Near Infrared Absorbing Materials Market Overview — Precision Optics, Thermal Control, and Security Durability Driving Scalable Demand

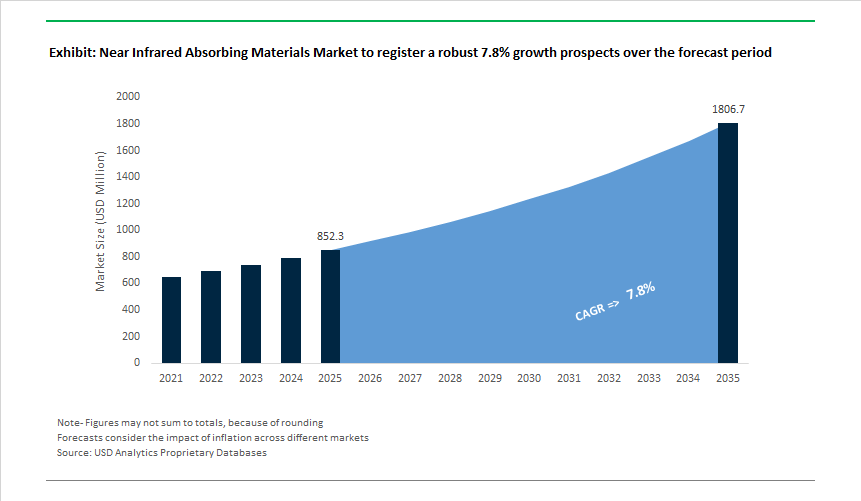

Market Value (2025): USD 852.3 Million | CAGR (2025–2035): 7.8% | Forecast Value (2035): USD 1,806.3 Million

The Near Infrared (NIR) Absorbing Materials Market is transitioning from a niche optical additives segment into a performance-critical materials category underpinning smartphone imaging, automotive glazing, semiconductor packaging, security printing, and defense stealth systems. Market expansion is directly linked to tighter wavelength control requirements, rising thermal management mandates, and the integration of NIR functionality into mass-produced consumer and infrastructure products. For manufacturers, competitive positioning increasingly depends on absorption precision, long-term optical stability, and compatibility with high-volume coating, printing, and glass-processing platforms.

A defining shift in 2025 is the move toward narrow-band NIR absorption, with leading dye and pigment suppliers achieving Full Width at Half Maximum (FWHM) below 30 nm. This precision is now a gating requirement in optical filter stacks used for smartphone 3D sensing, facial recognition, and LiDAR, where interference with the visible spectrum must be minimized while maintaining high infrared attenuation. In parallel, miniaturization pressure in CMOS image sensors has elevated demand for NIR-absorbing photoresists and wave-control materials that enable ~25% pixel pitch reduction without increasing module thickness—directly supporting higher resolution and low-light imaging performance.

Thermal management and energy efficiency represent the second major demand pillar. Cesium-doped Tungsten Oxide (CWO) and Lanthanum Hexaboride (LaB₆) nanoparticles used in architectural and automotive glazing now routinely deliver >90% Infrared Rejection (IRR) while preserving >70% Visible Light Transmittance (VLT). This performance ratio has become a benchmark for green building certification compliance and heat-load reduction strategies in warm-climate urban infrastructure. At the same time, security inks and defense coatings increasingly specify organic NIR absorbers capable of surviving 2,000+ hours of QUV accelerated weathering with <5% absorption loss, establishing lightfastness as a non-negotiable procurement criterion for banknotes, passports, and camouflage systems.

Near Infrared Absorbing Materials Market Analysis — Optical Innovation, Space-Grade Stability, and Energy Efficiency Investments

The market landscape has been shaped by a sequence of high-impact product launches and manufacturing investments that underscore the strategic importance of NIR absorbing materials across electronics, space, energy, and infrastructure sectors. In December 2025, Fujifilm Corporation announced the global launch of its WAVE CONTROL MOSAIC™ color filter material—the world’s first KrF-compatible, PFAS-free solution for high-sensitivity image sensors. The material is engineered to enhance infrared photography in smartphone cameras while aligning with tightening environmental regulations, reinforcing Fujifilm’s leadership in optical materials for mobile imaging.

Space and satellite applications also advanced significantly. In November 2025, SCHOTT introduced Solar Glass exos, developed in collaboration with the European Space Agency, offering optimized UV/NIR absorption and optical stability under extreme radiation exposure. This development highlights the growing role of NIR-tuned glass in next-generation satellite solar cells and aerospace optics. Earlier, in June 2025, SCHOTT enabled a major improvement in low-light photography for the OPPO Find X8 Ultra by supplying a specialized NIR-cut filter glass that boosted infrared absorption efficiency by 81%, demonstrating how incremental optical gains translate into measurable consumer-device performance improvements.

Materials innovation extended into energy efficiency and electronics manufacturing. In October 2025, Sumitomo Metal Mining detailed the scaling of its SOLAMENT technology, which incorporates NIR-absorbing nanoparticles into heat-generating apparel and agricultural films—applications that convert absorbed infrared energy into functional heat output. This was complemented in September 2025 by the company’s development of a 100 nm nano copper powder with high oxidation resistance, enabling conductive and NIR-reflective pastes for advanced electronics. Meanwhile, in March 2025, AGC Inc. inaugurated a refurbished flat-glass production line in Europe, deploying a world-first low-carbon manufacturing technology to supply high-performance, NIR-optimized glazing for the energy-efficiency market—signaling that sustainability and optical performance are now being scaled simultaneously at the manufacturing level.

Near Infrared Absorbing Materials Market Trends and Opportunities

Trend 1: High-Thermal-Stability NIR Dyes for Advanced Semiconductor Patterning

As logic and memory nodes push below 3 nm, semiconductor manufacturers are confronting a non-obvious bottleneck: spectral drift and chemical instability of NIR absorbers during high-temperature processing. Photoresist underlayers and bottom anti-reflective coatings (BARCs) must now tolerate bake and plasma steps that routinely exceed 280–300°C without decomposition, outgassing, or wavelength shift.

Recent breakthroughs reported in 2025 demonstrate that heptamethine cyanine dyes paired with bistriflimide anions can surpass 300°C thermal stability, a threshold that materially reduces defect formation during annealing and dry etch steps. This is strategically important because even trace outgassing at these nodes can cause line-edge roughness and critical dimension (CD) variation—yield killers at sub-3 nm geometries.

Performance is also improving at the molecular efficiency level. Pyrrole-based NIR absorbers are now achieving molar extinction coefficients approaching 6.9×10⁴ L/mol·cm, roughly 4–5× higher than legacy blue or visible-range dyes. This allows fabs to deploy thinner absorber layers, directly supporting pixel miniaturization in CMOS image sensors and tighter overlay control in advanced logic.

Parallel to organic systems, inorganic CuS-based NIR-absorbing thin films fabricated via high-temperature spray pyrolysis (≈400°C) are gaining traction for optoelectronic patterning. These films maintain stable bandgaps (≈2.10–2.26 eV) and carrier mobility under thermal stress, positioning them as candidates for next-generation hybrid resist stacks where organic dyes alone cannot meet durability requirements.

Trend 2: Engineering of Biocompatible NIR-II Absorbers for Precision Medical Therapies

Medical R&D is decisively shifting from the conventional NIR-I window toward the NIR-II range (1000–1700 nm), where deeper tissue penetration and reduced autofluorescence dramatically improve therapeutic precision. This trend is redefining NIR absorbers from imaging aids into active therapeutic actuators.

In 2025, nitrogen/oxygen co-doped carbon dots (N-O-CDs) demonstrated photothermal conversion efficiencies of ~38%, enabling effective tumor ablation at relatively low laser power densities (≈0.8 W/cm²). This efficiency is not incremental—it materially reduces collateral tissue damage while enabling combined imaging and therapy within a single material platform.

Targeted nano-prodrug systems are reinforcing this shift. Late-2024 and 2025 clinical research showed that PA1094 dye-loaded PLGA nanoparticles, when conjugated with immune-modulating antibodies, can trigger pyroptotic cell death under NIR-II illumination. The implication is strategic: NIR absorbers are becoming immuno-oncology enablers.

From a regulatory standpoint, the continued clinical relevance of the AuroLase platform underscores regulatory confidence in NIR-absorbing nanomaterials. Follow-on feasibility studies in 2025 for NIR-activated hydrogel patches in dermatologic oncology signal a widening approval pathway for “light-triggered” material systems in mainstream care.

Opportunity 1: Laser-Protective Coatings for Domestic Semiconductor Tooling

The reshoring of semiconductor manufacturing under the U.S. CHIPS and Science Act is creating a non-cyclical demand pocket for NIR absorbers embedded in laser-protective optics and lithography tooling. Advanced fabs rely heavily on laser-based alignment, metrology, and emerging EUV-adjacent light sources, all of which require high-LIDT (Laser-Induced Damage Threshold) materials.

In December 2025, the U.S. Department of Commerce announced a letter of intent with xLight to develop a domestic free-electron laser prototype for next-generation lithography. FEL architectures generate intense stray radiation across the NIR spectrum, creating a direct need for thermally resilient, spectrally selective NIR-absorbing coatings to protect optics and sensors.

Simultaneously, U.S. legislation aimed at excluding non-allied chipmaking equipment is forcing fabs to localize sourcing of optical filters and shielding windows. Suppliers such as SCHOTT are scaling advanced hard-coat optical stacks that integrate NIR absorbers capable of maintaining stable transmission under continuous high-power laser exposure. These coatings are no longer discretionary—they are essential to tool uptime, yield protection, and regulatory compliance.

Opportunity 2: Spectral-Selective Films for Smart Greenhouse Photonics

Precision agriculture is emerging as a volume-driven downstream opportunity for NIR-absorbing materials, particularly in climate-controlled greenhouses where energy efficiency directly affects operating margins. The objective is not full shading, but selective suppression of heat-generating NIR wavelengths while preserving photosynthetically active radiation (PAR).

Studies from 2024–2025 show that ZnO-filled and silica-based NIR-selective films can block thermal radiation while maintaining near-100% PAR transmittance. This enables passive cooling without compromising plant growth—an increasingly valuable capability as energy prices and water scarcity intensify.

More advanced deployments are integrating quantum and nonlinear metamaterial additives into greenhouse covers, allowing growers to fine-tune spectral transmission. Field data indicates that these films can reduce internal temperatures by several degrees Celsius, translating into 20–30% HVAC energy savings in indoor farming operations.

Durability is becoming a key differentiator. To withstand prolonged UV exposure, suppliers are formulating UV-stabilized NIR-absorbing additives for PE and PVC films, enabling long service life in harsh agricultural environments. These “smart covers” are evolving into agronomic tools—actively influencing transpiration rates, crop metabolism, and water efficiency rather than merely providing thermal comfort.

Market Share Analysis: Near Infrared Absorbing Materials Market

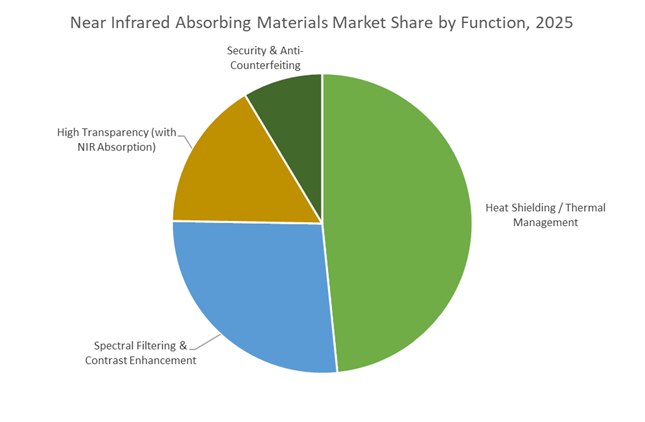

Market Share by Function: Heat Shielding and Thermal Management as the Core Demand Driver

Heat shielding and thermal management applications account for approximately 45% of the Near Infrared (NIR) absorbing materials market, reflecting their central role in controlling solar heat gain without compromising optical clarity or connectivity. This segment dominates because NIR-absorbing materials address a structural inefficiency in modern design: nearly 40% of solar energy is concentrated in the 800–1,200 nm band, which directly drives interior temperature rise in vehicles and buildings. Advanced nano-ceramic and cesium tungsten oxide (CWO) materials selectively absorb this thermal wavelength range while remaining transparent in the visible spectrum, allowing manufacturers to lower surface and cabin temperatures by 10–15°C without darker tinting. The segment’s leadership is further reinforced by dosage efficiency economics—CWO-based absorbers achieve equivalent or superior infrared rejection at 1/6 to 1/50 the loading of legacy ITO or ATO materials, significantly reducing formulation costs and dispersion complexity. From a durability perspective, next-generation NIR heat-shielding films engineered for 3,000+ hours of thermal stability at 175°C enable adoption in high-stress automotive and industrial environments where polymer degradation would otherwise limit lifespan. As energy efficiency standards tighten globally and EV thermal loads intensify, heat-shielding functionality has moved from a comfort upgrade to a system-level thermal management requirement, anchoring its position as the largest functional segment in the NIR absorbing materials market.

Market Share by Application: Automotive as the Primary Commercialization Engine

The automotive sector represents roughly 35% of total NIR absorbing materials demand, making it the largest end-use application and the fastest route to scale for material suppliers. This dominance is driven by a convergence of electrification, passenger comfort expectations, and energy efficiency mandates. In electric vehicles, solar heat gain directly increases HVAC power draw; NIR-absorbing glazing and coatings reduce cooling loads by up to 20%, translating into a 5–10% real-world driving range extension during peak thermal conditions—one of the most compelling ROI metrics for OEMs battling range anxiety. The shift toward metal-free, signal-transparent NIR materials has further accelerated adoption, as modern vehicles rely on uninterrupted 5G, GPS, and vehicle-to-everything (V2X) communication; non-metallized nano-ceramic films now deliver 99% UV rejection with zero signal interference, eliminating a major historical trade-off. Beyond glazing, high-temperature-stable NIR polymers are increasingly specified for automotive displays, sensor housings, and Li-Fi-enabled optical communication modules, where resistance to warping above 250°C ensures manufacturing yield stability. As EV platforms evolve toward integrated thermal and electronic architectures, automotive applications continue to anchor volume growth and validate NIR absorbing materials as a critical enabler of next-generation vehicle efficiency and comfort.

China: Zero-Carbon Industrial Parks Driving Inorganic NIR Scale

China continues to dominate global supply of inorganic NIR absorbers as 2025 policy shifts convert sustainability targets into mandatory deployment. In June 2025, the National Development and Reform Commission and Ministry of Industry and Information Technology jointly launched the Zero-Carbon Industrial Park mandate, requiring ultra-efficient factory envelopes. This directive has triggered large-volume adoption of CsWO₃- and ATO-based NIR-absorbing window coatings to suppress solar heat gain while preserving visible light transmission—directly reducing HVAC energy intensity across state-led infrastructure.

Complementing policy enforcement, MIIT’s August 2025 polysilicon inspection program tightened energy audits across 41 producers, indirectly accelerating the use of NIR-active pigments in tandem organic photovoltaics to boost conversion efficiency. On the innovation front, Nanjing University unveiled a colorless unidirectional diffractive solar concentrator (CUSC) in September 2025, using cholesteric liquid crystals to channel NIR photons to edge-mounted PV cells—transforming glazing into power-generating surfaces with 18.1% overall efficiency.

United States: CHIPS Act Pull-Through for LiDAR and Defense Optics

The U.S. NIR market is being pulled forward by semiconductor security and defense optics rather than architectural retrofits. In March 2025, the U.S. Department of Commerce established the Investment Accelerator Office to fast-track CHIPS-funded projects, prioritizing domestic optical filters and NIR-selective coatings critical for semiconductor manufacturing resilience.

Supply security intensified with Spring 2025 executive orders to expand domestic access to rare-earth precursors for lanthanide-doped NIR absorbers (notably Sm and Yb) used in LiDAR interference mitigation and thermal masking. Reinforcing circularity, the U.S. Department of Energy announced $134 million (December 2025) to commercialize rare-earth recovery from e-waste—creating a secondary feedstock stream for inorganic NIR nanoparticles aligned with defense and aerospace requirements.

Japan: GX 2040 and Fineceramic Leadership

Japan leads in high-purity cesium tungsten bronze and organic NIR dyes, anchored by its GX 2040 Vision (Cabinet-approved January 2025). This policy channels R&D subsidies toward carbon-neutral fineceramic manufacturing, enabling producers such as Sumitomo Metal Mining and Resonac to scale low-carbon synthesis of NIR-blocking oxides.

Market pull is strongest in automotive glazing, where the Ministry of the Environment, Japan feed-in frameworks have accelerated nanostructured metal-oxide films that extend EV range by lowering cabin cooling loads. In parallel, the Japan Science and Technology Agency reported 2025 milestones in heptamethine cyanine (HMC) dyes, optimized for photothermal therapy with improved photostability—expanding medical demand beyond energy applications.

European Union: Binding Green Deal Measures and PFAS-Free Chemistry

The EU has shifted decisively from voluntary standards to binding obligations. In Spring 2025, the European Parliament advanced Green Deal 2025 measures requiring solar-ready buildings from 2027, catalyzing demand for NIR-absorbing interlayers in laminated glass that balance insulation with energy harvesting.

Chemical compliance is a parallel growth vector. German and French majors—such as Merck KGaA and Heraeus—are scaling PFAS-free NIR dyes to meet REACH and Circular Economy Action Plan requirements while serving medtech and architectural glazing. Additionally, REPowerEU funding now covers up to 50% of domestic solar-integrated window retrofits, accelerating installer adoption of NIR-selective thin films across member states.

India: Solar PLI Momentum and Green Hydrogen Synergies

India is rapidly domesticating metal-oxide NIR pigments to support its solar and EV ambitions. Under the High-Efficiency Solar PV Modules PLI, multiple greenfield plants commissioned by late 2025 are integrating NIR-absorbing coatings to capture wavelengths in the 700–1400 nm range—broadening spectral utilization and improving module yields.

Beyond PV, the Ministry of New and Renewable Energy launched a Hydrogen Valley Innovation Cluster (June 2025) that includes R&D into NIR-active photoelectrochemical catalysts for water splitting. On trade integrity, the Directorate General of Foreign Trade tightened export traceability (January 2025) to ensure Indian metal-oxide nanoparticles meet global optical communications benchmarks—supporting higher-value exports.

Taiwan: ESG Glass and Sub-2nm Optical Control

Taiwan leverages its semiconductor-display ecosystem to lead signal-friendly NIR films. At Intersolar Europe 2025, firms including Vastalent ESG Technology debuted LUCIH nano-ceramic coatings that block ~95% of solar IR while maintaining ~80% electromagnetic transmittance, addressing RF attenuation issues inherent to metal-coated glass.

In parallel, R&D in Hsinchu Science Park is aligning NIR-absorbing photoresists with the sub-2nm roadmap, where precise light management is critical for advanced lithography and heterogeneous integration. This positions Taiwan at the intersection of smart buildings and next-node semiconductor manufacturing.

2025 Strategic Matrix: Near Infrared Absorbing Materials

Near Infrared Absorbing Materials Matrix

|

Country

|

Primary Market Driver

|

2025 Strategic Milestone

|

Key Material Focus

|

|

China

|

Zero-carbon industrialization

|

NDRC/MIIT mandate (June 2025)

|

CsWO₃, ATO, organic PV dyes

|

|

United States

|

LiDAR, stealth & CHIPS

|

Investment Accelerator launch

|

Lanthanide-doped absorbers

|

|

Japan

|

EV range & GX 2040

|

GX 2040 Cabinet approval

|

Fineceramic NIR blockers, HMC dyes

|

|

European Union

|

Building directives

|

Green Deal 2025 binding measures

|

PFAS-free NIR resins

|

|

India

|

Solar PV & hydrogen

|

PLI scale-up; Hydrogen Valley

|

Metal-oxide nanoparticles

|

|

Taiwan

|

Smart buildings & sub-2nm

|

LUCIH ESG glass debut

|

Nano-ceramic NIR coatings

|

Near Infrared Absorbing Materials Market Report Scope

Near Infrared Absorbing Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$852.3 Million

|

|

Market Size (2035)

|

$1806.3 Million

|

|

Market Growth Rate

|

7.8%

|

|

Segments

|

By Material Type (Inorganic Materials, Organic Materials), By Absorption Range (700–900 nm, 900–1200 nm, 1200–1700 nm), By Function (High Transparency, Heat Shielding, Spectral Filtering & Contrast Enhancement, Security & Anti-Counterfeiting), By Application (Automotive, Electronics & Sensors, Building & Construction, Healthcare, Defense & Security)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sumitomo Metal Mining Co. Ltd., Fujifilm Corporation, BASF SE, TDK Corporation, Keeling & Walker Ltd., Epolin, Mitsui Chemicals Inc., Heraeus Group, Yamamoto Chemicals Inc., Nanophase Technologies, DuPont de Nemours Inc., Tokuyama Corporation, Adamant Namiki Precision Jewel, GFE GmbH, Solaris Chem Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Near Infrared Absorbing Materials Market Segmentation

By Material Type

- Inorganic Materials

- Organic Materials

By Absorption Range (Wavelength)

- Short-Wavelength NIR (700–900 nm)

- Mid-Wavelength NIR (900–1200 nm)

- Long-Wavelength NIR (1200–1700 nm)

By Function

- High Transparency

- Heat Shielding / Thermal Management

- Spectral Filtering & Contrast Enhancement

- Security & Anti-Counterfeiting

By Application

- Automotive

- Electronics & Sensors

- Building & Construction

- Healthcare

- Defense & Security

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Near Infrared Absorbing Materials Market

- Sumitomo Metal Mining Co., Ltd.

- Fujifilm Corporation

- BASF SE

- TDK Corporation

- Keeling & Walker Ltd.

- Epolin

- Mitsui Chemicals, Inc.

- Heraeus Group

- Yamamoto Chemicals, Inc.

- Nanophase Technologies Corporation

- DuPont de Nemours, Inc.

- Tokuyama Corporation

- Adamant Namiki Precision Jewel Co., Ltd.

- GFE (Gesellschaft für Elektrometallurgie mbH)

- Solaris Chem Inc.

*- List not Exhaustive