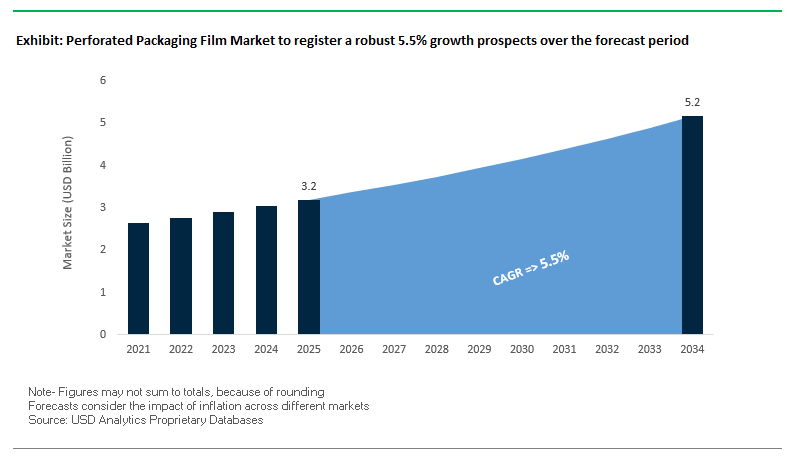

Perforated Packaging Film Market Overview: Shelf-Life Extension via Precision Venting (MV: USD 3.2 Bn in 2025 → USD 5.2 Bn by 2034, CAGR 5.5%)

The global perforated packaging film market—covering micro-perforated and macro-perforated films across BOPP, BOPET, PE and PP—underpins modern fresh produce and bakery packaging by tuning gas exchange and MVTR to product respiration. Precisely engineered holes (often via laser perforation) slow spoilage, mitigate condensation, and preserve visual appeal, directly reducing food waste and markdowns for retailers. Demand is amplified by consumers’ pivot to fresh, minimally processed foods, while brands seek anti-fog clarity, printable surfaces, and recycle-ready mono-material constructions that comply with evolving circularity goals.

Professionals evaluating perforated films today focus on three outcomes: (1) shelf-life extension for produce, bread, and chilled meals; (2) brand and category lift from clear, anti-fog visibility at shelf; and (3) sustainability via lighter gauges, mono-PE/PP designs, PCR content, and downgauging without loss of barrier integrity. With MV USD 3.2 billion (2025) scaling to USD 5.2 billion by 2034 (CAGR 5.5%), investments are flowing into laser systems, high-barrier coatings, and recyclable structures, positioning perforated films as a critical lever in food-waste reduction strategies.

Key insights for buyers & operators

- Respiration-matched packs cut shrink: Micro-perfs balance O₂/CO₂ to slow senescence in fruits/veg; macro-perfs vent moisture for bakery.

- Laser perforation = repeatable QA: Hole diameter and density can be tailored by SKU, crop, season, and lane speed.

- Retail impact: Anti-fog, high-clarity films improve product signaling and conversion while enabling variable messaging and codes.

- Circularity momentum: Mono-material PE/PP lidding & flow-wrap plus PCR content support EPR/PPWR trajectories.

Market Analysis: Technology, Sustainability, and Consolidation Accelerate Adoption

The 2024–2025 period shows a tight linkage between sustainable materials and precision venting. In August 2025, ProAmpac spotlighted ProActive Recyclable RP-1050 at FACHPACK, underscoring demand for recycle-ready films that can still accept micro-perforation without compromising machinability. Also in August 2025, Amcor (with a yogurt partner) launched the first all-PE spouted pouch, signaling a broader mono-PE shift relevant to perforated and breathable pack designs. KM Packaging’s July 2025 lidding film range prioritized recyclability assessments, aligning respiration control with end-of-life claims. Earlier, February 2025, UFlex introduced 3D bags with perforation to couple convenience and venting, while in September 2024 Specialty Polyfilms emphasized micro-perforated solutions for produce at a major floral/produce forum, and UFlex Flex Films launched F-UHB-M high-barrier BOPET (September 2024) to replace foil in certain flexible applications.

Beyond films, the ecosystem is pivoting. April 2025, Storopack’s PAPERplus Classic CX paper cushioning launch reflects the parallel rise of fiber-based, recyclable components within the same perishables value chain. November 2024 saw ProAmpac showcase ProActive Recyclable FibreSculpt—another data point in cross-material “paperization,” even as converters keep perforated plastics for respiration-critical SKUs. Net-net: market leaders are harmonizing laser-perfed PE/PP, anti-fog coatings, and high-barrier monomaterial platforms, while qualifying for retailer recyclability schemes and tightening OEE with faster line speeds and consistent hole density.

Trends and Opportunities Transforming the Perforated Packaging Film Market

Adoption of Laser Perforation for Precision-Modified Atmosphere Packaging (MAP)

The perforated packaging film market is witnessing a rapid shift from mechanical to laser perforation as food manufacturers and retailers prioritize precision and shelf-life optimization. Laser systems are capable of creating micro-perforations as small as 5 micrometers, offering unprecedented control over oxygen transmission rates (OTR). This level of precision enables packaging to be calibrated to the specific respiration rate of products such as fresh fruits, vegetables, and bakery items, significantly extending shelf life and reducing spoilage. Studies show that laser-perforated films can extend the freshness of broccoli and berries by several days, a critical advantage in global food supply chains where waste reduction is directly tied to profitability.

Beyond functionality, laser perforation also improves packaging integrity and aesthetics. Unlike mechanical punching, laser perforation is a non-contact process that eliminates risks of tearing or stretching the film. The result is a clean, volcano-shaped hole that maintains packaging safety and strength. Additionally, laser technology enables the integration of design features such as tear lines and laser-cut windows, which improve consumer convenience while enhancing brand differentiation. With demand for modified atmosphere packaging (MAP) surging across fresh produce, bakery, and ready-to-eat segments, laser-perforated films are fast becoming a cornerstone of next-generation sustainable packaging.

Development of Bio-Based and Compostable Perforated Films

As sustainability becomes a non-negotiable requirement in packaging, manufacturers are investing heavily in bio-based and compostable perforated films. Driven by regulatory frameworks such as the EU’s Packaging and Packaging Waste Regulation (PPWR), the market is shifting toward compostable solutions that minimize environmental impact while delivering reliable performance. Materials like polylactic acid (PLA) and next-generation biopolymer blends are increasingly being commercialized as substitutes for conventional plastics. These films, certified for industrial composting, are designed to meet both regulatory compliance and consumer demand for eco-friendly packaging.

Importantly, technological advancements have addressed the performance issues of early bio-films. Modern compostable perforated films now deliver excellent breathability, moisture management, and transparency, making them suitable for high-demand applications such as fresh produce and baked goods packaging. For retailers and foodservice companies, adopting bio-based perforated films provides a dual advantage: compliance with tightening sustainability mandates and the ability to meet consumer preferences for environmentally responsible packaging. This positions bio-based perforated films as one of the fastest-growing product segments in the market.

Integration of Responsive/Smart Perforations

A transformative opportunity in the perforated packaging film market lies in the development of responsive or “smart” perforations. Instead of maintaining a static oxygen transmission rate, researchers are exploring films that dynamically adjust their permeability based on environmental factors such as temperature or the buildup of ethylene gas. This innovation can actively manage the internal atmosphere of a package, extending shelf life further and adapting to product aging in real time.

Beyond permeability, smart perforated films are also being integrated with freshness indicators. Academic research has demonstrated the potential of intelligent films embedded with natural colorants, such as red cabbage extract or curcumin, which change color when spoilage occurs. This dual-function approach not only preserves product quality but also provides consumers with a visible indicator of freshness, boosting confidence in perishable products. As demand grows for active packaging systems that go beyond passive protection, responsive perforations represent a cutting-edge growth avenue with wide applications in both food and pharmaceutical supply chains.

Digital Printing Integration for Perforation-Labeling Combinations

Another emerging opportunity lies in combining perforation with digital printing technologies to streamline production and enhance consumer engagement. The flat surface of perforated films provides an ideal canvas for high-resolution branding, variable data printing, and functional features such as QR codes. By integrating perforation and printing into a single production run, manufacturers can eliminate the need for separate labeling processes, reducing costs, optimizing inventory management, and improving supply chain efficiency.

From a consumer perspective, digital printing on perforated films unlocks powerful engagement tools. QR codes can provide instant access to product origin, freshness, handling instructions, or recycling information. This not only enhances transparency but also strengthens brand trust and loyalty. For manufacturers of high-value products such as fresh produce, baked goods, or medical supplies, the ability to combine protective functionality with interactive branding elevates the role of perforated films from a commodity material to a premium, value-added packaging solution.

Competitive Landscape: Specialists Scaling Laser-Perfed, Mono-Material, and Anti-Fog Platforms

A concentrated set of converters and film producers compete on laser-perforation accuracy, barrier tuning, sustainability claims, and global converting capacity. Below is a focused view of leading strategies.

Amcor plc Scaling monomaterial, recycle-ready perforated films

Amcor leverages a global materials science organization to deliver perforated and micro-perforated film families for produce, meat, and bakery, integrating easy-open, anti-fog, and high-barrier options. Its all-PE spouted pouch (Aug 2025) illustrates the company’s pathway to mono-material performance—a foundation for perforated PE flow-wraps and lidding where recyclability is prioritized. Strategic programs target the goal of 100% recyclable or reusable packaging, with R&D focused on laser pattern control, shelf-life modeling, and consistent sealing at commercial speeds.

Mondi Group Dual track in paper & plastics for breathable packs

Mondi’s edge is its hybrid portfolio (paper and plastics), advising customers on best-fit sustainability while meeting respiration needs via perforated and laser-perforated films. The launch of FunctionalBarrier Paper Ultimate signals serious intent to replace conventional films where possible, while retaining perforated plastic for moisture- and gas-critical SKUs. Under MAP2030, Mondi designs “sustainable-by-design” packs, balancing clarity, anti-fog, and machinability with mono-material PE/PP pathways to recyclability.

Sealed Air Corporation Fresh-food leaders with Cryovac® micro-perfs

Sealed Air’s Cryovac® portfolio is synonymous with fresh-food shelf-life extension. The company engineers micro-perforated structures to match crop respiration curves and anti-fog optics for premium display. Current programs emphasize recycle-ready PET/PE architectures and durability under cold-chain stress, with R&D targeting barrier-perforation balance (maintaining clarity and seal integrity at high line speeds) to cut retailer shrink and food waste.

UFlex Ltd. Integrated film-to-pack innovation with convenience features

UFlex’s vertically integrated model (films to finished packs) speeds translation of R&D into commercial SKUs. The 3D bags with perforation (Feb 2025) combine easy-tear convenience with breathability—useful for bakery and snacks needing controlled venting. Parallel launches such as patented high-barrier BOPET (F-UHB-M, Sep 2024) broaden the toolset for foil-replacement laminates that can accommodate targeted perforation patterns while pursuing “green path” initiatives in PCR and waste-to-energy.

Jindal Poly Films Ltd. Capacity, cost leadership, and high-barrier breadth

Jindal Poly Films brings scale in BOPP/BOPET with metallized, transparent, and high-barrier grades that can be laser-perforated for produce and bakery. Recent capacity and technology investments focus on consistent hole geometry at speed, sealability, and anti-fog compatibility—key to maintaining pack integrity post-perforation. The company’s cost-effective manufacturing and global footprint position it well for retailer programs standardizing on recycle-ready, breathable mono-structures.

Perforated Packaging Film Market Share Insights, 2025-2034

Micro-perforation dominates Market Share by Perforation Technology in Perforated Packaging Films

Micro-perforation holds 40% of perforation-technology share because it is the enabling process for modified atmosphere packaging (MAP) that precisely matches O₂/CO₂ exchange to the respiration profile of fresh produce and fresh-cut meals, materially extending shelf life and reducing shrink without inducing anaerobic conditions. Macro-perforation (25%) remains essential for bulk produce (potatoes, onions) where high ventilation and condensation control trump gas-mix precision, delivering high-speed, cost-effective runs for agricultural supply chains. Laser perforation is the fastest-growing technology: non-contact drilling, on-the-fly hole density control, micron-level uniformity, and zero tool wear deliver tight permeability windows tailored to SKUs (e.g., strawberries vs. broccoli), supporting premium retailers and brands focused on freshness KPIs and food-waste reduction. Mechanical punching sustains a role in heavy-duty films where larger apertures suffice and rugged uptime matters; hot-needle systems continue a legacy presence but lose share on precision limits and film embrittlement. Water-jet perforation serves a small but critical niche for complex multilayer structures where thermal/mechanical stress would risk delamination. The technology mix mirrors customer priorities—predictable permeability, hygienic processing, and high-throughput convertibility—with lasers redefining the capex-to-OEE equation for high-value MAP programs.

Fresh Produce commands Market Share by Application in Perforated Packaging Films, with Bakery a moisture-management stronghold

Fresh produce accounts for 50% of application share, reflecting the outsized impact of tailored permeability on respiring fruits, vegetables, and herbs; SKU-specific micro-perforation patterns are now a core lever for retailers to extend shelf life, protect visual quality, and cut waste across cold-chain nodes. Bakery & confectionery (20%) leverages perforated films to balance crust crispness and crumb moisture, preventing condensation without over-drying—critical for in-store bakeries and short shelf-life premium items. Ready-to-eat salads and produce-forward meals are a rapid-growth use case, increasingly pairing zoned packaging (perforated produce compartments plus high-barrier sections for proteins/dressings) to optimize safety and sensory performance. Meat & poultry employs selective micro-perforation alongside MAP strategies to maintain color and mitigate off-odors in case-ready formats, while dairy & cheese uses tightly controlled micro-perfs to vent maturing gases and prevent package swelling without compromising hygiene. In pet food and other niches, macro-perfs aid odor/fat vapor release and specialty horticulture (e.g., fresh flowers) benefits from ethylene and moisture management. Overall, share concentration in fresh produce highlights how precision gas exchange, food-waste reduction, and retail presentation drive specification, while adjacent categories adopt perforation to solve moisture, aroma, and safety challenges within integrated MAP ecosystems.

United States Perforated Packaging Film Market Driven by Sustainability and Intelligent Packaging

The United States perforated packaging film market is evolving rapidly, supported by innovation in materials and strong regulatory pressure for sustainable packaging. Companies like Amcor plc are investing heavily in recyclable portfolios such as the AmPrima® recycle-ready films, which cater to consumer and corporate demand for sustainable, high-performance packaging. Similarly, ProAmpac’s AdaptMAP system uses precision laser perforation technology to regulate respiration in fresh foods, a crucial factor for extending shelf life and minimizing food waste.

The U.S. market is also witnessing significant momentum in co-extruded multilayer films, which provide the ideal balance of barrier protection and breathability with fewer raw materials. New frontiers in intelligent packaging, including sensor-enabled perforated films for real-time freshness monitoring, are gaining traction, particularly in e-commerce and long-haul food distribution. The U.S. EPA’s push for compostable and recyclable solutions, coupled with the rising importance of automation in packaging lines, is making perforated films indispensable for the food, logistics, and fresh produce industries.

China Perforated Packaging Film Market Strengthened by E-Commerce Growth and Advanced Production

The China perforated packaging film market is experiencing strong expansion due to large-scale investments and the explosive growth of online grocery delivery. Amcor’s USD 100 million flexible packaging plant in Huizhou stands as a milestone, integrating automated smart production lines with laser scanners and real-time quality control, positioning China as a leader in large-scale perforated packaging production.

Technological advancements in precision laser perforation are optimizing gas transmission rates (OTR), directly benefiting the preservation of fruits, vegetables, and ready-to-eat meals. The country’s growing urban workforce and preference for convenience foods are driving demand for micro-perforated packaging, especially in meal kits and takeaway services. Additionally, the proliferation of supermarkets and e-commerce grocery platforms underscores the need for durable polypropylene (PP) perforated films, which are rapidly emerging as the material of choice for scalable, cost-effective solutions.

Germany Perforated Packaging Film Market Focused on Biodegradable Materials and Advanced Laser Systems

The Germany perforated packaging film market is being shaped by EU directives on single-use plastics and sustainability mandates. German manufacturers are at the forefront of replacing traditional needle perforation with laser-based systems, ensuring consistent gas exchange rates and higher efficiency. There is also a strong move toward Polyethylene Terephthalate (PET) films, valued for their clarity, recyclability, and barrier properties, which align with EU circular economy goals.

The country is also a leader in developing compostable and biodegradable perforated films, meeting consumer expectations and regulatory requirements for eco-friendly packaging. Applications in fresh produce, meat, and bakery sectors are growing, as German companies innovate with lidding films and multi-layer structures to improve shelf life and reduce plastic dependency. This positions Germany as a hub for sustainable perforated film innovation in Europe.

United Kingdom Perforated Packaging Film Market Driven by Recycling Policies and Customized Perforation Technologies

The United Kingdom perforated packaging film market is being reshaped by both regulation and innovation. The Flexible Plastic Fund’s 2025 report and the mandate for local authority collection of flexible plastics by March 2027 are strong regulatory drivers for recyclable solutions. KM Packaging’s sustainable lidding film portfolio and Protos Packaging’s multi-pattern perforation technology—including micro and macro options like P1, P8, and P360—highlight the UK’s commitment to customized and recyclable film designs.

Consumer demand for eco-friendly packaging for fresh foods and perishables is fueling innovation, with companies like Mars introducing recyclable mono-material retort pouches for pet food. The strong e-commerce and retail packaging sector in the UK is ensuring steady adoption of recyclable perforated films, while government tax incentives on non-recycled plastics are further accelerating this shift.

Japan Perforated Packaging Film Market Supported by Health-Conscious Consumers and Vertical Farming Trends

The Japan perforated packaging film market is characterized by a unique blend of health-conscious consumer behavior and a growing demand for packaging that extends food freshness. The aging population and preference for nutrient-rich, portion-controlled meals have created a steady market for advanced perforated films that optimize food preservation.

The rise of vertical farming and micro-portion packaging is a niche yet growing trend, requiring specialized breathable films to maintain product quality. Japan’s strong e-commerce and home delivery culture is driving the adoption of protective, breathable perforated packaging for fresh and frozen foods. Manufacturers are focusing on advanced food preservation technologies, with an emphasis on minimizing waste, enhancing convenience, and catering to the country’s premium-quality packaging standards.

India Perforated Packaging Film Market Expanding with High-Capacity Manufacturing and Fresh Food Demand

The India perforated packaging film market is rapidly expanding, driven by its booming food processing, e-commerce, and logistics sectors. Uflex Limited’s Flexfresh™ Modified Atmosphere Packaging (MAP), which uses nano-perforation to extend freshness, has positioned the company as a leader in the sustainable packaging segment. Similarly, Jindal Poly Films operates one of the world’s largest single-location BOPP and BoPET plants, producing recyclable mono-material solutions at scale. Cosmo Films adds to India’s competitive strength with extensive specialty film exports across more than 100 countries.

Urbanization and rising disposable incomes are fueling demand for ready-to-eat, bakery, and fresh produce packaging, where perforated films are essential for shelf-life extension. The country’s e-commerce boom requires durable yet lightweight packaging that safeguards goods in transit. India is also emerging as a global export hub for specialty perforated films, thanks to high production capacities and government initiatives supporting sustainable and domestic manufacturing under the Make in India program.

France Perforated Packaging Film Market Transitioning to Biodegradable and AI-Driven Perforation Technologies

The France perforated packaging film market is transitioning strongly towards eco-friendly and compliant solutions, spurred by EU Regulation 2025/40, which mandates recycled content in plastic food packs. French companies are adopting thinner-gauge films that minimize resin use while maintaining barrier properties, reducing both costs and environmental impact.

Innovation is also being fueled by AI-driven laser perforation systems, which allow dynamic adjustment of oxygen transmission rates (OTR) for different products, improving efficiency and reducing food waste. The market is seeing significant growth in biodegradable solutions such as PLA-based perforated films, which provide compostable alternatives with performance parity to plastics. With the rise of e-commerce grocery delivery services, demand for protective and breathable films is increasing, reinforcing France’s role as a European hub for sustainable perforated film technologies.

Perforated Packaging Film Market Report Scope

Perforated Packaging Film Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.2 Billion

|

|

Market Size (2034)

|

$5.2 Billion

|

|

Market Growth Rate

|

5.5%

|

|

Segments

|

By Material (PE, PP, PET, Others), By Perforation Technology (Macro, Micro, Laser, Hot Needle, Mechanical Punching, Water Jet), By Application (Fresh Produce, Bakery & Confectionery, Ready-to-Eat Meals, Meat & Poultry, Dairy & Cheese, Pet Food, Others), By Product Type (Bags & Pouches, Rolls & Wraps, Sheets & Trays, Lidding Films)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Sealed Air Corporation, Constantia Flexibles, Uflex Limited, Bolloré Packaging Films, A·ROO Company, KM Packaging Services Ltd., TCL Packaging Ltd, ProAmpac, Toray Industries, Berry Global, Inc., Innovia Films, Cosmo Films, Jindal Poly Films

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Perforated Packaging Film Market Segmentation

By Material

By Perforation Technology

- Macro

- Micro

- Laser

- Hot Needle

- Mechanical Punching

- Water Jet

By Application

- Fresh Produce

- Bakery & Confectionery

- Ready-to-Eat Meals

- Meat & Poultry

- Dairy & Cheese

- Pet Food

- Others

By Product Type

- Bags & Pouches

- Rolls & Wraps

- Sheets & Trays

- Lidding Films

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Perforated Packaging Film Market

- Amcor plc

- Mondi Group

- Sealed Air Corporation

- Constantia Flexibles

- Uflex Limited

- Bolloré Packaging Films

- A·ROO Company

- KM Packaging Services Ltd.

- TCL Packaging Ltd

- ProAmpac

- Toray Industries

- Berry Global, Inc.

- Innovia Films

- Cosmo Films

- Jindal Poly Films

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive and data-driven approach to analyze the global Perforated Packaging Film Market, combining primary research through interviews with key stakeholders—including packaging manufacturers, converters, retailers, and end-users—with extensive secondary research encompassing company reports, industry journals, patent filings, regulatory guidelines, and sustainability initiatives. Our methodology emphasizes quantitative modeling of market value (MV), compound annual growth rates (CAGR), product segmentation, regional dynamics, and material adoption trends. By integrating insights from technology adoption, laser and mechanical perforation innovations, and precision-modified atmosphere packaging (MAP) applications, USDAnalytics delivers actionable intelligence on supply chain, regulatory compliance, and sustainability trajectories. Advanced analytics are applied to assess the competitive landscape, identify emerging opportunities in micro- and macro-perforation technologies, and evaluate the impact of digital printing, bio-based films, and smart perforations on shelf-life extension, food-waste reduction, and retailer adoption. Our study ensures data reliability through triangulation across multiple sources, while offering industry professionals nuanced foresight into market shifts, technological advancements, and regulatory drivers shaping perforated packaging film demand globally.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.