Organometallics Market Growth Fueled by Semiconductor Integration, Catalytic Efficiency, and High-Purity Pharmaceutical Demand (2025–2034)

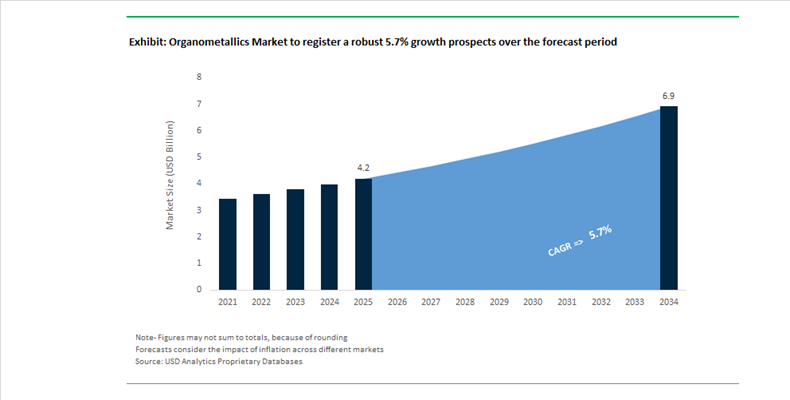

The Organometallics Market is projected to grow from USD 4.2 billion in 2025 to USD 6.9 billion by 2034, registering a CAGR of 5.7%, driven by expanding applications in semiconductors, pharmaceutical synthesis, and advanced catalysis. The sector is increasingly defined by the shift toward high-purity organometallic precursors for next-generation electronics and green catalytic cycles in fine chemicals manufacturing. As of early 2026, 51% of global catalytic systems in fine chemicals and polymer production utilize organometallic catalysts, reflecting their superior selectivity and reduced waste generation. In parallel, 47% of next-generation semiconductors and specialty materials integrate organometallic precursors, particularly for Atomic Layer Deposition (ALD) and Chemical Vapor Deposition (CVD) processes that enhance conductivity and thermal stability. The pharmaceutical sector further reinforces demand, with 44% of new drug formulations relying on organometallic intermediates for complex API synthesis, necessitating high-purity and automated production systems. Market concentration remains moderate, with top players controlling 45–65% of supply, enabling sustained R&D investments averaging 2.3% of revenue, while liquid organometallics dominate with over 52% market share, favored for precision dosing and improved reaction kinetics in industrial-scale operations.

The global organometallics industry is undergoing rapid transformation driven by innovation in energy applications, catalytic research, and infrastructure-led manufacturing expansion. In March 2026, industry reports highlighted a surge in organometallic-based photovoltaics and solar inks, signaling strong adoption in renewable energy systems and advanced fuel cell technologies, where structural tunability and efficiency gains are critical. In February 2026, India’s Union Budget introduced a ₹600 crore ($72 million) allocation for three dedicated chemical parks, designed as plug-and-play hubs for specialty chemical and organometallic manufacturers, integrating shared infrastructure for waste management and carbon capture, utilization, and storage (CCUS). This policy reflects a broader push toward cluster-based manufacturing and sustainability compliance.

Technological advancements in catalysis are further strengthening the market’s innovation pipeline. In February 2026, the CNR-ICCOM announced a breakthrough in zeolite-supported platinum catalysts, improving efficiency in propane-to-propylene conversion, a key process for petrochemical and polymer industries. Meanwhile, in January 2026, Saudi Arabia accelerated its position in the global chemical value chain as Ma’aden advanced feedstock allocation for large-scale expansion projects aimed at tripling chemical output by 2030, with a strong focus on downstream organometallic derivatives. These developments highlight increasing vertical integration and regional capacity scaling.

M&A activity and policy-driven decarbonization initiatives are reshaping competitive dynamics and investment priorities. In December 2025, global chemical M&A activity rose 18% year-over-year, with major players such as BASF, DuPont, and AkzoNobel actively restructuring portfolios to prioritize high-margin specialty organometallics and advanced polymers. In November 2025, governments allocated approximately ₹20,000 crore ($2.4 billion) toward carbon capture deployment in the chemical sector, directly benefiting organometallic manufacturers transitioning to low-carbon production models. Additionally, in October 2025, ADEKA Corporation announced a new facility dedicated to EUV lithography organometallic precursors, targeting the stringent purity requirements of advanced semiconductor manufacturing. Earlier, in July 2025, NITI Aayog outlined a long-term roadmap to strengthen India’s position in global chemical value chains, focusing on reducing import dependency for critical organometallic intermediates and APIs. Collectively, these developments underscore a market evolving toward high-purity innovation, energy transition alignment, and globally integrated specialty chemical ecosystems.

Organometallics Market Trends and Opportunities

Trend: Capacity Expansion for High-Purity Organometallic Reagents in Advanced API Synthesis

The organometallics market is experiencing a structurally important shift toward high-purity, pharmaceutical-grade reagents as drug discovery pipelines increasingly focus on complex small molecules, chiral intermediates, and peptide-based therapeutics. Modern oncology, antiviral, and metabolic disease APIs demand precise late-stage functionalization, where organoaluminum, organomagnesium (Grignard), and lithium-based reagents play a non-substitutable role. As synthesis pathways become shorter but more chemically sophisticated, impurity tolerance has narrowed significantly, elevating organometallic purity from a quality attribute to a regulatory necessity.

This shift is directly influencing capacity investment decisions. In 2025, life-sciences-focused expansions signaled that pharmaceutical demand is now one of the most profitable end markets for organometallic manufacturers. Contract Development and Manufacturing Organizations are increasingly integrating organometallic reagent production into their own facilities to eliminate transportation risk, reduce exposure to thermal instability, and maintain strict batch-to-batch consistency for regulated APIs. This insourcing trend reflects both safety considerations and economic logic, as in-situ production improves yield control and shortens development timelines.

At the innovation level, breakthroughs in late-stage functionalization are redefining the strategic value of organometallic chemistry. New bench-stable reagents and skeletal editing techniques demonstrated in 2025 allow direct carbon insertion into complex drug molecules at room temperature, achieving near-quantitative yields. These advances reduce the number of synthetic steps required to diversify molecular libraries, potentially lowering pharmaceutical R&D costs by up to 30% while accelerating time-to-clinic. As a result, demand is shifting away from commodity organometallics toward high-margin, application-specific reagents optimized for pharmaceutical synthesis under GMP conditions.

Trend: Transition to Metallocene Catalyst Systems for Circular and High-Performance Polyolefins

The global polyolefins industry is rapidly transitioning from traditional Ziegler-Natta catalysts to single-site metallocene systems as sustainability, recyclability, and material efficiency become non-negotiable requirements. Metallocene organometallic catalysts offer precise control over polymer chain architecture, enabling narrower molecular weight distributions and superior mechanical properties. This precision is increasingly essential as packaging, automotive, and consumer goods producers pursue downgauging strategies to reduce material usage without compromising performance.

Commercial adoption accelerated through 2024–2025 as new high-capacity polyethylene and polypropylene plants were commissioned using metallocene-based technologies. These systems allow producers to manufacture thinner films with up to 35% higher tensile strength, enabling material reductions of 15 to 20% while maintaining barrier and stiffness requirements. For flexible packaging converters, this performance advantage has shifted metallocene resins from premium options to baseline specifications, particularly for food, medical, and high-clarity applications.

Metallocene organometallics are also proving critical in advanced recycling and upcycling pathways. As post-consumer recycled feedstocks exhibit inconsistent molecular structures, single-site catalysts offer superior tolerance to variability, allowing producers to restore mechanical performance in recycled polymers. Regulatory approvals obtained in 2025 for food-contact applications underscore the role of metallocene catalysts in closing the loop on plastics. This trend positions organometallic catalyst systems as foundational enablers of circular economy compliance across global polymer value chains.

Opportunity: Ultra-High-Purity Organometallic Precursors for OLED and Semiconductor Fabrication

The expansion of 5G infrastructure, miniaturized electronics, and flexible display technologies is creating a high-margin opportunity for ultra-high-purity organometallic precursors used in metalorganic chemical vapor deposition and atomic layer deposition processes. Compounds such as trimethylindium and dimethylzinc are now mission-critical inputs for next-generation OLED displays, image sensors, and advanced logic devices, where even trace metallic or oxygen impurities can compromise device performance and yield.

By late 2025, more than one-quarter of new flat-panel displays relied on ALD-deposited organometallic coatings to enhance resolution, moisture resistance, and operational lifespan. This has fundamentally shifted procurement toward sub-parts-per-billion purity specifications, elevating purification technology and precursor handling systems into strategic differentiators. Semiconductor fabs are increasingly upgrading to inert-gas-shielded delivery systems to manage the moisture sensitivity of these reagents, which now represent a significant share of total ALD material costs.

Regionalization is reinforcing this opportunity. Asia-Pacific has emerged as the dominant hub for electronics-grade organometallics, supported by localized investments that ensure supply security for display and semiconductor manufacturers. This “local-for-local” model reduces logistics risk and aligns with national industrial policies, creating long-term, high-visibility demand for specialty organometallic producers with advanced purification and quality control capabilities.

Opportunity: Organotin-Free Catalyst Systems for Next-Generation Silicone Applications

Regulatory pressure on organotin compounds is accelerating a fundamental reformulation cycle in the global silicone industry. Organotin catalysts, long favored for their efficiency in RTV and elastomer curing, are being phased out due to mounting concerns around reproductive toxicity and long-term human exposure. The 2025 expansion of restricted substance lists under EU chemical regulations has set firm compliance deadlines, effectively mandating a transition to alternative organometallic catalyst systems.

This shift is opening a substantial growth avenue for organo-titanate and organo-zirconate catalysts, which offer comparable curing efficiency without the toxicological profile associated with tin. Demand is particularly strong in medical devices, electronics encapsulation, aerospace coatings, and personal care silicones, where catalyst residues must meet stringent biocompatibility and migration standards. Manufacturers are increasingly positioning tin-free systems as both a regulatory solution and a performance upgrade, emphasizing improved clarity, reduced odor, and enhanced long-term stability.

Strategic capacity expansions in 2025 underscore the commercial importance of this transition. New specialty silicone complexes are being designed specifically to serve high-safety, high-purity markets, where compliance with global health and environmental standards is a prerequisite for market access. As organotin-free curing becomes the industry norm rather than an exception, alternative organometallic catalysts are expected to capture sustained, premium-priced demand across multiple downstream sectors.

Organometallics Market Share and Segmentation Insights

Organo-Aluminum Compounds Lead Organometallics Market Through Polyolefin Polymerization Catalysis

Organo-aluminum compounds accounted for 28.40% of the Organometallics Market by type in 2025, making them the leading class of organometallic chemicals used in polymer manufacturing. Compounds such as triethylaluminum, trimethylaluminum, and methylaluminoxane are essential co-catalysts in Ziegler-Natta and metallocene polymerization processes used to produce polyethylene and polypropylene. The massive scale of global polyolefin production continues to drive demand for these highly reactive organometallic intermediates. In 2025, the growth of metallocene catalyst technologies is strengthening consumption of high-purity organo-aluminum activators such as methylaluminoxane, which enable precise polymerization control and support the production of advanced polyolefins with improved mechanical properties and processability.

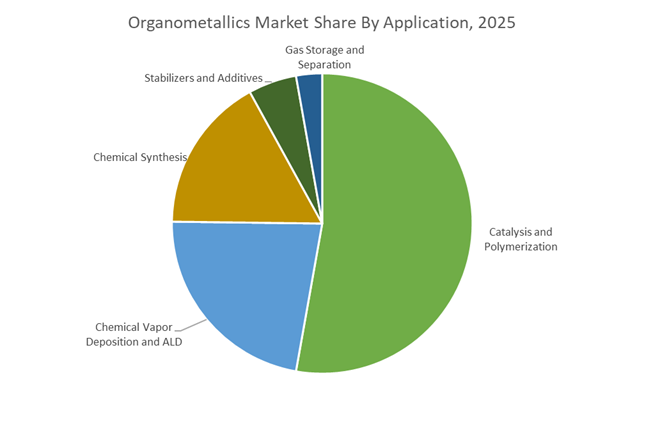

Catalysis and Polymerization Segment Dominates Organometallic Consumption in Advanced Chemical Manufacturing

Catalysis and polymerization represented 52.80% of the Organometallics Market by application in 2025, accounting for the majority of global organometallic compound usage. These materials function as catalysts and co-catalysts in the production of high-volume polymers including polyethylene and polypropylene, as well as in numerous industrial chemical synthesis processes. Their unique reactivity enables efficient and selective catalytic transformations that improve manufacturing productivity and product consistency. In 2025, the growing adoption of single-site catalyst systems, including metallocene and post-metallocene catalysts, is increasing demand for specialized organometallic activators and initiators capable of controlling polymer architecture and molecular structure in advanced polymerization technologies.

Organometallics Market Competitive Landscape

The Organometallics Market is evolving toward high-purity electronic-grade precursors, advanced catalytic systems, and vertically integrated supply chains. Key players are prioritizing semiconductor-grade materials, sustainable organometallic chemistry, and localized production capabilities to address stringent process tolerances and geopolitical supply chain risks.

Albemarle sharpens focus on lithium organometallics and semiconductor-grade precursors

Albemarle Corporation is strengthening its leadership in organometallic intermediates by pivoting toward high-growth lithium-based organometallics and advanced materials. The planned divestment of its Ketjen catalyst business in Q1 2026 enables sharper capital allocation toward energy storage and specialty chemicals. Strong operational performance, with $1.3 billion in cash flow and over $450 million in productivity gains in 2025, underpins its expansion strategy. The company is investing in high-purity organometallic precursors tailored for semiconductor and polymer applications requiring ultra-tight process tolerances. Despite operational disruptions at its Jordan Bromine Company joint venture, rapid recovery ensured continuity in bromine-based organometallic supply. This combination of resource control, financial strength, and specialty focus enhances Albemarle’s competitive positioning.

BASF scales homogeneous catalysis and Asia-Pacific capacity via Verbund integration

BASF SE is leveraging its integrated Verbund model and ECMS division to maintain a strong position in organometallic catalysts and intermediates. Its expertise in homogeneous catalysis supports critical industrial processes such as hydroformylation and carbonylation, reinforcing its role in high-performance chemical manufacturing. The Zhanjiang Verbund expansion significantly increases production capacity in Asia-Pacific, aligning with regional demand for organometallic catalysts. BASF’s cost optimization program, targeting €2.3 billion in savings by 2026, enhances operational efficiency amid global cost pressures. Financial guidance of €6.2–€7.0 billion EBITDA reflects stable growth driven by Chemicals and Nutrition & Care segments. This integration of scale, efficiency, and catalytic expertise strengthens BASF’s global market leadership.

Dow accelerates AI-driven specialty organometallics for electronics and sustainable materials

Dow Inc. is advancing its position in organometallic stabilizers and catalysts through its Transform to Outperform strategy, focused on AI-driven operational efficiency and portfolio simplification. The initiative targets $2 billion in EBITDA improvement, supported by automation and digitalization across specialty chemicals production. Dow’s Cooling Science Studio in Shanghai enhances development of organometallic precursors for semiconductor applications, including ALD processes critical for advanced electronics. The company’s ISCC PLUS-certified facilities support bio-circular feedstocks for sustainable organometallic-based polyurethane catalysts. Strong liquidity, bolstered by a CAD $1.62 billion legal settlement, enables continued R&D investment. This strategic alignment of digitalization, sustainability, and electronics-focused innovation strengthens Dow’s competitive edge.

Evonik advances custom organometallic synthesis for pharmaceuticals and high-performance polymers

Evonik Industries AG is differentiating itself through custom organometallic synthesis and focus on high-margin specialty applications. Long-term supply agreements with pharmaceutical companies for transition metal catalysts highlight its strength in complex drug synthesis. Its Advanced Technologies segment, generating €5.97 billion in 2025 revenue, targets high-performance polymers and specialty additives for automotive and aerospace industries. Structural optimization under the “Evonik Tailor Made” program, including workforce reduction, is improving agility and cost efficiency. With projected EBITDA of €1.7–€2.0 billion in 2026, the company is balancing profitability with innovation investments. This specialization in low-volume, high-value organometallic chemistry reinforces Evonik’s niche leadership.

Merck drives electronic-grade organometallic innovation for semiconductor miniaturization

Merck KGaA is a leading provider of ultra-high-purity organometallic precursors, critical for semiconductor manufacturing and next-generation electronics. Its Optronics and semiconductor solutions portfolio focuses on ALD and CVD precursors essential for chip miniaturization in AI and 5G applications. Following the divestment of its Surface Solutions business, Merck has restructured its Life Science division to better serve regulated markets requiring precision organometallic reagents. With €21.1 billion in sales and a 28.9% EBITDA margin in 2025, the company demonstrates strong profitability in high-value specialty materials. Strategic focus on R&D pipeline expansion and digital sales channels supports long-term growth. This emphasis on electronic-grade purity and innovation positions Merck at the forefront of semiconductor-driven demand.

China – Polymer Catalyst Scale-Up and MOF Commercialization

China’s organometallics industry is moving decisively toward scale leadership in polymer catalysts while simultaneously incubating next-generation applications in carbon capture and semiconductors. In October 2025, Nouryon completed a major expansion at its Jiaxing facility, doubling production capacity for triethylaluminum. TEAL remains a cornerstone co-catalyst for Ziegler–Natta and metallocene systems, underpinning China’s rapid growth in high-performance polyethylene and polypropylene. This expansion directly supports domestic resin producers seeking tighter molecular weight control and improved process economics.

Beyond polymers, China is accelerating organometallic innovation through Metal-Organic Frameworks. The Tianjin Nangang Industrial Zone has emerged as a focal point for MOF research, with a dedicated innovation center scheduled for 2026 to advance MOF-based carbon capture and storage solutions at industrial scale. Forward-looking capacity plans further reinforce this trajectory. Nouryon’s announcement to localize production of modified methylaluminoxane by 2027 positions China to supply critical elastomer catalysts used in solar encapsulants. In semiconductors, Sumitomo Chemical expanded its mainland footprint through the acquisition of a Taiwanese process-chemicals business, strengthening access to high-purity organometallic precursors. Integration across the value chain is deepening via Prime Polymer, where Mitsui Chemicals, Idemitsu Kosan, and Sumitomo Chemical centralized catalyst procurement, while joint R&D efforts earned recognition through the 2025 Nikkei New Office Award for process efficiency.

United States – Semiconductor Precursors and Functional Material Substitution

The United States organometallics market is defined by semiconductor demand, productivity-led growth, and material substitution away from restricted chemistries. In late 2024 and early 2025, American Elements expanded domestic manufacturing of organometallic precursors for metal-organic chemical vapor deposition, aligning supply with the rapid build-out of U.S. chip fabrication capacity. Distribution partnerships are also shaping access. In March 2024, Nordmann partnered with Ketjen to strengthen availability of high-purity cross-linking agents for elastomers and polymers.

Operational efficiency remains a differentiator. Albemarle reported volume growth in 2025 within its Ketjen catalysts division, reflecting improved fixed-cost absorption and productivity across U.S. assets. Advanced applications are broadening. Mitsubishi Chemical Group is scaling U.S. manufacturing for organometallic binders used in carbon fibers that enhance thermal management in AI server hardware. Parallel R&D has yielded PFAS substitutes, with Mitsubishi Chemical’s SoarnoL resin platform demonstrating organometallic-based performance in oil-resistant paper packaging, supporting regulatory-driven material transitions.

Germany – EU Raw Materials Security and Circular Organometallic Additives

Germany anchors the European organometallics ecosystem through policy alignment with critical materials security and demonstrable life-cycle benefits. Following the EU Critical Raw Materials Act in May 2024, Germany prioritized dozens of strategic projects, including organometallic processing routes for rare earth elements essential to permanent magnets in wind turbines. These initiatives are closely linked to the Minerals Security Partnership, which coordinated substantial capital in 2025 to support extraction and secondary recovery of metals feeding organometallic synthesis.

Product innovation is converging with sustainability. At K 2025 in Düsseldorf, Evonik unveiled organometallic–silane hybrids under its Smart Effects unit, targeting efficiency gains in green tire compounds. German majors have also published life-cycle assessments for organometallic-stabilized polyamides such as VESTAMID®, evidencing significant carbon reductions via mass-balanced certified processes. These disclosures are strengthening buyer confidence in circular polymer additives while reinforcing Germany’s role as a compliance-led innovation hub.

India – Demand-Led Catalyst Localization and Cluster-Based R&D

India’s organometallics industry is scaling primarily through polymer demand and targeted localization of precursor synthesis. Polypropylene consumption reached multi-million-tonne levels in 2024, driving increased domestic use of Ziegler–Natta catalysts and associated organometallic components. This demand pull is reshaping investment priorities across petrochemicals and specialty additives.

Government-backed innovation infrastructure is accelerating capability build-out. Expansion of the Science and Technology Clusters initiative to 25 sites in 2025 has enabled localized synthesis and application development of organometallic precursors for pharmaceuticals and agrochemicals. Large integrated players are reinforcing this shift. Reliance Industries increased investments in organometallic-based additives to support high-performance polymers under the Atmanirbhar Bharat framework, improving domestic resilience in advanced materials.

Japan – Electronic Materials Leadership and MOF Applications

Japan’s organometallics industry remains tightly coupled to electronics, batteries, and space technologies, with a strong emphasis on intellectual property and precision manufacturing. In 2025, Mitsubishi Chemical Group received the Asia IP Elite award for excellence in electrolyte licensing, an area reliant on organometallic lithium salts and advanced synthesis control. This recognition underscores Japan’s leadership in high-purity organometallic materials for energy storage.

Emerging applications are broadening the scope. Space technology ventures such as Pale Blue, in collaboration with JAXA, are leveraging MOF technology to develop lightweight fuel tanks for satellite propulsion. In batteries, Sumitomo Chemical restructured its separator business in late 2025, refocusing R&D on organometallic coatings that enhance thermal stability, aligning safety performance with next-generation cell designs.

Comparative Country Snapshot – Organometallics Industry

Organometallics Market County Level Snapshot

|

Country

|

Primary Growth Driver

|

Key Organometallic Focus

|

Strategic Position

|

|

China

|

Polymer scale and MOF CCS

|

TEAL, MMAO, MOFs

|

Global scale-up and diversification leader

|

|

United States

|

Semiconductor fabs and substitution

|

MOCVD precursors, functional resins

|

High-purity and productivity-driven

|

|

Germany

|

Raw materials security and circularity

|

Silane hybrids, stabilized polyamides

|

EU compliance and LCA benchmark

|

|

India

|

Polymer demand and localization

|

Ziegler–Natta catalysts

|

Fast-growing domestic consumption base

|

|

Japan

|

Electronics, batteries, space

|

Lithium salts, MOF systems

|

Precision and IP-led innovation

|

Organometallics Market Report Scope

Organometallics Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.2 Billion

|

|

Market Size (2034)

|

$6.9 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Type (Organo-Aluminum Compounds, Organo-Lithium Compounds, Organo-Tin Compounds, Organo-Magnesium Compounds, Organo-Silicon Compounds, Transition Metal Organometallics, Metal-Organic Frameworks), By Application (Catalysis and Polymerization, Chemical Vapor Deposition and ALD, Chemical Synthesis, Stabilizers and Additives, Gas Storage and Separation), By End-User Industry (Polymers and Plastics, Electronics and Semiconductors, Pharmaceuticals and Medical Technology, Automotive, Environmental and Aerospace)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Albemarle, Nouryon, BASF, Sumitomo Chemical, Mitsubishi Chemical Group, Evonik Industries, Dow, American Elements, Mitsui Chemicals, Sinopec, LANXESS, Johnson Matthey, LG Chem, Tosoh, Merck

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Organometallics Market Segmentation

By Type

- Organo-Aluminum Compounds

- Organo-Lithium Compounds

- Organo-Tin Compounds

- Organo-Magnesium Compounds

- Organo-Silicon Compounds

- Transition Metal Organometallics

- Metal-Organic Frameworks

By Application

- Catalysis and Polymerization

- Chemical Vapor Deposition and ALD

- Chemical Synthesis

- Stabilizers and Additives

- Gas Storage and Separation

By End-User Industry

- Polymers and Plastics

- Electronics and Semiconductors

- Pharmaceuticals and Medical Technology

- Automotive

- Environmental and Aerospace

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Organometallics Industry

- Albemarle

- Nouryon

- BASF

- Sumitomo Chemical

- Mitsubishi Chemical Group

- Evonik Industries

- Dow

- American Elements

- Mitsui Chemicals

- Sinopec

- LANXESS

- Johnson Matthey

- LG Chem

- Tosoh

- Merck

*- List not Exhaustive