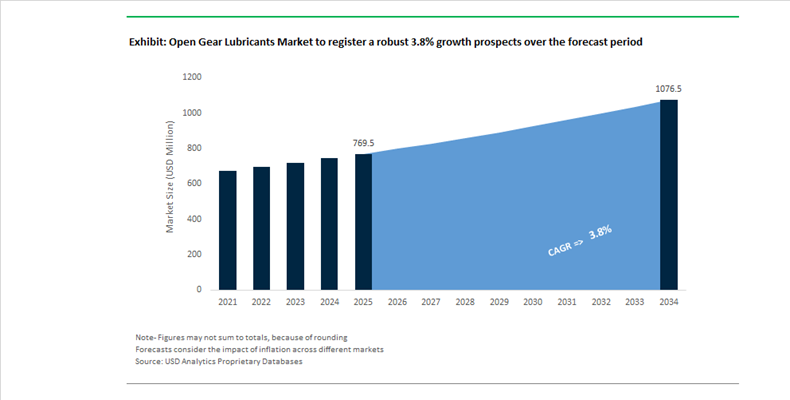

Open Gear Lubricants Market Valued at $769.5 Million in 2025, Projected to Reach $1,076.4 Million by 2034 at 3.8% CAGR Amid Digital Reliability and Sustainable Formulation Shift

The Open Gear Lubricants Market is valued at $769.5 Million in 2025 and is projected to reach $1,076.4 Million by 2034, registering a CAGR of 3.8%. Market expansion is driven by rising capital expenditure in mining, cement, power generation, and bulk material handling sectors where large girth gears, kilns, ball mills, and crushers operate under extreme shock loads and boundary lubrication regimes. Growth is increasingly tied to reliability engineering, predictive maintenance, and sustainability compliance. OEMs and plant operators are shifting from conventional asphaltic compounds toward synthetic, semi-fluid, and high-viscosity open gear lubricants engineered for improved adhesion, micropitting resistance, and reduced consumption rates. Advanced base oil chemistry and solid lubricant dispersion technologies are becoming core differentiators in procurement decisions.

In early 2025, Klüber Lubrication introduced Klübersynth OA 98-15000, utilizing Solid Lubricant Integrated Base Fluid technology to reduce nozzle clogging and lubricant consumption in cement and mining operations. In April 2025, FUCHS SE strengthened its specialty lubrication capabilities through the acquisition of IRMCO, enhancing film-forming chemistry expertise relevant to its CEPLATTYN open gear series. In July 2025, Shell plc completed the acquisition of Raj Petro Specialities Pvt. Ltd., expanding localized production of industrial greases and open gear lubricants in India. In September 2025, FUCHS announced a strategic partnership with KCF Technologies, integrating AI-driven vibration and temperature monitoring with lubricant dosing systems to enable condition-based lubrication in heavy industrial gear drives.

Sustainability and regional capacity expansion are reshaping supply chains. In October 2025, Klüber launched REDcert²-certified lubricants based on biomass-balanced feedstocks to reduce lifecycle carbon intensity without compromising extreme-pressure performance. In November 2025, Whitmore Manufacturing LLC, a subsidiary of CSW Industrials, acquired Hydrotex Partners Ltd., broadening its open gear and reliability portfolio for power generation and agriculture sectors. In February 2026, Lubrizol Corporation and VKTR introduced the Sustainable Mining Operations Alliance in Indonesia, focusing on molecularly engineered lubricants to extend gear life and minimize chemical waste in high-load mining conditions.

Manufacturing localization is accelerating in high-growth Asia. ExxonMobil’s lubricant plant in Isambe, Maharashtra, is scheduled to commence full operations by late 2025 with a 159,000 kiloliter annual capacity, targeting demand for Mobilgear OGL products in Indian cement and mining industries. In November 2025, Klüber Lubrication India received a Green Energy Efficiency Initiative Award for developing friction-reducing gear lubricants that deliver measurable electricity savings in kiln gearboxes. Portfolio-wide additive advancements are also influencing industrial formulations. In August 2025, Shell upgraded its Helix product line to meet the 2025 API SQ standard, incorporating anti-wear and deposit-control chemistries that are being adapted for heavy-duty industrial gear systems.

The open gear lubricants market is transitioning toward digitally integrated lubrication management, biomass-balanced formulations, localized manufacturing in Asia-Pacific, and high-performance synthetic chemistries engineered for shock-load durability and energy efficiency across mining and cement megaprojects.

Open Gear Lubricants Market Trends and Opportunities

Trend: Mandatory Shift Toward Biodegradable and Non-Toxic Open Gear Lubricants

Environmental compliance has moved from a procurement preference to a binding operational requirement in open gear lubrication across mining, marine, and offshore industries. The June 2025 update to EU chemical legislation under Commission Regulation (EU) 2025/1090 has tightened restrictions on hazardous solvents and polymers listed in REACH Annex XVII. This has materially accelerated the phase-out of traditional bitumen-based and solvent-rich open gear sprays, replacing them with solvent-free synthetic ester formulations capable of achieving more than 90% biodegradation within 28 days under OECD 301B criteria. From a market standpoint, this regulatory tightening is reshaping formulation economics, supplier qualification, and long-term maintenance strategies.

In offshore environments, compliance with the U.S. EPA’s Vessel Incidental Discharge Act standards has driven operators in the North Sea and the Gulf of Mexico to adopt polyol ester-based environmentally acceptable lubricants. These lubricants provide strong polar attraction to metal surfaces, forming a persistent lubricating film that resists saltwater washout while maintaining a low aquatic toxicity profile in the event of incidental discharge. For mining operators, particularly in environmentally sensitive regions such as Australia’s Pilbara, environmental audits conducted during 2024–2025 show a 15% rise in the use of vegetable-oil-based open gear lubricants near groundwater catchments. This shift reflects a broader risk-management mindset, where lubricant selection is now directly tied to environmental liability, remediation cost avoidance, and the ability to maintain operating permits.

Trend: Adoption of Smart Automated Lubrication Systems with Condition Monitoring

Open gear lubrication is undergoing a structural transformation as Industry 4.0 principles are embedded into heavy asset maintenance. Manual, time-based lubrication is being replaced by automated lubrication systems integrated with real-time monitoring and predictive analytics. By late 2025, suppliers such as SKF and Bijur Delimon had commercialized IoT-enabled lubrication platforms capable of tracking gear temperature, vibration signatures, and lubricant film thickness in real time. Field data indicates that these systems reduce lubricant consumption by 20–30% while extending gear life by as much as 50%, materially improving total cost of ownership for high-value gear sets.

The value proposition is particularly compelling in remote operations. In large-scale mining projects such as Simandou in Guinea, centralized automated lubrication systems are now standard, engineered to operate reliably across temperature ranges from minus 40°C to plus 50°C. Heated reservoirs, insulated delivery lines, and viscosity-managed formulations ensure consistent lubricant flow even under extreme climatic stress. Beyond mechanical benefits, digital lubrication records have become critical for compliance. Automated systems generate timestamped lubrication logs that support ISO 55001 asset management requirements and simplify regulatory and safety audits. As documentation expectations rise, digital traceability is becoming a decisive purchasing factor alongside lubricant performance.

Opportunity: High-Load Extreme Pressure Lubricants for Offshore Wind Yaw and Pitch Gears

The rapid scaling of offshore wind turbines to 15 MW and 20 MW capacities has created a high-margin opportunity for advanced open gear lubricants capable of handling extreme static and dynamic loads. Yaw and pitch drives in these turbines experience contact pressures of 150 to 200 bar, particularly during cold starts and prolonged idle periods. According to the 2025 NREL wind turbine design guidance, lubricants with solid lubricant contents of approximately 15%, such as molybdenum disulfide or graphite, are increasingly specified to mitigate fretting corrosion and micro-pitting.

Field trials conducted in the North Sea during 2024 demonstrated that lithium-complex and calcium-sulfonate thickened greases deliver superior adhesion and resistance to water spray-off compared to conventional products. These formulations maintain a stable protective film even under constant salt exposure, addressing one of the primary failure modes in offshore drivetrains. The economic logic is compelling. With offshore repair campaigns often exceeding USD 100,000 per day due to vessel mobilization costs, turbine operators are prioritizing lubricant reliability as a risk-reduction tool. This has led to growing demand for premium synthetic gear lubricants compatible with fine filtration down to five microns and real-time oil condition monitoring, creating a defensible, specification-driven niche within the broader open gear lubricants market.

Opportunity: Non-Flammable Lubricants for High-Temperature Steel and Cement Kilns

Steel mills and cement kilns represent another structurally attractive opportunity where conventional lubricants fail under extreme thermal stress. Surface temperatures on rotary kilns and mill gears frequently exceed 500°C, conditions under which asphaltic or mineral greases carbonize, ignite, or form abrasive residues. To address this, suppliers such as Whitmore and Petron have developed graphite-based dry film and synthetic gel lubricants. These systems allow the carrier fluid to evaporate after application, leaving a solid lubricating layer stable up to approximately 538°C, well beyond the operational limits of traditional greases.

Safety considerations are a major adoption driver. Steel industry safety assessments published in late 2024 show that replacing low-flash-point asphaltic products with high-flash-point synthetic lubricants reduces the risk of flash fires and eliminates the formation of hardened grease deposits in gear tooth roots. In cement operations, 2025 field data indicates that high-viscosity synthetic fluids, including advanced girth gear oils such as the Berugear HV class, enable longer relubrication intervals while maintaining robust lambda film thickness. This not only reduces maintenance downtime but also lowers energy losses associated with poorly lubricated gear meshes, directly supporting decarbonization and energy-efficiency targets across heavy industry.

Open Gear Lubricants Market Share and Segmentation Insights

Grease-Type Open Gear Lubricants Lead Market Demand Due to Superior Adhesion and Load-Carrying Capacity

Grease-type lubricants accounted for 42.80% of the Open Gear Lubricants Market by product type in 2025, making them the dominant lubrication solution for heavy-duty industrial gears. Their strong adhesion to exposed gear surfaces enables them to resist lubricant throw-off under high centrifugal forces while maintaining a durable protective film under extreme loads and contamination. These properties make grease-based open gear lubricants widely used in mining machinery, cement kilns, and large construction equipment where operational reliability is critical. A key 2025 development is the emergence of semi-fluid grease formulations, which combine high adhesion with improved pumpability, enabling centralized automatic lubrication systems that reduce manual maintenance requirements and enhance operational safety in large industrial installations.

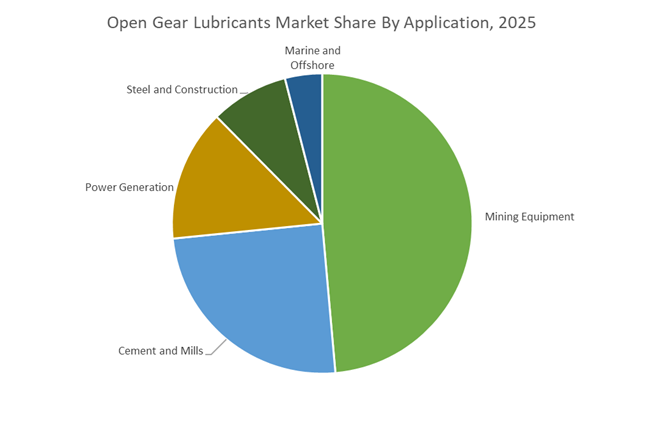

Mining Equipment Segment Drives Open Gear Lubricant Consumption in High-Load Industrial Operations

Mining equipment represented 48.60% of the Open Gear Lubricants Market by application in 2025, reflecting the intensive lubrication requirements of large-scale surface mining machinery. Open gears used in draglines, electric shovels, excavators, and haul trucks operate under extreme mechanical loads, abrasive contamination, and wide temperature variations, making high-performance lubrication essential to prevent gear wear and failure. Continuous mining operations require reliable lubricant performance to maintain equipment uptime and productivity. A significant 2025 trend is the integration of condition monitoring technologies, where operators use wear debris analysis, lubricant viscosity monitoring, and thermal imaging to track gear health, optimize lubrication intervals, and detect early-stage gear distress in mission-critical mining equipment.

Open Gear Lubricants Market Competitive Landscape

The open gear lubricants market in 2026 is driven by synthetic high-viscosity formulations, predictive lubrication services, and biodegradable EAL-compliant solutions. Competitive advantage lies in integrated reliability services, digital condition monitoring, and high-adhesion lubricants for mining, cement, marine, and heavy industrial gear systems.

Shell strengthens global leadership with synthetic base oil innovation and expanding industrial grease capacity

Shell maintains its dominance in open gear lubricants through its “Powering Progress” strategy, combining scale, advanced base oil technology, and strong OEM partnerships. The acquisition of Raj Petro Specialities enhances its footprint in high-growth industrial markets, particularly India. Its PurePlus Technology delivers 99.5% pure base oils, improving oxidation stability and gear protection under extreme loads. Expansion of its Indonesia grease manufacturing plant supports demand from mining and power sectors in Asia-Pacific. Long-term collaborations with OEMs like BMW and Ducati reinforce product validation and co-development capabilities. This integrated model positions Shell as a leader in high-performance, reliability-focused lubrication solutions.

ExxonMobil leverages upstream scale and digital monitoring to deliver lubrication-as-a-service solutions

ExxonMobil is capitalizing on its vertically integrated value chain and record upstream production of 4.7 million barrels per day to secure base stock supply for open gear lubricants. The Singapore Resid Upgrade enhances feedstock efficiency, supporting cost-competitive lubricant production. Its Mobil™ Lubricant Analysis and condition monitoring platforms enable predictive maintenance, optimizing oil drain intervals and reducing total cost of ownership. With $21.4 billion upstream earnings in 2025, ExxonMobil has strong financial backing for specialty product growth. The company is investing $1.0 billion in lower-carbon technologies, including friction-reducing lubricants. This service-led approach strengthens its position in industrial lubrication ecosystems.

TotalEnergies advances high-viscosity synthetic gear protection with OEM-approved additive technologies

TotalEnergies is differentiating through its GEARLOG and LUBRILOG portfolios, offering bitumen-free, fire-resistant open gear lubricants with white solid additive technology. Its GRAFOLOG aluminum complex greases provide high adhesion and load-carrying capacity, approved by OEMs such as FLSmidth and Metso Outotec. The company is expanding its presence in emerging markets through localized packaging and distribution strategies, particularly in India. Its LubAnac Fleet Management System enhances predictive maintenance through real-time oil analysis. Strong R&D capabilities support continuous innovation in heavy-duty lubrication systems. This positions TotalEnergies as a specialist in high-performance girth gear protection.

FUCHS leads biodegradable open gear lubrication with advanced inspection and circular technology integration

FUCHS is strengthening its leadership in sustainable lubrication through its ACT (Advanced Circular Technologies) framework and biodegradable PLANTO product range. CEPLATTYN remains a benchmark for adhesive open gear lubricants in mining and cement industries. Its digital FUCHS Lubricants Inspector system enables precise monitoring of gear conditions, improving maintenance efficiency. Operating in over 50 countries with 3,000+ products, FUCHS offers highly customized solutions for extreme environments. Its Plant Review services optimize lubrication cycles, extending gear life beyond 40 years. This sustainability-driven and service-oriented approach enhances its competitive differentiation.

Klüber Lubrication expands specialty portfolio with energy-efficient solutions and automated lubrication systems

Klüber Lubrication is reinforcing its position as a specialty lubricant leader through the integration of OKS, creating a portfolio exceeding €1 billion in annual sales. Its synthetic lubricants deliver 2–3% verified energy savings, with large-scale deployments achieving up to 7.65 million kWh annually. The acquisition of TriboServ strengthens its capabilities in automatic lubrication systems, critical for remote and continuous operations. EcoVadis Gold recognition highlights its leadership in sustainability and ESG performance. Klüber focuses on high-efficiency formulations tailored for demanding industrial gear systems. This positions the company strongly in energy-efficient and automated lubrication solutions.

Chevron enhances industrial gear reliability with environmentally compliant lubricants and system cleaning technologies

Chevron is advancing its open gear lubricants portfolio through high-performance formulations that meet EPA TCLP standards, ensuring low environmental impact and high load-bearing capacity. Its VARTECH® Industrial System Cleaner improves gear system efficiency by removing varnish and sludge without downtime. The Meropa® XL range supports long-term reliability in heavy-duty applications. Chevron’s $18–$19 billion 2026 capital program ensures stable feedstock supply and supports lubricant innovation. Investments in carbon capture and clean energy technologies align with industrial decarbonization trends. This integrated energy and lubrication strategy strengthens Chevron’s position in sustainable industrial maintenance solutions.

United States – PFAS-Free Reformulation and Predictive Maintenance Integration

The United States open gear lubricants industry is advancing through a combination of additive innovation, environmental compliance, and digital asset management. In late 2024, The Lubrizol Corporation launched the Lubrizol® GR91GC additive package, engineered specifically for Type 2 stationary open gear systems in mills and kilns. Built on Lucant™ base fluid technology, the formulation demonstrated measurable reductions in operating temperatures, supporting extended gear life under high-load conditions. This performance-driven innovation aligns with broader regulatory momentum. U.S. Environmental Protection Agency mandates for 2025–2026 targeting PFAS-free chemical formulations are accelerating the transition away from bituminous and chlorinated solvent-based OGLs toward synthetic, environmentally compliant alternatives.

Infrastructure renewal is reinforcing demand. Chevron Corporation expanded its premium lubricant portfolio in 2025 to address shock-load protection needs across aging power generation and mining assets. Field-level technology adoption is also reshaping lubricant usage patterns. Real-time condition monitoring systems deployed in large-scale excavation fleets, particularly in the Permian Basin, are enabling AI-driven predictive maintenance and more precise lubricant application, reducing waste and unplanned downtime. Market consolidation further strengthened competitive depth when Fuchs SE completed its acquisition of IRMCO in April 2025, broadening its high-performance industrial lubricant offerings for North American heavy machinery. Complementing private investment, Department of Energy Industrial Efficiency grants are incentivizing refiners and operators to adopt advanced lubricants that lower frictional energy losses in high-torque gear assemblies.

Germany – Circular Lubrication Models and Transparency-Led Performance

Germany’s open gear lubricants market is distinguished by circular economy leadership and formulation transparency. In March 2025, Klüber Lubrication became the sole specialty lubricant manufacturer participating in the GearOil LOOP initiative, a government-backed project targeting gear oils with at least 50% recycled base oil content. This initiative signals a structural shift toward closed-loop lubrication systems without compromising load-carrying capacity. Investment in innovation infrastructure remains robust. Fuchs SE committed €50 million to expand its Mannheim headquarters, increasing R&D and logistics capacity to support specialized industrial lubricant development.

Product innovation is increasingly aligned with sustainability mandates. At Lubricant Expo Europe 2025 in Düsseldorf, German manufacturers introduced PFAS-free and biodegradable open gear formulations designed for near-water mining and construction operations. Technological leadership is also evident in the development of translucent OGLs that allow visual gear inspection during operation, materially improving overall equipment efficiency by reducing inspection-related downtime. Concurrently, German producers are refining preservative systems to comply with European Biocidal Products Regulation updates effective August 2025, emphasizing non-toxic, water-resistant grease formulations.

Australia – Mining-Driven Demand and Automated Lubrication Systems

Australia’s open gear lubricants market is closely tied to large-scale mining and infrastructure investment. The 2025–26 federal budget allocation of $17.1 billion for road and rail projects is driving demand for heavy-duty OGLs used in tunnel-boring machines and earthmoving equipment. In parallel, mining operations in the Pilbara region are pushing the performance envelope. ExxonMobil, through Mobil Australia, introduced advanced synthetic lubricant ranges in 2024–2025 tailored for extreme shock loads encountered in iron ore extraction.

Environmental considerations are gaining traction. Following BP Australia’s 2024 rollout of biodegradable lubricant solutions, adoption of renewable-based open gear fluids increased notably across ESG-aligned mining projects. Automation is further reshaping consumption patterns. Widespread deployment of automated spray systems from providers such as Lincoln Industrial is optimizing lubricant delivery while reducing human exposure in hazardous zones. OEM collaboration remains a defining feature, with lubricant suppliers partnering with Caterpillar and Komatsu service centers in Western Australia to deliver factory-fill open gear greases for ultra-class draglines.

India – Industrial Scale-Up and Transition from Asphaltic Systems

India’s open gear lubricants industry is expanding rapidly alongside industrialization and regulatory reform. Under Mission Anveshan and the Oilfield Regulation and Development Amendment Act of 2025, policy incentives are encouraging adoption of sustainable industrial lubricants across mining and energy sectors. Capacity expansion is a cornerstone. The Lubrizol Corporation signed a 2025 memorandum to establish its largest global manufacturing facility in Aurangabad, focused on performance additives for South Asian markets.

Demand fundamentals are reinforced by cement sector dynamics. As India continues to operate among the world’s largest cement industries, the shift toward larger-capacity rotary kilns is driving higher usage of high-viscosity kiln and open gear lubricants. Sustainability policies under SATAT and broader green growth initiatives are accelerating replacement of asphaltic OGLs with synthetic alternatives offering cleaner handling and lower emissions. At the local level, domestic chemical manufacturers are innovating low-VOC open gear coatings to comply with tightening pollution norms in major industrial corridors such as the NCR and Mumbai.

Chile – Green Copper Standards and Water-Resistant Formulations

Chile’s open gear lubricants market is shaped by its leadership in copper mining and a strong emphasis on environmental stewardship. As the world’s largest copper producer, Chile’s 2025 Green Copper agenda is mandating biodegradable lubricants across large open-pit operations including Escondida and Chuquicamata. These requirements are elevating demand for high-load OGLs that meet both performance and environmental benchmarks.

Modernization investments are reinforcing this trend. Regional players, including Petrobras Chile, are expanding production of high-viscosity fluids to support digitally enabled mines where OGLs are integrated with IoT-based vibration and condition sensors. Regulatory reforms aimed at reducing permit approval timelines are unlocking new mining projects, broadening the demand pipeline for heavy-duty gear protection solutions. Water management investments add another layer of complexity. Desalination projects led by operators such as BHP are increasing the need for water-resistant and anti-corrosive greases capable of operating reliably in saline environments.

Strategic Country Comparison – Open Gear Lubricants

Open Gear Lubricants Market County Level Snapshot

|

Country

|

Primary Demand Driver

|

Technology Emphasis

|

Strategic Direction

|

|

United States

|

PFAS regulation and infrastructure aging

|

Synthetic OGLs, AI monitoring

|

Energy efficiency and compliance

|

|

Germany

|

Circular economy and regulation

|

Recycled base oils, translucent OGLs

|

Sustainability-led innovation

|

|

Australia

|

Mining and infrastructure expansion

|

Extreme-load synthetics, automation

|

Safety and ESG-aligned operations

|

|

India

|

Industrial growth and policy incentives

|

High-viscosity synthetics, low-VOC coatings

|

Scale-up and localization

|

|

Chile

|

Green mining and desalination

|

Biodegradable, water-resistant greases

|

Environment-driven performance

|

Open Gear Lubricants Market Report Scope

Open Gear Lubricants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$769.5 Million

|

|

Market Size (2034)

|

$1076.4 Million

|

|

Market Growth Rate

|

3.8%

|

|

Segments

|

By Product Type (Grease-Type Lubricants, Fluid-Type Lubricants, Compound-Type Lubricants, Aerosol and Spray-On Lubricants), By Base Oil (Mineral Oil, Synthetic Oil, Bio-Based Oil), By Application (Mining Equipment, Cement and Mills, Power Generation, Steel and Construction, Marine and Offshore)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Shell, ExxonMobil, Chevron, FUCHS, Klüber Lubrication, TotalEnergies, Lubrizol, BP, Afton Chemical, Whitmore Manufacturing, Petronas, Carl Bechem, Vanderbilt Chemicals, Bel-Ray, Schaeffer Manufacturing

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Open Gear Lubricants Market Segmentation

By Product Type

- Grease-Type Lubricants

- Fluid-Type Lubricants

- Compound-Type Lubricants

- Aerosol and Spray-On Lubricants

By Base Oil

- Mineral Oil

- Synthetic Oil

- Bio-Based Oil

By Application

- Mining Equipment

- Cement and Mills

- Power Generation

- Steel and Construction

- Marine and Offshore

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Open Gear Lubricants Industry

- Shell

- ExxonMobil

- Chevron

- FUCHS

- Klüber Lubrication

- TotalEnergies

- Lubrizol

- BP

- Afton Chemical

- Whitmore Manufacturing

- Petronas

- Carl Bechem

- Vanderbilt Chemicals

- Bel-Ray

- Schaeffer Manufacturing

*- List not Exhaustive