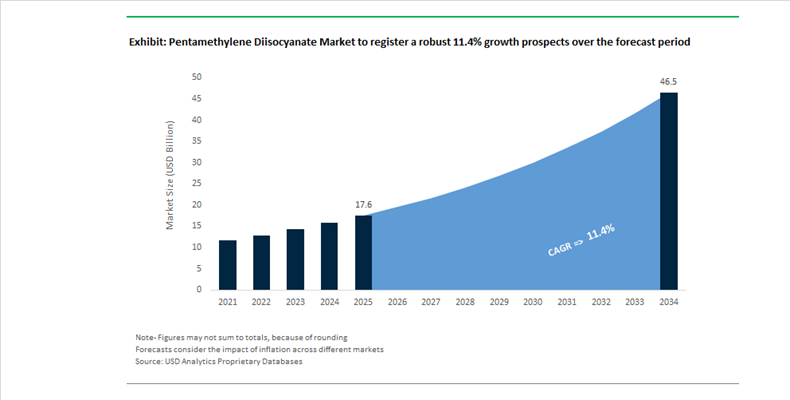

Pentamethylene Diisocyanate Market Size 2025–2034: $17.6 Billion to $46.5 Billion at 11.4% CAGR Driven by Bio-Based Polyurethane Innovation and Specialty Isocyanate Expansion

The global pentamethylene diisocyanate (PDI) market is projected to surge from $17.6 billion in 2025 to $46.5 billion by 2034, registering a compelling CAGR of 11.4%. This accelerated growth trajectory is underpinned by structural shifts toward bio-based aliphatic isocyanates, premium polyurethane coatings, and high-performance adhesives serving automotive, electronics, wood coatings, and sustainable packaging applications. As regulatory frameworks tighten around volatile organic compounds and carbon intensity in polyurethane systems, 1,5-pentamethylene diisocyanate is emerging as a high-value alternative to conventional HDI and MDI in specialty formulations requiring durability, chemical resistance, and lower environmental impact.

Technological validation in 2025 significantly strengthened PDI’s positioning. In July 2025, peer-reviewed research published in Macromolecules and MDPI confirmed that bio-based PDI trimers demonstrate higher reactivity and elevated glass transition temperatures compared to fossil-based HDI systems. The study highlighted improved microhardness and scratch resistance in premium wood coatings, accelerating substitution trends in high-end furniture, flooring, and architectural coatings. In August 2025, Tosoh Corporation reported sluggish global demand for HDI hardeners, increasing competitive pressure on conventional aliphatic isocyanates and indirectly reinforcing market migration toward specialty bio-based PDI solutions that command performance premiums within green chemistry segments.

Corporate expansion and supply chain consolidation are reshaping global isocyanate capacity. In August 2025, Covestro signed an agreement to acquire Vencorex specialty isocyanate production sites in Rayong, Thailand and Freeport, USA, with closing expected by Q1 2026. This transaction significantly strengthens Covestro’s footprint in aliphatic isocyanates across APAC and North America, reinforcing supply resilience for bio-based and specialty PDI derivatives. In January 2026, Covestro introduced the CQ-Configurator, a digital sustainability tool enabling polyurethane formulators to quantify carbon footprint reductions and sustainable material share when integrating bio-based or mass-balanced isocyanates into their systems. This digitalization initiative aligns with procurement requirements in automotive and electronics supply chains, where Scope 3 emissions tracking is becoming mandatory in 2026 contracts.

Mitsui Chemicals is intensifying its “Basic & Green Materials” strategy centered on bio-based polyurethane systems. In May 2025, the company released updated technical documentation for its STABIO™ series, the world’s first bio-based 1,5-PDI platform featuring 71% biomass content. The technology demonstrated superior low-temperature curability and chemical resistance compared to HDI, targeting next-generation automotive coatings and electronic adhesives in 2026. In September 2025 at K 2025 Düsseldorf, Mitsui positioned bio-based PDI as a cornerstone of its European expansion strategy. Parallel upstream restructuring occurred in September 2025 with the formation of Western Japan Ethylene LLP by Asahi Kasei, Mitsui Chemicals, and Mitsubishi Chemical, optimizing feedstock supply chains critical for downstream bio-based diamine and PDI synthesis.

Capacity synergies across polyurethane intermediates are reinforcing integrated strategies. In December 2025, Kumho Mitsui Chemicals announced expansion of MDI capacity at its Yeosu plant to 710,000 tons per year, with construction commencing February 2026. While MDI-focused, this expansion supports hybrid PDI/MDI polyurethane systems for flame-retardant insulation and specialty coatings, creating cross-product leverage within polyurethane raw materials markets.

End-use expansion into electronics and EV interiors is adding new demand vectors. In January 2026 at CES Las Vegas, Covestro showcased “The Material Effect,” highlighting circular, lightweight isocyanate-based films and coatings designed for AI devices, smart homes, and electric vehicle interiors. PDI-derived polyurethane materials were positioned for weight reduction, abrasion resistance, and long-term durability under thermal stress, aligning with automotive electrification trends.

Bio-based polymer integration is expanding into packaging adhesives. In October 2025, Braskem introduced bio-based polyethylene applications at K 2025, increasing demand for PDI-based adhesives capable of bonding mono-material bio-PE layers without compromising renewable certification. Meanwhile, in December 2025, Kiri Industries finalized a $689 million settlement related to DyStar, stabilizing ownership within a key specialty isocyanate-consuming textile value chain and shifting R&D focus toward Asia-based polyurethane innovation.

Strategic Trends and High-Value Opportunities Shaping the Pentamethylene Diisocyanate Market

Strategic Shift Toward Specialized, High-Performance Polyurethane Elastomers

The Pentamethylene Diisocyanate market is undergoing a structural repositioning as polyurethane producers move away from commoditized aromatic systems toward specialized elastomers engineered for durability, stability, and lifecycle performance. PDI is increasingly selected where failure is not an option, particularly in applications exposed to moisture, UV radiation, and thermal cycling. This transition reflects a broader industry pivot toward value density rather than volume growth.

Comparative performance benchmarks indicate that PDI-based elastomers deliver superior hydrolysis resistance and mechanical retention under prolonged stress. According to 2025 disclosures from Covestro, PDI-derived polyisocyanates such as Desmodur CQ N 7300 demonstrate curing speeds and chemical resistance on par with or exceeding conventional HDI-based systems, while enabling up to a 50% reduction in the carbon footprint of the hardener component. This combination of performance and sustainability is increasingly decisive for OEMs operating under ESG-linked procurement mandates.

The aliphatic structure of PDI also eliminates the yellowing and surface embrittlement associated with aromatic MDI systems. This is driving adoption in high-stress rollers, seals, and gaskets used in industrial automation and material handling, where material degradation can trigger unplanned shutdowns costing more than USD 15,000 per hour. Further, research published in mid-2025 highlights that the five-carbon pentamethylene backbone delivers a unique balance of flexibility and toughness, improving low-temperature impact resistance. This property is particularly relevant for aerospace components and cold-region logistics, where elastomer brittleness has historically constrained material selection.

Consolidation of Production Capacity and Technical Expertise

The PDI market remains structurally constrained by high technical, regulatory, and capital barriers, resulting in a concentrated competitive landscape dominated by a small group of technology leaders. Unlike conventional diisocyanates, PDI synthesis relies on advanced bioconversion routes to pentamethylene diamine, followed by highly controlled phosgenation or alternative chemistries. This complexity limits new entry and reinforces the strategic value of proprietary process know-how.

Global leadership in PDI production is anchored by companies with integrated bio-based platforms. Mitsui Chemicals and Covestro have secured durable competitive advantages through proprietary fermentation technologies that convert renewable feedstocks such as corn and cassava into PDI intermediates. This bio-based integration effectively decouples supply from petrochemical volatility, improving margin stability and long-term cost visibility.

Regulatory dynamics further entrench incumbents. Under EU REACH requirements, mandatory training and certification for diisocyanate handling introduced between 2023 and 2025 have raised compliance thresholds for downstream users. Established suppliers now increasingly offer low-monomer, ready-to-use PDI prepolymers with monomer content below 0.1%, enabling customers to meet occupational safety standards without major capital upgrades. In Asia-Pacific, new capacity announcements are concentrated within backward-integrated chemical parks. Chinese producers are embedding PDI units into existing starch and molasses processing hubs, leveraging bio-feedstock synergies while accepting high upfront capital expenditure in exchange for long-term cost leadership.

Non-Yellowing PDI Systems for Electric Vehicles and Urban Infrastructure

A key growth opportunity for the PDI market lies in its expanding role within high-performance coatings for electric vehicles and public infrastructure. As urban environments demand longer-lasting aesthetics and reduced maintenance cycles, coating systems are being evaluated on total lifecycle cost rather than upfront price. PDI-based polyurethanes are well positioned to meet these requirements.

Automotive OEMs are increasingly specifying clearcoats that retain gloss, color, and scratch resistance over service lives exceeding ten years. PDI-based coatings offer superior weatherability and resistance to thermal cycling, making them suitable for EV exterior plastics and battery enclosures that experience wider temperature swings than traditional steel components. In parallel, infrastructure modernization programs are prioritizing ultra-durable coatings for bridges, facades, and transport assets. PDI enables waterborne and high-solids polyurethane systems that lower VOC emissions while maintaining corrosion resistance in coastal and high-salinity environments.

Beyond automotive and infrastructure, PDI is gaining traction in synthetic leather and coated textiles. These applications value the softer hand-feel, improved breathability, and non-yellowing behavior of aliphatic systems. For luxury consumer goods and premium interiors, PDI-derived resins align with demand for vegan, high-performance, and carbon-reduced materials without sacrificing durability.

High-Value Penetration into Medical Devices and Biocompatible Applications

The most structurally attractive opportunity for PDI lies in medical and healthcare applications, where material safety and long-term biocompatibility are paramount. Unlike aromatic diisocyanates, aliphatic PDI-based polyurethanes degrade into non-toxic byproducts, avoiding the release of carcinogenic aromatic amines. Clinical evaluations conducted between 2024 and 2025 have reinforced the suitability of PDI-based systems for prolonged human contact.

This safety profile is accelerating adoption in catheters, wound dressings, tubing, and orthopedic components, where regulatory scrutiny is intense and failure risks are unacceptable. The rise of wearable medical technology further strengthens this opportunity. Flexible sensors and skin-contact devices require elastomers that are non-sensitizing, mechanically resilient, and capable of withstanding repeated sterilization cycles using autoclave, gamma irradiation, or ethylene oxide. PDI-based elastomers meet these criteria while maintaining comfort and flexibility.

Demand is also emerging for ultra-high-purity PDI grades tailored for diagnostics and electronics within healthcare settings. These specialty materials minimize ionic leaching, supporting the reliability of microelectronic housings and point-of-care diagnostic equipment. As healthcare systems continue to invest in decentralized diagnostics and wearable monitoring, PDI’s role as a premium, enabling material is expected to expand steadily, reinforcing its position as a high-value niche within the global diisocyanates landscape.

Pentamethylene Diisocyanate Market Share and Segmentation Insights

Pentamethylene Diisocyanate Monomer Leads Bio-Based Polyurethane Raw Material Demand

Pentamethylene diisocyanate accounted for 52.80% of the Pentamethylene Diisocyanate Market by type in 2025, establishing it as the primary bio-based isocyanate used in polyurethane manufacturing. Produced from pentamethylenediamine derived through lysine fermentation, PDI offers a renewable alternative to conventional petrochemical isocyanates while maintaining comparable reactivity and polymerization performance. The compound is widely used in polyurethane coatings, adhesives, elastomers, and specialty materials where durability and chemical resistance are required. In 2025, bio-based isocyanate positioning within sustainable polymer markets is strengthening adoption, as polyurethane manufacturers incorporate PDI to deliver products with verified renewable carbon content while maintaining performance characteristics expected from traditional polyurethane systems.

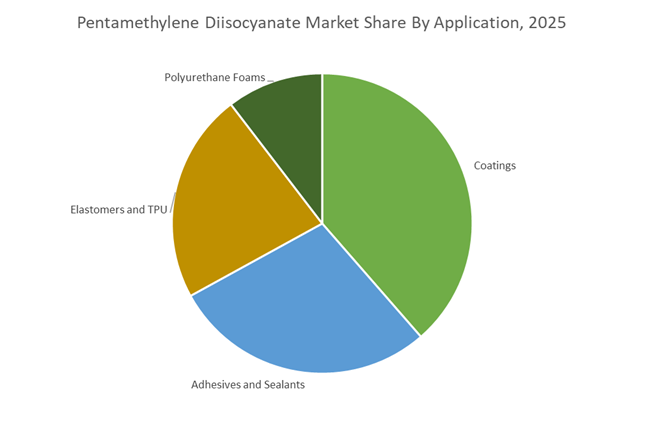

Coatings Applications Drive Pentamethylene Diisocyanate Demand in High-Durability Polyurethane Systems

Coatings represented 38.60% of the Pentamethylene Diisocyanate Market by application in 2025, reflecting the extensive use of PDI-based polyurethane binders in high-performance coating systems. Polyurethane coatings formulated with PDI deliver strong mechanical durability, weather resistance, and chemical stability required in automotive finishes, industrial coatings, and wood protection applications. Demand for advanced coating technologies continues to expand across automotive manufacturing, construction materials, and protective surface treatments. In 2025, the market trend toward high-performance and sustainable coating formulations is supporting increased use of PDI-based polyurethane chemistry, enabling coating manufacturers to combine long service life with renewable raw material content in premium coating products.

Pentamethylene Diisocyanate Market Competitive Landscape

The Pentamethylene Diisocyanate (PDI) Market is transitioning toward bio-based isocyanates, mass balance certification, and circular polyurethane chemistry. Competitive intensity is driven by low-carbon alternatives to HDI/IPDI, strategic acquisitions, and high-performance applications in automotive coatings, construction, and advanced elastomers.

Covestro accelerates bio-based PDI adoption with Desmodur eco N and global asset expansion

Covestro AG leads the PDI market through bio-based polyurethane innovation and circular economy integration. Its Desmodur® eco N 7300, with 70% renewable carbon content, has emerged as a benchmark low-carbon PDI solution for coatings and adhesives. The 2025 acquisition of Vencorex assets in the U.S. and Thailand strengthened its regional supply chain for aliphatic isocyanates. In March 2026, Covestro implemented a +$220/ton price increase, reinforcing a cost-anchored pricing strategy amid volatile feedstock markets. The company’s mass balance approach enables seamless integration of renewable raw materials into existing production infrastructure. This combination of sustainability leadership, pricing discipline, and global footprint secures Covestro’s dominant market position.

Mitsui Chemicals drives AI-enabled innovation and decarbonized isocyanate value chains

Mitsui Chemicals is strengthening its leadership in high-performance PDI through its STABIO™ portfolio and advanced materials strategy. The expansion of Kumho Mitsui Chemicals’ Yeosu facility will increase isocyanate capacity to 710,000 tons/year by 2027, targeting automotive and insulation applications. Its AI-driven R&D platform is accelerating the development of thermally stable PDI elastomers for EV battery systems. A strategic decarbonization agreement with Asahi Kasei and Mitsubishi Chemical ensures low-carbon ethylene feedstock integration. Mitsui is also advancing bio-polyurethane adoption through partnerships in consumer packaging. This convergence of AI innovation, capacity expansion, and circular chemistry positions Mitsui as a technology leader.

Wanhua Chemical reshapes global PDI supply through Vencorex acquisition and масштаб expansion

Wanhua Chemical Group has redefined the competitive landscape through its acquisition of Vencorex, adding 70,000 tons/year of HDI/PDI capacity and establishing a strong European presence. Its Fujian expansion project will raise total isocyanate capacity to 5.94 million tons, enabling unmatched economies of scale. The company has allocated 6.49 billion yuan toward polyurethane innovation and performance-driven product upgrades. Wanhua is targeting 40% international revenue contribution by 2026, leveraging EU-facing assets to meet Green Deal compliance. Its transition from volume-led growth to specialty chemical value creation marks a strategic inflection point. This scale combined with global expansion cements Wanhua’s influence over pricing and supply dynamics.

Tosoh leverages chlor-alkali integration to ensure cost-efficient and stable isocyanate supply

Tosoh Corporation maintains a strong position in the PDI market through vertical integration and advanced materials innovation. With FY2025 net sales of ¥1,063.4 billion, the company continues to invest in high-margin eco-products and specialty polymers. Its chlor-alkali integration provides a stable and cost-efficient supply of isocyanate precursors, enhancing competitiveness in Asia. Recent R&D breakthroughs in polymer electrolytes are being cross-applied to PDI-based membranes for fuel cell technologies. Tosoh’s share buyback program reflects strong liquidity and disciplined capital allocation. This integration of upstream control and innovation ensures long-term resilience in the evolving PDI landscape.

Evonik focuses on specialty additives and low-VOC PDI systems for high-performance applications

Evonik Industries AG is positioning itself as a specialty leader in PDI through its Advanced Technologies segment. With an adjusted EBITDA of €1.87 billion in 2025, the company continues to prioritize high-margin additives and crosslinkers for sustainable polyurethane systems. Demand for low-VOC coatings and specialty elastomers remains a key growth driver, particularly in healthcare and wearable technologies. Evonik is advancing PDI-based materials for PVC-free flooring and medical-grade applications, aligning with global regulatory trends. Its shift toward ROCE-driven capital allocation and dividend linkage underscores a performance-focused strategy. This emphasis on specialty applications and sustainability strengthens Evonik’s niche market leadership.

Japan – Bio-Based PDI as a Commercial and Export-Led Growth Engine

Japan has emerged as the global reference point for the commercialization of bio-based pentamethylene diisocyanate, driven by early-scale deployment and downstream adoption. As of May 2025, Mitsui Chemicals accelerated worldwide distribution of its STABiO™ PDI series, with verified biomass content of 71%. This development directly supports Japanese automotive and electronics OEMs in meeting 2030 Scope 3 emission targets without compromising polyurethane performance. Beyond volume scaling, Mitsui Chemicals’ May 2025 portfolio reorganization, splitting its Basic & Green Materials business, structurally prioritizes green polyurethanes and positions PDI alongside bio-based polyols such as ECONYKOL™ as core export products.

Application-led innovation is reinforcing demand depth. In December 2025, a partnership between Chugoku Marine Paints and Mitsui Chemicals resulted in the selection of a PDI-derived bio-based coating system for a liquefied ammonia tanker scheduled for delivery in 2026, representing the first industrial-scale maritime use of bio-based isocyanates. Concurrently, mid-2025 performance data shows PDI-based hardeners achieving curing temperatures roughly 35% lower than HDI systems, delivering tangible energy savings in automotive refinish operations. Japanese electronics manufacturers have also integrated PDI into Optical Clear Adhesives for wearable devices, leveraging its superior transparency and solvent resistance for next-generation consumer electronics.

Germany – Strategic Integration of PDI into Sustainable Isocyanate Portfolios

Germany’s role in the PDI industry is defined by portfolio integration and regulatory alignment rather than standalone capacity expansion. Under its “Sustainable Future” strategy, Covestro has embedded PDI into its global Solutions & Specialties segment, supported by a €300 million investment plan targeting bio-based aliphatic isocyanates for coatings and adhesives. A leadership realignment in July 2025 reinforced this strategic direction, even as operational resilience was tested by a temporary power-related disruption at the Dormagen site.

Beyond coatings, German chemical majors are exploring high-purity PDI for advanced patterning materials in semiconductor manufacturing, particularly for sub-2nm nodes where molecular stability and low outgassing are critical. Regulatory drivers further reinforce this trajectory. German producers have aligned 2026 roadmaps with the EU Sustainable Chemicals Strategy, positioning PDI as a preferred alternative to petroleum-derived hexamethylene diisocyanate. This alignment supports both compliance and differentiation in low-VOC, next-generation industrial coatings.

India – Policy-Driven Foundations for Domestic PDI Ecosystem

India’s PDI landscape is still emerging, but policy frameworks introduced in 2025 are laying the groundwork for domestic synthesis and derivative manufacturing. The launch of the BioE3 Policy has introduced targeted financial incentives for high-performance biomanufacturing, explicitly naming bio-based chemicals as priority sectors. This has been complemented by allocations of ₹858 crores under the National Bioenergy Programme through March 2026, catalyzing R&D and pilot-scale production of PDI precursors such as 1,5-pentanediamine derived from agricultural residues.

Structural synergies are accelerating readiness. The advancement of the national E20 ethanol blending target to 2025–2026 has expanded bio-refinery infrastructure, which is now being leveraged to supply biomass feedstocks for future PDI synthesis. Customs duty reductions on imported bio-production machinery announced in the 2025 Union Budget have further lowered capital barriers for establishing PDI derivative plants, positioning India as a medium-term manufacturing and formulation hub for Asia-Pacific markets.

Thailand – APAC Platform for Aliphatic Isocyanates

Thailand is being positioned as a regional manufacturing anchor for aliphatic isocyanates through cross-border asset realignment. In August 2025, Covestro signed an agreement with Vencorex Holding to acquire standalone production assets in Rayong, with closure expected in Q1 2026. This move strategically relocates key isocyanate capabilities closer to high-growth Southeast Asian automotive and textile markets.

The acquisition is designed to integrate with Thailand’s broader petrochemical ecosystem, particularly PTT Global Chemical, enabling a closed-loop supply chain for bio-based isocyanates. This configuration supports regional customers seeking lower-carbon polyurethane solutions while reducing dependence on long-distance imports from Europe.

China – High-Purity PDI and Policy-Led Demand Creation

China’s PDI development is characterized by upstream purity enhancement and policy-driven downstream demand. During 2024–2025, Gansu Yinguang Juyin Chemical optimized its phosgene-route synthesis, achieving PDI purity levels exceeding 99.8%. Such high-purity feedstocks are essential for producing low-viscosity PDI trimers used in EV coatings and sealants, where flow properties and consistency directly impact manufacturing yields.

Demand-side momentum is being reinforced by regulation. Under China’s updated 2025 Plastic Pollution Control Plan, public construction projects are mandated to adopt bio-based polymers, directly increasing the uptake of PDI-based coatings, sealants, and elastomers. This combination of upstream quality control and downstream policy enforcement is rapidly embedding PDI into China’s green construction and electric mobility value chains.

Comparative Snapshot – Pentamethylene Diisocyanate by Country

Pentamethylene Diisocyanate Market County Level Snapshot

|

Country

|

Strategic Role

|

Primary Driver

|

Market Impact

|

|

Japan

|

Global commercialization leader

|

Bio-based PDI scaling and export focus

|

Benchmark for green isocyanate adoption

|

|

Germany

|

Portfolio and regulatory anchor

|

EU sustainability strategy alignment

|

Replacement of fossil-based HDI systems

|

|

India

|

Emerging manufacturing base

|

BioE3 policy and ethanol infrastructure

|

Foundation for domestic PDI synthesis

|

|

Thailand

|

APAC production hub

|

Asset acquisition and regional integration

|

Localized supply for SE Asia

|

|

China

|

High-purity supplier and demand hub

|

Policy-led bio-based construction

|

Rapid adoption in EV and public projects

|

Pentamethylene Diisocyanate Market Report Scope

Pentamethylene Diisocyanate Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$17.6 Billion

|

|

Market Size (2034)

|

$46.5 Billion

|

|

Market Growth Rate

|

11.4%

|

|

Segments

|

By Type (Pentamethylene Diisocyanate, PDI Derivatives, Modified PDI), By Application (Coatings, Adhesives and Sealants, Elastomers and TPU, Polyurethane Foams), By End-Use Industry (Automotive and Transportation, Building and Construction, Electronics and Electrical, Furniture and Bedding, Packaging and Textile)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Mitsui Chemicals, Covestro, Vencorex, Bayer, Gansu Yinguang Juyin Chemical, Wanhua Chemical Group, Asahi Kasei, Tosoh, BASF, Evonik Industries, Perstorp Holding, Kumho Mitsui Chemicals

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Pentamethylene Diisocyanate Market Segmentation

By Type

- Pentamethylene Diisocyanate

- PDI Derivatives

- Modified PDI

By Application

- Coatings

- Adhesives and Sealants

- Elastomers and TPU

- Polyurethane Foams

By End-Use Industry

- Automotive and Transportation

- Building and Construction

- Electronics and Electrical

- Furniture and Bedding

- Packaging and Textile

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Pentamethylene Diisocyanate Industry

- Mitsui Chemicals

- Covestro

- Vencorex

- Bayer

- Gansu Yinguang Juyin Chemical

- Wanhua Chemical Group

- Asahi Kasei

- Tosoh

- BASF

- Evonik Industries

- Perstorp Holding

- Kumho Mitsui Chemicals

*- List not Exhaustive