Oxidized Polyethylene Wax Market Driven by PVC Expansion, PFAS-Free Processing, and Digitalized Additive Manufacturing

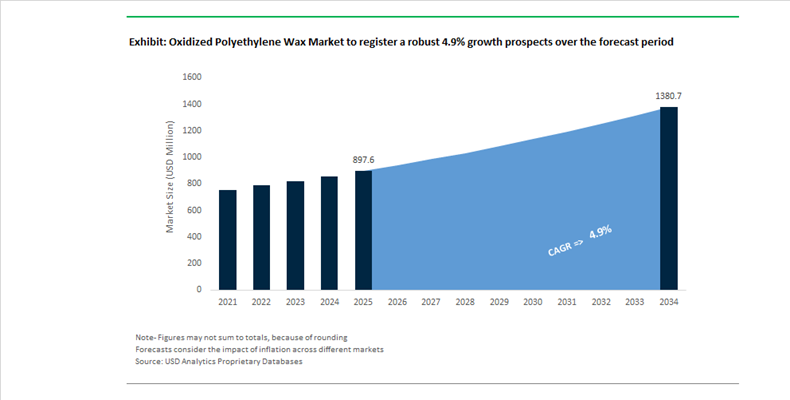

The Oxidized Polyethylene (OPE) Wax Market is projected to expand from $897.6 Million in 2025 to $1,380.6 Million by 2034, registering a CAGR of 4.9%. Growth is structurally tied to PVC processing, polyolefin film extrusion, masterbatch compounding, automotive coatings, and specialty inks. OPE waxes function as external lubricants, dispersing agents, and surface modifiers, offering improved melt flow, gloss control, scratch resistance, and pigment dispersion. Their polar functional groups—introduced during oxidation—differentiate them from non-oxidized polyethylene waxes, enabling stronger compatibility with PVC and polar polymers.

In May 2024, Clariant introduced Licolub® PED 1316 at NPE2024, a high-density oxidized polyethylene wax engineered for PVC extrusion. The product addresses supply tightness in construction applications such as window profiles, pipes, and moldings by enhancing lubrication efficiency and delivering improved optical whiteness. As global infrastructure programs accelerate—particularly in India and Southeast Asia—the demand for stable, high-performance PVC lubricants is intensifying. India’s initiative to quadruple PVC capacity by 2030 is reshaping procurement strategies, compelling global wax manufacturers to localize oxidation capacity to mitigate import tariffs and logistics volatility.

Industry consolidation is strengthening vertical integration. In late 2025, Westlake Corporation completed the acquisition of ACI Compounding Solutions. This transaction integrates upstream ethylene production with downstream compounding expertise, positioning Westlake to internalize OPE wax demand within its compound formulations. As compounding becomes more formulation-driven—particularly for cable insulation, rigid packaging, and automotive trim—OPE waxes are increasingly optimized for precise molecular weight distribution and acid number to ensure consistent dispersion in filled systems.

Sustainability and regulatory reform are reshaping additive portfolios. In April 2024, Clariant launched AddWorks® PPA, a PFAS-free polymer processing aid line, signaling a broader market shift away from fluorinated lubricants. Although distinct from OPE waxes, this regulatory shift increases the strategic importance of polar waxes as compliant lubrication alternatives in film extrusion. Meanwhile, BASF showcased at Plastindia 2026 how polar waxes extend the life cycle of agricultural films (“plasticulture”) by improving processing stability and UV resistance in irrigation and mulch films. BASF’s upcoming Digital Hub in Hyderabad (2026) is expected to leverage AI-driven oxidation control to refine acid value consistency and reduce batch variability—an increasingly critical differentiator in high-spec applications.

Technology-driven differentiation is also evident among established producers. Honeywell continues advancing its A-C® oxidized wax series with tighter oxidation precision through digitalized manufacturing, improving performance predictability in PVC and coatings. In coatings, OPE waxes enhance abrasion resistance and matting effects; collaborations such as BASF’s global refinish program with INEOS Automotive underscore their importance in automotive topcoats.

Simultaneously, bio-based competition is intensifying. At K 2025, Clariant introduced Licocare® RBW Vita, derived from rice bran wax, signaling the emergence of oxidized bio-waxes as partial substitutes in electronics and specialty plastics. While petroleum-based OPE wax retains dominance due to cost and scalability, ESG mandates are gradually opening niche markets for renewable alternatives.

Market-Defining Trends and Monetizable Opportunities in the Oxidized Polyethylene Wax (OPE Wax) Market

PCR-Driven Masterbatch Reformulation Accelerates Adoption of High-Acid OPE Wax Dispersants

The rapid escalation of post-consumer recycled (PCR) content mandates across packaging, consumer goods, and industrial plastics is fundamentally altering dispersion economics within the masterbatch industry. As recycled polyethylene and polypropylene streams exhibit higher polarity variance, contamination, and inconsistent melt behavior, conventional paraffin waxes are increasingly unable to deliver uniform pigment dispersion or surface finish consistency. Oxidized polyethylene waxes, particularly grades with elevated acid values, are emerging as indispensable compatibility agents that bridge polar pigments with non-polar recycled polymer matrices.

In January 2025, Nouryon publicly emphasized that specialized organic dispersants, including oxidized waxes, are essential to maintaining color consistency across mixed PCR feedstocks. Internal formulation benchmarks cited by industry participants show that optimized OPE wax usage enables a 10% to 15% increase in pigment loading without compromising tensile strength or impact resistance in recycled compounds. Complementing formulation gains, a 2024 technical assessment by SCG Chemicals demonstrated that OPE waxes outperform paraffin waxes due to their carbonyl and hydroxyl functionalities, which materially improve pigment and filler dispersion in polyethylene and polypropylene blends.

From a processing standpoint, late-2024 industry benchmarking indicates that replacing standard PE waxes with OPE waxes can reduce filter-pressure buildup by up to 25% in masterbatch extrusion lines. This translates into longer production runs, fewer screen changes, and improved line utilization when processing inconsistent or contaminated PCR streams. As surface luster and color uniformity increasingly determine pricing premiums in the Grade-A recycled plastics segment, OPE waxes are shifting from formulation enhancers to structurally necessary inputs.

Thermal Stability Requirements Force Reformulation Cycles in Hot Melt Adhesives

The expansion of high-speed e-commerce logistics and the growing thermal loads inside modern vehicles are driving mandatory reformulation across the hot melt adhesives market. Legacy hydrocarbon tackifiers are increasingly exposed to performance failure through bleeding, bond degradation, and charring under high-temperature storage and application conditions. High-melting-point oxidized polyethylene waxes are being adopted as functional replacements to stabilize open time, control viscosity, and preserve bond integrity.

In February 2025, Honeywell highlighted growing demand for high-performance specialty materials within its Sensing and Safety Technologies portfolio, positioning OPE wax-based systems as effective open-time regulators. These formulations enable e-commerce cartons to remain sealed even when stored in non-climate-controlled warehouses exceeding 50°C, a critical operational requirement as logistics networks expand into warmer regions.

Automotive applications are reinforcing this shift. As of 2025, OEMs are tightening specifications around low-fogging and low-VOC interior adhesives. Technology briefings issued during 2024–2025 by BASF underline a transition toward UV-curable and thermally stable OPE-modified adhesive systems that prevent adhesive oozing in dashboard and trim assemblies exposed to direct solar radiation. Additionally, OPE waxes offer a rare combination of low melt viscosity and high softening point, enabling instant set times on automated packaging lines processing over 100 units per minute while maintaining resistance to thermal degradation within melting tanks.

High-Purity OPE Wax Gains Traction in Semiconductor CMP and Precision Optics Polishing

The semiconductor industry’s migration toward 3nm and 2nm process nodes is sharply tightening tolerances for particle stability in chemical mechanical planarization slurries. In this context, oxidized polyethylene waxes are being evaluated as secondary emulsifiers and rheology modifiers capable of preventing agglomeration of alumina and silica abrasives in aqueous CMP systems.

Research published in 2025 by Polysciences confirms that polar organic additives play a critical role in controlling zeta potential within CMP slurries. OPE waxes improve abrasive suspension stability during the polishing of gallium nitride and silicon carbide wafers, materials that are increasingly central to electric vehicle power electronics and 5G infrastructure.

Parallel adoption is emerging in precision optics manufacturing. In high-end camera lenses and lithography optics, OPE-based emulsions are used as controlled surface lubricants during final-stage polishing. This approach reduces micro-scratching and has been shown to improve yields of defect-free optical components by approximately 12%. Regulatory momentum from EU Green Deal directives to reduce solvent usage is accelerating the shift toward aqueous polishing systems, where the emulsifiability and stability of OPE waxes create a clear competitive advantage.

Regulatory-Compliant Anti-Blocking Solutions for Compostable Food-Contact Films

The rapid penetration of biodegradable packaging materials such as PLA and PBAT has exposed persistent processing challenges, particularly film blocking during high-speed winding and bagging. Oxidized polyethylene waxes are emerging as a non-toxic, non-migratory anti-blocking solution that aligns processing efficiency with food-contact regulatory compliance.

Under FDA 21 CFR 172.260, oxidized polyethylene is approved as a surface-finishing agent for food-contact plastics, while EU Regulation 10/2011 establishes stringent migration limits. Updated technical validations released in July 2025 confirm that OPE wax grades meet both FDA and EFSA requirements, positioning them as safe-by-design additives for flexible food packaging. Application studies conducted in 2025 show that incorporating as little as 0.5% OPE wax into PLA films can reduce the coefficient of friction by approximately 40%, significantly improving machinability on automated packaging lines without compromising compostability.

Oxidized Polyethylene Wax Market Share and Segmentation Insights

Low-Density Oxidized Polyethylene Wax Leads Market Adoption in Waterborne Coatings and Additive Formulations

Low-density oxidized polyethylene wax accounted for 58.60% of the Oxidized Polyethylene Wax Market by product type in 2025, making it the dominant wax additive used across coatings, inks, and textile processing applications. Its lower molecular weight structure and higher acid number enable improved emulsifiability, compatibility with polymer systems, and efficient dispersion in formulation matrices. These characteristics make low-density oxidized polyethylene wax particularly valuable in paints and coatings, printing inks, and textile finishing processes where surface performance and additive stability are essential. In 2025, the transition toward waterborne coating systems has increased demand for low-density oxidized polyethylene wax because its emulsifiable properties allow stable incorporation into aqueous formulations while delivering slip resistance, mar protection, and enhanced surface durability.

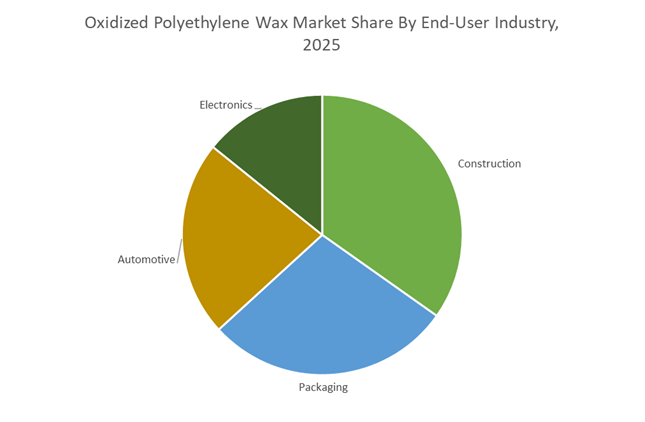

Construction Industry Drives Oxidized Polyethylene Wax Consumption in Architectural Coatings and Building Materials

The construction sector represented 34.80% of the Oxidized Polyethylene Wax Market by end-user industry in 2025, reflecting strong demand from architectural coatings, plastic building materials, and construction chemical formulations. Oxidized polyethylene wax is widely used as a performance additive in coatings applied to residential and commercial structures, as well as in polymer processing for building profiles, pipes, and construction plastics. Ongoing infrastructure development and building renovation activities continue to support wax additive consumption. In 2025, manufacturers are increasingly specifying oxidized polyethylene wax in durable building product formulations, where its ability to improve UV stability, weather resistance, scratch protection, and surface longevity enhances the performance and lifecycle of construction coatings and polymer-based building materials.

Oxidized Polyethylene Wax Market Competitive Landscape

The Oxidized Polyethylene Wax Market is driven by VOC-free formulations, bio-based wax alternatives, and ultra-low viscosity additives tailored for high-speed printing and PVC processing. Leading players are leveraging advanced oxidation technologies, vertical integration, and sustainable feedstocks to deliver high-performance OPE waxes with enhanced dispersion, lubrication, and processing efficiency.

Honeywell drives low-volatility OPE wax innovation for PVC and packaging inks

Honeywell International Inc. maintains a strong position in the oxidized polyethylene wax market through its A-C® performance additives portfolio, supported by advanced oxidation technology and digital-first R&D capabilities. The company is prioritizing low-volatility OPE waxes to meet stringent global emissions standards while improving processing efficiency in PVC and coatings applications. Its A-C® 300 series remains a benchmark for high-density OPE wax, delivering superior external lubrication and reduced plate-out during PVC extrusion. Production optimization at its Orange, Texas facility has increased output of micronized OPE waxes, targeting high-scuff resistance in packaging inks. Honeywell’s broad acid number range enables precise emulsification control in water-based systems such as floor polishes and textile finishes. This combination of formulation flexibility, process efficiency, and regulatory alignment strengthens its competitive edge.

Clariant integrates renewable wax technologies with high-performance OPE emulsions

Clariant AG is advancing its position in the oxidized polyethylene wax market by integrating green chemistry principles with high-performance wax additives. The launch of Ceridust® 1310 addresses supply chain volatility in printing inks by offering a stable alternative to natural waxes, while maintaining consistent performance in industrial applications. Its Licocare® RBW approval for food-contact plastics highlights a strategic shift toward blending OPE wax functionality with renewable feedstocks. Over 50% of Clariant’s wax portfolio now features a Renewable Carbon Index above 50%, appealing to automotive and construction sectors focused on Scope 3 emission reduction. The company’s global application labs provide real-time technical support for transitioning to aqueous OPE emulsions. This integrated approach positions Clariant as a leader in sustainable and application-specific wax solutions.

BASF strengthens pigment dispersion and sustainable wax production via Verbund integration

BASF SE leverages its Verbund integration model to deliver cost-efficient, high-performance oxidized polyethylene waxes under its Joncryl® and Luwax® brands. The introduction of Joncryl® Wax 30 enhances mar resistance in sustainable packaging coatings while maintaining recyclability of paper substrates. BASF is advancing its “Winning Ways” strategy by reducing product carbon footprint through mass-balanced bio-feedstocks in its Luwax® OA series. Its OPE waxes are widely used as pigment dispersants in masterbatches, ensuring uniform color distribution in polar polymers such as ABS and PA. Expansion of circular production capabilities, including the Shanghai loopamid® facility, supports access to high-quality recycled feedstocks. This integration of sustainability, performance, and supply security reinforces BASF’s leadership in specialty wax additives.

Westlake leverages ethylene integration to scale adhesive-grade OPE wax production

Westlake Corporation is strengthening its competitive position through vertical integration and reliable feedstock supply for its Epolene® oxidized polyethylene wax portfolio. The successful turnaround of its Petro 1 ethylene facility restored full capacity, ensuring consistent polyethylene availability for downstream oxidation processes. Its Epolene® E-series waxes are widely used in hot melt adhesives, delivering an optimal balance of open time and bond strength in packaging applications. The company’s ownership structure supports stable cash flow generation, enabling continued investment in specialty wax R&D. Expansion of its technical sales presence in the IMEA region targets growing demand in PVC pipe infrastructure and footwear manufacturing. This combination of feedstock security, application focus, and regional expansion enhances Westlake’s market positioning.

Mitsui Chemicals advances high-purity OPE waxes with biomass and metallocene technology

Mitsui Chemicals, Inc. is a leading Asian player in the oxidized polyethylene wax market, focusing on high-purity, performance-driven waxes for electronics and automotive applications. The consolidation of its Chiba Ethylene Complex with Idemitsu Kosan improves feedstock efficiency and cost competitiveness for its Hi-Wax™ product line. ISCC PLUS certification at its Otake Plant enables the production of biomass-based OPE wax via mass-balance methods, targeting sustainability-driven customers in Japan and South Korea. Hi-Wax™ 4051E and 4052E grades offer high acid value and low melting points, making them ideal for toner resins and high-gloss coatings. Mitsui’s expertise in metallocene-catalyzed polyolefins ensures narrow molecular weight distribution and superior thermal stability. This technological advantage positions Mitsui at the forefront of high-performance specialty wax innovation.

United States – Feedstock Security, Precision Additives, and High-Performance End Uses

The United States oxidized polyethylene wax industry is structurally advantaged by feedstock security, process precision, and expanding high-value applications. The successful mid-2025 turnaround of Westlake Chemical’s Petro 1 ethylene facility restored nameplate capacity, reinforcing domestic availability of high-purity polyethylene required for controlled oxidation processes. This stability is amplified by the shale gas ecosystem, where low-cost ethane continues to underpin cost-competitive PE and OPE wax production. In parallel, Honeywell International is directing 2025–2026 R&D toward its A-C® performance additives, positioning oxidized PE waxes as critical processing aids in PVC extrusion for high-voltage cable insulation and advanced electrical infrastructure.

Strategically, the U.S. market is also being shaped by regulatory and application-led shifts. The EPA’s 2025 technology transitions under the AIM Act are accelerating substitution of conventional lubricants with oxidized PE waxes compatible with low-GWP refrigerants. Distribution efficiency has improved through Nordmann’s 2024 partnership with Ketjen, broadening access to specialty wax cross-linkers and polymer additives across North America. Demand diversification is notable, with U.S. manufacturers increasingly deploying OPE waxes in AI server thermal management systems and premium automotive scratch-resistant coatings, signaling a move beyond traditional plastics and coatings toward electronics and data-center-driven consumption.

China – Scale Expansion, Specialty Integration, and Electronic-Grade Focus

China continues to define the global volume and export dynamics of oxidized polyethylene wax, supported by aggressive capacity expansion and deep integration with polyolefin value chains. In August 2025, Clariant commissioned its second production line at the Cangzhou facility under its joint venture with Beijing Tiangang Auxiliary, directly targeting Asian demand for high-end polymer stabilizers and modifiers. Feedstock integration is being reinforced through the September 2025 MOU between Mitsui Chemicals, Idemitsu Kosan, and Sumitomo Chemical to consolidate polyolefin operations under Prime Polymer, centralizing PE supply critical for consistent OPE wax synthesis.

Policy direction is equally influential. The Ministry of Industry and Information Technology of China 2026 roadmap prioritizes electronic-grade rheological modifiers and waxes, elevating purity and molecular-weight control standards for semiconductor packaging and EV battery components. Sustainability mandates are accelerating the replacement of metallic and fluorinated lubricants with PFAS-free organic waxes aligned with Green Manufacturing objectives. Export competitiveness remains strong, particularly in LD-OPE waxes, with producers in Ningbo and Shanghai upgrading to automated oxidation reactors to ensure batch-to-batch consistency demanded by global converters.

Germany – Regulatory Leadership, Circular Economy Alignment, and Low-Carbon Wax Portfolios

Germany’s oxidized polyethylene wax market is being reshaped by regulatory leadership and sustainability-driven innovation. In June 2025, BASF SE completed the transition of its specialty polymer additives to a certified mass-balance model, enabling substantial reductions in product carbon footprint across OPE wax lines. This decarbonization push was echoed at the K 2025 trade fair, where Evonik Industries and Clariant showcased next-generation OPE wax emulsions engineered to improve the mechanical performance of recycled polypropylene, directly supporting circular economy plastics.

Regulatory pressure is a central market driver. Germany is at the forefront of the EU REACH Revision 2025, which imposes stricter toxicological and impurity disclosure requirements on synthetic waxes. This is accelerating a shift toward high-purity oxidized wax grades and phasing out legacy formulations. Technological competitiveness is reinforced by Clariant’s EDHOX™ hydrogenation catalysis, recognized in late 2025 for improving energy efficiency along the ethylene chain, thereby lowering the embedded carbon intensity of PE and OPE wax production.

India – Standards Tightening, Domestic Investment, and Medical-Grade Momentum

India’s oxidized polyethylene wax industry is entering a structurally transformative phase driven by regulatory tightening and large-scale petrochemical investments. The Polyethylene Quality Control Amendment Order 2025, issued by the Department of Chemicals and Petrochemicals, has tightened certification requirements for all PE-based imports, including specialty waxes, thereby improving quality discipline and favoring compliant domestic suppliers. Concurrently, Reliance Industries and other majors have announced downstream investments totaling USD 37 billion, which include dedicated units for performance polymer additives that will indirectly expand domestic OPE wax availability.

Industrial policy initiatives are reinforcing long-term capability building. Expansion of the S&T Clusters program to 25 sites in 2025 is supporting indigenous R&D in catalyst systems, including Ziegler–Natta technologies critical for high-density PE used in oxidized wax production. On the demand side, a targeted exemption within the 2025 Quality Control Order for pharmaceutical-grade HDPE is accelerating adoption of medical-grade OPE waxes in syringe moulding and healthcare disposables. This positions India as both a quality-focused domestic market and an emerging regional supplier of compliant specialty waxes.

Comparative Country Snapshot – Oxidized Polyethylene Wax Industry

Oxidized Polyethylene Wax Market County Level Snapshot

|

Country

|

Core Market Driver

|

Policy / Regulatory Lever

|

Strategic Position

|

|

United States

|

Shale-based feedstock and precision additives

|

AIM Act technology transitions

|

High-performance and electronics-driven demand

|

|

China

|

Capacity scale and polyolefin integration

|

MIIT electronic-grade and green manufacturing roadmap

|

Global volume and export anchor

|

|

Germany

|

Sustainability and purity compliance

|

EU REACH Revision 2025

|

Premium, low-carbon specialty wax hub

|

|

India

|

Quality control and petrochemical investment

|

PE Quality Control Order 2025

|

Emerging compliant supplier with medical focus

|

Oxidized Polyethylene Wax Market Report Scope

Oxidized Polyethylene Wax Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$897.6 Million

|

|

Market Size (2034)

|

$1380.6 Million

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Product Type (High-Density Oxidized Polyethylene Wax, Low-Density Oxidized Polyethylene Wax), By Form (Solid, Liquid), By Application (Plastic Processing, Paints and Coatings, Printing Inks, Hot Melt Adhesives, Textile and Leather, Rubber Processing, Paper and Packaging), By End-User Industry (Construction, Automotive, Packaging, Electronics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Honeywell International, Westlake Chemical, Clariant, BASF, Mitsui Chemicals, Evonik Industries, Deurex, Marcus Oil and Chemical, Euroceras, Sanyo Chemical Industries, Nanjing Tianshi New Material Technologies, Qingdao Sainuo New Materials, SCG Chemicals, Innospec, Trecora Chemical

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Oxidized Polyethylene Wax Market Segmentation

By Product Type

- High-Density Oxidized Polyethylene Wax

- Low-Density Oxidized Polyethylene Wax

By Form

By Application

- Plastic Processing

- Paints and Coatings

- Printing Inks

- Hot Melt Adhesives

- Textile and Leather

- Rubber Processing

- Paper and Packaging

By End-User Industry

- Construction

- Automotive

- Packaging

- Electronics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Oxidized Polyethylene Wax Industry

- Honeywell International

- Westlake Chemical

- Clariant

- BASF

- Mitsui Chemicals

- Evonik Industries

- Deurex

- Marcus Oil and Chemical

- Euroceras

- Sanyo Chemical Industries

- Nanjing Tianshi New Material Technologies

- Qingdao Sainuo New Materials

- SCG Chemicals

- Innospec

- Trecora Chemical

*- List not Exhaustive