Pharmaceutical Cold Chain Packaging Market Size, Overview, and Growth Outlook (2025–2034)

Pharmaceutical Cold Chain Packaging Market Set to Surpass $65.6 Billion by 2034 Amid Rising Demand for Biologics and Advanced Temperature-Controlled Solutions

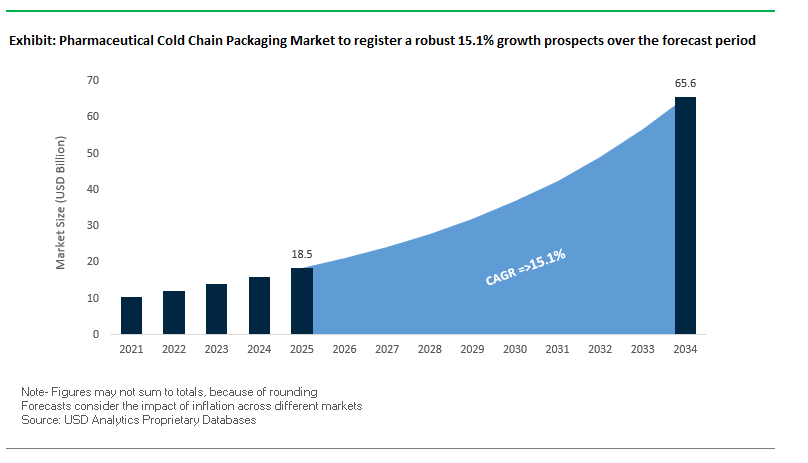

The Global Pharmaceutical Cold Chain Packaging Market is projected to grow from $18.5 billion in 2025 to $65.6 billion by 2034, reflecting a CAGR of 15.1%. This market includes temperature-controlled solutions for transporting and storing sensitive pharmaceuticals, vaccines, and biologics, ensuring safety, efficacy, and quality across the supply chain.

Key Insights for industry professionals and buyers:

- Biologics and Gene Therapies Drive Innovation: Increasing demand for ultracold and precise temperature solutions fuels advanced insulation and active container technologies.

- Shift Toward Sustainable and Reusable Packaging: Replacement of single-use EPS with recyclable, rental-based, and eco-friendly insulated systems.

- Real-Time Visibility and Digital Monitoring: Integration of IoT sensors, GPS trackers, and data loggers enhances traceability and shipment security.

- Direct-to-Patient and Last-Mile Delivery Focus: Smaller, user-friendly, and reliable cold chain solutions are emerging to support home deliveries.

- Technological Advancements: Innovations include TailorTemp, ultracold shipments without dry ice, and high-volume thermal packaging solutions.

Market Analysis: Strategic Investments and Sustainable Innovation Fuel Growth in the Pharmaceutical Cold Chain Packaging Industry

The pharmaceutical cold chain packaging industry is rapidly evolving due to heightened demand for biologics, cell and gene therapies, and temperature-sensitive vaccines. In September 2025, Cold Chain Technologies (CCT) announced a major investment and expansion in the Asia Pacific region to establish new hubs and distribution partnerships. The August 2025 expansion of Amcor’s healthcare packaging network in Costa Rica strengthened capabilities for Latin American cold chain operations. Collaborative innovations also featured prominently, with CCT and Tower Cold Chain launching new products at LogiPharma 2025, highlighting a focus on advanced, high-performance packaging solutions.

Technological breakthroughs continue to drive the market forward. In April 2025, CCT introduced TailorTemp, an environmentally conscious temperature-controlled solution, while Va-Q-tec launched ultracold shipment technology in January 2025, enabling -70°C transport without dry ice. Sustainability remains central: a February 2025 study emphasized demand for less-plastic alternatives, encouraging adoption of eco-friendly packaging across the sector.

Market consolidation and capacity expansion have also been key drivers. Pelican BioThermal launched the Crēdo Vault™ in December 2024 for bulk pharma shipments, and Cryopak acquired the gel-pack manufacturing segment of Garden State Cold Storage in July 2024. Additionally, CCT expanded its European footprint with a new facility in The Netherlands in June 2024, while the October 2023 acquisition of Exeltainer extended its global thermal packaging network.

Transformative Trends and Breakthrough Opportunities in the Pharmaceutical Cold Chain Packaging Market

Strategic Shift Toward Reusable and Rental Packaging Systems

The pharmaceutical cold chain packaging market is experiencing a decisive transition toward reusable and rental packaging systems, underpinned by lifecycle cost benefits, sustainability imperatives, and operational efficiency. Traditionally, single-use shippers have been favored for their lower upfront costs, but comparative lifecycle studies show reusable containers become more cost-effective as early as the second year of use, delivering significant savings across a nine-year span. The primary challenge lies in managing reverse logistics, which can account for nearly 17% of total system costs. However, pharmaceutical companies are now investing heavily in optimized return and refurbishment models to mitigate this. Corporate environmental, social, and governance (ESG) targets are further fueling the adoption of reusable solutions. Tower Cold Chain, for instance, secured substantial funding to expand its fleet of durable thermal packaging, citing a “global societal shift toward sustainable solutions” as the driver. Moreover, standardization of reusable container sizes is improving logistics efficiency, particularly on predictable high-volume trade routes. This reduces pallet inefficiencies, optimizes container loading, and lowers transportation emissions, aligning financial performance with sustainability goals.

Integration of IoT and Real-Time Condition Monitoring as a Standard

The role of Internet of Things (IoT) in pharmaceutical cold chain packaging has shifted from being a premium feature to becoming a standard requirement across global supply chains. Unlike traditional data loggers, which provide temperature data only after shipment completion, IoT-enabled sensors deliver continuous real-time monitoring of temperature, humidity, and location. Data is transmitted via cellular networks to cloud platforms, where automated alerts allow logistics teams to take immediate action if a temperature excursion occurs. This proactive approach prevents costly product losses and ensures regulatory compliance. For instance, the U.S. DSCSA requires interoperable electronic tracking, and IoT systems simplify compliance by automatically generating audit-ready digital records. The technology is also expanding beyond high-value biologics into bulk ocean freight and last-mile hospital deliveries, creating a resilient and transparent cold chain ecosystem. As adoption accelerates, pharmaceutical companies are increasingly using IoT data for predictive analytics, optimizing routes, minimizing risk, and reinforcing supply chain continuity.

Development of Packaging for Cell and Gene Therapy “Nano-Chains

The rise of cell and gene therapies (CGTs) is creating unprecedented demands for ultra-specialized cold chain packaging solutions. Unlike traditional biologics, autologous therapies such as CAR T-cell treatments require “nano-chain” logistics, where a single, patient-specific dose is transported from the hospital to the manufacturing facility and back under ultra-cold conditions, often below –150°C. Maintaining cell viability during this “vein-to-vein” process is mission-critical, as even minor temperature fluctuations can compromise efficacy. Current large-scale cryogenic dewars are poorly suited to these bespoke, high-value shipments. The opportunity lies in developing compact, high-performance cryogenic shippers that provide extended temperature stability in smaller formats tailored to one-dose logistics. Packaging innovation in this space not only supports the technical requirements of ultra-frozen transport but also underpins the reliability of next-generation personalized medicines. Companies that pioneer solutions for CGT cold chain packaging will be strategically positioned at the forefront of one of the fastest-growing segments in the pharmaceutical market.

Standardization and Optimization of Packaging for Last-Mile Delivery

Last-mile delivery is rapidly emerging as a critical frontier in pharmaceutical cold chain packaging, particularly with the rise of direct-to-patient and specialty pharmacy models. Current practices of using oversized shippers for single-patient deliveries create inefficiencies and unnecessary costs, particularly when routed through parcel carriers. The opportunity lies in designing compact, standardized packaging optimized for 24–72 hour temperature holds solutions that balance protection with shipping economy. A further innovation shift is underway toward alternatives to dry ice, which is hazardous and requires specialized handling. New packaging solutions utilizing phase change materials (PCMs) are being deployed to maintain refrigerated or frozen conditions without the safety risks of dry ice. For example, paper-based insulation liners with PCM inserts can provide up to 48 hours of reliable thermal protection while reducing hazardous material dependencies. Beyond logistics, patient experience is also central. Features such as easy-open perforations, curbside recyclability, and clear labeling enhance convenience, sustainability, and trust, making packaging not only a protective tool but also a driver of patient satisfaction and brand loyalty.

Competitive Landscape: Leading Pharmaceutical Cold Chain Packaging Companies Are Pioneering Reusable, High-Performance, and Digitally Integrated Solutions

The global pharmaceutical cold chain packaging market is dominated by key players who leverage materials science, engineering expertise, and innovative technologies to deliver high-performance, sustainable, and compliant packaging solutions.

Cold Chain Technologies, LLC (CCT): Expanding Global Presence with TailorTemp and Advanced Thermal Solutions

CCT provides passive thermal packaging solutions, including insulated containers, gel packs, and phase change materials (PCMs). The September 2025 Asia Pacific expansion and the October 2023 Exeltainer acquisition strengthened CCT’s global footprint. Its engineering expertise supports customized solutions for precise thermal management, making it a trusted partner for clinical trials and pharmaceutical distribution. The strategic focus emphasizes sustainable, reusable, and cost-efficient thermal packaging solutions.

CSafe Global: Integrating Active and Passive Technologies with Patient-First Digital Monitoring

CSafe offers active and passive temperature-controlled packaging, including the CSafe RKN and RAP containers, designed for long-duration ultracold shipments. Innovations such as the CGT Ultra D (-70°C for 37+ days) and Silverpod MAX RE reusable PCM shippers reinforce its position. With 70+ service centers globally and CSafe Connect digital tracking, the company excels in reliability, traceability, and patient-centric innovation, driving adoption by airlines and logistics providers.

Sonoco ThermoSafe: Strengthening Supply Chains Through Vertically Integrated Cold Chain Expertise

Sonoco ThermoSafe provides insulated boxes, pallet shippers, and reusable containers for pharmaceuticals and biologics. The July 2025 $30 million investment in Orlando boosted production and supply chain resilience. Leveraging Sonoco’s broader packaging capabilities, the company offers integrated solutions from design to thermal testing, with a strong emphasis on sustainability and value-added services.

Cryopak: Delivering Comprehensive Cold Chain Solutions with Advanced Materials and Testing Capabilities

Cryopak’s offerings include insulated containers, PCMs, gel packs, and temperature monitoring devices. The July 2024 acquisition of Garden State Cold Storage’s gel-pack segment expanded capabilities, while the new Solversa sustainable packaging line demonstrates commitment to eco-friendly innovation. Cryopak emphasizes full-service solutions, from product design to validation, ensuring integrity, performance, and compliance for high-value shipments.

Pelican BioThermal: Leading Reusable High-Performance Thermal Packaging with Sustainability at Core

Pelican BioThermal specializes in passive thermal packaging, including the Crēdo series and the Crēdo Vault™ for bulk pharma shipments. The company has achieved an EcoVadis Silver rating, ranking in the top 15% globally for sustainability. Its focus on reusable, durable, and cost-effective solutions, coupled with ongoing global network expansion, positions Pelican as a leader in sustainable pharmaceutical cold chain packaging.

Pharmaceutical Cold Chain Packaging Market Share Insights, 2025-2034

Insulated Shippers Drive Market Share by Product Type in Pharmaceutical Cold Chain Packaging

Insulated shippers command 35% of the pharmaceutical cold chain packaging market, establishing themselves as the most widely used and reliable solution for transporting temperature-sensitive drugs. Their leadership stems from their turnkey design corrugated or rigid outer boxes with integrated insulation that meets parcel carrier compliance and ensures consistent thermal performance during direct-to-patient and e-commerce shipments. Growth is further reinforced by expanding clinical trial logistics and the global uptake of biologics requiring cold storage. Phase change materials (PCMs) add high-value precision to the system, enabling long-duration thermal stability across a range of temperatures (2–8°C, –20°C, –70°C), particularly for biologics and cell therapies. Insulated containers serve bulk distribution and reusable logistics between production hubs and distributors, while gel packs, refrigerated containers, and dry ice fill specific operational roles in mid-range and ultra-cold supply chains. Data loggers and labels, though smaller in share, remain indispensable for regulatory compliance and shipment verification. This mix demonstrates how insulated shippers dominate through versatility, while specialized cold chain components add precision and redundancy to ensure integrity.

Biopharmaceuticals Lead Market Share by End-Use in Pharmaceutical Cold Chain Packaging

Biopharmaceuticals hold the largest share at 30% of the cold chain packaging market, driven by the rapid global expansion of monoclonal antibodies, recombinant proteins, and other high-value biologic therapies. These drugs are universally temperature-sensitive, typically requiring storage and transport at 2–8°C, with even brief deviations risking potency loss. The scale of global biologics production and distribution makes biopharmaceuticals the anchor end-use for cold chain packaging providers. Vaccines form the second-largest application, with volumes sustained by expanded immunization programs and the permanent establishment of frozen and ultra-cold distribution infrastructures from the COVID-19 pandemic. Clinical trials represent a smaller share by volume but are disproportionately important due to high costs, stringent regulatory oversight, and patient-specific shipments that demand advanced, often cryogenic packaging. Biological samples and blood/organ transport add specialized niches requiring tailored preservation solutions. Collectively, the market demonstrates that biopharmaceutical demand drives the bulk of cold chain revenues, while vaccines and clinical trials reinforce resilience and innovation across packaging technologies.

United States Pharmaceutical Cold Chain Packaging Market Driven by FDA Standards and IoT Integration

The United States pharmaceutical cold chain packaging market is advancing rapidly with a clear preference for passive cooling solutions such as phase change materials (PCMs) and vacuum-insulated panels (VIPs) over active systems due to their reliability, reusability, and ease of deployment. The FDA’s stringent validation requirements for packaging qualification and route risk assessments ensure that every cold chain solution meets safety and efficacy standards. Companies like Peli BioThermal are setting benchmarks with advanced bulk shippers offering thermal reliability and real-time monitoring, supporting high-value biologics and vaccines.

Another defining trend is the growth of direct-to-patient delivery and home healthcare services, which demand smaller, portable, and tamper-proof cold chain packaging formats. The surge in cell and gene therapies, many of which require ultra-low temperature storage below -80°C, is creating demand for specialized secondary packaging solutions. IoT-enabled packaging, RFID tags, and AI-driven predictive analytics are now standard features in next-generation U.S. cold chain packaging, addressing consumer safety, regulatory compliance, and operational efficiency.

Europe Pharmaceutical Cold Chain Packaging Market Shaped by EMA and GDP Guidelines

The Europe pharmaceutical cold chain packaging market is heavily regulated under Good Distribution Practice (GDP) guidelines and oversight by agencies such as the European Medicines Agency (EMA) and UK’s MHRA. These frameworks enforce validated containers for medicines, often within strict temperature bands of 2–8°C and 15–25°C, requiring packaging that meets rigorous performance standards. The European market is highly focused on sustainability and safety, with manufacturers adopting single-material, recyclable, and PFAS-free cold chain packaging.

Innovations like The Cool Chain’s ORCA high-performance isothermal containers are tailored for vaccines and biological products, offering superior insulation and reusability. Regulatory pressure combined with consumer demand is also pushing European companies toward circular economy models, ensuring cold chain packaging is designed for recyclability and reduced environmental impact while maintaining strict pharmaceutical quality compliance.

China Pharmaceutical Cold Chain Packaging Market Driven by Government Infrastructure and E-Commerce Growth

The China pharmaceutical cold chain packaging market is expanding under the country’s first five-year cold-chain logistics plan, which aims to build a cost-effective, wide-ranging, and secure infrastructure by 2025. This includes support for ultra-low temperature deliveries required by advanced biologics and vaccines. The Belt and Road Initiative is also expected to enhance pharmaceutical logistics capacity, enabling Chinese companies to expand into emerging global healthcare markets.

Leading logistics providers such as SF Express and ZTO Express are investing in advanced distribution networks, while regulatory updates now require temperature-monitoring devices to ensure compliance. A rising e-commerce market for pharmaceuticals and healthcare products is further driving demand for high-barrier, tamper-proof cold chain packaging solutions. The integration of digital traceability, blockchain pilots, and AI-driven monitoring is reshaping cold chain packaging adoption across China’s fast-growing pharmaceutical industry.

India Pharmaceutical Cold Chain Packaging Market Supported by CDSCO and Industry 4.0 Adoption

The India pharmaceutical cold chain packaging market is accelerating under CDSCO-led regulatory initiatives, including QR-coded pharmaceutical packaging for traceability and export authenticity. With India supplying over 50% of global vaccine demand and accounting for 20% of global generic medicine exports, robust cold chain packaging has become mission-critical. The Delhi Logistics and Warehousing Policy 2025 offers subsidies for cold chain upgrades, renewable energy adoption, and logistics hub development, strengthening the ecosystem.

Private investments such as Celcius Logistics’s ₹250 crore fundraise are expanding pharma-grade cold chain operations. Innovations like ALIVE, an IoT-enabled low-cost vaccine storage module, highlight the country’s focus on last-mile delivery in off-grid areas. Emerging studies on blockchain-enabled UAV systems point to future-ready, automated and audit-friendly inventory management. These advances position India as a global hub for pharmaceutical cold chain packaging aligned with Industry 4.0 transformation.

Japan Pharmaceutical Cold Chain Packaging Market Modernizing with Dual-Temperature and Smart Logistics

The Japan pharmaceutical cold chain packaging market is evolving with a dual focus on ultra-low temperature storage and precision logistics. New mRNA formulations stable at 4°C are reshaping packaging requirements, while therapies requiring -80°C logistics continue to drive innovation in advanced cold chain systems. The government is funding vaccine stockpiles and modernizing logistics through automation and digitization, reducing human error and strengthening national preparedness.

Collaborations between Toppan Inc., RM Tohcello, and academic institutions are advancing sustainable and safe pharmaceutical cold chain packaging. The market also benefits from Japan’s circular economy initiatives, promoting the use of recyclable PET materials and horizontal recycling systems. Combined with a strong focus on government-industry-academia partnerships, Japan is emerging as a leader in smart and sustainable cold chain packaging solutions.

United Kingdom Pharmaceutical Cold Chain Packaging Market Strengthened by MHRA and EPR Regulations

The United Kingdom pharmaceutical cold chain packaging market is underpinned by MHRA’s GDP guidelines, which enforce strict compliance for the distribution of medicinal products. Companies must secure a Wholesale Distribution Authorisation (WDA), reinforcing the demand for validated cold chain packaging solutions. Sustainability is a parallel driver, supported by the Extended Producer Responsibility (EPR) framework, which shifts waste management costs to producers.

Government initiatives such as the Sustainable Medicines Manufacturing Innovation Programme (SMMIP) are funding green chemistry and sustainable manufacturing projects, directly impacting pharmaceutical packaging innovation. UK manufacturers are also investing in recyclable and multi-use cold chain packaging solutions aligned with Ph. Eur. and USP standards. The move toward a circular economy for pharmaceutical packaging is accelerating, making the UK a model for sustainable cold chain packaging practices across Europe.

Pharmaceutical Cold Chain Packaging Market Report Scope

Pharmaceutical Cold Chain Packaging Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$18.5 Billion

|

|

Market Size (2034)

|

$65.6 Billion

|

|

Market Growth Rate

|

15.1%

|

|

Segments

|

By Product Type (Insulated Containers, Insulated Shippers, Refrigerated Containers, Gel Packs & Ice Packs, PCMs, Dry Ice, Others), By Temperature Requirement (Frozen, Chilled, Ambient, Deep-Frozen/Ultra-Low), By Material (Plastics, Paper & Paperboard, Metal, Others), By End-Use (Biopharmaceuticals, Vaccines, Clinical Trials, Biologics & Biological Samples, Blood & Organs, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Cold Chain Technologies, LLC, Pelican BioThermal LLC, CSafe Global, LLC, Sonoco ThermoSafe, AptarGroup, Inc., Cool Chain Logistics, Mondi Group, Intelsius, Cryopak, Sofrigam SA, Tower Cold Chain, UFP Technologies, Inc., Pluss Advanced Technologies, Novolex, ColdEX Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Pharmaceutical Cold Chain Packaging Market Segmentation

By Product Type

- Insulated Containers

- Insulated Shippers

- Refrigerated Containers

- Gel Packs & Ice Packs

- PCMs

- Dry Ice

- Others

By Temperature Requirement

- Frozen

- Chilled

- Ambient

- Deep-Frozen/Ultra-Low

By Material

- Plastics

- Paper & Paperboard

- Metal

- Others

By End-Use

- Biopharmaceuticals

- Vaccines

- Clinical Trials

- Biologics & Biological Samples

- Blood & Organs

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in Pharmaceutical Cold Chain Packaging Market

- Cold Chain Technologies, LLC

- Pelican BioThermal LLC

- CSafe Global, LLC

- Sonoco ThermoSafe

- AptarGroup, Inc.

- Cool Chain Logistics

- Mondi Group

- Intelsius

- Cryopak

- Sofrigam SA

- Tower Cold Chain

- UFP Technologies, Inc.

- Pluss Advanced Technologies

- Novolex

- ColdEX Limited

* List Not Exhaustive

Methodology

USDAnalytics follows a rigorous, multi-faceted research methodology to provide precise, actionable insights into the Pharmaceutical Cold Chain Packaging Market. Our approach combines primary research, including direct interviews with packaging manufacturers, logistics providers, pharmaceutical companies, and regulatory authorities, with secondary research encompassing corporate reports, validated trade publications, regulatory guidelines, and industry databases. Market sizing and CAGR projections are calculated using both top-down and bottom-up approaches, integrating regional adoption trends, product type performance, and temperature-specific requirements across frozen, chilled, and ultra-low segments. USDAnalytics evaluates technological innovations such as reusable packaging systems, IoT-enabled real-time monitoring, ultracold transport solutions, and sustainable materials, alongside regulatory frameworks including GDP, DSCSA, and local authority mandates. Competitive benchmarking and company-level analysis focus on strategic investments, sustainability initiatives, and high-performance packaging solutions that drive global adoption. This methodology ensures industry professionals gain an accurate understanding of market dynamics, growth drivers, and emerging opportunities, supporting informed decision-making for logistics optimization, patient safety, and regulatory compliance.

Deliverables:

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.