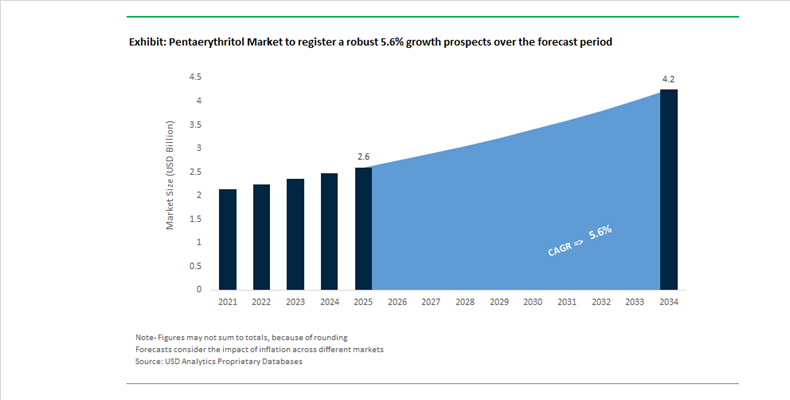

Pentaerythritol Market Size 2025–2034: $2.6 Billion to $4.2 Billion at 5.6% CAGR Amid Supply Tightening and Sustainable Polyol Transition

The global pentaerythritol market is projected to grow from $2.6 billion in 2025 to $4.2 billion by 2034, registering a CAGR of 5.6% over the forecast period. Market expansion is being shaped by tightening supply conditions, strong downstream demand from alkyd resins and synthetic lubricants, and accelerating investment in bio-based polyols for sustainable coatings and plasticizers. Pentaerythritol remains a critical tetrafunctional alcohol used in alkyd resin production, radiation-curable coatings, rosin esters, explosives, and high-performance lubricant esters, positioning it as a core intermediate in specialty chemicals and advanced materials markets.

Supply-demand imbalances became pronounced in December 2025 when Perstorp announced a price adjustment of up to 100% for its global Di-Pentaerythritol portfolio, effective January 2026. The increase was attributed to exceptional demand outpacing global supply, particularly in high-end lubricant and performance coating applications. This marked one of the most significant pricing events in the specialty polyol segment in recent years, signaling structural tightness in high-purity grades. Earlier in August 2025, Hubei Yihua Chemical Industry initiated maintenance shutdowns of its pentaerythritol production lines, followed by a facility parking in November 2025. These actions reduced spot availability in the Asian export market and amplified pricing volatility across merchant channels entering 2026.

Upstream integration and feedstock security are increasingly central to competitive positioning. In September 2024, Kanoria Chemicals & Industries commissioned a 345 MTPD formaldehyde expansion at its Ankleshwar facility, directly strengthening domestic pentaerythritol feedstock availability under its Vision-2030 roadmap. Simultaneously, the company expanded hexamine capacity by 18 MTPD, reinforcing backward integration across phenolic resin and agrochemical derivative chains. This capacity strategy addresses structural supply constraints linked to formaldehyde availability, a primary input in pentaerythritol synthesis.

Corporate restructuring within Europe is reshaping regional asset control. Throughout 2024 and 2025, Ercros became the subject of competing takeover bids from Bondalti Ibérica and Esseco Industrial. In October 2025, Spain’s National Commission on Markets and Competition approved Bondalti’s bid, marking a significant ownership transition for one of Europe’s largest pentaerythritol manufacturing platforms. Concurrently, Ercros reported €41 million in losses in its nine-month 2025 financial results, citing weak European demand and elevated energy costs relative to US and Asian producers. The company extended its 3D Strategic Plan into 2026 to pivot toward higher-margin specialty polyols and mitigate exposure to commodity-grade volatility.

Decarbonization and ESG compliance are materially influencing investment flows. In late 2025, Ercros secured a €14.6 million grant under Spain’s PERTE industrial decarbonization program, allocating funds toward waste energy recovery at its Vila-seca pentaerythritol facility with a targeted 39% CO₂ emissions reduction by 2025–2026. Sustainability-led innovation is also accelerating in renewable ester development. In May 2025, Perstorp showcased Voxtar™, a renewable pentaerythritol platform, at the STLE Annual Meeting, demonstrating biodegradable lubricant formulations with up to 60% lower carbon footprint versus fossil-based alternatives.

Vertical integration strategies are becoming more pronounced in downstream coatings markets. By early 2025, Asian Paints intensified in-house pentaerythritol manufacturing to secure alkyd resin feedstock stability, reducing dependence on volatile global merchant supply. This approach reflects a broader industry shift where paint and resin producers are internalizing key polyol intermediates to manage pricing shocks and ensure supply continuity.

Emery Oleochemicals further reinforced the bio-based transition in December 2025 with the release of its 2024 Sustainability Report, highlighting expanded integration of bio-based esters including pentaerythritol derivatives. The company’s EcoVadis Silver Medal recognition in June 2025 and leadership transition in July 2025 under a renewed ESG strategy underscore the competitive importance of low-carbon polyol supply chains in 2026 contract negotiations.

Strategic Trends and High-Value Opportunities Reshaping the Pentaerythritol Market

Strategic Backward Integration and Capacity Expansion Across Asia-Pacific

The global pentaerythritol market is entering a phase of structural rebalancing as producers respond to persistent volatility in formaldehyde and acetaldehyde feedstocks. Rather than relying on spot procurement and long-distance imports, leading manufacturers are prioritizing backward integration and regional capacity expansion to protect margins, improve supply reliability, and shorten customer lead times. This shift is most pronounced in Asia-Pacific, which has emerged as both the largest consumption base and the most competitive production hub.

A defining milestone was the commissioning of a 40,000-metric-tonne pentaerythritol facility in Sayakha, Gujarat, by Perstorp in February 2024. The site, integrated with calcium formate production, has reduced delivery lead times to Asian customers by roughly 50% and established a template for localized, feedstock-secured manufacturing. In China, regulatory and economic pressures have accelerated consolidation. By 2025, operating rates at large-scale plants average around 82%, while smaller, non-integrated producers continue to exit the market. Integrated players such as Hubei Yihua and Yunnan Yunwei are leveraging coal-to-chemical value chains to maintain cost competitiveness amid rising freight and energy costs.

Supply resilience is also being reinforced by Middle Eastern producers. Data from April 2025 indicates that Saudi Arabian exporters have maintained stable output by anchoring production to domestically integrated methanol feedstocks. Even as global shipping faced an estimated 11% delay rate due to port congestion, integrated Middle Eastern suppliers emerged as a strategic hedge for European and North American buyers seeking diversification away from single-region dependence.

Demand Migration Toward High-Purity and Specialty Pentaerythritol Grades

Alongside capacity realignment, the pentaerythritol market is witnessing a decisive shift in demand toward high-purity mono-pentaerythritol and di-pentaerythritol grades. In these segments, performance requirements outweigh price sensitivity, particularly in applications where thermal stability, hydroxyl functionality, and oxidative resistance directly impact equipment reliability and lifecycle cost.

This imbalance is clearly reflected in pricing dynamics. Effective January 1, 2026, Perstorp announced price increases of up to 100% for its global di-pentaerythritol portfolio, citing sustained demand from high-end synthetic lubricants and radiation-curable coatings. In aviation and industrial refrigeration, high-purity pentaerythritol esters have become the default base oils due to their superior viscosity index and oxidative stability. In these environments, unplanned downtime can exceed USD 10,000 per hour, making lubricant performance a strategic consideration rather than a procurement variable.

Radiation-cured coatings represent another fast-expanding demand center. UV and electron-beam cured systems based on pentaerythritol acrylates offer instant curing, high crosslink density, and zero volatile organic compound emissions. These attributes align closely with tightening environmental mandates under EU REACH and U.S. EPA frameworks, driving adoption across automotive interiors, furniture finishes, and industrial wood coatings. As a result, specialty-grade pentaerythritol is increasingly insulated from the pricing cycles that affect commodity-grade material.

Bio-Based Pentaerythritol Gains Traction in Sustainable Coatings and Resins

One of the most compelling growth opportunities in the pentaerythritol market lies in the commercialization of bio-based and mass-balance-certified grades. As coatings and resin producers face rising pressure to quantify and reduce cradle-to-gate emissions, renewable polyols are transitioning from pilot concepts to commercially accepted solutions.

Renewable pentaerythritol grades such as Voxtar, developed by Perstorp, are available with renewable carbon content ranging from 40% to 100% and carry ISCC PLUS certification. These materials allow formulators to reduce product carbon footprints without altering performance characteristics or reformulating existing systems. Carbon reduction claims of 60 to 80% compared with fossil-based equivalents are increasingly accepted by customers in premium architectural and decorative coatings markets across Europe and North America.

Strategic investment momentum is building, particularly in Asia. In April 2023, LG Chem committed capital toward expanding its portfolio of bio-based polyols, including pentaerythritol, as part of a broader alignment with global ESG benchmarks and the European Green Deal. As regulatory disclosure requirements tighten, bio-based pentaerythritol is emerging as a value-accretive input rather than a cost burden.

Expansion into Halogen-Free Flame Retardant Systems for EVs and Electronics

Electrification and digital infrastructure growth are unlocking a high-margin application space for pentaerythritol in flame retardant systems. As electric vehicles and high-density electronics proliferate, fire safety standards are becoming more stringent, while regulators simultaneously restrict the use of halogenated additives.

Pentaerythritol plays a central role as the carbon source in intumescent flame retardant systems, which are increasingly specified to meet UL 94 V-0 and IEC 62619 safety standards in EV battery enclosures and charging infrastructure. When exposed to heat, pentaerythritol-based formulations promote the formation of an insulating char layer that slows heat transfer and delays thermal runaway. This function is particularly critical in lithium-ion battery modules, where energy density continues to rise.

The transition toward halogen-free flame retardants under RoHS and ECHA guidelines further strengthens this opportunity. Phosphorus–nitrogen IFR systems rely on pentaerythritol to generate the foaming char structure required for effective fire protection. In consumer electronics and data center infrastructure supporting 5G and AI workloads, miniaturization and high thermal loads are driving demand for specialty grades that deliver flame retardancy without emitting toxic gases.

Pentaerythritol Market Share and Segmentation Insights

Mono-Pentaerythritol Leads Global Demand as Core Polyol for Alkyd Resin and Lubricant Ester Production

Mono-pentaerythritol accounted for 68.40% of the Pentaerythritol Market by product type in 2025, reflecting its widespread use as the primary polyol in industrial resin and lubricant synthesis. This grade provides the optimal balance of functionality, availability, and cost efficiency for large-volume applications such as alkyd resin production for paints and coatings and pentaerythritol ester synthesis for synthetic lubricants. Its tetrafunctional alcohol structure enables efficient polymer network formation in coating binders and lubricant additives. In 2025, demand linkage between mono-pentaerythritol and alkyd resin formulation is shaping market consumption, as coating manufacturers develop waterborne alkyds and high-solids coatings that require pentaerythritol with controlled purity and reactivity to achieve targeted viscosity and film performance.

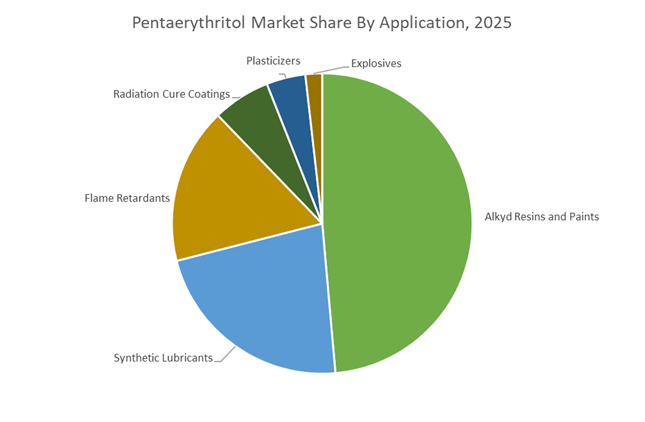

Alkyd Resins and Paints Segment Drives Pentaerythritol Consumption in Global Coatings Manufacturing

Alkyd resins and paints represented 48.60% of the Pentaerythritol Market by application in 2025, making coatings production the dominant outlet for pentaerythritol consumption. The compound serves as a critical polyol building block in alkyd resin synthesis, providing the branching structure necessary for film formation, durability, and adhesion in architectural and industrial coating systems. Global construction activity and industrial manufacturing continue to sustain large-scale demand for alkyd resin binders. In 2025, the transition toward high-solids alkyd coatings with reduced VOC emissions is influencing pentaerythritol specifications, with resin producers requiring optimized polyol functionality to control molecular weight, curing behavior, and viscosity in environmentally compliant coating formulations.

Pentaerythritol Market Competitive Landscape

The Pentaerythritol Market is driven by bio-based polyol innovation, circular feedstock integration, and consolidation across Europe and Asia. Key players are focusing on high-purity mono- and di-pentaerythritol, renewable acetaldehyde/formaldehyde sourcing, and advanced applications in coatings, lubricants, and resins to mitigate fossil feedstock volatility.

Perstorp leads renewable pentaerythritol transition with Voxtar and aggressive pricing strategy

Perstorp Holding AB, backed by PETRONAS Chemicals Group, is a global leader in high-purity pentaerythritol, driving the shift toward renewable polyols. Its Voxtar™ platform offers bio-based pentaerythritol with 60%–80% lower carbon footprint while maintaining identical chemical performance. The company implemented a significant price increase of up to 100% for di-pentaerythritol in 2026, reflecting strong demand and supply tightness. Perstorp’s RE-carbonization strategy emphasizes biogenic and recycled carbon integration into chemical production. It is also targeting high-growth applications such as EV thermal fluids and data center cooling systems using pentaerythritol esters. This combination of sustainability leadership and pricing power reinforces its competitive dominance.

Ercros strengthens high-purity polyol capacity amid takeover activity and European restructuring

Ercros S.A. is maintaining its position in the pentaerythritol market through operational scale and strategic restructuring, despite ongoing takeover activity by Bondalti. Its Tortosa facility is one of the largest integrated production sites globally, with a capacity of 35,000 tons and a 17% expansion in dipentaerythritol output. The company generated €20 million in free cash flow in 2025 while reducing net debt to €125 million, demonstrating financial resilience. Ercros’ 3D Plan focuses on diversification, digitalization, and decarbonization, targeting high-purity grades for intumescent coatings and formaldehyde-free resins. The takeover process signals potential consolidation in the European polyol market. This combination of scale, efficiency, and strategic repositioning strengthens its market role.

Celanese leverages acetyl chain integration to maintain cost leadership in polyol production

Celanese Corporation is reinforcing its position in the pentaerythritol market through deep backward integration across the acetyl chain, ensuring stable supply of acetaldehyde and formaldehyde. The expansion of its Michigan Technology Center enhances R&D capabilities for engineered materials and polyol-derived resins. Despite softer demand in 2025, Celanese generated $773 million in free cash flow and achieved over $120 million in cost reductions. The company optimized its production footprint by prioritizing low-cost U.S. Gulf Coast facilities while reducing exposure to high-cost European operations. With $9.5 billion in revenue, Celanese maintains strong financial flexibility. This integration of cost control, supply security, and innovation strengthens its competitive positioning.

Hubei Yihua dominates global volume with large-scale production and cost-efficient supply chain

Hubei Yihua Chemical Industry Co., Ltd. is the largest global producer of pentaerythritol, holding approximately 30% market share by volume with a capacity of 110,000 tons. Its specialty chemicals segment contributes around 15% of total revenue, supported by exports accounting for 45% of production. The company benefits from a coal-to-chemical cost advantage, enabling a strong gross margin of 28% in this segment. Hubei Yihua controls 70% of the Chinese domestic market and has diversified into high-value derivatives such as TMP and Di-TMP. Its scale and pricing influence make it a key determinant of global market trends. This cost leadership and production dominance position it as a critical market driver.

Yuntianhua advances high-performance polyols for automotive and industrial coating applications

Yunnan Yuntianhua Co., Ltd. is strengthening its presence in the pentaerythritol market by focusing on high-performance applications and industrial integration. The company introduced high-temperature stable lubricant grades in 2025, gaining strong adoption among Asian automotive OEMs. Its expansion in Southeast Asia supports growing demand for mono-pentaerythritol in infrastructure and coatings applications. Yuntianhua’s integration across fertilizer and chemical operations enhances resource efficiency and reduces production costs. Its Pentaerythritol-98 grade remains a key raw material for premium alkyd resins used in marine and architectural coatings. This combination of application focus, regional expansion, and operational synergy strengthens its competitive positioning.

India – From Import Dependency to Export-Oriented Polyol Hub

India has rapidly repositioned itself as a strategic production and export base for pentaerythritol, driven by large-scale capacity commissioning and downstream demand visibility. In February 2024, Perstorp inaugurated its largest Asian investment at Sayakha, Gujarat, establishing a state-of-the-art pentaerythritol facility that structurally shifts India from an import-reliant market to a regional supply hub. The plant has been engineered to reduce delivery lead times for Asian customers by approximately 50%, supported by proximity to western ports and integrated rail logistics. This configuration strengthens India’s competitiveness in supplying both standard Penta Mono and specialty grades to coatings, lubricants, and explosives value chains across Asia and the Middle East.

Sustainability and construction-led demand are reinforcing domestic absorption. The Gujarat site is the first in the region to commercialize Voxtar™, an ISCC PLUS-certified renewable pentaerythritol grade, enabling Indian paints and coatings manufacturers to reduce Scope 3 emissions without altering formulation performance. Parallel to this, the government’s “Housing for All” program, with an estimated US$1.3 trillion investment pipeline over the next six to seven years, is creating a structural uplift in alkyd resin consumption, directly translating into higher pentaerythritol offtake. Backward integration initiatives by Asian Paints in 2025 further underscore the strategic importance of securing domestic polyol supply amid global raw material volatility. New chemical plants are also adopting hybrid power models, blending renewable electricity with grid supply to align with 2030 decarbonization targets.

China – High-Purity Grades and Export Market Rebalancing

China’s pentaerythritol industry is increasingly characterized by asset consolidation, purity upgrades, and export strategy recalibration. In 2025, major conglomerates, including LB Group, intensified acquisitions of international chemical intermediates assets to secure upstream precursors such as formaldehyde and acetaldehyde. This upstream control is critical for stabilizing margins in polyol production. At the same time, Yunnan Yuntianhua Group expanded its portfolio to include high-purity pentaerythritol and polyoxymethylene, targeting automotive and electronics manufacturing clusters in Chongqing and adjacent regions.

Environmental performance and product differentiation are shaping competitiveness. Producers such as Hubei Yihua Chemical reported carbon emission reductions of around 15% by late 2025 through closed-loop catalytic processes. On the product side, Baoding Guoxiu Chemical Industry and Ruiyang Chemical have commercialized Pentaerythritol-98 grades tailored for synthetic lubricants, particularly high-performance EV hydraulic fluids where thermal stability and purity thresholds are stringent. Trade dynamics are also shifting, with Chinese exporters redirecting volumes toward Southeast Asia and the Middle East in response to tariff pressure and demand normalization in Western markets.

Spain – Digitized Polyol Manufacturing and Export Resilience

Spain continues to function as a diversified European polyol hub, anchored by Ercros SA and its integrated complex at Tortosa. The site hosts two pentaerythritol plants and one dipentaerythritol unit with a combined capacity of roughly 310,000 tonnes per year, positioning Spain as one of Europe’s largest producers. In 2025, Ercros advanced its value proposition through the launch of ErcrosGreen+ and ErcrosTech resin ranges, which leverage pentaerythritol to deliver lower environmental footprints and enhanced bonding performance for industrial coatings and adhesives.

Operational efficiency and export orientation underpin Spain’s role. Under its 2025–2029 “3D Plan,” Ercros is fully digitalizing intermediate chemical operations to improve yields and reduce the energy intensity of polyol synthesis. Approximately 56% of production from major Spanish sites is exported to more than 47 countries, reinforcing Spain’s strategic importance as a supplier to both European downstream formulators and Latin American markets seeking stable, high-quality polyol inputs.

United States – Acetyl Chain Security and High-Temperature Applications

The United States market is shaped by feedstock integration and specialty end-use demand rather than capacity-led expansion. Celanese Corporation leverages its global acetyl chain platform to ensure consistent access to acetic acid and intermediates required for pentaerythritol-based ester production. Financial flexibility has been strengthened through a US$1.75 billion revolving credit facility secured in August 2025, providing optionality for selective expansions in specialty materials through 2030.

Sustainability credentials and aerospace demand are key differentiators. Celanese achieved ISCC Carbon Footprint Certification in late 2025 for its ECO-C product grades, aligning pentaerythritol derivatives with circular economy procurement criteria. Concurrently, U.S. demand for di-pentaerythritol accelerated in 2025 due to its application in high-temperature synthetic lubricants for aviation and defense platforms, where thermal stability requirements exceed the capabilities of conventional polyols.

Sweden – Pricing Signals and Global R&D Leadership

Sweden remains the intellectual and strategic center of gravity for high-end pentaerythritol development. Perstorp announced a global price adjustment for its di-pentaerythritol portfolio in December 2025, effective January 2026, citing exceptional demand and tightness in high-purity supply. This pricing move is widely viewed as a leading indicator of sustained structural demand in specialty lubricants, explosives, and performance resins.

Beyond pricing, Swedish operations serve as Perstorp’s primary R&D nucleus for pro-environment polyols. Transition technologies developed at these sites are subsequently transferred to production facilities in the United States and India, reinforcing Sweden’s role as a global innovation anchor rather than a volume production center.

Comparative Snapshot – Pentaerythritol Industry by Country

Pentaerythritol Market County Level Snapshot

|

Country

|

Strategic Role

|

Core Differentiator

|

Structural Impact

|

|

India

|

Export-oriented growth hub

|

New large-scale capacity and renewable grades

|

Reduced Asian lead times, strong construction-led demand

|

|

China

|

High-purity and EV-focused supplier

|

Pentaerythritol-98 and emission-reduction processes

|

Shift toward specialty lubricants and new export corridors

|

|

Spain

|

European polyol backbone

|

Digitalized plants and resin innovation

|

Stable exports across Europe and Latin America

|

|

United States

|

Specialty and defense-driven market

|

Acetyl chain integration and certified low-carbon grades

|

Growth in aerospace and high-performance esters

|

|

Sweden

|

Innovation and pricing benchmark

|

Pro-environment R&D leadership

|

Technology transfer and global price signaling

|

Pentaerythritol Market Report Scope

Pentaerythritol Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.6 Billion

|

|

Market Size (2034)

|

$4.2 Billion

|

|

Market Growth Rate

|

5.6%

|

|

Segments

|

By Product Type (Mono-Pentaerythritol, Di-Pentaerythritol, Tri-Pentaerythritol, Nitrated Pentaerythritol), By Grade (Technical Grade, High-Purity Grade, Bio-Based Grade), By Application (Alkyd Resins and Paints, Synthetic Lubricants, Plasticizers, Flame Retardants, Explosives, Radiation Cure Coatings), By End-Use Industry (Construction and Infrastructure, Automotive and Transportation, Aerospace and Defense, Packaging and Printing, Chemical Manufacturing)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Perstorp Holding, Ercros, Celanese, Hubei Yihua Chemical Industry, Yunnan Yuntianhua, MKS Devre Resins, Kanoria Chemicals and Industries, Samyang Corporation, Mitsui Chemicals, Zarja Chemical, Ruiyang Chemical, Henan Pengcheng Group, Asian Paints, U-PICA, Hebei Chunda Chemical

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Pentaerythritol Market Segmentation

By Product Type

- Mono-Pentaerythritol

- Di-Pentaerythritol

- Tri-Pentaerythritol

- Nitrated Pentaerythritol

By Grade

- Technical Grade

- High-Purity Grade

- Bio-Based Grade

By Application

- Alkyd Resins and Paints

- Synthetic Lubricants

- Plasticizers

- Flame Retardants

- Explosives

- Radiation Cure Coatings

By End-Use Industry

- Construction and Infrastructure

- Automotive and Transportation

- Aerospace and Defense

- Packaging and Printing

- Chemical Manufacturing

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Pentaerythritol Industry

- Perstorp Holding

- Ercros

- Celanese

- Hubei Yihua Chemical Industry

- Yunnan Yuntianhua

- MKS Devre Resins

- Kanoria Chemicals and Industries

- Samyang Corporation

- Mitsui Chemicals

- Zarja Chemical

- Ruiyang Chemical

- Henan Pengcheng Group

- Asian Paints

- U-PICA

- Hebei Chunda Chemical

*- List not Exhaustive