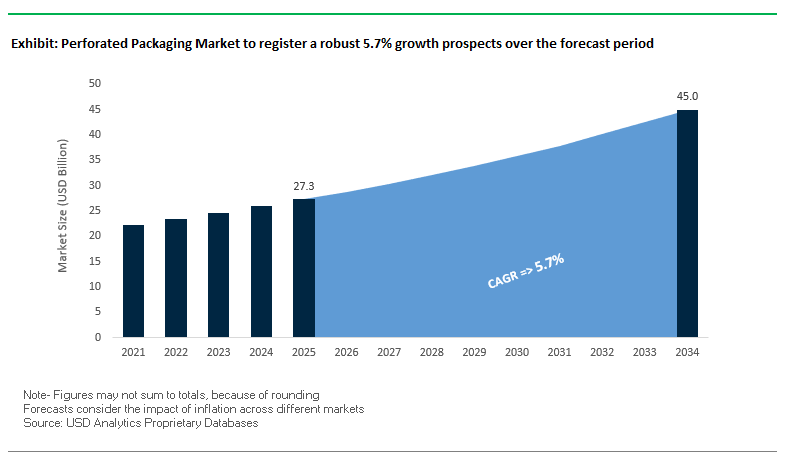

Market Overview: Perforated Packaging Market Set to Reach $45 Billion by 2034 at a CAGR of 5.7% Driven by Fresh Food Demand

The Global Perforated Packaging Market is a critical segment of flexible packaging, providing films with micro and macro-perforations that regulate gas exchange and moisture transmission. These packaging solutions are essential for maintaining the freshness of perishable goods such as fruits, vegetables, bakery products, and ready-to-eat meals. The market is propelled by increasing consumer demand for fresh, minimally processed foods, alongside the growing imperative to reduce food waste across retail and supply chains.

Key Insights for industry professionals and buyers:

- Market Growth Dynamics: The market is expected to expand from $27.3 billion in 2025 to $45 billion by 2034, reflecting a CAGR of 5.7%.

- Primary Drivers: Demand from fresh produce and bakery sectors, where controlled respiration and condensation prevention are crucial.

- Innovation in Material Science: Adoption of advanced laser perforation technology enables precise, product-specific gas exchange control.

- Sustainability Trends: Recyclable and monomaterial packaging is gaining prominence in response to environmental regulations.

- Enhanced Visibility and Branding: Anti-fog, transparent films allow consumers to assess product quality, driving purchase decisions.

- Supply Chain Efficiency: Extended shelf life minimizes product losses and improves logistical efficiency.

- Market Differentiation: High-barrier films and customized perforations provide brand-specific protection and premium presentation.

Market Analysis: Technological Innovations and Strategic Moves Shaping the Perforated Packaging Market

The perforated packaging industry is witnessing rapid advancements in sustainability, material innovation, and global expansion. In August 2025, Amcor collaborated with a yogurt manufacturer to launch the first all-polyethylene (PE) spouted pouch, enhancing recyclability while maintaining product performance. During the same month, ProAmpac unveiled ProActive Recyclable RP-1050 at FACHPACK 2024 in Germany, signaling a strong focus on eco-friendly, recyclable films.

In July 2025, KM Packaging introduced a new lidding film range designed to meet sustainability and recyclability targets, while April 2025 saw Storopack launching its PAPERplus Classic CX paper cushioning system, reflecting the broader packaging industry's pivot toward sustainable alternatives. February 2025 witnessed UFlex launching 3D perforated bags to enhance consumer convenience and functional packaging performance.

Late 2024 developments further underline market momentum. In November 2024, ProAmpac showcased ProActive Recyclable FibreSculpt at FACHPACK 2024, highlighting fiber-based ready-made food solutions. In October 2024, Amcor invested $100 million to open China’s largest flexible packaging plant, strengthening its position in Asia Pacific. In September 2024, Specialty Polyfilms presented micro-perforated films at a major produce and floral show, while UFlex launched the patented BOPET high-barrier film F-UHB-M, designed to replace aluminum foil in flexible packaging applications.

Trends and Opportunities Reshaping the Perforated Packaging Market

Major Retailers Mandating Perforated Packaging for Produce to Reduce Plastic Waste

The perforated packaging market is being strongly influenced by retailer-driven sustainability commitments. Leading global retail chains are mandating the use of perforated films to cut plastic waste, extend product freshness, and reduce in-store spoilage. In the United Kingdom, Tesco has introduced micro-perforated films for pre-packed bakery items, while major U.S. retailers such as Walmart and Whole Foods are implementing similar solutions for pre-cut fruits, salads, and fresh produce. These initiatives are a direct response to rising consumer demand for sustainable packaging formats that both reduce plastic use and minimize food waste.

Legislation is reinforcing this shift, particularly in Europe, where Extended Producer Responsibility (EPR) schemes are increasing the financial accountability of retailers for packaging waste. By adopting perforated films with extended shelf-life functionality, retailers can significantly reduce spoilage, which in turn lowers their EPR compliance costs. Case studies highlight the effectiveness of these solutions: PerfoTec’s laser micro-perforated bags have been shown to extend spinach freshness for up to 21 days and keep bananas fresh for three weeks, directly addressing one of the most pressing challenges in retail supply chains—food waste reduction. With sustainability, cost efficiency, and compliance converging, perforated packaging has become an essential component of retailer sustainability strategies.

Investment in Advanced Laser Perforation Technology for Modified Atmosphere Packaging (MAP)

Capital investment in advanced laser perforation systems is accelerating as packaging converters seek precision control to meet the demands of modified atmosphere packaging (MAP). Unlike mechanical perforation methods, which can damage film integrity, modern laser perforation is a non-contact process capable of producing clean, controlled holes as small as 40 micrometers. This micron-level accuracy enables films to deliver optimal oxygen transmission rates (OTR) that are tailored to the respiration rate of specific products, significantly extending shelf life while ensuring product safety.

Beyond fruits and vegetables, the application of laser-perforated MAP films is expanding to high-value categories such as meat and bakery products. In fresh protein packaging, controlled perforation technology helps prevent discoloration and microbial contamination by regulating moisture and gas levels, ensuring product integrity across complex cold-chain supply networks. In bakery, precision perforation ensures ideal moisture retention while preventing staleness, enhancing product quality on shelves. The ability to deliver both food safety and sustainability benefits positions advanced laser perforation technology as a cornerstone of future-ready food packaging strategies.

Development of Perforated Solutions for E-commerce Fresh and Frozen Food Delivery

The rapid growth of online grocery and direct-to-consumer food services is opening new opportunities for specialized perforated packaging films designed for e-commerce applications. Unlike retail packaging, e-commerce packaging must endure the rigors of transportation, including temperature fluctuations and handling stress, while maintaining freshness. Perforated bags and films tailored for frozen vegetables, fresh-cut salads, and ready-to-eat items provide the necessary breathability and protection, ensuring optimal product quality upon delivery.

Consumer convenience is also a critical growth driver in this segment. Perforated films with easy-open features such as laser-scored tear lines or pre-engineered opening mechanisms simplify the unboxing process, creating a better end-user experience. Since packaging is the first physical touchpoint for e-commerce grocery consumers, enhancing usability directly contributes to brand loyalty. By combining protective functionality with consumer-friendly features, perforated films for e-commerce are expected to become a vital growth area, particularly in urban markets where online grocery penetration is rising rapidly.

Engineering Perforated Films for Home-Compostable and Sustainable Material Substrates

Sustainability remains a defining opportunity, with innovation focused on developing perforated films from bio-based and compostable substrates. Traditional films like OPP (oriented polypropylene) are incompatible with home composting standards, pushing companies to engineer alternatives from PLA, starch-based polymers, and cellulose derivatives. However, designing functional compostable films with perforations presents technical challenges, as higher base permeability can diminish the effectiveness of perforation for modified atmosphere control.

Collaboration is emerging as a key pathway to address these hurdles. For instance, Domino Printing Sciences partnered with Futamura to test the compatibility of laser perforation with NatureFlex compostable films. Results confirmed that laser coding and perforation could be applied without compromising compostability or film performance, marking a breakthrough in scaling home-compostable perforated packaging. The ultimate goal is to achieve certifications that guarantee biodegradability in home composting environments, providing consumers with end-of-life solutions that do not rely on industrial infrastructure. By addressing material, performance, and regulatory challenges, compostable perforated films have the potential to redefine flexible packaging sustainability standards.

Competitive Landscape: Leading Players Are Driving Innovation, Sustainability, and Global Expansion in Perforated Packaging

The competitive landscape of the perforated packaging market is defined by companies that leverage material science expertise, advanced manufacturing, and sustainable product innovation. These players focus on creating high-performance films that extend product shelf life, reduce food waste, and cater to evolving consumer expectations.

Amcor plc: Expanding Global Leadership with Sustainable and Monomaterial Packaging

Amcor is a global leader in flexible and rigid packaging with a robust manufacturing network and expertise in material science. The company recently collaborated with a yogurt manufacturer to launch the first all-polyethylene (PE) spouted pouch and, in October 2024, opened China’s largest flexible packaging plant with a $100 million investment. Amcor’s offerings include perforated films for fresh produce, meat, and baked goods, featuring high-barrier properties. The company aims to make all packaging recyclable or reusable by 2025, reflecting its strategic commitment to circular economy solutions.

Mondi Group: Combining Paper and Plastic Expertise for High-Barrier Sustainable Packaging

Mondi excels in providing both paper-based and plastic-based packaging solutions. Its recent launch of FunctionalBarrier Paper Ultimate and acquisition of Schumacher Packaging’s Western European operations in August 2025 emphasize eco-friendly, high-barrier alternatives. Mondi offers a variety of perforated and laser-perforated flexible films for fresh food, pet food, and industrial applications. Its MAP2030 strategy focuses on circular-driven solutions, climate action, and sustainable product design.

Sealed Air Corporation: Enhancing Food Freshness and Supply Chain Efficiency

Sealed Air specializes in high-performance flexible films, including its Cryovac® brand, engineered for fresh produce, meat, and poultry. In August 2025, the company reported a 4% quarter-to-quarter increase in Protective segment sales and appointed a new CFO, Kristen Actis-Grande. Sealed Air’s strategic focus is on sustainable packaging aligned with circular economy principles, enhancing food safety and reducing waste while improving supply chain efficiency.

UFlex Ltd.: Innovating Consumer-Friendly and Environmentally Responsible Flexible Packaging

UFlex leverages a vertically integrated model with strong R&D capabilities. Its recent launches include 3D perforated bags offering an “easy-tear” experience and a patented BOPET high-barrier film to replace aluminum foil. UFlex provides BOPP and BOPET films with various perforation options for food, personal care, and industrial applications. Sustainability is central to its strategy, with initiatives for recycling post-consumer waste and minimizing environmental impact.

Jindal Poly Films Ltd.: Expanding Production and Technology for Global Market Leadership

Jindal Poly Films is a major Indian manufacturer of BOPP and BOPET films with a growing international presence. The company is investing in technology upgrades and capacity expansion to meet rising demand. Its flexible films include high-barrier, metallized, and transparent options for diverse packaging applications. Strategic priorities focus on innovation, production expansion, and strengthening market leadership globally.

Perforated Packaging Market Share Insights, 2025-2034

Fresh Produce Leads Market Share by Application in the Perforated Packaging Industry

Fresh produce accounts for 48% of the perforated packaging market, making it the undisputed leader due to its critical reliance on modified atmosphere packaging (MAP) for shelf-life extension, freshness preservation, and waste reduction. Micro-perforation technologies are specifically engineered to match the respiration rates of fruits, vegetables, and herbs, enabling precise oxygen and carbon dioxide exchange that prevents anaerobic conditions. Retailers and food brands rely on this application as a frontline strategy against shrink and spoilage, especially in high-volume supply chains where even minor improvements in shelf life translate into significant cost savings. Beyond fruits and vegetables, perforated films have become essential for herb packs, salad bags, and fresh-cut produce, creating an advanced packaging ecosystem that balances permeability, product visibility, and consumer appeal. This dominance is further strengthened by global regulatory and retail mandates focused on food waste reduction, ensuring fresh produce remains the anchor application for perforated packaging.

Bakery & Confectionery Retains High Market Share with Moisture-Optimized Packaging

Bakery and confectionery products hold 22% of the perforated packaging market, underscoring their dependence on packaging that manages moisture release and retention simultaneously. Freshly baked goods release steam that, if trapped, can cause sogginess, while insufficient moisture control accelerates staling. Perforated packaging delivers the fine balance required to maintain crispy crusts in breads and pastries while preserving softness in cakes and muffins, extending shelf appeal in retail and foodservice environments. In-store bakeries, convenience stores, and artisanal brands increasingly depend on perforated bags and wraps to minimize product loss while maintaining the sensory attributes that define quality. This segment’s share is further reinforced by the growing consumer demand for fresh, unpackaged-look presentation combined with hygienic protection, driving the adoption of custom-perforated pouches and lidding films.

United States Perforated Packaging Market Driven by Sustainable Innovation and Smart Films

The United States perforated packaging market is being transformed by sustainability initiatives, advanced film technologies, and the booming e-commerce sector. Leading players such as Amcor plc and ProAmpac are pioneering laser perforation systems designed to extend shelf life for fresh produce, dairy, and perishable goods. ProAmpac’s AdaptMAP shelf-life extension technology leverages precision perforation patterns to balance respiration in packaged foods, addressing a critical demand for freshness in cross-border shipping and long-haul distribution.

There is a notable shift toward co-extruded multilayer films, which reduce raw material usage while enhancing barrier and breathability properties. Alongside this, digital printing and sensor-enabled films are being deployed for real-time freshness monitoring, positioning the U.S. as a hub for intelligent packaging innovation. Consumer and regulatory demand for eco-friendly packaging continues to drive adoption of recyclable and compostable perforated films, with Amcor’s AmPrima® recycle-ready range setting industry benchmarks. The market is heavily fueled by the food, beverage, and online retail industries, all seeking long-lasting, sustainable perforated solutions to cut food waste and enhance supply chain efficiency.

China Perforated Packaging Market Strengthened by E-Commerce and Automation Investments

The China perforated packaging market is expanding rapidly, supported by government policies, e-commerce growth, and large-scale investments. Amcor’s USD 100 million investment in Huizhou established the country’s first fully automated packaging production line, integrating laser scanners and advanced quality control systems. This move highlights the country’s growing dominance in smart packaging production for both domestic and global markets.

Technological advancements in precision laser perforation are optimizing gas transmission rates (OTR) to extend the shelf life of fruits, vegetables, and ready-to-eat meals—critical for the fast-growing online grocery and takeaway sectors. The increasing urban workforce and rising demand for convenience foods are accelerating the adoption of micro-perforated films. Additionally, the market is experiencing a strong pivot toward polypropylene (PP) perforated films, which are gaining traction for their versatility and recyclability. Local manufacturers are focusing on high-volume, cost-effective, and sustainable solutions, reinforcing China’s role as a global supplier of perforated films.

Germany Perforated Packaging Market Leading in Biodegradable Solutions and Laser Precision

The Germany perforated packaging market is defined by regulatory compliance, material innovation, and advanced processing technologies. German manufacturers are moving from traditional needle perforation to laser systems, which ensure uniform gas transmission rates and enhance packaging performance for fresh foods. The country is also pioneering the use of Polyethylene Terephthalate (PET) for its oxygen barrier properties and recyclability, aligning with EU sustainability goals.

Germany is actively responding to the EU Single-Use Plastics Directive and the Packaging and Packaging Waste Regulation (PPWR) by introducing compostable and biodegradable perforated films. The food sector, particularly in fresh produce, meat, and bakery products, is driving this transition. Moreover, German companies are innovating in lidding films and multi-layer packaging formats to combine convenience, extended shelf life, and reduced environmental impact. With a strong focus on circular economy practices, Germany stands as a leader in sustainable perforated packaging technologies.

United Kingdom Perforated Packaging Market Supported by Flexible Plastic Fund and Customization Technologies

The United Kingdom perforated packaging market is advancing due to regulatory incentives and cutting-edge technology adoption. KM Packaging’s launch of sustainable lidding films and Protos Packaging’s multi-pattern perforation technology—featuring custom hole designs like P1, P8, P30, P160, and P360—demonstrates the country’s expertise in tailor-made perforated solutions. The UK government’s mandate for flexible plastics collection by 2027, as well as insights from the Flexible Plastic Fund’s 2025 report, are creating a strong demand for recyclable mono-material films.

Consumer preferences for eco-friendly packaging are reinforcing this trend, particularly in the fresh produce and perishable goods sectors. Major FMCG brands such as Mars are already shifting to recyclable mono-material perforated pouches for pet food, balancing sustainability with shelf life. The UK’s strong e-commerce and grocery delivery ecosystem continues to push adoption of high-performance perforated films, making it one of the most dynamic markets in Europe.

Japan Perforated Packaging Market Driven by Health-Conscious Consumers and Food Preservation Technologies

The Japan perforated packaging market is witnessing growth fueled by health-conscious consumers, an aging population, and a strong emphasis on food freshness. Manufacturers are focusing on advanced preservation technologies to minimize waste while catering to the country’s demand for premium-quality food packaging.

Emerging applications such as vertical farm micro-portion produce packaging highlight a trend toward specialized perforated solutions. The expansion of e-commerce and home delivery services is further boosting demand for breathable films that can withstand transit while protecting perishable products. Japan’s packaging sector is characterized by precision, sustainability, and convenience, reinforcing the use of perforated films across ready-to-eat meals, fresh produce, and premium retail packaging.

India Perforated Packaging Market Expanding with Flexfresh™ MAP and Global Export Capacity

The India perforated packaging market is undergoing rapid expansion, led by high-capacity domestic manufacturers and the surging consumption of fresh produce and ready-to-eat foods. Uflex Limited’s Flexfresh™ MAP (Modified Atmosphere Packaging), which leverages nano-perforation to significantly reduce product loss, has become a cornerstone of the market. Jindal Poly Films, with one of the world’s largest BOPP and BoPET plants in Nashik, demonstrates India’s ability to scale production for both domestic and international demand. Cosmo Films, another key player, supplies specialty perforated films to over 100 countries, cementing India’s position as a global export hub.

Urbanization, rising disposable incomes, and the e-commerce boom are driving demand for robust perforated films that maintain food quality during storage and delivery. Domestic manufacturers are also investing in mono-material and recyclable solutions to align with sustainability regulations and global customer preferences. India’s strong manufacturing capacity and export-oriented ecosystem make it a pivotal market for perforated packaging films.

France Perforated Packaging Market Embracing Biodegradable Films and AI-Driven Laser Technology

The France perforated packaging market is shaped by strict sustainability regulations and advanced technological innovation. EU Regulation 2025/40, which compels the use of recycled content in food packaging, is driving demand for thinner-gauge perforated films that minimize resin use while maintaining oxygen transmission rates. French companies are leveraging AI-driven laser perforation to dynamically adjust perforation patterns and optimize shelf life across diverse food categories.

There is a strong shift toward biodegradable perforated films, including PLA-based solutions that match the performance of conventional plastics while being fully compostable. The rapid growth of e-commerce grocery delivery in France further accelerates demand for breathable packaging formats that preserve food quality during transit. By combining sustainability compliance with advanced technology, France is positioning itself as a leading hub for eco-friendly perforated packaging innovation in Europe.

Perforated Packaging Market Report Scope

Perforated Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$27.3 Billion

|

|

Market Size (2034)

|

$45 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Material (PE, PP, PET, Others), By Perforation Technology (Macro, Micro, Laser, Hot Needle, Mechanical Punching, Water Jet), By Application (Fresh Produce, Bakery & Confectionery, Ready-to-Eat Meals, Meat & Poultry, Dairy & Cheese, Pet Food, Others), By Product Type (Bags & Pouches, Rolls & Wraps, Sheets & Trays, Lidding Films)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Amcor plc, Mondi Group, Sealed Air Corporation, Constantia Flexibles, Uflex Limited, Bolloré Packaging Films, A·ROO Company, KM Packaging Services Ltd., TCL Packaging Ltd, ProAmpac, Toray Industries, Berry Global, Inc., Innovia Films, Cosmo Films, Jindal Poly Films

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Perforated Packaging Market Segmentation

By Material

By Perforation Technology

- Macro

- Micro

- Laser

- Hot Needle

- Mechanical Punching

- Water Jet

By Application

- Fresh Produce

- Bakery & Confectionery

- Ready-to-Eat Meals

- Meat & Poultry

- Dairy & Cheese

- Pet Food

- Others

By Product Type

- Bags & Pouches

- Rolls & Wraps

- Sheets & Trays

- Lidding Films

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Perforated Packaging Market

- Amcor plc

- Mondi Group

- Sealed Air Corporation

- Constantia Flexibles

- Uflex Limited

- Bolloré Packaging Films

- A·ROO Company

- KM Packaging Services Ltd.

- TCL Packaging Ltd

- ProAmpac

- Toray Industries

- Berry Global, Inc.

- Innovia Films

- Cosmo Films

- Jindal Poly Films

* List Not Exhaustive

Methodology

USDAnalytics employs a comprehensive and multi-layered research methodology to deliver accurate, actionable insights into the Perforated Packaging Market. Our approach begins with extensive secondary research, analyzing regulatory frameworks, sustainability initiatives, technological innovations, and market dynamics across global regions. We consolidate data from company reports, press releases, trade publications, and government databases to establish a foundational understanding of material types, perforation technologies, and application segments. Primary research is conducted through interviews with key stakeholders, including packaging manufacturers, converters, retailers, and logistics operators, ensuring insights reflect operational realities and market adoption trends. Quantitative models are used to forecast market size, CAGR, and regional growth trajectories, incorporating factors such as fresh food demand, e-commerce penetration, and sustainability mandates. Additionally, USDAnalytics evaluates competitive strategies, material science innovations, and technological advancements such as laser perforation, AI-driven perforation systems, and bio-based substrates to provide a forward-looking perspective. The methodology integrates regulatory, environmental, and consumer behavior analysis, allowing clients to identify growth opportunities, benchmark competitive positioning, and optimize supply chain strategies. By combining qualitative insights with robust quantitative modeling, USDAnalytics ensures that industry professionals receive a clear, reliable, and actionable understanding of the perforated packaging market landscape.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.