Environmental Catalyst Market to Reach $5.2 Billion by 2034 at 4.6% CAGR Driven by Hydrogen, Circular Chemistry, and Emission Control Innovation

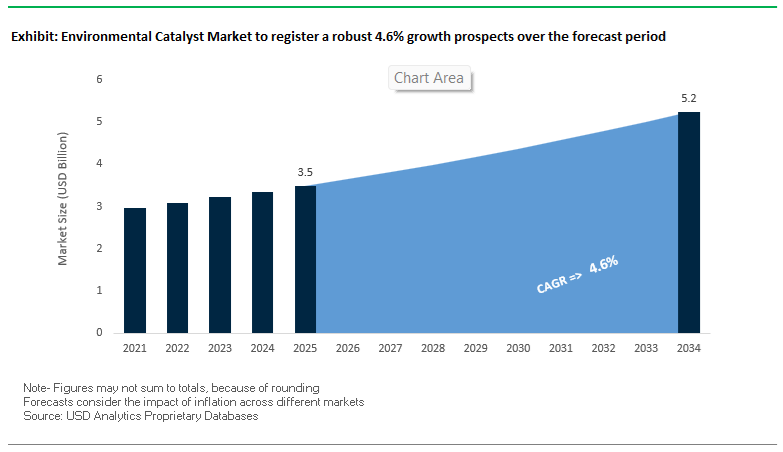

The Environmental Catalyst Market is projected to grow from $3.5 billion in 2025 to $5.2 billion by 2034, registering a CAGR of 4.6%. Market expansion is being shaped by consolidation among global catalyst leaders, rapid investment in hydrogen production technologies, and tightening industrial emission standards across Asia and Europe. In May 2025, Honeywell signed a $2.4 billion agreement to acquire Johnson Matthey’s Catalyst Technologies business. Expected to close in H1 2026, the deal integrates Honeywell UOP’s process licensing with Johnson Matthey’s advanced catalyst synthesis capabilities, forming a vertically integrated platform targeting ammonia cracking, hydrogen generation, sustainable aviation fuel, and low-carbon refinery upgrades. This transaction marks a strategic pivot toward energy transition catalysts rather than traditional hydrocarbon refining dominance.

Technology-led differentiation is accelerating in both emission control and circular production systems. In early 2025, BASF commenced commercial production of loopamid® in Shanghai, utilizing proprietary catalyst systems to enable textile-to-textile recycling of Nylon 6 with up to 70% lower CO₂ emissions. The company is also constructing a dedicated X3D® catalyst facility in Ludwigshafen scheduled for 2026 startup, employing 3D-printing to engineer open-structure catalysts that reduce pressure drop and increase conversion efficiency in emission control and reactor systems. Meanwhile, Topsoe inaugurated Europe’s largest Solid Oxide Electrolyzer Cell factory in Herning in 2025, scaling catalyst-enabled Power-to-X production for green hydrogen and e-fuels. In January 2026, Honeywell UOP’s eFining™ technology was named Energy Transition Solution of the Year, leveraging advanced catalysts to convert green hydrogen and captured CO₂ into eMethanol and ultimately sustainable aviation fuel with emissions reductions approaching 88%.

Automotive and industrial emission control remain core demand anchors, though competitive intensity is rising. Umicore received Nissan’s Global Innovation Award in July 2024 for a breakthrough catalyst coating enabling reduced Platinum Group Metal loadings while meeting stringent light-duty emission standards. Clariant unveiled titanium-based AddWorks™ catalysts in October 2025, positioned as antimony-free alternatives amid supply chain volatility following China’s export restrictions. Johnson Matthey reported achieving a 12.4% margin in its Clean Air division in November 2025, targeting 14–15% in FY2025/26 despite divesting portions of its catalyst portfolio. Simultaneously, China expanded its domestic environmental catalyst capacity by 40% through 2025, reducing reliance on Western NOx and VOC catalyst imports and intensifying pricing competition in Asia-Pacific. Umicore is set to commission a new fuel cell catalyst plant in China in 2026, targeting heavy-duty hydrogen truck platforms and reinforcing the sector’s migration toward fuel cell and electrochemical catalyst applications aligned with global decarbonization mandates.

Trends and Opportunities in the Environmental Catalyst Market

Shift from Fixed Replacement Cycles to Condition-Based Catalyst Management Using Digital Twins

- Environmental catalysts are increasingly treated as high-value, data-managed assets rather than expendable inputs. Refiners and chemical producers are replacing fixed regeneration or replacement schedules with digital twin frameworks that model catalyst kinetics, deactivation pathways, and real-time process interactions.

- Operational evidence from a September 2025 multi-refinery analysis covering more than 150 installations shows that catalyst digital twins are delivering maintenance cost reductions ranging from 25% to 55%. By synchronizing real-time plant data with reaction kinetics and mass-transfer models, operators are extending catalyst active life while reducing unplanned shutdowns. Return-on-investment timelines have shortened to 12–36 months, making digital catalyst management one of the fastest-payback digital investments in downstream and specialty chemical operations.

- Advanced twins now simulate poisoning, fouling, and thermal stress scenarios before performance degradation becomes irreversible. July 2025 industry benchmarking indicates that proactive process parameter adjustments enabled by these models can improve overall unit efficiency by 15% to 42%, particularly in hydrotreating, SCR, and VOC abatement units. Global operators including Shell and Siemens are scaling these systems across downstream and offshore assets, aligning catalyst performance optimization directly with ESG targets and energy-intensity reduction goals.

Acceleration of Multi-Functional Catalysts for Integrated Emissions Abatement

- Environmental regulation is mandating facilities to address NOx, VOCs, CO, ammonia slip, and nitrous oxide simultaneously, driving demand for catalysts that deliver multi-pollutant conversion within a single reactor footprint.

- Regulatory momentum intensified following the European Commission’s December 2025 evaluation of the NEC Directive, which emphasized the need for coordinated abatement to meet 2030 air-quality targets. This has accelerated adoption of tertiary catalyst systems such as EnviNOx®, developed through the BASF and thyssenkrupp Uhde collaboration, which demonstrate over 99% N₂O reduction while integrating NOx control. These solutions significantly reduce CAPEX by avoiding parallel reactor trains.

- On the innovation front, an August 2025 review in Catalysts documented the commercialization of trimetallic nickel-based catalysts supported on gamma-alumina. These formulations enable simultaneous dry reforming of methane and CO₂ utilization, lowering the energy intensity of carbon management while improving catalyst stability under fluctuating feed compositions. Low-temperature oxidation catalysts, including BASF’s VOCat™ series, are also gaining traction by operating efficiently at temperatures as low as 180°C, enabling VOC destruction in energy-constrained applications such as printing, packaging, and specialty chemicals without compromising thermal shock resistance.

Catalyst Demand from Variable-Load Green Hydrogen and E-Fuels Infrastructure

- The expansion of green hydrogen is creating a structurally new catalyst demand profile defined by intermittent operation, pressure cycling, and exposure to variable impurity loads. Unlike conventional steady-state processes, renewable-powered electrolyzers and hydrogen downstream units require catalysts that maintain activity under frequent start-stop conditions.

- In October 2025, India’s steel sector announced large-scale adoption of hydrogen-based direct reduced iron under the National Green Hydrogen Mission. This transition is opening a substantial market for catalysts used in hydrogen production, purification, and utilization that can withstand dynamic operating regimes. Late-2025 research shows that MXene-supported platinum nanocomposites can deliver equivalent activity with 60% to 70% lower PGM loading, directly addressing cost and supply constraints while improving resistance to mechanical stress at operating pressures between 30 and 80 bar.

- Globally, nearly 100 million tonnes of hydrogen-ready capacity has been announced for the mid-2030s. This creates first-mover opportunities for catalyst suppliers specializing in ammonia cracking and liquid organic hydrogen carrier systems, where resistance to nitrogen poisoning and long-term thermal cycling stability are critical to commercial viability.

Hybrid Plasma–Catalyst Systems for PFAS, N₂O, and Recalcitrant Pollutant Destruction

- Hybrid plasma-catalytic systems are emerging as one of the most disruptive opportunities in the environmental catalyst market, particularly for pollutants that resist conventional thermal oxidation. Non-thermal plasma coupled with tailored catalysts enables molecular bond cleavage at near-ambient temperatures, significantly reducing energy demand.

- A December 2025 U.S. Department of Defense–backed SERDP and ESTCP study demonstrated that non-thermal plasma GAP reactors can degrade PFAS in water and solids using roughly one-fifth of the energy required for thermal evaporation. This performance gap is catalyzing investment in plasma-compatible catalyst materials for water treatment, defense remediation, and industrial waste management.

- Indoor air quality applications represent a parallel growth vector. Research published in August 2025 in the Journal of Electrostatics showed that combining non-thermal plasma with TiO₂ photocatalysis achieved a three-log reduction in bioaerosols and substantial formaldehyde removal at industrial-scale airflow rates. These results align with economic analyses presented at the European Commission’s 2025 Clean Air Forum, which estimate a fourfold societal return on every euro invested in clean air technologies. This economic validation supports premium pricing for advanced hybrid catalysts that deliver high destruction efficiency at low operating temperatures.

Environmental Catalyst Market Share and Segmentation Insights

Selective Catalytic Reduction Catalysts Anchor NOx Abatement Across Diesel and Industrial Systems

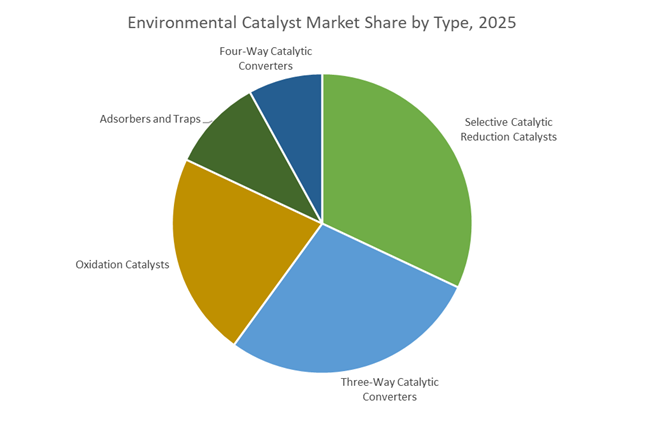

Selective catalytic reduction (SCR) catalysts account for 32% of total environmental catalyst market share in 2025, reflecting their indispensable role in reducing nitrogen oxide emissions from heavy-duty diesel vehicles, power plants, and industrial boilers. Adoption is strongly supported by tightening Euro VI, EPA, and Tier 4 regulations, driving consistent deployment across on-road and off-road applications. Three-way catalytic converters maintain a substantial share in gasoline-powered vehicles, simultaneously converting carbon monoxide, hydrocarbons, and NOx, supported by the continued dominance of internal combustion engines in emerging markets. Oxidation catalysts remain standard equipment for diesel platforms, enabling CO and hydrocarbon conversion while supporting diesel particulate filter regeneration. Adsorbers and traps are gaining traction as particulate matter limits tighten, while four-way catalytic converters are emerging for gasoline direct injection engines, integrating particulate filtration with traditional three-way functionality to meet next-generation emission thresholds.

Mobile Sources Command the Majority of Catalyst Demand Under Tightening Tailpipe Standards

Mobile sources represent 68% of global environmental catalyst consumption in 2025, driven by passenger cars, commercial trucks, buses, and off-road equipment complying with increasingly stringent tailpipe emission regulations. The sheer scale of global vehicle fleets ensures sustained demand for SCR systems, three-way converters, oxidation catalysts, and particulate filters. Stationary sources form a significant secondary segment, encompassing power generation, industrial boilers, chemical plants, and waste incineration facilities where catalysts mitigate NOx, CO, and volatile organic compound emissions to meet environmental compliance mandates. Marine and aviation applications are expanding steadily as International Maritime Organization rules tighten sulfur and NOx limits for ocean-going vessels and aviation authorities address emissions from auxiliary power units and ground operations. Together, these segments reinforce long-term growth across automotive emission control catalysts and industrial air pollution control technologies.

Competitive Landscape of the Environmental Catalyst Market

The Environmental Catalyst Market in 2026 is shaped by accelerating decarbonization mandates, Euro 7 and China 6b emission norms, green hydrogen deployment, and circular precious-metal recovery, with leading players competing on PGM integration, CCUS readiness, renewable fuels catalysts, and closed-loop sustainability models.

BASF drives circular emission control and hydrogen purification through vertically integrated catalyst platforms

BASF Environmental Catalyst and Metal Solutions (ECMS) remains the global benchmark in environmental catalysts after spinning off its mobile emissions and precious metals businesses to sharpen its green energy focus. In late 2025 to early 2026, BASF operationalized its circular economy loop in Chennai, expanding heavy-duty on-road and off-road catalyst capacity. Its DASH™ and FWC™ four-way conversion catalysts enable gasoline engines to meet Euro 7 and China 6b standards by removing particulates and gaseous pollutants in a single unit. The Puristar® series supports ultra-high-purity hydrogen markets. BASF’s defining advantage is vertical PGM integration and Metal-as-a-Service, shielding OEMs from platinum and rhodium volatility while ensuring secure supply for emission control systems.

Honeywell UOP accelerates renewable fuels and CCUS leadership through landmark catalyst acquisition

Honeywell UOP strengthened its sustainability leadership in February 2026 by finalizing the £1.325 billion acquisition of Johnson Matthey’s Catalyst Technologies business, dramatically expanding its footprint in syngas, ammonia, and methanol. The company is widely recognized for its CCUS deployments, including advanced point-source capture with ExxonMobil. Honeywell’s Ecofining™ catalysts are the global standard for producing Sustainable Aviation Fuel from fats, oils, and greases. Its strategy centers on integrating process technologies with next-generation catalyst portfolios to dominate renewable diesel, SAF, and blue hydrogen, positioning Honeywell UOP as a cornerstone supplier for the global energy transition.

Umicore anchors light-duty emission catalysts with closed-loop precious metal recovery

Umicore differentiates itself through a circular materials model that recovers PGMs from spent catalysts and batteries. The company reported €3.6 billion in 2025 revenue with a 24.0% EBITDA margin and is executing its CORE strategy in 2026 to navigate peak ICE production. A final investment decision to expand precious metals refining will increase copper and nickel capacity while shortening PGM throughput times. Umicore maintains a leading share in light-duty gasoline catalysts, even as electrification accelerates. Its ability to “give new life to used metals” provides a more resilient raw-material supply than mining-dependent rivals, reinforcing its role in sustainable automotive emission control.

Topsoe powers green hydrogen, SAF, and e-fuels with next-generation catalyst technologies

Topsoe leads high-performance catalysts for green chemicals and renewable fuels. In February 2026, it inaugurated Europe’s largest SOEC manufacturing facility, strengthening its position in green hydrogen. Its HydroFlex™ 2026-gen catalysts now command over one-third of global renewable diesel and SAF capacity. Topsoe also signed a flagship January 2026 agreement for a major green ammonia project in Yanbu, Saudi Arabia. Guided by its “Perfecting Chemistry for a Better World” strategy, the company targets e-fuels and Power-to-X markets as they reach commercial scale across the US and Europe, making Topsoe a critical enabler of industrial decarbonization.

Clariant advances non-toxic polyester and low-energy ammonia catalysts for net-zero chemistry

Clariant focuses on high-margin environmental catalysts that replace hazardous legacy materials. In early 2026, it launched AddWorks™ titanium-based catalysts as a sustainable alternative to antimony in polyester production, responding to 2024–2025 export constraints. The AmoMax-Casale catalyst, commercialized in 2025–2026, significantly lowers energy intensity in ammonia synthesis, reducing fertilizer carbon footprints. Clariant’s Catalysts and Energy segment benefits from a 4.98% CAGR in catalyst regeneration, where it is a top-tier ex-situ recovery provider. Its portfolio is heavily aligned with net-zero hydrogen purification and emission reduction, cementing Clariant’s position in decarbonized chemical manufacturing.

Germany: Advanced Manufacturing and Hydrogen-Linked Catalyst Leadership

Germany is consolidating its position as a technology anchor for the Environmental Catalyst Market by coupling advanced manufacturing with decarbonization policy. BASF is on track to commission a commercial-scale 3D-printed catalyst facility in Ludwigshafen by Q1 2026. The deployment of proprietary X3D technology enables highly complex catalyst geometries that increase active surface area and optimize gas flow dynamics. These design advantages are expected to materially improve reactor efficiency while supporting up to 20% emission reduction in industrial chemical processes. For German heavy industry, this marks a structural shift from incremental catalyst upgrades toward digitally engineered emission-control solutions.

Parallel to this, Germany is emerging as a critical hub for hydrogen-related catalyst systems. In November 2025, BASF Environmental Catalyst and Metal Solutions inaugurated a specialized production site in Budenheim focused on catalyst-coated membranes and fuel cell components. This facility directly supports the European Union’s hydrogen mobility and heavy-duty transport decarbonization agenda. Regulatory alignment is reinforcing this trajectory. German manufacturers are integrating AI-driven product stewardship tools to meet the 2026 REACH recast and Corporate Sustainability Reporting Directive requirements. The emphasis on Safe and Sustainable by Design catalysts is pushing producers to eliminate hazardous intermediates early in the value chain, transforming compliance into a competitive differentiator rather than a cost center.

United States: Specialty Catalyst Expansion and Emissions Reliability Focus

The United States Environmental Catalyst Market is being shaped by targeted capacity expansion and regulatory fine-tuning aimed at operational reliability. In May 2025, Umicore announced a double-digit million-dollar investment to expand homogeneous catalyst production at its Catoosa, Oklahoma site. Construction commenced in late 2025, with the expansion designed to scale Grubbs Catalyst® output by early 2027. This investment reflects sustained demand from high-performance specialty chemicals and pharmaceutical synthesis, where catalyst selectivity and consistency directly influence process economics.

Regulatory agencies are also recalibrating emission-control expectations. In August 2025, Environmental Protection Agency addressed industry concerns around Selective Catalytic Reduction system reliability in diesel engines. Updated 2026 guidance focuses on preventing engine derates linked to Diesel Exhaust Fluid sensor failures, particularly under extreme heat conditions. Beyond ground transport, aviation is emerging as a niche but high-value application. In early 2025, BASF ECMS introduced VOC2.0™ catalyst technology for the Airbus A320 fleet, enabling onboard conversion of ozone and volatile organic compounds into oxygen and CO₂. This application underscores how environmental catalysts are increasingly embedded into safety, comfort, and regulatory compliance strategies across transport segments.

China: Policy-Driven Replacement Cycles and Large-Scale Industrial Adoption

China’s Environmental Catalyst Market is entering an accelerated replacement cycle driven by national planning and accountability mechanisms. Ahead of the formal rollout of the 15th Five-Year Plan in 2026, the government released a 2025–2030 Green Production roadmap mandating the phase-out of outdated catalyst technologies in petrochemical operations. This directive prioritizes high-efficiency four-way catalytic converters to address nitrogen oxides, sulfur oxides, particulates, and unburned hydrocarbons in a single system. The policy is catalyzing large-scale retrofit demand across state-owned and private refining assets.

Industrial capacity is aligning rapidly with these mandates. BASF’s €10 billion Zhanjiang Verbund site reached a critical milestone in November 2025 with the installation of all steam cracker modules. Downstream units at the complex include advanced catalyst and additive plants designed to supply China’s automotive and high-tech manufacturing ecosystems by late 2026. Regulatory enforcement is tightening further under the July 2025 Provisional Regulations linking local officials’ performance metrics to environmental outcomes. This governance shift has driven municipal-level procurement of stationary source catalysts for waste-to-energy and industrial combustion facilities, embedding environmental catalysts into public infrastructure planning.

India: Refining Expansion and Localized Emission Control Manufacturing

India’s Environmental Catalyst Market is being structurally supported by rapid refining expansion and tightening emission norms. According to the Ministry of Petroleum and Natural Gas, national refining capacity reached 248.9 MMTPA in 2025, driven by projects such as the Numaligarh Refinery expansion. This scale-up has created a substantial captive market for fluid catalytic cracking and hydrotreating catalysts, as refiners seek to maximize yield while meeting sulfur and nitrogen emission constraints.

On the mobility side, BASF’s Chennai catalyst plant, fully operational in 2025, is now producing specialized emission control catalysts for heavy-duty on-road and off-road equipment. These products directly support India’s phased tightening of Bharat Stage norms and localized emission standards. The combination of domestic production and regulatory pressure is reducing dependence on imported catalyst systems while fostering a more resilient local supply chain tailored to Indian fuel qualities and operating conditions.

South Korea: Hydrogen Economy Funding and Emissions Trading Pressure

South Korea is positioning environmental catalysts as a core enabler of its hydrogen economy and carbon pricing framework. The Ministry of Climate, Energy and Environment, established in October 2025, allocated KRW 648 billion in the 2026 budget for RE100 industrial complexes. A significant share of this funding is directed toward clean hydrogen catalyst development and fuel cell vehicle deployment, creating sustained demand for high-performance catalyst systems across power generation and mobility applications.

Regulatory pressure is intensifying through market-based mechanisms. The Korea Emissions Trading Scheme enters its fourth phase in 2026, increasing the financial penalties associated with nitrogen oxide and sulfur oxide emissions. This shift is compelling industrial conglomerates such as SK Innovation to upgrade catalytic emission control systems across refining and petrochemical assets. The result is a move away from minimum-compliance solutions toward catalyst technologies optimized for long-term allowance cost minimization and operational flexibility.

Environmental Catalyst Market: Country-Level Strategic Summary

Environmental Catalyst Market County Level Snapshot

|

Country / Region

|

Strategic Focus Area

|

Key Catalyst Applications

|

Policy or Market Driver

|

|

Germany

|

3D-printed and hydrogen catalysts

|

Industrial reactors, fuel cells

|

REACH recast, EU decarbonization

|

|

United States

|

Specialty and transport catalysts

|

SCR systems, aviation air quality

|

EPA reliability guidance

|

|

China

|

Large-scale replacement cycles

|

Petrochemical and WtE catalysts

|

Five-Year Plan mandates

|

|

India

|

Refining and mobile emission control

|

FCC, hydrotreating, BS norms

|

Refinery expansion

|

|

South Korea

|

Hydrogen and ETS-driven upgrades

|

FCEV, industrial emission control

|

K-ETS Phase 4

|

Environmental Catalyst Market Report Scope

Environmental Catalyst Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.5 Billion

|

|

Market Size (2034)

|

$5.2 Billion

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Type (Oxidation Catalysts, Selective Catalytic Reduction Catalysts, Three-Way Catalytic Converters, Four-Way Catalytic Converters, Adsorbers and Traps), By Metal Group (Platinum Group Metals, Base Metals), By Application (Mobile Sources, Stationary Sources, Marine and Aviation), By Technology (Extruded and Tableted Catalysts, Additive Manufactured Catalysts, Catalyst-Coated Membranes)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Johnson Matthey PLC, Umicore NV, Honeywell International Inc., Corning Incorporated, Cataler Corporation, Heraeus Holding, Cormetech Inc., Tenneco Inc., Clean Diesel Technologies, Inc., DCL International Inc., Bosal Group, Haldor Topsoe A/S, Kunming Sino-Platinum Metals Co., Ltd., Heesung Catalysts Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Environmental Catalyst Market Segmentation

By Type

- Oxidation Catalysts

- Selective Catalytic Reduction Catalysts

- Three-Way Catalytic Converters

- Four-Way Catalytic Converters

- Adsorbers and Traps

By Metal Group

- Platinum Group Metals

- Base Metals

By Application

- Mobile Sources

- Stationary Sources

- Marine and Aviation

By Technology

- Extruded and Tableted Catalysts

- Additive Manufactured Catalysts

- Catalyst-Coated Membranes

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Environmental Catalyst Industry

- BASF SE

- Johnson Matthey PLC

- Umicore NV

- Honeywell International Inc.

- Corning Incorporated

- Cataler Corporation

- Heraeus Holding

- Cormetech Inc.

- Tenneco Inc.

- Clean Diesel Technologies, Inc.

- DCL International Inc.

- Bosal Group

- Haldor Topsoe A/S

- Kunming Sino-Platinum Metals Co., Ltd.

- Heesung Catalysts Corporation

*- List not Exhaustive