Oil Water Separator Market Overview: Regulatory, Industrial, and Technological Drivers Fueling Steady Growth

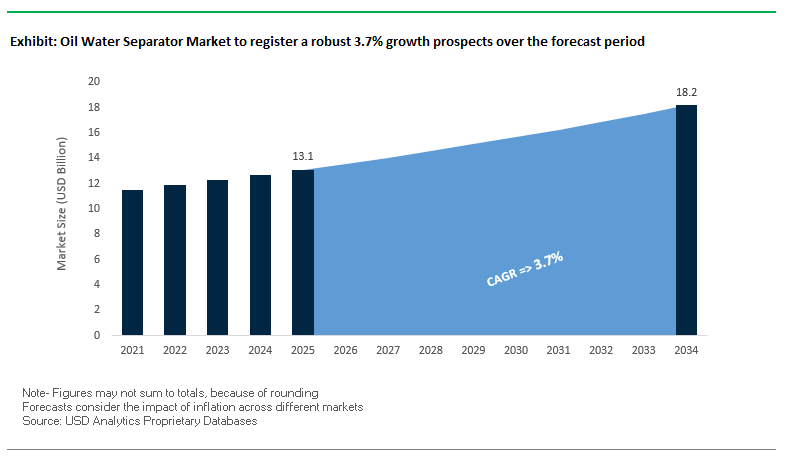

The global oil water separator market is projected to grow from USD 13.1 billion in 2025 to USD 18.2 billion by 2034, registering a CAGR of 3.7%. The growth trajectory is underpinned by tightening international and national discharge regulations, increasing industrial compliance standards, and the adoption of next-generation, non-chemical, and smart separation technologies.

For industry professionals, the 2025 market landscape is informed by key regulatory events. IMO MARPOL Annex I regulation, becoming effective in January 2025, prohibits oil or oily mixture discharge in Special Areas like the Red Sea and Gulf of Aden, pushing ship companies to invest in high-capacity bilge water treatment systems. Concurrently, the U.S. EPA's Clean Water Act requires a stringent "no sheen" standard usually equating to oil and grease concentration limits below 15 mg/L, pushing companies to adopt sophisticated coalescing plate separators and ultrafiltration systems. In the oil & gas industry, produced water management challenge wherein a producing well produces in excess of ten barrels of water per producing barrel oil continues to be a key enabler for powerful separation technology.

A further growth lever is technology innovation, where manufacturers switch to non-chemical, IoT-enabled mechanical separation technology that has lower operating costs owing to predictive maintenance and long-distance compliance monitoring.

Key Insights

- Market Value Growth: USD 13.1B (2025) → USD 18.2B (2034), 3.7% CAGR.

- Regulatory Impact: IMO MARPOL Annex I (Jan 2025) and EPA Clean Water Act are major adoption drivers.

- Industrial Scope: Produced water management in oil & gas is one of the most critical application segments.

- Technology Trends: Transition toward non-chemical, smart, and autonomous oil water separation systems.

Market Analysis – Regulatory Timelines and Strategic Developments Shaping Competitive Positioning

The implementation of IMO MARPOL Annex I’s prohibition in January 2025 on oil discharge in the Red Sea and Gulf of Aden has intensified demand for next-generation bilge water separation systems. Maritime operators are under increasing pressure to integrate solutions capable of achieving oil content levels well below the mandated discharge thresholds, often requiring investments in advanced centrifugal, CPI, and tilted plate separation systems.

Corporate strategies are actively evolving to match the regulatory pace. In August 2025, Nalco Water (Ecolab) announced its acquisition of Ovivo’s Electronics Ultra-Pure Water Business, signaling a consolidation trend where water treatment expertise for high-purity environments intersects with oil water separation capabilities. The positions Ecolab to better serve industries such as semiconductors, where even trace hydrocarbons in wastewater can be operationally catastrophic.

In addition to acquisitions, operational exhibits prove maturity in the market. PetroChina's Chengdu plant was commissioned by SUEZ (now Veolia) and treats 67,000 m³/day of effluent, reusing 70% (i.e., producing 2,500 m³/hour treated water). TiPSS systems by Veolia further exemplify gains in efficiency, reducing oil to a maximum of 90% without any operator intervention. Envopur® ultrafilters from Enviro-Chemie represent a non-chemical solution that separates oil-water emulsions while holding back hydrocarbons, microparticles, and microplastics, allowing facilities to exceed effluent limits.

Product innovations target sector-specified compliance needs too. Alfa Laval's PureBilge system ensures <5 ppm oil content in marine applications, while Ovivo's EnviroSEP™ CPI ensures ≤5 mg/L oil in treated water beyond worldwide regulatory requirements. Pentair's polishing filtration applications round out the value chain by scrubbing out fine solids and trace hydrocarbons to deliver compliance in discharge across both industrial and offshore applications.

Trends and Opportunities in Oil Water Separator Market

Trend 1: High-Efficiency Electrocoagulation Systems

Oil water separator market is experiencing an increasing trend toward high-efficiency electrocoagulation (EC) system applications that continue to replace traditional chemical coagulation processes. Advanced systems provide superior emulsified oily wastewater treatment with up to 99.6% oil and gas removal efficiency in concert with polishing treatments such as centrifugation. In addition to oil removal, EC systems are very efficient in decreasing turbidity removal efficiencies ranging between 91–97%, improving water clarity for both industrial and environmental compliance applications. Unlike conventional processes, EC produces coagulants in situ through electrically dissolving sacrificial electrodes and reduces chemical consumption and sludge generation. The sustainable solution reduces operating expenses, eliminates chemical storage and handling, and complies with industry trends to environmentally friendly wastewater treatment.

Trend 2: Smart Separators with IoT Connectivity

Internet of Things -empowered oil-water separators are revolutionizing wastewater treatment with real-time monitoring, predictive maintenance, and automatic operation. Intelligent systems utilize sensors to monitor oil concentration, flow rates, and levels continuously, while AI-based algorithms control operations by varying chemical dosing or pump speed to achieve uniform effluent quality. Predictive maintenance function minimizes unscheduled downtime by foreseeing likely failures in equipment ahead of time, while central monitoring supports control of offshore or unmanned facilities to ensure better operational safety and regulatory compliance. These intelligent separators serve applications that aim to decrease operational expenditure, improve environmental performance, and incorporate sophisticated digital solutions in wastewater treating processes.

Opportunity 1: Offshore Wind Farm Expansion

Global installation growth in offshore wind farms is generating demand for highly-specialized oil/water separators capable of accepting air compressor condensate and bilge water. Strict environmental regulations mandating oil discharge limits to levels such as 15 ppm require consistent separation technology to prevent pollution of oceans. Accurate oil/water separators ensure not only compliance levels mandated by stringent environmental regulations but also protection for valuable offshore equipment against damage, extending service life while cutting costly downtime. Offshore wind energy growth is a prime area of growth because these units provide a long-term solution to environmental control and operational efficiency at a minimal cost.

Opportunity 2: Airport Deicing Fluid Recovery

Growing regulatory attention to airport stormwater runoff, including runoff that's contaminated with deicing chemicals, is prompting use of oil water separators in airports. NPDES permits granted by the U.S. EPA and FAA regulations demand that airports treat contaminated runoff, such as oil and glycol cocktails, prior to discharge. High-end separators, and in particular those equipped with coalescer plate technology, achieve oil content to regulatory levels (usually below 10 ppm) while facilitating compliance while preserving the environment. By installing these systems, airports can also recover glycol, gaining cost effectiveness, operational ease, and compliance with sustainability initiatives, making oil water separators an important part of airports' modern infrastructures.

Oil Water Separator Market Share Insights

Market Share by Technology: Gravity Separators Leading the Industry

Gravity separators are projected to account for around 50% of the global oil water separator market share in 2025, solidifying their role as the industry’s most widely adopted technology. Their dominance stems from proven reliability, low operating costs, and effectiveness in separating free oil and large suspended solids, making them the first-line treatment step in most industrial wastewater systems. While centrifugal separators and membrane filtration are steadily gaining ground due to their efficiency and compact footprint, gravity-based solutions remain the preferred choice for oil refineries, petrochemical plants, and large-scale industrial facilities where robust and cost-effective operation is paramount. The entrenched market position highlights how regulatory compliance and practical performance continue to drive preference for gravity-based designs over emerging technologies.

.png)

Market Share by Type/Installation: Above-Ground Systems as the Industrial Standard

By installation type, above-ground oil water separators are expected to represent about 55% of the market share in 2025, underscoring their strong adoption in industrial retrofits and compliance-driven projects. Above-ground systems are favored for their ease of inspection, maintenance, and integration with existing infrastructure, making them the go-to solution in manufacturing plants, power generation units, and heavy industry. In contrast, below-ground systems are increasingly adopted in municipal wastewater projects and new construction where space optimization is crucial. The marine segment, shaped by stringent IMO MEPC 107(49) and MARPOL standards, represents a specialized yet highly regulated market, emphasizing how environmental compliance continues to influence product design and adoption strategies.

Market Share by Capacity/Flow Rate: 100–500 GPM as the Industrial Sweet Spot

The 100–500 GPM capacity range dominates with nearly 40% of the global market share in 2025, reflecting its suitability for medium-sized industrial facilities, vehicle service stations, and manufacturing sites. The segment has become the practical balance point between performance and affordability, aligning with the needs of the majority of industrial users. Above 500 GPM systems cater to large-scale refineries, municipal treatment headworks, and offshore platforms, typically involving custom-engineered solutions with high capital investment. Meanwhile, smaller units below 100 GPM continue to serve automotive workshops, small machine shops, and decentralized discharge points, making them vital for standardized, packaged installations where footprint and cost efficiency are critical.

Market Share by End-Use Industry: Oil & Gas Sector as the Primary Growth Driver

The oil & gas sector is forecasted to capture approximately 25% of the global oil water separator market by 2025, reinforcing its position as the single largest end-user. The segment’s dominance is driven by the sheer volume and complexity of produced water, refinery wastewater, and stormwater runoff from terminals, all of which demand highly effective separation systems to meet environmental standards. Industrial and manufacturing users follow closely, as compliance with wastewater discharge regulations continues to tighten across developed and emerging economies. Marine applications remain highly regulation-driven, while municipal wastewater treatment and power generation collectively account for another quarter of demand. Niche sectors such as food & beverage, automotive, and aerospace are increasingly contributing to specialized adoption, reflecting how diverse end-use industries rely on oil water separators not just for compliance, but also for operational sustainability.

Country Analysis of the Oil Water Separator Market

United States: Regulatory Compliance Driving Advanced Separation Solutions

The U.S. oil water separator market is driven largely by stringent regulations imposed by the Environmental Protection Agency (EPA) and sections in the Clean Water Act. Standards for industrial water effluent are encouraging companies to invest in sophisticated oil water separator systems that not only treat oil efficiently but also recover hydrocarbons and provide them for reuse. The Bipartisan Infrastructure Law's $50+ billion investment in water and sewer system upgrades further accelerates deployment demand within municipal and oil and gas applications. Smart technology integration in the American market is becoming a deciding factor in favor of IoT-equipped monitoring and predictive maintenance powered by AI. Large industrial categories, especially oil and petroleum product-based, greatly depend upon these systems due to large flows of oily effluent produced during petroleum exploration and production, oil refining, and petrochemistry. Environmentally friendly and compliant technology leaders such as Xylem Inc. and Evoqua Water Technologies dominate this market.

China: Government Policies and Smart Automation Boost Market Growth

China oil water separator market is growing owing to policies of the government that provide a push to marine environmental protection and control of industrial effluent waters. Legislation mandates installation of oil water separation systems on offshore petroleum structures and ships to guarantee that treated effluent waters are released against tough standards. Adoption of automatic and sensor-based separation facilities is becoming widespread to aid monitoring and energy-efficient operations. Industrial initiatives that aid carbon control efforts are furthering uptake of energy-efficient separator facilities. Both technology deployment and regulatory compliance drive demand within Chinese industrial and shipping applications.

India: Industrial Effluent Regulations and National Programs Expand Demand

Indian oil water separator market is primarily driven by environmental laws such as the Water (Prevention and Control of Pollution) Act, 1974, and The Environment (Protection) Act, 1986. Enforcement at the behest of Central and State Pollution Control Boards requires industry-specific effluent quality standards, compelling implementations of efficient industrial oil water separation technology. Government programs such as the Namami Gange plan aim at large-scale treatment of wastewater, especially industrial effluent disposition, often dependent upon pre-engineered or packaged type separation schemes. Further, programs such as the Water Technology Initiative (WTI) ensure RD&D facilitation for sustainable waters technology, opening up opportunities for Indian companies to provide economical and high-performance separator technology both for industrial and marine applications.

Germany: Technological Innovation and Regulatory Compliance Fuel Growth

Germany’s oil water separator market benefits from the EU Water Framework Directive, which sets strict environmental standards for water quality. The market is witnessing the rise of efficient, compact separators employing advanced filtration and coalescence techniques. Companies such as Klaro GmbH and FRIESS GmbH are introducing innovative solutions like energy-efficient light oil separators and coalescer-based “Skimmtelligent” systems. Germany’s strong manufacturing and automotive sectors require separators for coolant and washing water, enabling extended equipment life and reduced disposal costs. The integration of sensors, data analytics, and digitalization is shaping interconnected and smart oil water separation networks across industrial facilities.

Saudi Arabia: Oil and Gas Expansion Drives Separator Demand

Saudi Arabia’s oil water separator market is primarily fueled by investments in the oil and gas sector under Vision 2030, with capital expenditures of $45-$55 billion for Aramco in 2025. The Saudi Water Partnership Company (SWPC) oversees public-private partnerships in water infrastructure, including wastewater treatment using advanced separators. Strategic collaborations, such as the Aramco-TotalEnergies petrochemical complex, require state-of-the-art oil water separation technologies. Additionally, emerging applications in carbon capture, hydrogen, and cleaner engine technologies are creating new market segments. Initiatives like the IKTVA program encourage domestic participation, promoting local manufacturing and deployment of high-performance industrial separators.

United Kingdom: Smart Filtration Solutions Respond to Environmental Standards

The UK’s oil water separator market is guided by environmental regulations consistent with European directives, promoting cleaner industrial, marine, and commercial operations. Companies like Walker Filtration have launched products such as the SmartSep Oil Water Separator, featuring organoclay filter cartridges and low-maintenance polypropylene bags, capable of achieving oil traces as low as 5 PPM. The increasing focus on efficient oil separation technologies and sustainable wastewater management is driving demand for advanced, easy-to-deploy separator systems across diverse industrial applications.

Competitive Landscape – Global Leaders Driving Oil Water Separator Innovation

The oil water separator market is shaped by a small number of global leaders leveraging diverse technology portfolios, strategic acquisitions, and strong service networks to maintain competitive advantage.

Veolia Environnement S.A. – Integrated Ecological Transformation Solutions

Veolia provides a complete range of oil water separation technology, ranging from gravity systems to ultimate coalescing plate designs, complemented by its Hubgrade™ digital services to optimize operations. It furthered its large-scale water reuse and industrial produced water treatment expertise with its acquisition of SUEZ. Veolia's TiPSS systems represent a market standard in the gravity-based removal of oil and can treat sophisticated industrial wastewater streams with minimal operator attention. Its global presence and integrated lifecycle service approach represent distinctives.

Ecolab Inc. (Nalco Water) – Industrial Water Treatment with Digital Optimization

Nalco Water blends chemical treatment know-how and 3D TRASAR™ monitoring to automate separation applications and provide compliance in real-time. Its August 2025 purchase of Ovivo's ultra-pure business broadens its ability to serve high-spec markets such as electronics production. Its twin specialization within chemicals and in digital control allows tailoring to heavy industry.

Alfa Laval – High-Speed Centrifugal Separation for Marine and Energy Sectors

Alfa Laval is a pioneer in centrifugal separation technology, with its PureBilge system designed to meet and exceed IMO MARPOL Annex I limits under variable flow conditions. Its marine focus is complemented by applications in the energy sector, where handling emulsified mixtures is a critical challenge. The company’s strong brand reputation, engineering heritage, and global service infrastructure reinforce its leadership position.

SUEZ (Part of Veolia) – Expertise in Produced Water and Industrial Wastewater Reuse

As part of Veolia today, SUEZ's heritage technology like API separator units, CPI units, and DAF units continues to be a core component of the integrated solution. Promising applications like PetroChina refinery plant in Chengdu demonstrate ability to integrate oil/water separation within broader schemes of wastewater reuse while meeting both regulatory compliance and operational efficiency goals.

Ovivo – High-Performance CPI Systems for Industrial Applications

Ovivo is a world leader in low-maintenance, high-strength CPI separators, and EnviroSEP system was developed to achieve ≤5 mg/L oil concentration in secondary effluent. Though it has divested the ultra-pure water business unit, Ovivo continues to innovate around basic industrial water treatment products. Its designs can be easily installed in refineries, petrochemical plants, and heavy manufacturing facilities.

Oil Water Separator Market Report Scope

Oil Water Separator Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$13.1 Billion

|

|

Market Size (2034)

|

$18.2 Billion

|

|

Market Growth Rate

|

3.7%

|

|

Segments

|

By Technology (Gravity Separators, Centrifugal Separators, Membrane Filtration Systems, Electrocoagulation Systems, Bioremediation Systems), By Type / Installation (Above Ground, Below Ground, Marine), By Capacity / Flow Rate (Below 100 GPM (Gallons Per Minute), 100-500 GPM, Above 500 GPM), By End-Use Industry (Oil & Gas, Marine, Industrial, Manufacturing, Automotive, Power Generation, Food & Beverage, Aerospace & Defense, Wastewater Treatment)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Alfa Laval AB, GEA Group AG, Andritz AG, Siemens AG, Parker-Hannifin Corporation, Wärtsilä Oyj Abp, Donaldson Company, Inc., SUEZ, Veolia, Aquatech International LLC, BOGE America, Inc., Ellis Corporation, Victor Marine, SPX Flow, Sulzer Chemtech Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Oil Water Separator Market Segmentation

By Technology

- Gravity Separators

- API Separators

- CPI (Corrugated Plate Interceptors)

- Hydrocyclone Separators

- Centrifugal Separators

- Membrane Filtration Systems

- Electrocoagulation Systems

- Bioremediation Systems

By Type / Installation

- Above Ground

- Below Ground

- Marine

By Capacity / Flow Rate

- Below 100 GPM (Gallons Per Minute)

- 100-500 GPM

- Above 500 GPM

By End-Use Industry

- Oil & Gas

- Marine

- Industrial

- Manufacturing

- Automotive

- Power Generation

- Food & Beverage

- Aerospace & Defense

- Wastewater Treatment

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Oil Water Separator Market

- Alfa Laval AB

- GEA Group AG

- Andritz AG

- Siemens AG

- Parker-Hannifin Corporation

- Wärtsilä Oyj Abp

- Donaldson Company, Inc.

- SUEZ

- Veolia

- Aquatech International LLC

- BOGE America, Inc.

- Ellis Corporation

- Victor Marine

- SPX Flow

- Sulzer Chemtech Ltd.

* List Not Exhaustive

Research Coverage

This report investigates the Global Oil Water Separator Market, presenting analysis reviews of regulatory impacts, industrial demand drivers, and technological breakthroughs transforming separation solutions across industries. Published by USDAnalytics, it highlights how global regulations such as IMO MARPOL Annex I and the U.S. EPA’s Clean Water Act are reshaping compliance requirements, compelling industries to adopt high-efficiency separators including coalescing plate, centrifugal, ultrafiltration, and IoT-enabled smart systems. The study further highlights consolidation trends, capacity expansions, and product innovations designed to address complex produced water, bilge water, and industrial effluent challenges. By covering key applications, regulatory milestones, and competitive strategies, this report is an essential resource for industry professionals, technology developers, regulators, and investors seeking clarity on evolving opportunities and long-term prospects in the oil water separator market.

Scope Includes:

- Segmentation: By Technology (Gravity Separators, Centrifugal, Membrane Filtration, CPI, DAF, Electrocoagulation, Others), By Type/Installation (Above-Ground, Below-Ground, Marine), By Capacity/Flow Rate (<100 GPM, 100–500 GPM, >500 GPM), and By End-Use Industry (Oil & Gas, Industrial Manufacturing, Marine, Municipal, Power, Food & Beverage, Automotive, Aerospace, Others).

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Timeframe: Historic data from 2021–2024 and forecast data from 2025–2034.

- Companies: Profiles and competitive analysis of 15+ leading companies active in the global oil water separator market.

Methodology

The research methodology developed by USDAnalytics applies a multi-layered approach combining both primary and secondary data sources. Primary research involved structured interviews with manufacturers, regulatory agencies, ship operators, oil & gas companies, and wastewater treatment specialists to validate technology adoption and market trends. Secondary research drew on government regulations, corporate filings, industry journals, and technical white papers. Market sizing was established through top-down and bottom-up modeling, further refined via data triangulation to ensure accuracy across regions, segments, and technologies. Scenario analysis was applied to assess regulatory enforcement, technology substitution, and investment trends, ensuring a reliable and forward-looking forecast that supports decision-making for stakeholders across the oil water separator ecosystem.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.

Table of Contents: Oil Water Separator Market

1. Executive Summary

1.1. Market Highlights

1.2. Key Insights

1.3. Global Market Snapshot

2. Oil Water Separator Market Overview, Size, and Growth Drivers (2025–2034)

2.1. Introduction to the Market

2.2. Market Valuation and Growth Projections (2025–2034)

2.2.1. Current Market Size (2025): $13.1 Billion

2.2.2. Forecasted Market Size (2034): $18.2 Billion at 3.7% CAGR

2.3. Key Drivers and Market Dynamics

2.3.1. Tightening Regulatory Mandates

2.3.2. Produced Water Management in Oil & Gas

2.3.3. Technological Innovations in Separation

3. Market Analysis: Regulatory Timelines and Strategic Developments

3.1. Overview of Market Evolution

3.2. Regulatory Catalysts

3.2.1. IMO MARPOL Annex I (January 2025)

3.2.2. U.S. EPA's Clean Water Act

3.3. Corporate and Strategic Developments

3.3.1. Nalco Water (Ecolab) Acquisition of Ovivo's Business

3.3.2. SUEZ/Veolia's PetroChina Plant Commissioning

3.3.3. Product Innovations (Alfa Laval's PureBilge, Ovivo's EnviroSEP™)

4. Trends and Opportunities in Oil Water Separator Market

4.1. Trend 1: High-Efficiency Electrocoagulation Systems

4.1.1. Superior Emulsified Oil Removal

4.1.2. Reduced Chemical Consumption and Sludge Generation

4.2. Trend 2: Smart Separators with IoT Connectivity

4.2.1. Real-Time Monitoring and Predictive Maintenance

4.2.2. Automated Operations for Unmanned Facilities

4.3. Opportunity 1: Offshore Wind Farm Expansion

4.3.1. Demand for Specialized Separators for Condensate and Bilge Water

4.3.2. Ensuring Environmental Compliance and Equipment Protection

4.4. Opportunity 2: Airport Deicing Fluid Recovery

4.4.1. Regulatory Attention to Airport Stormwater Runoff

4.4.2. Glycol Recovery for Cost-Effectiveness and Sustainability

5. Oil Water Separator Market Share Insights

5.1. By Technology

5.1.1. Gravity Separators

5.1.2. Centrifugal Separators

5.1.3. Membrane Filtration

5.2. By Type / Installation

5.2.1. Above-Ground Systems

5.2.2. Below-Ground Systems

5.2.3. Marine Separators

5.3. By Capacity / Flow Rate

5.3.1. 100–500 GPM

5.3.2. Above 500 GPM

5.3.3. Below 100 GPM

5.4. By End-Use Industry

5.4.1. Oil & Gas Sector

5.4.2. Industrial and Manufacturing Users

5.4.3. Marine, Municipal, and Power Applications

6. Country Analysis of the Oil Water Separator Market

6.1. United States: Regulatory Compliance and Infrastructure Investment

6.2. China: Government Policies and Smart Automation

6.3. India: Industrial Effluent Regulations and National Programs

6.4. Germany: Technological Innovation and EU Regulations

6.5. Saudi Arabia: Vision 2030 and Oil & Gas Sector Growth

6.6. United Kingdom: Smart Filtration Solutions

6.7. Other Country Analysis

7. Oil Water Separator Market Size Outlook by Region (2025–2034)

7.1. North America Market Size Outlook to 2034

7.1.1. By Technology, Type, Capacity, and End-User

7.2. Europe Market Size Outlook to 2034

7.2.1. By Technology, Type, Capacity, and End-User

7.3. Asia Pacific Market Size Outlook to 2034

7.3.1. By Technology, Type, Capacity, and End-User

7.4. South America Market Size Outlook to 2034

7.4.1. By Technology, Type, Capacity, and End-User

7.5. Middle East and Africa Market Size Outlook to 2034

7.5.1. By Technology, Type, Capacity, and End-User

8. Company Profiles: Top Companies in Oil Water Separator Market

8.1. Alfa Laval AB

8.2. Veolia Environnement S.A.

8.3. Ecolab Inc. (Nalco Water)

8.4. SUEZ (Part of Veolia)

8.5. Ovivo

8.6. GEA Group AG

8.7. Andritz AG

8.8. Siemens AG

8.9. Parker-Hannifin Corporation

8.10. Wärtsilä Oyj Abp

8.11. Donaldson Company, Inc.

8.12. Aquatech International LLC

8.13. Victor Marine

8.14. SPX Flow

8.15. Sulzer Chemtech Ltd.

9. Research Coverage & Methodology

9.1. Report Scope and Focus

9.2. Research Methodology

9.3. Deliverables

10. Appendix

10.1. List of Tables

10.2. List of Figures

10.3. Abbreviations