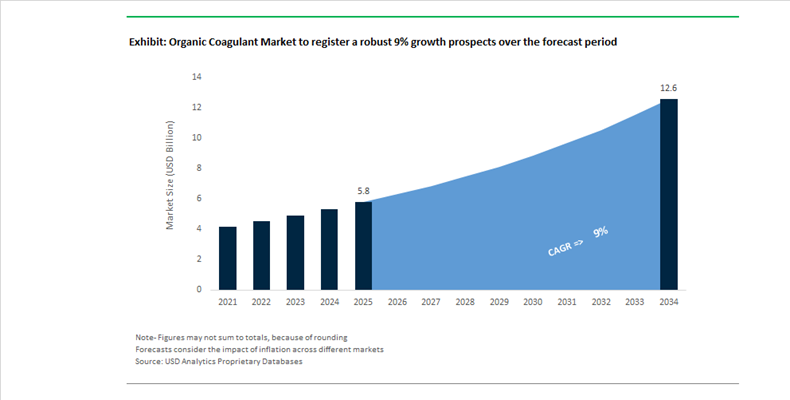

Organic Coagulant Market Valued at $5.8 Billion in 2025, Projected to Reach $12.6 Billion by 2034 at 9% CAGR Amid Water Reuse and ESG Compliance Pressures

The Organic Coagulant Market is valued at $5.8 billion in 2025 and is forecast to reach $12.6 billion by 2034, expanding at a CAGR of 9%. Growth is underpinned by rising regulatory enforcement on wastewater discharge, accelerating municipal water reuse programs, and industrial mandates to reduce sludge volumes and total treatment costs. Organic coagulants, including polyamines, PolyDADMAC, and cationic acrylamide-based polymers, are increasingly replacing traditional inorganic salts due to their superior charge neutralization efficiency, lower residual metal content, and reduced sludge generation. Market momentum is strongest in municipal wastewater treatment, pulp and paper processing, oilfield produced water management, and industrial effluent clarification.

Strategic portfolio realignments began in February 2024 when Kemira Oyj divested its Oil & Gas portfolio to Sterling Specialty Chemicals, sharpening its focus on water treatment chemistry. This repositioning was reinforced in February 2026 with Kemira’s acquisition of SIDRA Wasserchemie GmbH, expanding its coagulant production footprint in Western and Central Europe and strengthening its municipal water treatment dominance. In parallel, SNF Group achieved EcoVadis Platinum status in September 2024, positioning itself favorably in ESG-driven procurement frameworks. SNF further secured upstream integration by expanding ADAM monomer capacity by 80% at its Riceboro, Georgia site in late 2024, ensuring feedstock security for high-demand cationic organic coagulants in North America. In early 2026, SNF finalized its €135 million acquisition of Syensqo’s Oil & Gas division, integrating over 700 specialty products including advanced flocculants and coagulants used in drilling and produced water treatment.

Product innovation accelerated throughout 2024 and 2025. In 2024, Solenis LLC launched the ALAPURE™ bio-based coagulant family, derived from renewable plant materials to replace petroleum-based PolyDADMAC in environmentally sensitive applications. In September 2024, Tidal Clear received U.S. EPA Safer Choice certification for its TideForce coagulants, marking a decisive shift toward non-toxic formulations. Through 2025 and early 2026, BASF SE expanded the global rollout of its Zetag® ULTRA series, engineered for lower dosage efficiency and measurable sludge reduction in municipal wastewater plants. Mid-2025 research from Qatar University introduced choline chloride-based Natural Deep Eutectic Solvents as a new class of green organic coagulants, demonstrating scalable potential for industrial colloidal treatment.

Digitalization is reshaping chemical dosing economics. In late 2025, major players including Ecolab Inc. and Kemira deployed AI-enabled automated dosing platforms that adjust organic coagulant feed rates based on real-time turbidity and pH monitoring. Pilot programs report chemical consumption reductions of up to 20%, directly improving plant operating margins and ESG performance metrics. Meanwhile, Solenis completed the integration of NCH Corporation’s water treatment operations in 2025, enhancing localized service delivery and mid-market industrial penetration. These developments collectively signal a transition from volume-driven commodity sales toward performance-based, digitally optimized organic coagulant solutions aligned with circular water management frameworks.

Organic Coagulant Market Trends and Opportunities

Trend: Mandatory Transition to Organic Coagulants for Municipal Drinking Water Safety

Municipal drinking water systems are undergoing a structural shift as regulators and utilities respond to growing concerns over residual metals, particularly aluminum, in treated water. While traditional alum-based coagulants remain technically effective, their long-term implications for distribution system integrity, aesthetic water quality, and public health perception are increasingly scrutinized. As of December 2025, the U.S. EPA continues to reference a Secondary Maximum Contaminant Level for aluminum in the range of 0.05–0.2 mg/L, but operational reality is being shaped more strongly by international guidance. Health Canada and multiple European authorities have moved toward tighter operational thresholds near 0.1 mg/L, effectively forcing utilities to redesign coagulation strategies to consistently remain below this level under variable source-water conditions.

Organic coagulants, particularly polyDADMAC and advanced polyamines, are being adopted as primary coagulants or high-efficiency coagulant aids to stabilize compliance. Their precise charge density and controlled molecular weight distribution allow for effective destabilization of colloids without introducing additional metal ions into the water matrix. Beyond compliance, sludge volume reduction has emerged as a decisive economic driver. Municipal pilot programs conducted during 2024 demonstrated that replacing inorganic salts with high-purity organic polymers reduced sludge generation by 40%–70%, directly addressing rising disposal costs driven by landfill scarcity and stricter handling regulations across North America and Europe.

Concerns around polymer residuals are also being systematically addressed. Analytical innovations introduced in late 2023 and refined through 2024 now enable colorimetric detection of residual polyDADMAC down to 3.22 µg/L. This real-time monitoring capability has significantly reduced operator hesitation by enabling precise dose control, mitigating risks related to membrane fouling or downstream interactions, and reinforcing confidence in organic coagulants as a long-term solution for potable water treatment.

Trend: Strategic Scaling of Organic Coagulants for Circular Water Systems in Food and Beverage Operations

The food and beverage sector has become one of the fastest-growing end users of organic coagulants as water reuse shifts from a sustainability initiative to an operational necessity. Escalating freshwater costs, tightening discharge norms, and corporate water stewardship commitments are pushing manufacturers toward Zero Liquid Discharge and high-rate reuse architectures. Organic coagulants are structurally advantaged in these systems because they efficiently remove fats, oils, greases, and suspended organics without introducing inorganic ions that complicate reuse chemistry or membrane performance.

According to the U.S. EPA’s 2024 Water Reuse Action Plan, more than 40% of beverage facilities in the United States have already implemented some form of water recycling. In parallel, India’s 2024 liquid waste management regulations mandate an additional 20% wastewater reuse by 2027 for food and beverage plants, creating a non-discretionary demand spike for high-performance organic coagulants in pretreatment stages. Integrated Pretreatment Systems introduced in 2024 for high-organic-load effluents have demonstrated that organic clarification can improve overall recycling efficiency by up to 85%, enabling treated water to be redeployed for non-product-contact applications such as cleaning-in-place systems and cooling towers.

Cost efficiency further reinforces adoption. Industrial guidance issued in India during 2024 indicates that facilities deploying organic coagulant-based recovery systems can reduce total water expenditure by up to 35%. By removing more than 74% of total suspended solids and organics early in the treatment train, these polymers significantly reduce fouling and energy demand in downstream membrane and advanced oxidation systems, improving both operating margins and system reliability.

Opportunity: Commercialization of Chitosan-Based Coagulants for Eco-Certified Processes

Naturally derived organic coagulants are emerging as a high-growth opportunity as industries pursue clean-label and eco-certified processing frameworks. Chitosan, derived from crustacean shell waste, has gained prominence due to its biodegradability, non-toxicity, and strong affinity for heavy metals, dyes, and fine particulates. By late 2025, more than half of industrial wastewater treatment plants globally were either evaluating or actively adopting chitosan-based solutions, with North America leading early deployment in municipal and specialty industrial applications.

High-purity grades, particularly chitosan with a degree of deacetylation around 95%, are becoming the benchmark for drinking water and pharmaceutical-grade purification. This segment already accounts for roughly one-fifth of the bio-coagulant market, reflecting a willingness among operators to pay a premium for materials that deliver high removal efficiency without introducing synthetic residues. Strategic partnerships launched since 2022 have focused on scaling bio-derived coagulants for textiles and pulp and paper, sectors facing tightening restrictions under toxic-free manufacturing frameworks. As certification schemes such as EU Ecolabel and Nordic Swan gain traction, chitosan-based coagulants are positioned to move from niche adoption to mainstream specification in environmentally audited processes.

Opportunity: Performance-Driven Organic Coagulants for Offshore Oil and Gas Produced Water

Offshore oil and gas operations represent a specialized but highly attractive opportunity for organic coagulant suppliers. Produced water treatment on platforms and floating production systems demands chemicals that perform reliably under extreme salinity, variable oil loads, and severe space constraints. Inorganic coagulants struggle in these environments due to reduced effectiveness at high ionic strength and the logistical burden of bulk chemical storage.

Cationic organic polymers retain charge density and coagulation efficiency even in hypersaline produced water, enabling consistent removal of turbidity and total suspended solids in compact treatment units. Performance evaluations conducted in October 2025 confirmed that organic coagulants achieve stable clarification without the need for oversized dosing systems or secondary polishing. This capability is critical for meeting marine discharge limits, where Oil in Water concentrations must typically remain below 29 mg/L to comply with international and regional offshore regulations.

Sludge minimization further strengthens the value proposition. Offshore operators prioritize low-volume, high-density floc formation to reduce waste handling and transport back to shore. Organic coagulants generate drier, more compact sludge, lowering waste management costs by an estimated 20%–25% per cubic meter of treated water. For large FPSO installations processing millions of barrels annually, this translates into substantial lifecycle cost savings, positioning organic coagulants as a strategic enabler of compliant, cost-efficient offshore water management.

Organic Coagulant Market Share and Segmentation Insights

Synthetic Organic Coagulants Lead Market Adoption with High Charge Density and Reliable Water Treatment Performance

Synthetic organic coagulants accounted for 52.80% of the Organic Coagulant Market by source in 2025, establishing them as the dominant category used across municipal and industrial water treatment operations. Polyamines, polyDADMAC, and polyacrylamide-based coagulants are widely adopted due to their high charge density, predictable coagulation efficiency, and cost-effective performance in removing suspended solids, turbidity, and dissolved organic matter. These characteristics make synthetic organic coagulants essential in large-scale wastewater treatment and potable water purification infrastructure. A notable 2025 development is the green synthetic evolution, where manufacturers are introducing bio-based synthetic coagulants derived from renewable monomers and green chemistry processes to improve biodegradability and reduce toxicity while maintaining the performance standards required for regulated water treatment applications.

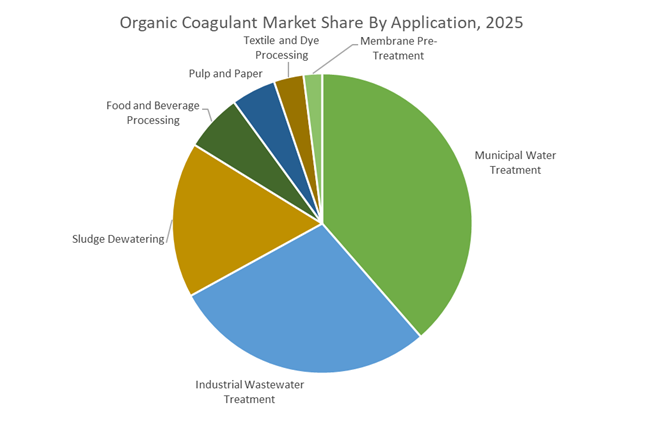

Municipal Water Treatment Drives Global Demand for Organic Coagulants in Drinking Water and Wastewater Systems

Municipal water treatment represented 38.60% of the Organic Coagulant Market by application in 2025, reflecting the extensive use of coagulation technologies in drinking water purification and municipal wastewater management systems worldwide. Organic coagulants play a critical role in removing suspended solids, colloidal particles, turbidity, and natural organic matter to meet stringent drinking water quality standards and environmental discharge regulations. The scale of urban water infrastructure and population-driven water demand continues to support significant chemical consumption in municipal treatment facilities. A major 2025 trend is the increasing focus on emerging contaminant removal, where treatment plants optimize coagulation processes to improve removal efficiency for PFAS, microplastics, and pharmaceutical residues using advanced organic coagulant formulations with tailored molecular structures and charge properties.

Organic Coagulant Market Competitive Landscape

The organic coagulant market in 2026 is driven by high-charge density polymers, sludge minimization, and digital dosage optimization. Competitive advantage lies in bio-based coagulants, IoT-enabled dosing systems, and integrated water treatment solutions that enhance turbidity removal efficiency while meeting stringent wastewater and potable water regulations.

SNF strengthens global dominance with vertically integrated polymer production and strategic acquisitions

SNF Group leads the organic coagulant market through its unmatched scale in water-soluble polymers and backward integration into key monomers, ensuring supply stability and cost control. The €135 million acquisition of Syensqo’s Oil & Gas division expands its footprint in high-pressure industrial water treatment and enhanced oil recovery. Additional acquisitions, including Obsidian Chemical Solutions and PfP Industries, strengthen its North American manufacturing base. Its EcoVadis Platinum rating supports positioning in decarbonized water chemistry and sustainable coagulation solutions. SNF’s innovation focus on NVF technology and collaboration with Mitsubishi Chemical enhances next-generation polymer performance. This integrated and sustainability-driven strategy reinforces its leadership in organic coagulants.

Kemira advances water treatment leadership through AI-driven innovation and service-based coagulation solutions

Kemira is positioning itself as a pure-play water solutions leader, focusing on high-performance organic coagulants following its strategic exit from oil and gas. The acquisition of Water Engineering, Inc. enables “Coagulation-as-a-Service” offerings for industrial clients, expanding its service-based revenue model. With a 19.1% EBITDA margin in 2025, Kemira demonstrates strong operational resilience while optimizing production efficiency at its Botlek facility. The acquisition of SIDRA Wasserchemie strengthens its European footprint. Its partnership with CuspAI accelerates development of advanced polymers for PFAS removal, a high-value application segment. This combination of digital innovation and strategic expansion positions Kemira strongly in next-generation water treatment chemistry.

Solenis scales global water treatment capabilities through NCH integration and digital chemical solutions

Solenis is expanding its leadership in organic coagulants following the acquisition of NCH Corporation, increasing its workforce to 23,000 employees across 160 countries. This integration enhances cross-selling opportunities and strengthens its presence in the middle-market industrial segment. With 78 manufacturing facilities, Solenis delivers large-scale, localized supply of high-performance coagulants. Its “360 approach” integrates chemical treatment with digital monitoring to optimize dosing and reduce operational costs. Recognition as a Best Managed Company Gold Standard highlights its execution capability in large-scale consolidation. This strategy positions Solenis as a global leader in sustainable and digitally enabled water treatment solutions.

Kurita drives digital water treatment innovation with advanced sensing technologies and global expansion

Kurita is strengthening its position through its PSV-27 strategy, aligning financial growth with environmental impact in water treatment. Expansion into Mexico enhances its presence in North American industrial corridors, particularly automotive and electronics manufacturing. Its S.sensing™ CS technology enables real-time optimization of coagulant dosing, improving efficiency and reducing chemical waste. Strong performance in its Water Treatment Chemicals segment reflects rising demand for high-purity and ultrapure water solutions. Investment in its Tokyo R&D hub supports innovation in advanced organic polymers for semiconductor applications. This focus on digitalization and sustainability positions Kurita as a key innovator in organic coagulants.

Ecolab enhances high-efficiency coagulation through AI-driven platforms and integrated water management solutions

Ecolab, through Nalco Water, leads the organic coagulant market with its eROI-driven approach, demonstrating measurable financial and environmental benefits. Its Water Track IQ™ platform provides real-time monitoring and optimization of coagulant performance, supporting industrial and municipal applications. The acquisition of Ovivo’s ultrapure water business strengthens its capabilities in high-tech sectors such as microelectronics. Its 2025 impact report highlights large-scale water savings, reinforcing its value proposition in resource efficiency. Building on its ULTIMER® polymer technology, Ecolab is advancing natural coagulant concentrates to reduce logistics-related emissions. This integration of digital intelligence and green chemistry solidifies its competitive edge.

United States – PFAS Regulation and Infrastructure-Led Demand Realignment

The United States organic coagulant industry is being structurally reshaped by drinking water regulation tightening and federally backed infrastructure investment. During 2024–2025, the U.S. Environmental Protection Agency finalized stringent National Primary Drinking Water Regulations for PFAS, forcing utilities to deploy advanced pre-treatment solutions to safeguard downstream membrane and adsorption systems. Organic coagulants, particularly high-charge-density polyamines and PolyDADMAC variants, are increasingly specified at the front end of treatment trains to reduce fouling risks and improve lifecycle performance of advanced filtration assets. This regulatory push coincides with large-scale capital deployment under the Bipartisan Infrastructure Law, with more than USD 50 billion allocated through 2026 for clean water and emerging contaminant removal projects, materially expanding addressable demand for organic polymer coagulants across municipal and industrial segments.

Supply chain strategy is evolving in parallel. Following 2025 tariff schedule adjustments, producers such as Solenis and Ecolab have accelerated vertical integration into botanical raw materials, including domestic cultivation of Moringa oleifera, to mitigate import volatility. Capacity resilience has been reinforced by facility upgrades announced by Buckman and USALCO along the Gulf Coast to expand domestic production of organic cationic polymers. At the innovation layer, U.S.-based biotech firms are advancing enzymatically modified tannin and lignin coagulants that deliver materially higher turbidity removal efficiency in cold-water conditions. State-level zero-waste sludge targets, particularly in California and New York, are further accelerating substitution away from alum toward biodegradable organic coagulants that significantly reduce non-recoverable sludge volumes.

India – Agro-Based Feedstocks and ZLD-Driven Industrial Uptake

India’s organic coagulant industry is entering a formalized growth phase under regulatory recognition and industrial effluent mandates. A 2025 amendment to the Fertilizer Control Order issued by the Ministry of Agriculture and Farmers Welfare formally recognized biostimulants and bio-coagulants, legitimizing large-scale industrial deployment of agro-waste-derived treatment agents. This regulatory clarity has unlocked demand across water-intensive sectors, particularly textiles, pulp and paper, and food processing. Under the Mission Anveshan framework, government-backed R&D grants in 2025 accelerated development of chitosan-based organic coagulants sourced from seafood processing waste, targeting heavy metal removal in high-load textile clusters such as Tirupur.

Manufacturing scale-up is reinforcing domestic supply depth. Aditya Birla Chemicals commissioned new capacity within its performance chemicals division in Q3 2025 to address rising demand for organic coagulants across South Asia. On the regulatory front, the Central Pollution Control Board’s enforcement of Zero Liquid Discharge norms for the pharmaceutical sector during 2025–2026 is driving rapid adoption of quaternary ammonium-based organic coagulants capable of handling complex, high-COD effluent streams. India’s strategic advantage lies in feedstock security. Government subsidies under the National Mission on Edible Oils have positioned the country as the global leader in commercial Moringa plantations for industrial coagulant production, anchoring long-term cost competitiveness.

Germany – Traceable Biomass and Circular Polymer Innovation

Germany’s organic coagulant market is being shaped by traceability mandates, circular economy innovation, and tightening VOC regulations. In preparation for 2026 enforcement of the EU Deforestation Regulation, German manufacturers including BASF SE have revised procurement frameworks to ensure all plant-based coagulants are sourced from verifiably non-deforested supply chains. This shift is elevating demand for certified tannins, starches, and bio-polymers with full upstream transparency. Circularity initiatives are also influencing product development. Outputs from the government-funded GearOil LOOP project have enabled the adaptation of recycled-polymer binders into high-efficiency organic coagulants for industrial oil-water separation, particularly in metalworking and automotive effluent treatment.

Environmental compliance is accelerating formulation change. Following tighter VOC emission thresholds introduced by the Federal Environment Agency in 2025, chemical parks across Germany are transitioning toward waterborne acrylic-based organic coagulants to treat paint shop and surface finishing wastewater. Energy transition is another differentiator. Kemira, with substantial German operations, transitioned a significant share of its regional coagulant output to renewable energy by late 2025, supporting its roadmap toward net-zero water treatment products. At the research level, German innovation clusters have achieved stabilization of black wattle tannin extracts for high-pH industrial environments, unlocking new applications in domestic tanning and textile wastewater systems.

China – Digital Dosing and Consolidation-Driven Quality Control

China’s organic coagulant industry is advancing through policy-backed localization, digitalization, and structural consolidation. The Ministry of Industry and Information Technology’s 2025–2026 petrochemical growth plan prioritizes domestic production of high-end water treatment polymers to close self-sufficiency gaps in specialty organic chemicals. This policy emphasis is translating into expanded capacity for cationic and amphoteric organic coagulants designed for municipal and industrial reuse systems. Operational efficiency is being enhanced through large-scale deployment of AI-driven dosing platforms across the Yangtze River delta, where real-time turbidity control using organic coagulants has reduced chemical overuse by an estimated 15%.

Industry structure is tightening. A 2026 mandate requiring consolidation of small and mid-sized chemical plants is favoring larger, standardized producers such as Shandong Shuiheng Chemical, improving export consistency and quality assurance for organic polymer coagulants. Regulatory pull from maritime applications is also emerging. Under the Green Shipping Corridor initiative launched in late 2024, all new-build vessels operating in designated corridors must utilize biodegradable organic coagulants in ballast water treatment systems by 2026, creating a specialized demand stream aligned with international environmental standards.

Brazil – Agro-Waste Extraction and Mining Safety Applications

Brazil’s organic coagulant industry is leveraging agricultural abundance and regulatory pressure in mining to expand high-value applications. In 2025, companies such as Grupo Bauminas announced significant investments in extracting organic coagulants from sugarcane bagasse and citrus processing residues, converting agricultural surplus into industrial water treatment inputs. This agro-waste valorization model aligns with export demand for renewable coagulants while strengthening domestic supply resilience.

Mining regulation is a parallel demand driver. Following updated tailings dam safety requirements in 2025, Brazilian mining operators have accelerated adoption of high-viscosity organic polymer coagulants to improve iron ore tailings dewatering and reduce structural risk. Policy incentives are reinforcing this shift. The National Water and Sanitation Agency introduced tax credits for industrial facilities achieving high water reuse rates using bio-based treatment agents, directly supporting uptake of organic coagulants in water-stressed regions and heavy industry clusters.

Strategic Country Comparison – Organic Coagulants

Organic Coagulant Market County Level Snapshot

|

Country

|

Primary Demand Driver

|

Feedstock or Technology Focus

|

Strategic Position

|

|

United States

|

PFAS regulation and infrastructure funding

|

Polyamines, enzymatic bio-coagulants

|

High-value municipal and industrial market

|

|

India

|

ZLD mandates and agro-feedstocks

|

Chitosan, moringa-based coagulants

|

Fastest scaling bio-based supply base

|

|

Germany

|

Traceability and VOC compliance

|

Certified tannins, circular polymers

|

Premium compliance-driven innovation

|

|

China

|

Digital water management and consolidation

|

AI-dosed organic polymers

|

Volume and quality standardization leader

|

|

Brazil

|

Agro-waste valorization and mining safety

|

Bagasse- and citrus-derived polymers

|

Resource-backed niche growth market

|

Organic Coagulant Market Report Scope

Organic Coagulant Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.8 Billion

|

|

Market Size (2034)

|

$12.6 Billion

|

|

Market Growth Rate

|

9%

|

|

Segments

|

By Source (Plant-Based, Animal-Based, Microbial-Based, Synthetic Organic), By Physical Form (Liquid, Powder), By Application (Municipal Water Treatment, Industrial Wastewater Treatment, Food and Beverage Processing, Pulp and Paper, Textile and Dye Processing, Sludge Dewatering, Membrane Pre-Treatment)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

SNF Group, Kemira, Ecolab, Solenis, BASF, Veolia, Kurita Water Industries, Baker Hughes, USALCO, Buckman, Aditya Birla Chemicals, Feralco Group, Shandong Shuiheng Chemical, IXOM, Aries Chemical

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Organic Coagulant Market Segmentation

By Source

- Plant-Based

- Animal-Based

- Microbial-Based

- Synthetic Organic

By Physical Form

By Application

- Municipal Water Treatment

- Industrial Wastewater Treatment

- Food and Beverage Processing

- Pulp and Paper

- Textile and Dye Processing

- Sludge Dewatering

- Membrane Pre-Treatment

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Organic Coagulant Industry

- SNF Group

- Kemira

- Ecolab

- Solenis

- BASF

- Veolia

- Kurita Water Industries

- Baker Hughes

- USALCO

- Buckman

- Aditya Birla Chemicals

- Feralco Group

- Shandong Shuiheng Chemical

- IXOM

- Aries Chemical

*- List not Exhaustive