grade Wood Preservation

China’s naphthenic acid landscape is being reshaped by a structural pivot toward chemical-grade refining under the Ministry of Industry and Information Technology Workplan for Stable Growth in the Petrochemical and Chemical Industry. As refiners reallocate capacity away from diesel toward higher-value petrochemicals in 2025–2026, the localized extraction of crude naphthenic acids as refinery byproducts is accelerating. This transition is reinforced by a regulatory hard cap on refining capacity effective January 2026, which phases out sub-scale “teapot” refineries below 2 million tonnes per year. The result is a concentration of naphthenic acid production within large, state-owned complexes operated by Sinopec and PetroChina, improving consistency in acid number profiles and overall yield.

Quality and downstream compatibility are emerging as strategic priorities. Sinopec’s Q3 2025 disclosures confirmed a 1.38 billion yuan investment in environmental and technical upgrades, including advanced distillation columns capable of producing refined naphthenic acid at 99% or higher purity. These upgrades directly reduce dependence on imported high-grade material for semiconductor processing and pharmaceutical intermediates. At the application level, China’s furniture manufacturing rebound in late 2025 is creating incremental demand for naphthenate-based wood preservatives, particularly for export-oriented timber that must comply with international anti-decay and durability standards.

United States: Regulatory Tightening, Pricing Realignment, and Fuel Additive Demand

In the United States, the naphthenic acid market is being shaped by regulatory scrutiny and downstream resilience. Under updated TSCA Section 6 risk evaluations, the Environmental Protection Agency is expected to introduce stricter workplace chemical protection programs by mid-2026. These measures are pushing formulators toward low-VOC naphthenic acid derivatives in industrial paints and coatings, particularly in applications with prolonged worker exposure. At the same time, supply-side stability was supported in May 2025 when Ergon Inc. reduced naphthenic oil prices by $0.20 per gallon across North America, a move designed to cushion downstream metal naphthenate producers against crude feedstock volatility.

Environmental compliance is also driving innovation. Department of Energy–funded research in 2025 demonstrated the viability of constructed wetland treatment systems for degrading naphthenic acids in process-affected water. Pilot deployments at Gulf Coast refining sites are now being evaluated against 2026 Clean Water Act discharge requirements. On the demand side, U.S. aviation and defense procurement remains a notable growth lever. Fleet expansion in 2025 drove a measurable increase in naphthenic acid consumption as a jet fuel additive, where it functions as a corrosion inhibitor and fuel stability enhancer for long-range military aircraft.

Belgium: Catalyst Intermediates and Circular Feedstock Recovery

Belgium occupies a specialized position in the European naphthenic acid value chain, anchored in metal naphthenates and high-efficiency intermediates. Umicore’s facility expansion, completed in mid-2024 and fully ramped by Q1 2025, strengthened regional capacity for catalyst-grade and specialty chemical derivatives based on refined naphthenic acid. This expansion aligns Belgium with high-margin downstream segments rather than bulk consumption.

Sustainability is reinforcing this positioning. In line with the EU Circular Economy Action Plan, Belgian producers are piloting closed-loop recovery of refined naphthenic acids from spent lubricants. These initiatives are projected to reduce virgin feedstock requirements for industrial coatings by roughly 12% by late 2026, while also improving lifecycle compliance for customers operating under tightening EU environmental standards.

Canada: Tailings Remediation and Infrastructure-Driven Wood Preservation

Canada’s naphthenic acid market is closely linked to oil sands operations and infrastructure policy. Following Alberta Energy Regulator directives issued in 2025, operators have deployed NAPFINING caustic extraction technology to remove naphthenic acids from tailings ponds. This approach enables effective acid recovery from heavy crudes and condensates without forming persistent emulsions, addressing a long-standing environmental liability while creating a secondary supply stream.

Downstream, infrastructure renewal programs in 2025 have shifted timber preservation standards. Copper naphthenate is increasingly specified for utility poles and railroad ties, displacing creosote due to its lower environmental toxicity and superior penetration characteristics. This regulatory-driven substitution is reinforcing stable domestic demand for naphthenic acid derivatives in Canada’s construction and transport networks.

India: Cluster Investments and Trade Reorientation

India’s naphthenic acid dynamics are defined by cluster-based investments and evolving trade exposure. In May 2025, Gujarat Alkalies and Chemicals Limited announced an ₹81 crore investment at the Dahej chemical cluster to optimize downstream units capable of handling naphthalene and naphthenic derivatives. These assets are being aligned with domestic agrochemical and textile dye requirements, where naphthenic intermediates support formulation performance and dispersion efficiency.

Despite these investments, India remains structurally dependent on imported naphthenic feedstocks from the United States and the Middle East. Anticipated trade policy shifts during 2025–2026, including the possibility of tariffs on select U.S. chemical goods, are forcing Indian formulators to diversify sourcing toward Asian refining hubs such as Singapore and South Korea. This reorientation is reshaping procurement strategies and increasing the importance of consistent purity specifications in imported material.

Snapshot Summary: Naphthenic Acid Market Positioning by Country

Naphthenic Acid Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Structural Shift

|

Market Implication

|

|

China

|

Refining consolidation and oil-to-chemical pivot

|

Centralized, high-purity production

|

Reduced imports, stronger export-grade applications

|

|

United States

|

TSCA compliance and aviation demand

|

Low-VOC reformulation and fuel additive pull

|

Stable specialty demand with environmental upgrades

|

|

Belgium

|

Specialty intermediates and circularity

|

Closed-loop recovery from lubricants

|

Higher-margin, sustainability-led positioning

|

|

Canada

|

Tailings remediation and infrastructure policy

|

Acid recovery and copper naphthenate substitution

|

Environmentally driven domestic demand

|

|

India

|

Cluster investment and trade shifts

|

Import diversification and local optimization

|

Increased sensitivity to purity and sourcing

|

Naphthenic Acid Market Report Scope

Naphthenic Acid Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$106 Million

|

|

Market Size (2034)

|

$135.9 Million

|

|

Market Growth Rate

|

2.8%

|

|

Segments

|

By Type (Refined Naphthenic Acid, High-Purity Naphthenic Acid, Crude Naphthenic Acid), By Application (Paint and Ink Driers, Wood Preservatives, Fuel and Lubricant Additives, Rubber Additives, Surfactants and Emulsifiers, Plasticizers), By End-Use Industry (Automotive and Transportation, Construction and Infrastructure, Aerospace and Defense, Agrochemicals, Pharmaceuticals and Personal Care)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Merichem Technologies, Umicore, Sinopec, Ergon, Nynas, Fulltime Chemical, Sea Chemical, Midas International, Changfeng Chemical, Zhangming Chemical, Rare-Earth Chemical, Triveni Chemicals, A B Enterprises, Lok Chemicals, Deepak Chem Tex

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Naphthenic Acid Market Segmentation

By Type

- Refined Naphthenic Acid

- High-Purity Naphthenic Acid

- Crude Naphthenic Acid

By Application

- Paint and Ink Driers

- Wood Preservatives

- Fuel and Lubricant Additives

- Rubber Additives

- Surfactants and Emulsifiers

- Plasticizers

By End-Use Industry

- Automotive and Transportation

- Construction and Infrastructure

- Aerospace and Defense

- Agrochemicals

- Pharmaceuticals and Personal Care

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Naphthenic Acid Market

- Merichem Technologies

- Umicore

- Sinopec

- Ergon

- Nynas

- Fulltime Chemical

- Sea Chemical

- Midas International

- Changfeng Chemical

- Zhangming Chemical

- Rare-Earth Chemical

- Triveni Chemicals

- A B Enterprises

- Lok Chemicals

- Deepak Chem Tex

*- List not Exhaustive