Nitrite Market Expansion Driven by Pharmaceutical-Grade Demand, Industrial Corrosion Control, and Regional Pricing Arbitrage (2025–2034)

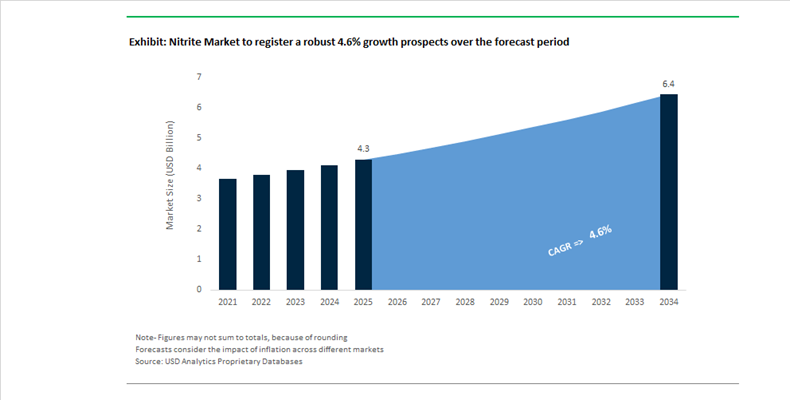

The Nitrite Market is projected to grow from USD 4.3 billion in 2025 to USD 6.4 billion by 2034, registering a CAGR of 4.6%, reflecting steady expansion across food preservation, pharmaceuticals, and industrial chemical applications. The global nitrite industry, including sodium nitrite, potassium nitrite, and calcium nitrite, is undergoing a structural transformation driven by pharmaceutical-grade demand escalation and corrosion-control mandates in infrastructure and energy sectors. As of early 2026, the food and beverage sector accounts for 38.6% of global demand, underpinned by nitrites’ critical role as antimicrobial curing agents in processed meats. Meanwhile, industrial-grade nitrites dominate with over 89% revenue share, supported by large-scale utilization in dye intermediates, metal finishing, and pipeline corrosion inhibition. Regional price disparities remain significant, with technical-grade sodium nitrite priced at $383/MT in China versus over $1,300/MT in Western Europe, creating arbitrage and trade flow opportunities influenced by environmental compliance and energy costs. Additionally, the pharmaceutical segment is the fastest-growing, driven by increasing use of high-purity nitrites in treatments for neurological and muscular disorders, while strong financial metrics, such as current ratios of 3.29 and interest coverage exceeding 60.0 among leading producers, reflect robust balance sheets supporting downstream integration and capacity expansion.

The global nitrite industry is witnessing accelerated investment cycles, regulatory tightening, and strategic downstream integration as companies reposition for higher-margin specialty chemical applications. In March 2026, BASF implemented a global price increase of up to 20% across its chemical additive portfolio, including nitrite-related stabilization agents, citing escalating raw material and freight costs. This pricing shift underscores ongoing cost inflation pressures and supply chain disruptions impacting the broader nitrite value chain. In February 2026, regional expansion momentum intensified, particularly in the Middle East, where infrastructure development for downstream chemical hubs is advancing in line with long-term capacity expansion strategies aimed at tripling chemical output by 2030.

Corporate financial disclosures and integration strategies further highlight the sector’s transformation. In February 2026, Deepak Nitrite Ltd. emphasized its pivot toward nitric acid production and downstream derivatives such as MIBK and MIBC, aimed at reducing exposure to commodity price volatility and enhancing margin stability. Earlier, in January 2026, BASF successfully commenced operations at its Verbund site in Zhanjiang, China, a key asset supporting its €6.2–€7.0 billion EBITDA target for 2026, driven by optimized, integrated chemical manufacturing. These developments reflect a broader industry trend toward scale-driven efficiency, vertical integration, and regional production hubs.

Regulatory developments and capital investments are also reshaping competitive dynamics and compliance frameworks. In November 2025, the United Nations (UNECE) introduced updated guidelines under the 24th revised Recommendations on the Transport of Dangerous Goods, mandating stricter GHS compliance for nitrite logistics and labeling, thereby increasing operational complexity in international trade. In August 2025, Deepak Nitrite approved a ₹8,500 crore ($1.02 billion) investment pipeline, including one of the world’s largest phenol and acetone complexes, reinforcing its position in the broader chemical value chain. Policy support is also strengthening domestic production ecosystems, as seen in July 2025, when India’s NITI Aayog outlined initiatives for chemical cluster development and expedited environmental clearances. Additionally, regulatory scrutiny intensified in May 2025, when the U.S. FDA enforced deadlines for nitrosamine impurity mitigation, triggering widespread audits of nitrite sourcing and purity standards. Collectively, these developments signal a market transitioning toward high-purity applications, regulatory compliance rigor, and integrated chemical manufacturing ecosystems, redefining growth trajectories in the global nitrite market.

Nitrite Market Trends and Opportunities

Trend: EU Regulatory Realignment Accelerating Clean-Label Nitrite Solutions in Processed Meats

The food-grade nitrite market is undergoing a structural reset as European regulators intensify scrutiny of nitrosamine formation and residual nitrite exposure. Regulation (EU) 2023/2108, issued by the European Commission, has moved nitrites from a permissive additive framework to a tightly managed risk-mitigation regime. Effective October 9, 2025, the regulation enforces sharply reduced maximum addition limits, cutting allowable added nitrites to 80 mg/kg for most meat products and as low as 55 mg/kg for sterilized formats, alongside new residual caps of 45–50 mg/kg in finished goods. These thresholds are reshaping formulation economics across Europe, compelling processors to adopt higher-efficiency curing systems rather than relying on traditional dosing buffers.

In response, the industry is scaling the use of pre-converted natural nitrites, particularly celery powder derivatives, which enable compliance while preserving product identity. During 2024–2025, the USDA National Organic Program advanced reviews prioritizing certified organic celery inputs, reinforcing global supply chains for naturally sourced nitrites that deliver 70–75% curing efficiency. At the formulation level, processors are deploying synergistic hurdle technologies, combining lower nitrite concentrations with antioxidants such as ascorbic acid to stabilize color and inhibit Clostridium botulinum. This approach reflects a broader shift toward ion-specific NO₂⁻ control rather than gross additive limits, positioning clean-label nitrites as a premium, compliance-driven growth segment rather than a commoditized preservative.

Trend: Sodium Nitrite as a Strategic Corrosion Inhibitor in District Heating Networks

Beyond food applications, industrial-grade sodium nitrite is becoming a strategic material in energy infrastructure, particularly within expanding district heating networks across Europe and China. As cities pursue carbon-neutral heating under long-term decarbonization roadmaps, asset owners are prioritizing lifecycle reliability over short-term cost minimization. Sodium nitrite has emerged as the corrosion inhibitor of choice in closed-loop district heating systems, where maintaining concentrations of 500–1000 ppm promotes formation of a stable gamma-iron oxide passivation layer on carbon steel pipelines.

Operational data from 2024 municipal utilities confirm that nitrite-based programs are critical in preventing under-deposit corrosion in high-temperature loops operating above 90°C, extending asset life across multi-decade horizons. China’s leadership in district heating expansion under its 14th Five-Year Plan has made it the world’s largest consumer of industrial sodium nitrite, reinforcing global price differentiation. By Q3 2025, Chinese market prices hovered near USD 383 per metric ton, while European pricing exceeded USD 1,300 per metric ton due to energy and logistics constraints. The closed-loop nature of district heating amplifies sodium nitrite’s value proposition, as minimal replenishment is required once system equilibrium is achieved, reinforcing its role as a low-maintenance, high-reliability infrastructure chemical.

Opportunity: Nitrite-Based Aqueous Gold Leaching as a Safer Mining Reagent

Environmental and regulatory pressure on cyanide use in gold mining is opening a high-value opportunity for nitrite chemistry as an alternative lixiviant system. Calcium and sodium nitrite are gaining attention in hydrometallurgical circuits designed to reduce the ecological footprint and security burden associated with sodium cyanide. In 2025, pilot programs in Kazakhstan demonstrated nitrite-assisted leaching systems combined with sodium percarbonate achieving 99.99 percent detoxification efficiency in tailings, comfortably meeting the International Cyanide Management Institute discharge threshold of 0.2 mg/L.

This performance positions nitrite-based systems as particularly attractive for small-scale and in-situ mining operations, where cyanide’s exclusion zones, transport restrictions, and insurance costs are disproportionately burdensome. As regulators tighten cyanide handling requirements through 2032, nitrite-enabled gold recovery represents a strategic R&D and commercialization pathway for specialty chemical suppliers, especially those targeting modular, low-capex extraction technologies aligned with responsible mining standards.

Opportunity: Electrolyte Stabilization in Grid-Scale Zinc-Ion Energy Storage

The emergence of aqueous zinc-ion batteries as a contender in long-duration energy storage is creating a novel specialty demand stream for sodium nitrite. One of the primary technical barriers for zinc-based systems has been dendrite formation and parasitic hydrogen evolution at the anode. Peer-reviewed studies published in late 2025 demonstrate that sodium nitrite acts as an effective electrolyte additive by regulating Zn²⁺ solvation dynamics, enabling uniform zinc deposition and suppressing dendritic growth.

Laboratory and pilot pouch-cell data show that nitrite-enhanced electrolytes can extend cycle life by 30–40%, a critical threshold for grid-scale systems targeting 20-year operational lifetimes. This technical validation is translating into strategic investment. Specialty manufacturers such as Deepak Nitrite allocated approximately ₹2,000 crore in FY 2024–25 toward capacity expansion and specialty nitration platforms, explicitly positioning for battery, pharmaceutical, and advanced materials demand. As utilities prioritize non-flammable, aqueous storage chemistries, sodium nitrite’s transition from bulk intermediate to performance-critical additive underscores a structural upgrade in the nitrite market’s value chain.

Nitrite Market Share and Segmentation Insights

Sodium Nitrite Leads Nitrite Market Due to Broad Industrial and Food Processing Applications

Sodium nitrite accounted for 58.60% of the Nitrite Market share in 2025, making it the most widely used nitrite compound across food processing, industrial chemistry, and corrosion protection applications. Sodium nitrite is valued for its high chemical reactivity, stable supply chain, and versatility across multiple industries, enabling its use as a curing agent in processed meats, an intermediate in dye and rubber chemical synthesis, and a corrosion inhibitor in industrial systems. In food processing, sodium nitrite plays a critical role in preventing the growth of Clostridium botulinum, stabilizing the characteristic pink color of cured meats, and contributing to flavor development in products such as bacon, ham, and sausages. In industrial applications, it is widely used in metal treatment processes, heat transfer systems, and water treatment formulations to control corrosion in pipelines and industrial equipment. In 2025, increasing consumer demand for clean label food products has encouraged the development of natural curing alternatives such as celery powder and nitrate-rich plant extracts, though regulatory constraints and performance limitations continue to maintain sodium nitrite as the dominant preservative in commercial meat processing.

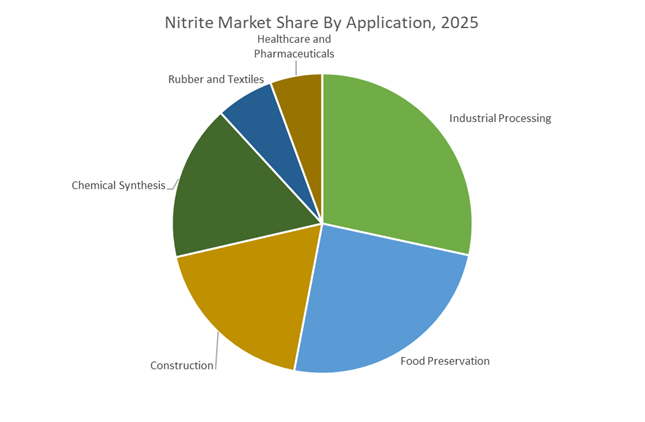

Industrial Processing Drives the Largest Demand for Nitrite-Based Chemicals

Industrial processing accounted for 28.40% of the Nitrite Market share in 2025, making it the largest application segment for nitrite-based chemicals. Nitrites are widely used across industrial systems for corrosion inhibition, metal surface treatment, cooling water system protection, and boiler water treatment, where they prevent oxidation and corrosion of steel and iron components exposed to water and chemical environments. Industrial corrosion inhibitors containing sodium nitrite are commonly applied in closed-loop cooling systems, heat exchangers, pipelines, and metal processing equipment, where they protect infrastructure and extend equipment lifespan. The extensive scale of industrial manufacturing, energy production, and infrastructure maintenance has sustained strong demand for nitrite-based corrosion control chemicals worldwide. In 2025, increasing environmental regulation regarding nitrite discharge into wastewater systems has encouraged industrial operators to adopt more controlled chemical management practices. Many facilities now implement closed-loop corrosion protection systems equipped with automated monitoring and dosing technologies, allowing operators to maintain optimal nitrite concentrations for corrosion prevention while reducing chemical consumption and minimizing environmental release.

Nitrite Market Competitive Landscape

The nitrite market in 2026 is driven by vertical integration, high-purity specialty grades, and decarbonized ammonia pathways. Competitive leadership hinges on nitric acid integration, green hydrogen-based production, and regionalized supply chains serving pharmaceuticals, electronics, and industrial applications with stable pricing and low-carbon credentials.

Deepak Nitrite strengthens ammonia-to-amines integration with nitric acid backward linkage and specialty expansion

Deepak Nitrite has emerged as a globally competitive integrated nitrite producer through its ammonia-to-amines strategy and backward integration into nitric acid. The commissioning of a ₹515 crore nitric acid plant in Gujarat secures feedstock and enhances margin stability. Its ₹85 crore nitration and hydrogenation expansion targets high-value pharmaceutical and agrochemical intermediates. The company’s ₹9,000 crore polycarbonate project further strengthens its downstream integration into specialty chemicals. With a target of 60–70% renewable energy usage in 2026, Deepak is reducing carbon intensity across its nitrite portfolio. This integration-driven model positions it strongly in the global “China Plus One” sourcing shift.

BASF leverages integrated Verbund systems to deliver high-purity nitrites and specialty intermediates

BASF is reinforcing its nitrite market position through its globally integrated Verbund model and high-tech production hubs. The Zhanjiang site in China enhances feedstock efficiency by recycling intermediates into downstream specialty nitrites and amines. With €59.7 billion in 2025 sales, BASF continues to invest in high-margin segments such as agricultural solutions and environmental catalysts. Portfolio optimization, including divestments, allows greater focus on integrated chemical systems. The company’s innovation in food-contact compliant materials reflects tightening regulatory demands for clean chemistry. BASF’s scale, integration, and advanced processing capabilities underpin its leadership in high-purity nitrite applications.

Yara advances low-carbon nitrite production through clean ammonia and carbon capture integration

Yara International is leading the decarbonized nitrogen transition by integrating clean ammonia and carbon capture technologies into its nitrite value chain. The company generated US$15.6 billion in 2025 revenue, with deliveries rising to 23.8 million tonnes. Its CCS-enabled ammonia production at Sluiskil enables lower-emission “blue nitrites” for industrial applications. Yara’s strategic plan targets US$200 million EBITDA improvement through operational optimization and logistics efficiency. Collaboration with Air Products on low-carbon ammonia projects further strengthens feedstock sustainability. Its global distribution network and sustainability focus position Yara as a key supplier of low-carbon nitrite derivatives.

SABIC accelerates integrated petrochemical expansion with large-scale feedstock advantages and global synergies

SABIC is strengthening its nitrite market presence through large-scale petrochemical integration and global expansion projects. The US$6.4 billion Fujian complex, nearing completion in 2026, will provide extensive intermediates for downstream chemical production. Synergies with Saudi Aramco, generating up to US$1.8 billion annually, significantly reduce feedstock and logistics costs. SABIC’s strategic focus across MOVE, BUILD, POWER, and CARE sectors aligns nitrite applications with EV infrastructure, construction, and healthcare materials. Its agrinutrients division is expanding into high-value nitrogen-based specialty solutions. This scale-driven, integrated model ensures cost competitiveness and supply reliability.

Honeywell restructures advanced materials portfolio to focus on high-performance specialty chemicals and sustainability solutions

Honeywell is reshaping its role in the nitrite ecosystem through the spin-off of Solstice Advanced Materials and a strategic focus on high-performance chemistries. With US$40 billion in 2025 sales and a US$37 billion backlog, the company maintains strong financial stability. Its reorganization into four core segments enhances focus on industrial automation and process technologies relevant to chemical manufacturing. Capital allocation toward energy and sustainability solutions supports innovations in carbon capture and efficiency. The spin-off enables sharper focus on specialty materials used in high-value applications. Honeywell’s technology-driven approach supports evolving demand for precision chemical processing.

India: Capacity-Led Scale-Up Anchored by Feedstock Security

India’s nitrite market is entering a structurally transformative phase, led by large-scale asset commissioning and improved nitrogen feedstock resilience. The most significant catalyst is the ₹2,000 crore capital expenditure program underway at Deepak Nitrite, which is adding advanced hydrogenation and nitration assets scheduled for commissioning by June 2026. These units are designed to operate at high utilization rates by mid-Q3 2026, strengthening domestic availability of nitrite intermediates for pharmaceuticals and agrochemicals. In parallel, stabilization of greenfield solvent assets in late 2025 expands India’s capability to supply high-purity downstream chemistries aligned with the country’s life sciences industry trajectory toward a $100 billion valuation by 2026.

Feedstock volatility mitigation has emerged as a parallel strategic pillar. By November 2025, Indian nitrite producers expanded ammonia storage infrastructure from two days to nearly fifteen days of consumption, materially reducing exposure to global supply shocks. Policy support under the New Investment Policy integration has further reinforced this direction, with nitrogen-based chemical units in Gorakhpur and Sindri receiving interest-free loans totaling ₹894.80 crore in March 2025. The inauguration of a dedicated R&D center in Q4 2025 is now accelerating diversification into fluorination and complex nitration chemistries, positioning India as a competitive supplier of specialty nitrite derivatives rather than a purely volume-driven market.

China: Carbon Governance and Performance Chemicals Integration

China’s nitrite market is being reshaped by environmental regulation and performance-led downstream integration. The August 2025 Industrial N₂O Control Action Plan jointly released by the Ministry of Ecology and Environment and MIIT establishes a long-term compliance framework requiring catalytic abatement systems across nitric acid and nitrite facilities. With reporting obligations beginning in 2026, producers are already reallocating capital toward emissions monitoring and abatement technologies, fundamentally altering cost structures and operational priorities across the sector.

At the same time, China continues to strengthen its role as a supplier of nitrite-based intermediates for high-performance applications. BASF doubled its DMAPA capacity at Nanjing in July 2025, directly increasing nitrite consumption for water treatment and crop protection chemistries. The transition of the entire amine and nitrite-intermediate portfolio at the site to renewable electricity by late 2025 delivered a measurable reduction in product carbon footprint, aligning Chinese output with global sustainability benchmarks. The commissioning of a CFRP-based dispersant line in November 2025 further anchors nitrites in advanced coatings and automotive finishes, reinforcing China’s position as a technologically integrated producer rather than a commoditized supplier.

Germany: Sustainability-Driven Purity and Agricultural Linkages

Germany’s nitrite market is characterized by regulatory rigor and integration with low-emission agriculture and food systems. In 2025, BASF, together with Danish Crown, expanded the “Climate-Smart Meat” pilot to 84 farms covering 20,000 hectares. The use of advanced nitrification inhibitors across feed crop cultivation has demonstrated up to a 50% reduction in nitrous oxide emissions, reinforcing the strategic importance of nitrite chemistry within sustainable nitrogen management frameworks.

On the industrial side, renewed distribution agreements between BASF SE and Häffner GmbH & Co. KG in 2025 improved accessibility of sodium nitrite and nitrate for small-to-medium industrial users across the DACH region. Concurrently, German manufacturers are accelerating the transition toward ultra-high-purity sodium nitrite grades to comply with forthcoming EU 2026 food safety guidance on residual nitrosamines. This regulatory shift is pushing the market away from bulk food-preservation applications toward tightly specified, traceable nitrite products.

United States: Regulatory Scrutiny and Energy Transition Demand

In the United States, the nitrite market is increasingly shaped by regulatory oversight and non-food industrial demand. The FDA’s August 2025 update placing nitrites under continued post-market chemical review has intensified data requirements around dietary exposure and long-term toxicity through 2026. This scrutiny is driving food processors and suppliers toward tighter quality control, alternative formulations, and differentiated technical-grade offerings.

Beyond food applications, the U.S. Department of Energy highlighted in late 2025 the growing use of molten nitrite and nitrate salt blends as heat transfer fluids in Concentrated Solar Power projects across the Southwest. This application underscores the strategic relevance of industrial-grade nitrites in long-duration thermal energy storage. Additionally, patent activity in 2025 indicates a shift toward liquid nitrite corrosion inhibitors optimized for automated dosing in closed-loop cooling systems, particularly for data centers, further broadening the U.S. demand base beyond traditional preservation uses.

Norway: Premium Nitrogen Products and Ammonia Flexibility

Norway’s nitrite market is anchored by premium-grade nitrogen products and upstream ammonia optimization. Yara International reported a 47% EBITDA increase in its premium product segment in Q1 2025, driven by strong European demand for technical-grade nitrates and nitrites. Rather than adding new capacity, Yara is maximizing output from existing assets in Porsgrunn and Rostock, emphasizing efficiency and margin optimization.

Strategically, Yara’s 2025 Capital Markets Update confirmed a pivot toward U.S.-based ammonia equity investments, ensuring long-term cost stability and supply security for European nitrite production lines through 2027. This upstream flexibility allows Norwegian and broader European nitrite operations to remain competitive amid tightening environmental standards and volatile global nitrogen markets.

Summary Table: Nitrite Market – Country-Level Strategic Positioning

Nitrite Market County Level Snapshot

|

Country

|

Strategic Focus

|

Key Developments

|

Market Implication

|

|

India

|

Capacity expansion and feedstock security

|

New nitration assets, ammonia storage, policy loans

|

Rapid scale-up of domestic nitrite intermediates

|

|

China

|

Emissions control and performance integration

|

N₂O action plan, renewable-powered production

|

Compliance-driven cost shifts and higher-value output

|

|

Germany

|

Sustainability and purity leadership

|

Nitrification inhibitors, UHP food-grade transition

|

Premiumization and regulatory alignment

|

|

United States

|

Regulatory review and energy applications

|

FDA scrutiny, CSP heat transfer demand

|

Diversified industrial demand beyond food

|

|

Norway

|

Premium products and ammonia flexibility

|

Yara asset optimization, U.S. ammonia sourcing

|

Margin stability and supply resilience

|

Nitrite Market Report Scope

Nitrite Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.3 Billion

|

|

Market Size (2034)

|

$6.4 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Type (Sodium Nitrite, Potassium Nitrite, Calcium Nitrite, Organic Nitrites), By Grade (Food Grade, Industrial Grade, Pharmaceutical Grade), By Form (Solid, Liquid), By Application (Food Preservation, Industrial Processing, Chemical Synthesis, Healthcare and Pharmaceuticals, Construction, Rubber and Textiles)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF, Deepak Nitrite, Yara International, Shandong Haihua Group, Airedale Chemical, UralChem, SNDB, Yingfengyuan Industrial Group, Radiant Indus Chem, Shandong Hailan Chemical, Merck, Dow, Nilkanth Organics, Hualong Nitrite, Anmol Chemicals

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Nitrite Market Segmentation

By Type

- Sodium Nitrite

- Potassium Nitrite

- Calcium Nitrite

- Organic Nitrites

By Grade

- Food Grade

- Industrial Grade

- Pharmaceutical Grade

By Form

By Application

- Food Preservation

- Industrial Processing

- Chemical Synthesis

- Healthcare and Pharmaceuticals

- Construction

- Rubber and Textiles

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Nitrite Market

- BASF

- Deepak Nitrite

- Yara International

- Shandong Haihua Group

- Airedale Chemical

- UralChem

- SNDB

- Yingfengyuan Industrial Group

- Radiant Indus Chem

- Shandong Hailan Chemical

- Merck

- Dow

- Nilkanth Organics

- Hualong Nitrite

*- List not Exhaustive