Oleic Acid Market Valued at $395 Million in 2025, Projected to Reach $587 Million by 2034 at 4.5% CAGR Amid Bio-Based Oleochemical Integration

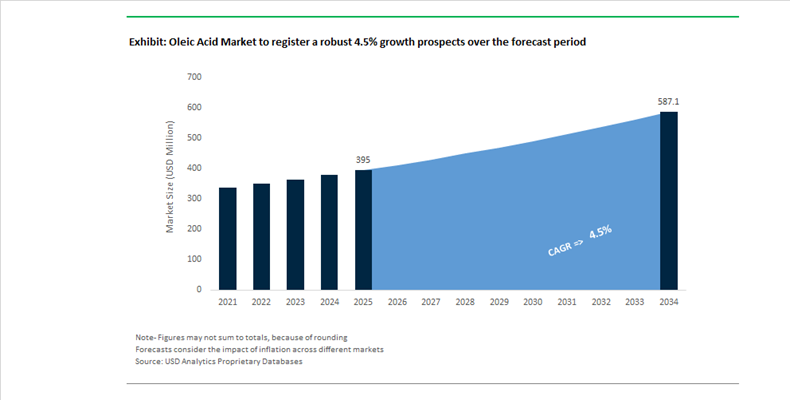

The Oleic Acid Market is valued at $395 Million in 2025 and is forecast to reach $587 Million by 2034, expanding at a CAGR of 4.5%. Growth is anchored in the expanding oleochemicals value chain, rising demand for bio-based surfactants, lubricants, and pharmaceutical excipients, and increasing integration between upstream palm oil refining and downstream fatty acid derivatives. Oleic acid, a monounsaturated C18 fatty acid, remains a strategic feedstock for tertiary amines, esters, amides, metallic soaps, biodiesel components, and polymer additives. The market is increasingly shaped by sustainability certification schemes, renewable carbon mandates, and traceable palm-based supply chains.

Throughout 2024 and 2025, Indonesia reinforced its B35 and B40 biodiesel mandates, tightening global crude oleic acid availability as fatty acid methyl ester demand accelerated. This policy shift increased price volatility in industrial-grade oleic acid and redirected supply toward energy markets. In October 2024, Emery Oleochemicals expanded its 100% bio-based portfolio by adding new pelargonic acid grades produced via ozonolysis of oleic acid, reinforcing the molecule’s importance as a green herbicide and industrial ester precursor. In January 2025, Croda International launched a comprehensive brand evolution marking its centenary year, emphasizing non-animal-derived, high-purity oleic acid grades for biopharmaceutical and consumer care applications.

Vertical integration intensified in June 2025 when Wilmar International announced the $70 million acquisition of PZ Cussons plc’s 50% stake in the PZ Wilmar joint venture. This move consolidates Wilmar’s control over its palm oil and oleochemical value chain, securing long-term feedstock stability for refined oleic acid and downstream derivatives. In July 2025, Emery Oleochemicals appointed Min Chong as Group CEO, signaling a sustainability-driven strategy focused on high-margin natural-based specialty chemicals, including pharmaceutical and polymer-grade oleic acid. In August 2025, Kao Corporation inaugurated a new tertiary amine plant in the United States. Tertiary amines are synthesized from fatty acids such as oleic acid, making this expansion a significant downstream demand driver for North American bio-based surfactants.

Regional market development strengthened in October 2025 when KLK OLEO established KLK OLEO India in Mumbai, targeting pharmaceutical and personal care demand in South Asia. The same month, KLK OLEO launched its Life Science business unit to expand plant-based pharmaceutical-grade oleic acid under its EDENOR and DavosLife brands. In June 2025, Emery Oleochemicals GmbH earned an EcoVadis Silver Medal, reflecting the growing procurement requirement for verified ESG performance among fatty acid suppliers. In January 2026, Croda International was named Britain’s Most Admired Chemicals Company following its 2025 expansion of the Super Refined™ facility in Staffordshire, strengthening capacity for ultra-pure oleic acid used in biologics manufacturing. In February 2026, Kao Corporation reported improved chemical segment sales driven by pricing adjustments across oleochemicals, indicating successful cost pass-through amid rising palm and soybean oil feedstock prices.

Oleic Acid Market Trends and Opportunities

Trend: Strategic Pivot to High-Oleic Seed Oils for Clean-Label and Low-Risk Feedstocks

The global oleic acid market is undergoing a structural shift toward high-oleic (HO) seed oils as chemical producers and consumer packaged goods companies de-risk their formulations from volatility, regulatory scrutiny, and clean-label backlash. High-oleic sunflower and canola oils are increasingly preferred over commodity soy and animal tallow because they offer superior oxidative stability without synthetic antioxidants or heavy genetic modification. This transition is directly reshaping upstream agricultural contracts and downstream oleochemical processing economics.

A key signal of this shift is the seed genetics strategy of Corteva, which reported a 33% increase in Seed net sales in Q3 2025, driven in part by demand for advanced high-oleic oilseed varieties. These crops deliver consistent oleic acid content above 70%, which is critical for producing detergents, surfactants, and personal care ingredients with longer shelf life and improved thermal stability. For chemical processors, this uniform fatty acid profile improves transesterification efficiency and reduces downstream purification losses.

On the supply chain side, Cargill has embedded high-oleic sourcing into its sustainability roadmap, achieving a 20.9% reduction in Scope 1 and 2 emissions by optimizing local, identity-preserved oil supply chains. Its 69 million dollar investment in efficiency projects supports refining high-oleic feedstocks into high-purity oleic acid for sustainable detergents and personal care formulations. Traceability is now a commercial differentiator rather than a compliance checkbox. By late 2025, more than 60% of North American consumers actively sought traceable functional oils, accelerating adoption of identity-preserved high-oleic feedstocks and reinforcing long-term offtake agreements between farmers, crushers, and oleochemical producers.

Trend: Capacity Expansion for Pharma-Grade Oleic Acid in mRNA and Injectable Delivery Systems

Oleic acid has transitioned from a commodity fatty acid to a critical pharmaceutical excipient due to the rapid expansion of mRNA and lipid nanoparticle technologies. Ultra-high-purity oleic acid is essential for synthesizing lipid nanoparticles that encapsulate and protect mRNA payloads, making purity, peroxide control, and metal impurity thresholds non-negotiable.

Strategic investments by innovators such as Pfizer, following its long-term collaboration with Acuitas Therapeutics, have created sustained demand for injectable-grade oleic acid beyond pandemic-related applications. With mRNA platforms expanding into oncology, protein replacement, and rare disease pipelines through 2025 and beyond, supply-side constraints are emerging for ≥99 percent pure oleic acid that meets GMP and injectable-grade specifications.

To address this, oleochemical manufacturers are commissioning dedicated white-room distillation and molecular separation lines that isolate oleic acid from linoleic and palmitic fractions with exceptional consistency. Pharmaceutical-grade suppliers are now filtering oleic acid to remove trace metals and peroxides that could destabilize lipid nanoparticles or degrade sensitive mRNA constructs. This shift is structurally upgrading the value mix of the oleic acid market, with pharma-grade volumes commanding premium pricing and long-term supply contracts that are insulated from cyclical demand in soaps and surfactants.

Opportunity: Oleate-Based Esters as Environmentally Acceptable Lubricants for Marine and Offshore Use

Environmental regulation in maritime and offshore industries is creating a mandatory growth avenue for oleic acid derivatives in the form of environmentally acceptable lubricants. High-oleic esters offer a rare combination of high viscosity index, strong boundary lubrication, and rapid biodegradability, positioning them as direct substitutes for mineral-based lubricants at oil-to-sea interfaces.

The enforcement of the Vessel Incidental Discharge National Standards of Performance by the U.S. Environmental Protection Agency has reinforced the requirement that lubricants be readily biodegradable, exceeding 60% degradation in 28 days under OECD 301 protocols. Oleate esters comfortably meet this threshold, accelerating their adoption in stern tubes, thrusters, and deck machinery. In parallel, regulatory pressure from the OSPAR Commission is driving North Sea operators to replace mineral oils with synthetic oleate esters that provide equivalent load-bearing performance with minimal aquatic toxicity risk.

Technological advances are further expanding the addressable market. Chemical modification of oleic acid has reduced pour points below minus 30 degrees Celsius, overcoming historical cold-flow limitations of vegetable oil derivatives. This positions oleate-based lubricants for Arctic, deep-water, and cold-climate offshore applications, transforming them from niche green alternatives into performance-critical industrial fluids.

Opportunity: Oleic Acid Derivatives for High-Capacity and Sustainable Battery Binders

The transition toward silicon-dominant anodes in electric vehicle batteries is exposing the mechanical limitations of conventional binders such as PVDF, which cannot tolerate silicon’s extreme volume expansion during cycling. Oleic acid derivatives are emerging as a high-potential solution in next-generation battery architectures.

Peer-reviewed research published in 2024 and 2025 demonstrates that oleic-acid-derived small molecules and polymers can function as flexible binders or artificial solid electrolyte interfaces. Their long-chain alkyl structures act as mechanical buffers, reducing particle pulverization and preserving electrode integrity during repeated lithiation and delithiation. This directly supports longer cycle life and higher usable capacity in silicon-rich anodes.

An additional opportunity lies in aqueous battery manufacturing. Water-soluble oleate dispersants are enabling stable slurry rheology and uniform electrode coating, allowing manufacturers to move away from N-methyl-2-pyrrolidone solvents. This aligns battery production with tightening environmental standards and lowers overall carbon intensity. Further downstream, bio-based azelaic acid derived from high-oleic oils is gaining attention as a monomer for high-performance battery polymers. A December 2025 study by the U.S. Department of Energy highlighted a competitive bio-based production pathway approaching carbon neutrality, reinforcing oleic acid’s role as a strategic feedstock in the sustainable battery materials ecosystem.

Oleic Acid Market Share and Segmentation Insights

Plant-Based Oleic Acid Dominates Supply Through High-Oleic Oilseed Production and Sustainable Feedstocks

Plant-based oleic acid accounted for 72.80% of the Oleic Acid Market by source in 2025, reflecting strong demand for renewable, vegan, and sustainable fatty acid ingredients across global industries. Derived primarily from vegetable oils such as palm, sunflower, rapeseed, and soybean, plant-based oleic acid benefits from stable agricultural supply chains and consistent quality control in large-scale oilseed processing. Market growth is increasingly supported by the development of high-oleic oilseed varieties, including high-oleic sunflower, canola, and soybean crops that produce oils containing 80–90% oleic acid content. These advanced oilseed cultivars reduce purification requirements, improve production efficiency, and enable the supply of premium-grade oleic acid for pharmaceutical, cosmetic, and specialty chemical applications.

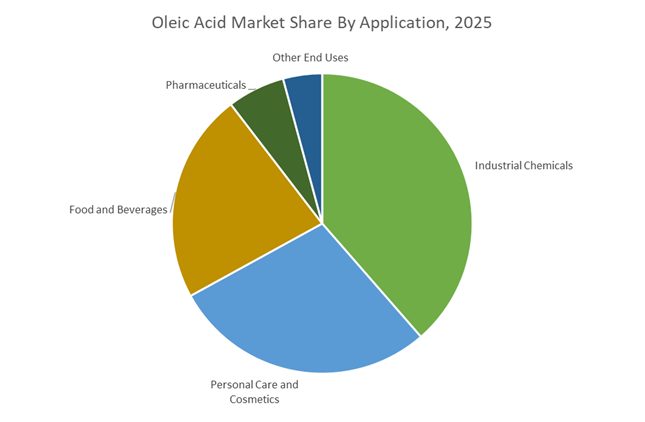

Industrial Chemicals Segment Leads Oleic Acid Consumption Across Surfactants and Bio-Based Chemical Production

Industrial chemicals held 38.60% of the Oleic Acid Market by application in 2025, making it the largest consumption segment driven by extensive use in surfactants, lubricants, coatings, and rubber processing chemicals. Oleic acid functions as a critical feedstock in the production of soaps, detergents, metalworking lubricants, greases, and surface-active agents used in multiple industrial manufacturing sectors. The growing transition toward bio-based chemical intermediates is further strengthening demand, as oleic acid serves as a renewable platform molecule for producing bio-based polymers, plasticizers, and specialty surfactants. Chemical manufacturers are increasingly investing in oleochemical conversion technologies that transform oleic acid derivatives into sustainable alternatives to petroleum-based industrial chemicals.

Oleic Acid Market Competitive Landscape

The oleic acid market in 2026 is driven by RSPO-certified feedstock diversification, high-purity oleochemical demand, and bio-lubricant integration. Competitive differentiation centers on traceable supply chains, premium food-grade oleic acid, and vertically integrated oleochemicals addressing regulatory compliance and shifting palm oil export dynamics.

KLK OLEO leverages integrated oleochemical assets to deliver high-purity oleic acid across life science and personal care sectors

KLK OLEO operates a globally integrated network of 16 manufacturing facilities, enabling seamless production of high-purity oleic acid under brands like PALMAC®. Its vertically integrated plantation-to-derivative model ensures traceability, supply reliability, and cost control amid Southeast Asian supply disruptions. The company is expanding its sustainable personal care portfolio, emphasizing clean-label formulations through its Sympare Sense range. With a market capitalization of USD 5.45 billion and recognition in the FORTUNE Southeast Asia 500, KLK OLEO maintains strong financial and operational positioning. Its focus on life sciences, food-grade oleochemicals, and specialty derivatives aligns with premiumization trends. This integration-driven strategy strengthens its leadership in global oleic acid markets.

Wilmar drives traceability and ESG-led growth with large-scale oleochemical integration and downstream consolidation

Wilmar International is reinforcing its dominance through a data-driven ESG strategy, targeting 100% Traceability to Plantation (TtP) by 2026, with 91% already achieved across 24 million tonnes of palm products. Its US$70 million acquisition of PZ Cussons’ stake enhances downstream control in surfactants and consumer chemicals. With FY2025 net profit of US$1.41 billion, Wilmar continues investing in low-carbon certified oleic acid and glycerin portfolios backed by SBTi-validated net-zero targets. Its Landscape Projects further strengthen sustainable sourcing and emissions reduction. The company’s scale and traceability provide a strong compliance advantage in regulated markets. This ESG-led integration positions Wilmar as a key supplier of premium oleochemicals globally.

IOI Corporation expands high-margin specialty oleochemicals with RSPO-certified feedstock and pharmaceutical-grade innovation

IOI Corporation is shifting toward value-added downstream products, leveraging RSPO-certified palm oil to capture premium pricing in global markets. Its PALMAC® oleic acid portfolio is enhanced by proprietary Core Shell technology, enabling applications in pharmaceutical excipients and specialty chemicals. A 5–8% projected increase in FFB production ensures feedstock security for expansion initiatives. Strategic investments include a new specialty fats plant in Amsterdam and capacity growth via Bunge Loders Croklaan in the U.S. IOI is also diversifying into coconut-based oleochemicals to reduce reliance on palm feedstocks. This multi-feedstock and high-purity strategy strengthens its competitive positioning.

Emery Oleochemicals focuses on bio-based performance chemicals for coatings and lubricant applications

Emery Oleochemicals is advancing its “Engineered Performance” strategy with a strong emphasis on bio-based oleochemical derivatives for coatings, lubricants, and elastomers. Its USDA BioPreferred® certified portfolio and bio-based polyols (48%–99% content) target high-performance industrial applications. Under new leadership, the company is strengthening feedstock integration and sustainability-driven operations. Its Cincinnati facility’s ISO 50001 certification underscores energy efficiency and environmental compliance. Emery’s participation in ACS 2026 highlights its focus on eco-friendly coatings and adhesives. This specialization in high-value applications positions Emery as a premium player in oleic acid derivatives.

Musim Mas strengthens sustainable oleochemical supply with smallholder integration and long-term decarbonization roadmap

Musim Mas is executing its 2026–2030 sustainability roadmap focused on responsible sourcing, sustainable production, and smallholder empowerment. Its GS Series high-yield oil palm varieties enhance feedstock productivity and long-term supply stability. The company has trained over 9,400 smallholders, ensuring compliance with global sustainability and labor standards. SBTi-validated emissions targets reinforce its commitment to low-carbon oleochemical production. Its integrated refining and kernel-crushing operations support consistent oleic acid output despite export tightening in Indonesia. Musim Mas’ focus on resilient supply chains and ESG compliance strengthens its global market competitiveness.

Indonesia – Biodiesel Pull Reshaping Oleochemical Export Economics

Indonesia’s oleic acid industry is undergoing a structural realignment as biofuel policy increasingly competes with oleochemical exports for crude palm oil feedstock. Following discussions at IPOC 2025, Indonesia reaffirmed its role as the world’s largest exporter of palm-based oleochemicals, even as exports are expected to soften in 2026 due to accelerating domestic absorption. The government’s decision to raise the biodiesel mandate to B40 in February 2025, alongside formal tracking toward B50 by the second half of 2026, is materially tightening CPO availability for fatty acid and oleic acid production. This policy-driven feedstock constraint is shifting producer priorities toward higher-value refined oleic acid grades rather than volume-led exports.

Supply chain governance and sustainability are now central to Indonesia’s competitive positioning. Musim Mas Group announced a new landscape strategy in October 2025, supported by four high-yield oil palm varieties designed to meet EU Deforestation Regulation requirements ahead of 2026 enforcement. Government intervention has further stabilized upstream supply through the reclamation of more than 3.3 million hectares of illegally acquired plantation land, now managed by state-owned Agrinas Palma Nusantara. On the processing side, integrated oleochemical complexes in Jakarta and Medan completed upgrades in 2025 to boost output of 65 to 75% purity refined oleic acid for the Asia Pacific cosmetics market. Advanced AI-driven satellite monitoring partnerships are also being deployed to certify deforestation-free sourcing, particularly for pharmaceutical and personal care grade oleic acid.

Malaysia – Certified Supply and Specialty Oleic Acid Differentiation

Malaysia’s oleic acid industry continues to strengthen its premium positioning through certification depth, R&D intensity, and portfolio consolidation. More than half of Malaysia’s planted palm area now carries dual RSPO and MSPO certification, positioning the country as a preferred supplier for European green chemistry and regulated personal care applications. Strategic market access is expanding, with KLK OLEO opening a representative office in Mumbai in February 2025 to accelerate exports of specialty fatty acids and oleic acid esters into India.

Financial performance and consolidation reinforce this momentum. Wilmar International reported a sharp increase in profitability during the first half of 2025, driven largely by its oleochemicals and specialty fats division, and subsequently moved to acquire full control of its joint venture with PZ Cussons. Innovation remains a differentiator. Malaysian research institutes disclosed late-2025 breakthroughs in oleic-acid-assisted nanolubricants derived from palm kernel oil, delivering substantial friction reduction under extreme pressure conditions. Parallel commitments by producers such as IOI Oleo to science-based net-zero targets for 2026 are accelerating renewable energy integration into distillation and fractionation operations, strengthening Malaysia’s long-term sustainability credentials.

United States – High-Purity Demand and Feedstock Diversification

The United States oleic acid market is characterized by downstream-driven demand for high-purity, application-specific formulations rather than feedstock-scale expansion. Product innovation is a key theme. In May 2025, Emery Oleochemicals introduced EMEROX® specialty acids at STLE 2025, highlighting oleic-acid-based friction modifiers optimized for electric vehicle thermal management and drivetrain fluids. The U.S. also remains a primary consumer of high-oleic formulations in the snack food and pharmaceutical sectors, with sustained growth in demand for USP-compliant pharmaceutical-grade oleic acid.

Sustainability and regulatory alignment are shaping sourcing strategies. Partnerships launched in mid-2025 between specialty chemical suppliers and Tier-1 personal care brands accelerated the adoption of plant-derived oleic acid emulsifiers for clean-label skincare. At the same time, U.S. manufacturers are diversifying away from palm-oil-linked volatility by increasing procurement of high-oleic sunflower and safflower oils. Investment is flowing into ester base stocks for biodegradable lubricants, supported by rising demand for bio-lubes and new FDA guidance encouraging biocompatible excipients, where oleic acid plays a critical role in controlled-release drug delivery systems.

India – Policy Support and Rapid Capacity Build-Out

India is emerging as the fastest-growing oleic acid market globally, underpinned by government-backed oilseed programs and expanding downstream consumption. New high-oleic oilseed initiatives launched in 2025 are improving domestic feedstock availability, while the Oilfield Regulation and Development Amendment Act has incentivized the use of bio-based surfactants derived from oleic acid in sustainable drilling fluids. Corporate consolidation is accelerating domestic capability, with Godrej Industries completing the acquisition of Savannah Surfactants to scale bio-based offerings for home and personal care applications.

Biofuel integration is reinforcing oleochemical synergies. Under the SATAT initiative, more than 130 compressed bio-gas plants commissioned by late 2025 are generating sustainable byproducts that feed into localized oleochemical synthesis. On the demand side, a pronounced shift toward natural and organic personal care products among India’s middle class is driving double-digit growth in cosmetic-grade oleic acid consumption. In parallel, new entrants in Gujarat and Maharashtra have announced plans for fractional distillation units by 2026, targeting 99% high-purity oleic acid grades for pharmaceuticals and specialty formulations.

Germany – Pharmaceutical-Grade Leadership and Advanced Processing

Germany anchors the European oleic acid market through its dominance in ultra-high purity pharmaceutical applications and regulatory-driven innovation. The country leads regional consumption for pharmaceutical-grade oleic acid, supported by stringent quality benchmarks and clean-label reformulation trends in food and personal care. Strategic partnerships are reinforcing this position. BASF SE entered into a collaboration with RiKarbon to develop bio-based emollients using oleic acid as a core building block, targeting premium personal care formulations.

Regulatory frameworks are influencing derivative selection. Approaching 2026 deadlines for biocidal active substances are encouraging substitution toward non-toxic oleic acid derivatives across industrial and consumer applications. At the K 2025 trade fair, German producers showcased oleic-acid-derived bio-based plasticizers for lightweight polymers, underscoring diversification beyond traditional fatty acid markets. Germany also remains a global hub for NIAS testing, ensuring exported oleic acid meets international food safety requirements. Investment in supercritical fluid extraction by academic-industrial consortia is further advancing allergen-free oleic acid production from domestic rapeseed oil, strengthening supply resilience and traceability.

Comparative Country Snapshot – Oleic Acid Industry

Oleic Acid Market County Level Snapshot

|

Country

|

Primary Growth Driver

|

Feedstock or Technology Focus

|

Strategic Market Position

|

|

Indonesia

|

Biodiesel mandates and supply control

|

Palm oil, AI-verified sourcing

|

High-volume production with sustainability transition

|

|

Malaysia

|

Certification and specialty expansion

|

Certified palm derivatives, nanolubricants

|

Premium supplier for green chemistry

|

|

United States

|

High-purity downstream demand

|

High-oleic seed oils, bio-lubes

|

Application-led innovation hub

|

|

India

|

Government programs and consumer shift

|

Domestic oilseeds, fractional distillation

|

Fastest-growing consumption market

|

|

Germany

|

Pharmaceutical and regulatory leadership

|

Rapeseed oil, SFE processing

|

Ultra-high purity and compliance benchmark

|

Oleic Acid Market Report Scope

Oleic Acid Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$395 Million

|

|

Market Size (2034)

|

$587 Million

|

|

Market Growth Rate

|

4.5%

|

|

Segments

|

By Source (Plant-Based, Animal-Based), By Grade (Pharmaceutical Grade, Food Grade, Industrial Grade), By Application (Personal Care and Cosmetics, Food and Beverages, Pharmaceuticals, Industrial Chemicals, Other End Uses)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Wilmar International, BASF, KLK OLEO, Emery Oleochemicals, Oleon, Musim Mas, Cargill, Godrej Industries, Croda International, Eastman Chemical, IOI Oleochemical, Vantage Specialty Chemicals, Kao, Pacific Oleochemicals, Archer Daniels Midland

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Oleic Acid Market Segmentation

By Source

By Grade

- Pharmaceutical Grade

- Food Grade

- Industrial Grade

By Application

- Personal Care and Cosmetics

- Food and Beverages

- Pharmaceuticals

- Industrial Chemicals

- Other End Uses

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Oleic Acid Industry

- Wilmar International

- BASF

- KLK OLEO

- Emery Oleochemicals

- Oleon

- Musim Mas

- Cargill

- Godrej Industries

- Croda International

- Eastman Chemical

- IOI Oleochemical

- Vantage Specialty Chemicals

- Kao

- Pacific Oleochemicals

- Archer Daniels Midland

*- List not Exhaustive