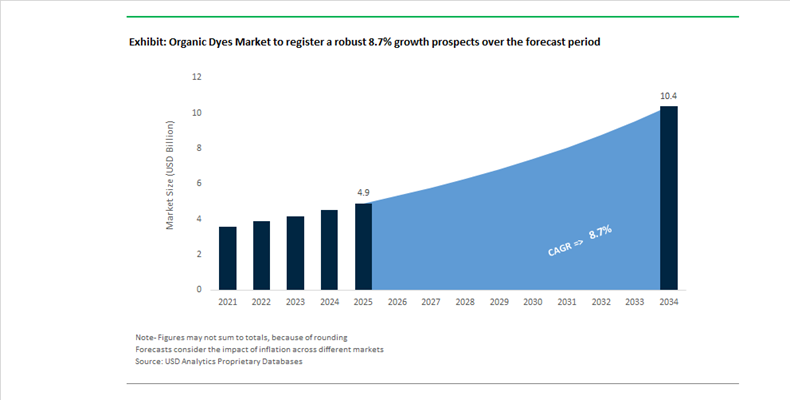

Organic Dyes Market Valued at $4.9 Billion in 2025 Projected to Reach $10.4 Billion by 2034 at 8.7% CAGR Driven by Sustainable Textile and High-Performance Colorant Innovation

The Organic Dyes Market is valued at $4.9 billion in 2025 and is projected to reach $10.4 billion by 2034, expanding at a robust CAGR of 8.7%. Growth is being fueled by accelerating demand for sustainable textile coloration, regulatory pressure on hazardous azo intermediates, and increased adoption of bio-based and low-impact dye chemistries across apparel, paper, coatings, and specialty applications. Textile processing remains the dominant end-use segment, particularly reactive dyes for cotton, disperse dyes for polyester, and sulfur and vat dyes for denim. The shift toward fiber-efficient dyeing systems, low-salt reactive technologies, and reduced-water processing is redefining procurement strategies among global apparel brands. Simultaneously, digital printing, specialty inks, and high-fastness organic dispersions are expanding the application scope of high-purity organic dyes beyond traditional bulk textile markets.

Industry consolidation intensified through 2025. In March 2025, Sudarshan Chemical Industries Ltd. completed the acquisition of the Heubach Group’s global pigment and colorant business, creating the world’s second-largest pigment player. While pigment-focused, the transaction significantly strengthens Sudarshan’s portfolio in high-performance organic colorants and dispersions across Europe and the Americas. In December 2025, Kiri Industries Ltd. finalized the sale of its 37.57% stake in DyStar Global Holdings to Zhejiang Longsheng Group for $689.83 million, ending a decade-long legal dispute. The payment, received on December 30, 2025, consolidated DyStar ownership under Zhejiang Longsheng and positioned Kiri as debt-free entering 2026. In January 2026, Kiri further secured approval under India’s Production Linked Incentive scheme to expand manufacturing of dye intermediates and specialty organic colorants, strengthening domestic backward integration.

Sustainability-driven innovation accelerated from 2024 onward. In May 2024, AMA Herbal launched Bio Indigo PreR, a liquid, pre-reduced natural indigo offering lower energy consumption and reduced CO₂ emissions compared to conventional synthetic indigo dyeing. In early 2024, Archroma Management GmbH entered an exclusive partnership with Innovo Fiber LLC to combine its AVITERA® SE reactive dyes with Fibre52® low-temperature bleaching technology, enabling cotton mills to reduce water and energy use by up to 50%. In September 2024, DIC Corporation obtained ISCC PLUS certification, allowing mass-balance integration of bio-based and circular feedstocks into its organic dye portfolio. Archroma strengthened its R&D base in October 2025 by inaugurating its expanded Global Innovation Center in Mumbai, dedicated to sustainable dye chemistries and fiber-to-finish process optimization. The same month, Archroma received the ITMF 2025 Sustainability & Innovation Award for its DENIM HALO technology, which enables distressed denim effects without traditional harsh chemicals.

Corporate restructuring and operational optimization are reshaping cost structures. Throughout 2025, Huntsman Corporation advanced a global restructuring program targeting $100 million in annual savings by 2026, rationalizing specialty chemical and organic dye production in response to volatile European energy costs. In November 2024, Heubach Colorants India appointed new leadership to implement its “Efficiency 2026” strategy, focusing on localized high-value organic dispersions to improve EBITDA margins. In January 2026, DIC Corporation transitioned to a Global Operating Model aligned with its Vision 2030 strategy, accelerating commercialization of sustainable organic colorants under a more integrated global structure. These developments reflect a market transitioning from commodity reactive dyes toward performance-engineered, certified-sustainable organic color solutions optimized for global ESG compliance and supply chain resilience.

Organic Dyes Market Trends and Opportunities

Trend: Regulatory Phase-Out of Heavy-Metal and Restricted Azo Dyes

The organic dyes market is undergoing a structural realignment as regulators in Europe and Asia aggressively eliminate legacy dye chemistries linked to carcinogenic aromatic amines and heavy-metal contamination. Compliance is no longer limited to factory audits but is now embedded directly into market access mechanisms. In June 2025, the European Union enacted Commission Regulation (EU) 2025/1090 under REACH Annex XVII, extending restrictions on hazardous dye intermediates and reinforcing the earlier 2024 ban on PFHxA in textiles. These measures are tightly coupled with the 2025 Digital Product Passport requirements, under which non-compliant garments can be blocked at the border regardless of downstream brand ownership. As a result, textile and apparel brands are mandating ZDHC MRSL Level 3 compliant organic dyes across their Tier 1 and Tier 2 supply chains.

India has emerged as a parallel regulatory catalyst. By late 2024, the Indian government enforced a prohibition on 112 azo and benzidine-based dyes, introducing mandatory Pre-Shipment Certification for all imported textiles. With a 25% compulsory sampling rate for suspect consignments, exporters face tangible financial and logistical risk if dye formulations are not fully heavy-metal-free. This has accelerated global adoption of certified organic dyes with zero-detection thresholds for regulated amines. Beyond compliance, traceability has become a commercial differentiator. The 2025 rollout of the EU Ecodesign for Sustainable Products Regulation has elevated digitally stored dye-recipe libraries into strategic assets. Technology providers are enabling batch-level traceability of organic dyes, allowing brands to demonstrate chemical provenance and eliminate legacy azo risk across complex, multi-country production networks.

Trend: Scalability of High-Purity Organic Dyes for On-Demand Digital Printing

The migration from analog screen printing to digital textile printing is reshaping demand patterns within the organic dyes market. While traditional screen printing continues to expand at low single-digit rates, digital textile printing is growing at over 16% annually as of 2025, driven by fast-fashion compression cycles and AI-enabled, on-demand manufacturing models. This shift places stringent technical requirements on organic dyes, particularly for reactive and acid dye chemistries used in inkjet systems. Printhead tolerances demand ultra-filtered dyes with near-zero particulate content, pushing suppliers toward advanced purification, membrane filtration, and controlled synthesis.

Innovation in waterless and near-waterless dyeing technologies is reinforcing this trend. In 2024, dry dye platforms based on organic reactive pigments demonstrated commercial viability by eliminating steaming and washing stages entirely. These systems deliver inherent compliance with REACH and RoHS while reducing process water consumption by almost 100%, a decisive advantage as textile clusters face tightening water withdrawal limits. Parallel developments in high-gamut organic inks are expanding application scope. High-purity reactive and pigment-based inks launched in late 2024 were engineered to deliver superior color saturation, wash fastness, and adhesion for Direct-to-Film and hybrid printing workflows. As digital textile ink becomes a performance-driven rather than commodity segment, demand is consolidating around organic dyes that can guarantee consistency, equipment safety, and color precision at industrial scale.

Opportunity: Organic Fluorophores for Security and Anti-Counterfeiting Applications

The rapid expansion of counterfeit goods in cosmetics, pharmaceuticals, and luxury products has created a high-margin opportunity for advanced organic dyes with latent and programmable optical properties. Unlike conventional visible dyes, next-generation organic fluorophores remain invisible under ambient conditions and reveal a unique optical signature only under controlled excitation. Research published in late 2025 demonstrated that carbon-dot-based organic inks can be encoded using fluorescence lifetime rather than color alone, enabling authentication through time-resolved imaging that is extremely difficult to replicate using standard pigments.

Photochromic organic dyes are gaining particular traction. Spiropyran-based systems, capable of reversible color and fluorescence switching under ultraviolet exposure, are being adopted for tamper-evident and encrypted packaging. Their low toxicity profile and stability under cosmetic and pharmaceutical storage conditions make them well suited for regulated consumer markets. More advanced multicolor security concepts are also emerging. New organic dye families capable of producing precisely quantifiable red, green, and blue emissions through controlled photochemical reactions provide a direct bridge between physical packaging and digital authentication platforms. As brands seek scalable, non-invasive anti-counterfeiting solutions, organic fluorophores are transitioning from laboratory novelty to strategic packaging components.

Opportunity: Organic Sensitizer Dyes for Flexible and Low-Light Photovoltaics

Organic dyes are increasingly positioned as functional energy materials rather than purely aesthetic additives. Dye-sensitized solar cells rely on tailored organic sensitizers to harvest light and convert it into electrical energy, making dye chemistry central to performance. In September 2025, research teams reported record-breaking photovoltage levels exceeding 1.2 volts using newly designed organic sensitizers paired with copper-based electrolytes. These results significantly narrow the efficiency gap between dye-sensitized systems and conventional photovoltaic technologies in specific use cases.

Machine learning has emerged as a decisive accelerator in this space. By late 2025, integrated ML and density functional theory pipelines were being used to predict light-harvesting efficiency and charge transfer behavior of thousands of candidate organic dyes, dramatically reducing development timelines. This computational approach is enabling rapid identification of molecules optimized for low-light environments, where traditional silicon photovoltaics underperform. As demand grows for self-powered indoor sensors, wearables, and building-integrated photovoltaics, organic sensitizer dyes offer tunable absorption profiles that align precisely with ambient light spectra. This positions the organic dyes market at the intersection of advanced materials science, renewable energy, and distributed power generation.

Organic Dyes Market Share and Segmentation Insights

Reactive Dyes Lead Organic Dye Consumption in Cellulosic Fiber Processing and Textile Coloration

Reactive dyes accounted for 32.80% of the Organic Dyes Market by type in 2025, making them the leading dye category used in large-scale textile coloration. Their dominance is linked to strong compatibility with cellulosic fibers such as cotton, viscose, and linen, which represent a major share of global textile fiber consumption. Reactive dyes chemically bond with fibers through covalent attachment, enabling superior wash fastness, color vibrancy, and durability required in apparel and home textile manufacturing. In 2025, the industry is advancing sustainable reactive dye technologies, including high-fixation reactive dyes that reduce salt and water usage during dyeing processes and cold-brand reactive dyes that lower energy consumption while maintaining consistent shade development and dyeing efficiency.

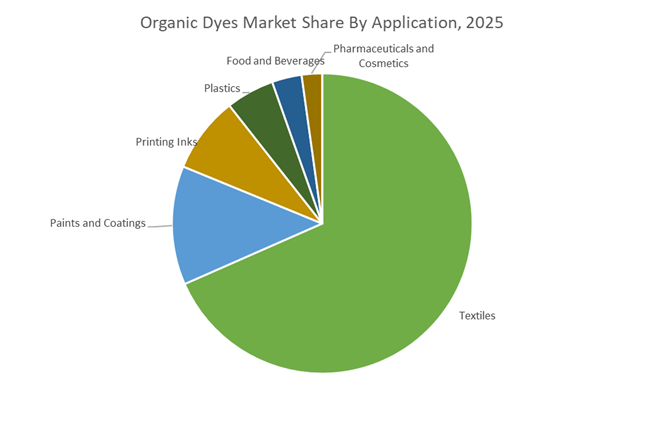

Textile Industry Dominates Organic Dye Demand Driven by Global Apparel and Fabric Production

The textile sector represented 68.40% of the Organic Dyes Market by application in 2025, accounting for the majority of dye consumption worldwide. Dyeing processes for fibers, yarns, and fabrics remain essential across apparel manufacturing, home textiles, and technical textile production, with fashion cycles and seasonal color trends driving continuous demand for diverse dye formulations. Large-scale textile production hubs in Asia continue to sustain high consumption of reactive, disperse, and acid dyes used in different fiber systems. A key 2025 development is the growing adoption of waterless dyeing technologies, including supercritical CO₂ dyeing, foam-based dyeing, and digital textile printing, which improve dye transfer efficiency while encouraging the development of specialized dye formulations compatible with low-water textile processing methods.

Organic Dyes Market Competitive Landscape

The organic dyes market in 2026 is driven by aniline-free chemistries, water-efficient dyeing systems, and circular pigment innovation. Competitive differentiation centers on bio-based dyes, digital color twin platforms, and low-salt, decarbonized indigo solutions aligned with ESG mandates and stringent wastewater discharge regulations.

Archroma leads circular dye innovation with aniline-free indigo and bio-waste derived color technologies

Archroma is strengthening its leadership in sustainable organic dyes following the integration of Huntsman’s Textile Effects business, creating a global specialty chemicals powerhouse. Its DENISOL® PURE INDIGO platform enables aniline-free, pre-reduced indigo with lower pollution risk and improved process efficiency for denim applications. The EarthColors® technology leverages agricultural waste to produce high-performance dyes, supporting circular economy objectives. The launch of DIRESUL® EVOLUTION BLACK delivers a 57% reduction in synthesis resource impact, enhancing ESG compliance. With operations across 42 countries and 35 production sites, Archroma maintains strong global reach. This innovation-driven portfolio positions the company at the forefront of decarbonized textile coloration.

DyStar strengthens global dye leadership through ownership consolidation and sustainability compliance expansion

DyStar is reinforcing its position in high-performance organic dyes following its transition to full ownership under Zhejiang Longsheng Group in January 2026. The governance reset and board restructuring support long-term international expansion and operational resilience. ISO 14001 certification at its Indonesia facility highlights its commitment to environmental compliance amid tightening wastewater regulations. The company remains a key supplier of reactive and disperse dyes with high color fastness, serving automotive textiles and outdoor apparel markets. Its technical expertise supports advanced dyeing processes with improved efficiency and durability. This combination of scale and compliance strengthens DyStar’s competitive positioning in global dye markets.

Kiri Industries accelerates capacity expansion with strong capital base and focus on specialty dye intermediates

Kiri Industries is entering a growth phase following the $689 million stake sale in DyStar, significantly strengthening its balance sheet and funding expansion initiatives. The company is prioritizing high-margin specialty reactive dyes and organic intermediates to enhance profitability and reduce exposure to commoditized segments. Backward integration into key raw materials such as sulfuric acid improves cost efficiency and supply stability. Expansion of manufacturing facilities in India targets rising demand from Southeast Asia and Turkey. Despite global supply chain volatility, Kiri maintains stable production through integrated operations. This capital-backed expansion strategy positions Kiri as a competitive regional supplier of specialty organic dyes.

LANXESS advances low-carbon coloration with Scopeblue-certified dyes and high-performance aqueous dispersions

LANXESS is focusing on sustainable organic dyes through its Scopeblue label, offering products with at least 50% lower carbon footprint or sustainable raw material content. Its Levanyl® aqueous pigment preparations deliver superior lightfastness and weather resistance for architectural coatings and industrial applications. Improvements in its Mesamoll® plasticizer line support lower-carbon textile printing systems. The company’s expertise in functional coloration ensures compliance with stringent environmental and fire safety regulations. LANXESS continues to strengthen its position in paints, plastics, and coatings markets through high-stability organic colorants. This sustainability-led strategy enhances its competitiveness in advanced coloration technologies.

BASF integrates digital carbon tracking and advanced materials to enhance high-performance organic dye applications

BASF is leveraging its materials science capabilities to integrate organic dyes into high-performance coatings and polymer systems. Its digital PCF calculation tool enables customers to track carbon emissions across the value chain, supporting Scope 3 reporting requirements. The company’s focus on nature-inspired color trends aligns with evolving automotive and consumer preferences. Expansion of Ultrason® PPSU grades with compliant organic colorants addresses high-temperature and food-contact applications. Local production expansion in India strengthens supply for architectural coatings and construction sectors. This combination of digital tools, regulatory compliance, and material innovation positions BASF as a key player in advanced organic dye systems.

China – Regulatory Redirection Toward Natural Colorants and High-End Purity

China’s organic dyes industry is undergoing a decisive regulatory and structural pivot, combining macro-level growth mandates with targeted application bans and technology upgrades. In September 2025, the Ministry of Industry and Information Technology released a multi-agency plan targeting sustained expansion in petrochemicals and chemicals through 2026, with organic dyes positioned within higher value specialty segments rather than bulk commodity output. A major inflection point emerged on May 1, 2025, when new food industry regulations mandated that all food colorings be derived exclusively from natural sources using physical extraction methods. This effectively eliminated synthetic organic dyes from food applications, accelerating domestic demand for plant-based and algae-derived natural colorants while compressing legacy synthetic dye volumes.

At the same time, China is strengthening its position in advanced organic pigments. The 2025–2026 industrial roadmap prioritizes electronic chemicals and high-purity organic pigments for semiconductors and display panels, where impurity control and chromatic stability are critical. Industry structure is consolidating rapidly. Zhejiang Longsheng Group completed its transition to full ownership of DyStar in June 2025, centralizing one of the world’s largest textile dye portfolios under Chinese control. Parallel investments are reinforcing localization. Kiri Industries established a new subsidiary in China in August 2025 to support regional production of dye intermediates. Environmental enforcement is intensifying ahead of 2026, with chemical parks required to deliver measurable carbon reductions, forcing older sulfate-based dye plants to transition toward lower-waste chloride and closed-loop technologies.

India – Domestic Recovery Amid Export Pressure and Global Integration

India’s organic dyes industry is navigating near-term export headwinds while strengthening its global competitive position through consolidation and innovation. According to CareEdge Ratings, the dyes and pigments sector is expected to contract modestly in FY26, largely due to a decline in export volumes linked to intensified global competition and new U.S. tariffs. Despite this, domestic fundamentals remain resilient. Leading Indian producers maintained healthy solvency positions through late 2025, supported by steady local demand and easing raw material costs for key dye intermediates.

Strategic investment and M&A activity are reshaping India’s global footprint. In 2025, Sudarshan Chemical Industries completed the acquisition of Heubach Group, creating a globally diversified organic pigment platform spanning 19 production sites. Innovation infrastructure is also expanding. Archroma opened a Global Center of Innovation in Mumbai in September 2025, focused on sustainable organic colorants for flexible packaging and wood applications. Financial indicators point to selective recovery. Kiri Industries reported strong year-on-year revenue growth in Q2 FY26, signaling renewed momentum in domestic dye intermediates. Government-backed Science and Technology Clusters are being scaled from eight to twenty-five sites by 2028, anchoring localized R&D for high-performance organic colorants.

United States – High-Purity Applications and Trade-Driven Realignment

The United States organic dyes market is increasingly oriented toward advanced materials, packaging, and automotive design, while trade policy reshapes sourcing patterns. R&D investment remains a defining feature. In late 2025, Archroma opened a Global Center of Innovation in Charlotte, North Carolina, dedicated to fiber coloration, board packaging, and next-generation biomaterials. Manufacturing footprints are being optimized for efficiency. DyStar consolidated its Charlotte operations into its Reidsville, North Carolina site in early 2025, improving production economics for the Americas.

Advanced purification is another strategic focus. Huntsman Corporation expanded purification and packaging capabilities at its E-GRADE® facility in Texas to supply ultra-high-purity organic chemicals for electronics and semiconductor uses. In automotive coatings, color innovation continues to drive differentiation. BASF Coatings introduced Auxetic Neutral as a flagship color for 2025–2026, reflecting a shift toward tactile, multidimensional organic dye and pigment hybrids. Meanwhile, new U.S. tariffs on dyes and pigments implemented in the second half of FY26 are forcing a realignment of trade flows, particularly reducing reliance on Asia-Pacific imports and favoring localized or near-shore supply chains.

Germany and EMEA – Portfolio Refocus and Regulatory Tightening

Germany remains a strategic anchor for organic dyes within the EMEA region, balancing portfolio restructuring with high-end innovation. In late 2025, BASF SE agreed to divest a majority stake in its coatings business to Carlyle Group, reallocating capital toward core organic chemical and dye clusters. Capacity investment continues selectively. LANXESS announced expansion plans for non-toxic organic pigment production in response to rising European demand from plastics and coatings manufacturers.

Automotive aesthetics remain a key downstream driver. BASF Coatings debuted Tesseract Blue in late 2025, a vivid multidimensional color engineered with advanced interference pigments for premium automotive finishes. Regulatory pressure is intensifying. The European Union proposed bans on several persistent organic pollutants in December 2025, with adoption expected in 2026, directly impacting certain chlorinated dye formulations and accelerating reformulation toward safer chemistries. Collaboration is expanding service-based differentiation. Archroma partnered with Lilienweiss to provide localized, sustainability-focused color management services across Europe from 2026 onward.

Spain – Packaging and Label Colorant Innovation Hub

Spain is emerging as a focused innovation center within Europe’s organic dyes landscape, particularly for packaging and labeling applications. In September 2025, Archroma opened its second European Global Center of Innovation in Prat, Spain, dedicated to organic colorants for tapes, labels, and specialty packaging substrates. This facility strengthens Southern Europe’s role in application-driven dye development, particularly for fast-moving consumer goods and logistics packaging.

Sustainability credentials are reinforcing Spain’s strategic relevance. Spanish and broader European manufacturing sites contributed to Archroma achieving Cradle to Cradle Certified® Material Health Gold status for multiple product groups in late 2025. This achievement reflects rising demand from brand owners for traceable, non-toxic organic dyes that meet stringent material health and recyclability standards, positioning Spain as a key node in Europe’s sustainable colorant value chain.

Comparative Country Snapshot – Organic Dyes Industry

Organic Dyes Market County Level Snapshot

|

Country / Region

|

Primary Regulatory or Market Driver

|

Strategic Focus Area

|

Competitive Position

|

|

China

|

Natural color mandates and consolidation

|

Food-safe dyes, electronic-grade pigments

|

Volume leader moving into high purity

|

|

India

|

Export pressure and M&A-led scale

|

Pigments, intermediates, packaging

|

Globally integrated growth platform

|

|

United States

|

Advanced applications and tariffs

|

Electronics, automotive, packaging

|

High-purity and innovation-driven

|

|

Germany / EMEA

|

Regulatory bans and portfolio refocus

|

Non-toxic pigments, automotive colors

|

Compliance-led premium supplier

|

|

Spain

|

Packaging innovation and sustainability

|

Labels, tapes, FMCG packaging

|

Niche innovation hub

|

Organic Dyes Market Report Scope

Organic Dyes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.9 Billion

|

|

Market Size (2034)

|

$10.4 Billion

|

|

Market Growth Rate

|

8.7%

|

|

Segments

|

By Type (Reactive Dyes, Disperse Dyes, Acid Dyes, Direct Dyes, Vat and Sulfur Dyes, Basic Dyes), By Source (Synthetic Organic Dyes, Natural Organic Dyes, Bio-Based Dyes), By Application (Textiles, Paints and Coatings, Printing Inks, Plastics, Food and Beverages, Pharmaceuticals and Cosmetics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Archroma, Huntsman, Zhejiang Longsheng Group, BASF, Sudarshan Chemical Industries, Kiri Industries, Everlight Chemical, Jay Chemical Industries, Meghmani Organics, DIC, Kyung-In Synthetic, Heubach Group, Atul, Colourtex Industries, Yorkshire Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Organic Dyes Market Segmentation

By Type

- Reactive Dyes

- Disperse Dyes

- Acid Dyes

- Direct Dyes

- Vat and Sulfur Dyes

- Basic Dyes

By Source

- Synthetic Organic Dyes

- Natural Organic Dyes

- Bio-Based Dyes

By Application

- Textiles

- Paints and Coatings

- Printing Inks

- Plastics

- Food and Beverages

- Pharmaceuticals and Cosmetics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Organic Dyes Industry

- Archroma

- Huntsman

- Zhejiang Longsheng Group

- BASF

- Sudarshan Chemical Industries

- Kiri Industries

- Everlight Chemical

- Jay Chemical Industries

- Meghmani Organics

- DIC

- Kyung-In Synthetic

- Heubach Group

- Atul

- Colourtex Industries

- Yorkshire Group

*- List not Exhaustive