Panel Filters Market to Surge to $23.2 Billion by 2034 as Demand for Clean Air and Energy-Efficient Systems Intensifies

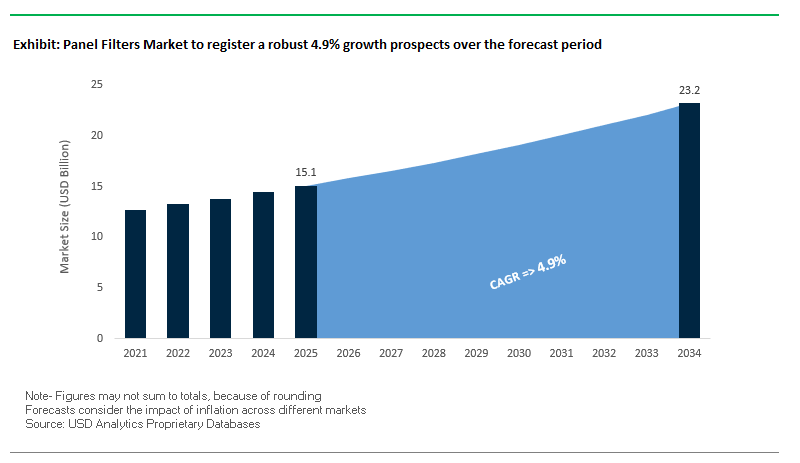

The Global Panel Filters Market is expected to grow from $15.1 billion in 2025 to $23.2 billion by 2034, at a CAGR of 4.9%, driven by rising indoor air quality (IAQ) awareness, industrial expansion, and the adoption of energy-efficient HVAC and filtration systems. Panel filters play a critical role in removing airborne particulates, allergens, and gaseous contaminants, ensuring clean air for residential, commercial, and industrial applications, while protecting sensitive machinery and processes.

Key Insights for Industry Professionals:

- Rising IAQ Concerns: Growing awareness of pollutants, allergens, and airborne pathogens is increasing the demand for high-efficiency panel filters in homes, offices, and healthcare facilities.

- Energy-Efficient Filtration Technologies: Filters with lower pressure drops reduce energy consumption in HVAC systems, supporting sustainability and operational cost savings.

- Critical Process Protection: High-performance filters are essential in cleanrooms, data centers, and food and beverage facilities where product integrity and hygiene are critical.

- Smart Filtration Integration: IoT-enabled systems and real-time sensors allow predictive maintenance and optimized replacement cycles, enhancing operational efficiency.

- Sustainable Materials Adoption: Manufacturers are increasingly focusing on recyclable and low-carbon filter media, aligning with environmental regulations and ESG goals.

Strategic Investments and Technological Innovations Are Accelerating Growth in the Panel Filters Market

The Global Panel Filters Industry continues to evolve rapidly, driven by technological advancements, sustainability initiatives, and strategic acquisitions. In August 2025, Intertape Polymer Group (IPG)’s Chicago facility achieved TRUE Gold Zero Waste Certification, demonstrating leadership in the circular economy and sustainable manufacturing practices. July 2025 marked the completion of the all-stock combination of Amcor and Berry Global, creating a new leader in packaging solutions, indirectly influencing demand for specialized filter-related materials.

In May 2025, Durst Group expanded its digital printing capabilities by acquiring callas software, fostering integration across industrial processes. March 2025 saw Billerud launch a heat-sealable paper that offers a fossil-free, low-carbon alternative to plastic, presenting new opportunities for protective coatings in filtration applications. January 2025 witnessed Ahlstrom introducing MasterTape® Cristal, a recyclable and compostable paper-based tape, highlighting ongoing innovation in sustainable materials.

The industry is also experiencing strategic expansions and market consolidation. In October 2024, Smurfit Kappa completed the acquisition of WestRock, creating a paper and packaging giant impacting end-user applications for wax coatings and filter media substrates. Simultaneously, Donaldson launched its Isolere Bio IsoTag™ AAV reagent, demonstrating diversification into life sciences filtration solutions. Investments in manufacturing infrastructure continue, as seen in Camfil’s March 2024 expansion in Ipoh, Malaysia, to meet growing APAC demand for high-quality air filtration systems.

Trends and Opportunities Transforming the Panel Filters Market

Regulatory Mandates Driving Adoption of Higher Efficiency Ratings (MERV 13+)

The panel filters market is witnessing strong growth driven by stringent regulatory mandates and public health priorities. In the United States, the General Services Administration (GSA) updated its Facilities Standards (P100) to mandate MERV 13 filters in federal buildings, setting a new compliance baseline that influences private sector building design and procurement. Similarly, school air quality initiatives funded through the American Rescue Plan (ARP) have directed billions of dollars toward upgrading ventilation systems, with the CDC and U.S. Department of Education recommending MERV 13 or higher as a standard for schools.

Beyond direct mandates, ASHRAE Standard 62.1 has become a reference point for architects, HVAC designers, and policymakers, encouraging adoption of MERV 13 filters across commercial and institutional buildings. These filters offer at least 50% efficiency in capturing particles between 0.3 and 1.0 microns, according to the U.S. EPA, effectively trapping airborne pathogens, smog, and allergens. With documented benefits such as reduced absenteeism, lower illness rates, and improved cognitive performance, the regulatory shift toward MERV 13+ filters represents both a compliance necessity and a public health-driven performance upgrade for building owners and operators.

Integration of IoT Sensors for Predictive Filter Maintenance

The second transformative trend is the integration of IoT-enabled predictive maintenance in panel filters, moving away from outdated scheduled replacement models. Companies like Johnson Controls are embedding sensors that track pressure drop and airflow resistance, enabling real-time monitoring of filter condition. This ensures filters are replaced only when necessary, avoiding premature changes that waste resources or delayed changes that compromise efficiency.

Case studies highlight significant benefits: one commercial building achieved 34% lower fan energy consumption and reduced labor hours by 80% after implementing smart monitoring systems. Beyond efficiency gains, IoT integration supports holistic indoor air quality (IAQ) management, with multi-sensor platforms monitoring PM2.5, VOCs, CO₂, and humidity levels. These data-driven insights allow building managers to optimize HVAC performance dynamically, making IoT-enabled filters a cornerstone of next-generation smart building strategies.

Development of Anti-Microbial and Self-Sterilizing Filter Media

One of the most promising opportunities lies in anti-microbial and self-sterilizing filter technologies designed to prevent microbial buildup on filter surfaces. Filters in humid environments and healthcare facilities are particularly vulnerable to harboring bacteria, viruses, and fungi. Innovations such as photo-catalytic titanium dioxide (TiO₂) coatings, which break down VOCs and destroy pathogens when exposed to light, are gaining traction as advanced self-sterilizing solutions.

The healthcare sector represents a particularly strong market for this innovation. Hospitals and clinics require higher levels of filtration to minimize the risk of hospital-acquired infections (HAIs), making anti-microbial media a critical differentiator. By preventing the filter itself from becoming a contamination source, self-sterilizing panel filters not only improve air quality but also support safer, more resilient healthcare infrastructure.

Expansion of Sustainable and Recyclable Filter Media

Sustainability is emerging as a major growth driver in the panel filters industry, with increasing emphasis on recyclable and recycled materials. Researchers are experimenting with rPET fibers from post-consumer plastic bottles as high-performance filter media, reducing dependency on virgin plastics while creating a valuable end-use for plastic waste.

Manufacturers are also rethinking end-of-life design. The shift toward mono-material frames—using a single recyclable plastic or paperboard instead of composites—simplifies disassembly and recycling. By creating panel filters that are both high-performance and eco-friendly, companies can align with corporate sustainability goals, regulatory pressure, and consumer demand for greener building products. This opportunity not only reduces environmental impact but also supports circular economy initiatives in the HVAC industry, giving companies a strong competitive advantage.

Competitive Landscape Highlights Innovation, Sustainability, and Custom Solutions in Panel Filters

The Panel Filters Industry is shaped by key players leveraging expertise in filtration technology, materials science, and sustainable manufacturing to deliver high-performance, durable, and energy-efficient solutions. Leading companies differentiate through innovative filter designs, IoT-enabled monitoring, and adherence to strict IAQ standards.

AAF Flanders is Transforming Indoor Air Quality with Advanced Filtration and IoT Monitoring

AAF Flanders offers a comprehensive portfolio of disposable and HEPA panel filters for commercial, industrial, and healthcare applications. In August 2024, it was recognized as Large Enterprise Manufacturer of the Year for its sustainability efforts. The company’s Sensor360® IoT platform enables real-time performance monitoring and predictive maintenance, enhancing energy efficiency and operational reliability. AAF Flanders focuses on delivering innovative, energy-saving filtration solutions while advancing its mission of “Bringing Clean Air to Life.

Camfil is Driving Energy-Efficient Filtration Solutions with Global R&D Excellence

Camfil is renowned for its high-performance air filters, including Hi-Flo bag filters and HEPA solutions, tailored for cleanrooms, life sciences, and industrial processes. In March 2025, its Swedish lab received ISO/IEC 17025:2017 accreditation, validating its rigorous testing standards. In January 2025, Camfil launched TurboPulse T10 filters, improving turbine efficiency and reducing energy degradation. The company emphasizes sustainable raw materials and energy-efficient filter media to support cleaner indoor environments.

Freudenberg Filtration Technologies Leverages Material Science to Deliver High-Performance Panel Filters

Freudenberg Filtration Technologies offers the Viledon product line, including pre-filters for HVAC systems and fine filters for industrial processes. In May 2024, the company installed one of the largest photovoltaic arrays in Shunde, China, reflecting a commitment to renewable energy. Freudenberg focuses on innovative materials and technologies to enhance clean air and water quality, emphasizing sustainability and customer-centric filtration solutions.

Parker Hannifin Corporation Integrates Motion and Control Expertise with Industrial Filtration Solutions

Parker Hannifin provides pleated panel filters and specialty air filtration solutions for industrial and aerospace applications. In June 2025, it acquired Curtis Instruments, strengthening its electrification portfolio, while in April 2025, it increased dividends, reflecting strong shareholder returns. Parker leverages its motion and control expertise to offer filtration solutions that boost efficiency, safety, and operational performance across diverse industries.

Donaldson Company, Inc. Focuses on Technology-Led Filtration with High-Margin Replacement Models

Donaldson delivers panel filters and advanced air, oil, and liquid filtration solutions across industrial, mobile, and life sciences segments. In August 2025, it reported record fiscal year 2025 sales and strong Life Sciences growth, with a 20% increase in food and beverage segment revenue. Donaldson emphasizes a technology-led “razor-and-blade” business model, generating recurring revenue through high-margin replacement parts and consumables, while continuing to innovate in sustainable filtration technologies.

Panel Filters Market Share Insights, 2025-2034

Synthetic and Pleated Media Dominate Market Share by Media Type in the Panel Filters Industry

Synthetic media, primarily polyester and polypropylene, lead the panel filters market with a projected 45% share, driven by their high dust-holding capacity, moisture resistance, and adaptability for electrostatic charging to boost capture efficiency without increasing airflow resistance. This performance profile has made synthetics the default standard across HVAC and industrial applications. Pleated filters, which are largely made from synthetic media, hold the next significant share due to their maximized surface area, longer service life, and higher efficiency ratings (MERV 8–13), aligning with post-pandemic IAQ upgrades in commercial and institutional buildings. Fiberglass, while still present due to its low cost, continues to lose ground as maintenance costs, poor efficiency, and fiber-shedding risks outweigh price advantages. HEPA filters, though a small share by volume, are indispensable in healthcare, pharma, and semiconductor cleanrooms, where their 99.97% efficiency at 0.3 microns is a non-negotiable requirement. Activated carbon filters represent a critical niche for molecular filtration of VOCs, odors, and gases, increasingly relevant in urban environments and specialized industrial processes. The “Others” category, including PTFE membranes and advanced hybrid media, serves highly specialized niches requiring chemical resistance or ultra-high filtration efficiency, underscoring the technological diversification of the market.

HVAC Systems Account for the Largest Market Share by End-Use Industry in the Panel Filters Market

The HVAC sector commands around 50% of the global panel filters market, making it the single largest end-use driver. Demand is amplified by global building stock expansion, regulatory mandates on indoor air quality, and a post-pandemic emphasis on ventilation upgrades to higher MERV-rated systems. Industrial manufacturing follows as a significant segment, spanning paint booths, welding fume extraction, and machinery protection, where high-capacity pleated and synthetic filters are essential for maintaining operational uptime. Automotive represents a dual demand stream, both in manufacturing facilities and in the aftermarket cabin air filter sector, where synthetic filters are indispensable for passenger safety and comfort. Healthcare is a high-value niche, requiring multi-stage systems culminating in HEPA filtration to meet infection control standards in operating rooms and laboratories. The food and beverage industry prioritizes hygienically designed filters to meet FDA and global food safety requirements, while microchip manufacturing demands ultra-pure environments requiring HEPA/ULPA systems at the most advanced levels of technology. Power generation applications add another layer of demand, with large-scale intake filters for turbines prioritizing durability, extreme dust-holding capacity, and reliability. Collectively, HVAC drives volume, while healthcare, semiconductors, and power generation shape specification-driven, high-value growth.

United States Panel Filters Market Driven by EPA Regulations and Smart Filtration Adoption

The United States panel filters market is experiencing robust growth under the influence of stricter regulations from the Environmental Protection Agency (EPA), which has intensified standards for indoor air quality across commercial buildings and industrial facilities. This regulatory landscape is significantly boosting demand for high-efficiency panel filters, particularly in sectors such as healthcare, cleanrooms, and pharmaceuticals, where HEPA-grade filters are required to meet contamination control standards.

Technological advancements are reshaping the market, with the integration of Internet of Things (IoT) sensors into filtration systems enabling real-time air quality monitoring and predictive maintenance. The rise of smart homes is further driving innovation, with residential HVAC panel filters now being developed for mobile app control and monitoring. Additionally, the “Made in America” initiative is spurring domestic production of panel filters, helping companies mitigate tariff-related risks on imported components. With cleanroom expansion, pharmaceutical industry growth, and consumer demand for sustainable, recyclable filter media, the U.S. remains a leading market for advanced and eco-friendly panel filtration technologies.

Germany Panel Filters Market Supported by Automotive, Battery, and Green Building Sectors

The Germany panel filters market is strongly influenced by its world-class automotive sector, which drives significant demand for cabin air filters and paint booth filtration systems. Freudenberg Filtration Technologies, a global leader headquartered in Germany, is spearheading innovations in filtration solutions for new mobility, including hydrogen fuel cell applications, highlighting the country’s focus on next-generation clean technologies.

Germany’s role in the battery manufacturing industry is another critical factor, as clean production environments require ultra-efficient panel filters. The European Union’s green building standards and the German government’s commitment to achieving climate neutrality by 2039 are accelerating the adoption of low-resistance, high-efficiency panel filters that reduce energy consumption. This sustainability-driven approach, combined with strong R&D investment, positions Germany as a leader in developing panel filtration solutions that support both industrial performance and environmental compliance.

China Panel Filters Market Expands with Clean Air Programs and Semiconductor Investments

The China panel filters market is advancing rapidly under the government’s National Clean Air Programme, which aims to significantly reduce particulate pollution nationwide. This policy has triggered strong demand for advanced panel filters across both industrial and residential HVAC applications. The country’s rapid expansion in electronics and semiconductor manufacturing is also fueling the adoption of cleanroom technologies and ULPA-grade filters, ensuring air purity in high-tech production facilities.

Domestic companies such as CleanLink Filtration Tech. are scaling up aggressively, leveraging cost-efficient production and a strong manufacturing base to expand their global competitiveness. At the same time, China’s infrastructure boom—including the construction of new hospitals, data centers, and healthcare facilities—is creating further opportunities for high-efficiency panel filters. With growing investments in automation and AI-driven filtration systems, China is cementing its role as a global hub for large-scale panel filter production and innovation.

India Panel Filters Market Boosted by National Clean Air Programme and Smart Cities Mission

The India panel filters market is witnessing significant momentum due to the National Clean Air Programme (NCAP), which targets pollution reduction across more than 130 cities. This initiative is directly boosting demand for industrial-grade panel filters that can control emissions and safeguard worker health in manufacturing facilities. India’s rapid industrialization and urbanization further amplify the market need for high-performance filtration solutions.

Government-backed infrastructure programs such as the Smart Cities Mission are driving adoption of energy-efficient and technologically advanced filters in urban construction projects. Additionally, the Pradhan Mantri Awas Yojana (PMAY) affordable housing scheme is expanding the residential HVAC market, further increasing demand for cost-effective yet efficient panel filters. With strong regulatory support, rising awareness of indoor air quality, and investments in advanced production capabilities, India’s panel filters industry is aligning itself with both environmental and economic growth objectives.

Japan Panel Filters Market Strengthened by ESG Commitments and Heavy-Duty Applications

The Japan panel filters market is defined by strong innovation from companies like YAMASHIN-FILTER CORP., which is expanding its global footprint with new overseas subsidiaries. Japanese manufacturers are leading in the development of filters that comply with ESG (Environmental, Social, and Governance) standards, with YAMASHIN-FILTER targeting SBT certification as part of its sustainability roadmap.

Demand for panel filters in Japan is robust across the automotive aftermarket and heavy-duty construction machinery, where durability and reliability are critical. Additionally, Japan’s stringent regulations on industrial air quality, particularly in microelectronics and pharmaceutical manufacturing, create a strong need for high-efficiency and precision panel filters. By combining a focus on sustainability with advanced filtration technologies, Japan continues to strengthen its role as a global innovator in panel filters for both industrial and consumer applications.

Panel Filters Market Report Scope

Panel Filters Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$15.1 Billion

|

|

Market Size (2034)

|

$23.2 Billion

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Media Type (Fiberglass, Synthetic, Pleated, Activated Carbon, HEPA, Others), By Frame Material (Cardboard, Metal, Plastic, Other), By Application (Residential, Commercial, Industrial), By End-Use Industry (HVAC, Automotive, Industrial Manufacturing, Power Generation, Healthcare, Food & Beverage, Microchip Manufacturing, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Camfil, MANN+HUMMEL, Donaldson Company, Inc., Freudenberg Filtration Technologies, Parker Hannifin Corporation, American Air Filter (AAF) International, Hengst Filtration, Lydall, Inc., 3M Company, Daikin Industries Ltd., Purafil, Atlas Copco, Filtration Group, Cummins Inc., Clarcor, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Panel Filters Market Segmentation

By Media Type

- Fiberglass

- Synthetic

- Pleated

- Activated Carbon

- HEPA

- Others

By Frame Material

- Cardboard

- Metal

- Plastic

- Other

By Application

- Residential

- Commercial

- Industrial

By End-Use Industry

- HVAC

- Automotive

- Industrial Manufacturing

- Power Generation

- Healthcare

- Food & Beverage

- Microchip Manufacturing

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Panel Filters Market

- Camfil

- MANN+HUMMEL

- Donaldson Company, Inc.

- Freudenberg Filtration Technologies

- Parker Hannifin Corporation

- American Air Filter (AAF) International

- Hengst Filtration

- Lydall, Inc.

- 3M Company

- Daikin Industries Ltd.

- Purafil

- Atlas Copco

- Filtration Group

- Cummins Inc.

- Clarcor, Inc.

* List Not Exhaustive

Methodology

USDAnalytics employs a robust, multi-faceted research methodology to deliver accurate, actionable insights into the global Panel Filters Market. Our approach integrates primary research, including interviews with key stakeholders such as manufacturers, HVAC designers, facility managers, and regulatory bodies, alongside comprehensive secondary research from company reports, industry publications, patent filings, and government regulations. We analyze market dynamics across media types (synthetic, pleated, fiberglass, HEPA, activated carbon, and others), frame materials, applications, and end-use industries, while evaluating trends in energy-efficient HVAC systems, smart IoT-enabled filters, antimicrobial innovations, and sustainable materials adoption. USDAnalytics leverages quantitative modeling to forecast market growth from 2025 to 2034, assess competitive landscapes, and identify emerging opportunities in high-efficiency, recyclable, and IoT-integrated panel filters. Regional insights encompass key markets including the U.S., China, India, Germany, and Japan, considering regulatory mandates, national clean air programs, smart city initiatives, and industrial expansion. By combining qualitative and quantitative analyses, USDAnalytics provides industry professionals with a holistic view of technological advancements, regulatory drivers, and sustainability trends, enabling informed decision-making and strategic investment in the evolving panel filters landscape.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.