Phosphorescent Pigments Market Growth Accelerated by Strontium Aluminate Dominance, Safety Regulations, and Smart Infrastructure Demand (2025–2034)

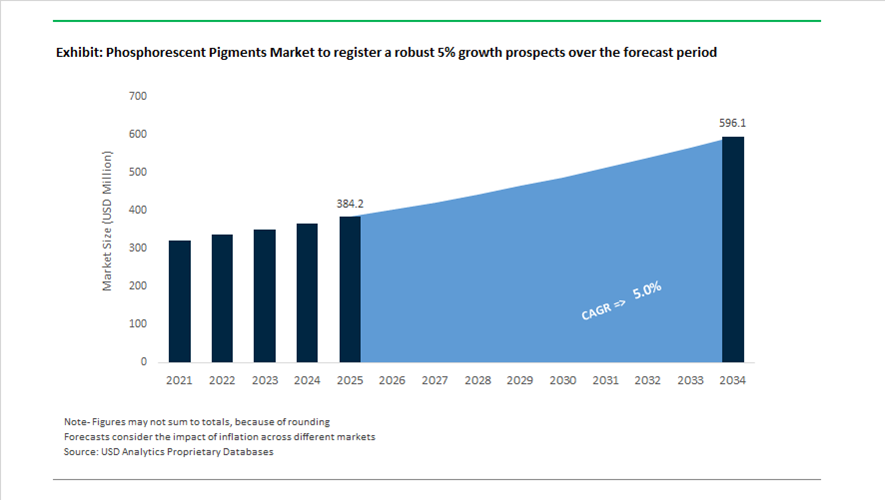

The Phosphorescent Pigments Market is projected to grow from USD 384.2 million in 2025 to USD 596 million by 2034, registering a CAGR of 5%, driven by rising adoption in safety signage, smart infrastructure, automotive applications, and energy-free lighting solutions. The market is undergoing a critical transition from legacy zinc sulfide systems to high-performance strontium aluminate pigments, which now command 63% to 65% of the global product share due to their 10x higher brightness and afterglow exceeding 12 hours. Demand is strongly anchored in safety and signage applications valued at approximately $262.4 million in 2025–2026, supported by stringent global standards such as DIN 67510 and ISO 17398 mandating zero-power emergency egress systems. The Asia-Pacific region controls nearly 46% of global manufacturing capacity, driven by large-scale production in China and advanced material innovation in Japan, while also emerging as the fastest-growing regional market due to smart city and high-speed rail investments. Additionally, automotive applications are expanding at a 7.1% growth rate in 2026, leveraging phosphorescent pigments for safety indicators and interior enhancements. However, raw material cost sensitivity remains a critical constraint, with rare-earth dopants like europium and dysprosium accounting for ~60% of production costs, exposing manufacturers to supply chain volatility and pricing risks.

The global phosphorescent pigments industry is evolving rapidly with advancements in smart infrastructure, regulatory enforcement, and high-performance material innovation. In March 2026, Keyser & Mackay expanded its market positioning in Europe by showcasing next-generation LumiNova pigment dispersions at the Paint & Coatings 2025/2026 event, targeting construction applications across Spain and Portugal. This aligns with growing demand for high-performance, durable photoluminescent coatings in infrastructure projects. In February 2026, pilot programs in South Korea and Japan marked a significant breakthrough in smart city lighting, deploying phosphorescent road markings and helipad perimeters designed for blackout-resilient urban systems, utilizing advanced encapsulated pigments with enhanced UV and water resistance.

Regulatory developments continue to act as a major demand catalyst across transportation and public safety sectors. In January 2026, updated recommendations from the United Nations (UNECE) increased compliance requirements for photoluminescent safety markings in marine and aviation environments, driving procurement of pigments meeting stricter 2026 standards. Earlier, in November 2025, Nemoto & Co., Ltd. introduced ultra-fine phosphorescent pigments at the High-Performance Plastics Expo, targeting applications in thin-film plastics and wearable electronics, highlighting innovation in miniaturized and flexible material formats. Sustainability initiatives are also gaining momentum, as seen in October 2025, when leading chemical producers emphasized the role of phosphorescent materials in green building solutions, aligning with global carbon neutrality targets through energy-free illumination technologies.

Technological crossovers and material innovation are further expanding application boundaries. In September 2025, the U.S. Naval Research Laboratory resumed operations of advanced detection systems on the International Space Station, utilizing scintillator materials closely related to phosphorescent pigment technologies, reinforcing R&D synergies between aerospace and specialty materials. Meanwhile, in August 2025, Nature Coatings scaled carbon-negative pigment production, triggering industry-wide research into bio-based carriers for phosphorescent materials, signaling a shift toward sustainable formulations. Financial and regional expansion strategies are also shaping the competitive landscape, as demonstrated in July 2025, when the International Finance Corporation committed up to $50 million to develop specialty chemical hubs in Latin America, supporting localized production of high-value luminous pigments. Collectively, these developments indicate a market transitioning toward high-performance materials, regulatory-driven demand, sustainable innovation, and smart infrastructure integration, redefining growth trajectories in the phosphorescent pigments market.

Strategic Trends and High-Value Opportunities in the Phosphorescent Pigments Market

Functional Integration of Phosphorescent Pigments in Sustainable and Bio-Fuse Architecture

The phosphorescent pigments market is moving decisively beyond decorative applications toward deep functional integration within architectural materials. In 2025, architecture is increasingly defined by responsive, energy-neutral environments, where materials themselves contribute to safety, orientation, and wellbeing without reliance on electrical systems. This shift aligns closely with the rise of “Bio-Fuse” and “Warm Minimalism” design philosophies, which emphasize natural interaction, sensory comfort, and low-energy performance.

Strontium aluminate-based phosphorescent pigments are being embedded directly into concrete, tiles, façade coatings, and interior wall systems to deliver energy-free wayfinding and ambient illumination. According to 2025 architectural design benchmarks, biophilic environments enhanced with low-level luminescent cues have demonstrated up to a 15% reduction in occupant stress, particularly in residential and healthcare-adjacent spaces. This positions phosphorescent pigments not only as visual elements but as contributors to human-centric building performance.

From a safety and compliance perspective, next-generation architectural coatings now achieve extended afterglow durations exceeding 10 to 12 hours. These high-performance phosphors reduce or eliminate the need for electrically powered emergency lighting in stairwells, corridors, and shared residential spaces, supporting compliance with LEED, BREEAM, and Net Zero building certifications. Developers are increasingly viewing phosphorescent integration as a cost-avoidance strategy over the full building lifecycle rather than a design add-on.

A parallel trend is the adaptive reuse of industrial-grade phosphorescent pigments in premium architectural aesthetics. Materials historically used for industrial safety markings are being repurposed into high-end lofts and mixed-use developments, where glow elements serve both safety and brand differentiation. This dual-use positioning is expanding addressable demand from infrastructure and safety markets into high-margin architectural and urban redevelopment projects.

Supply Chain Security and Strategic Control of Rare-Earth Inputs

Supply chain resilience has emerged as a defining strategic concern for the phosphorescent pigments market, driven by the concentrated global availability of strontium aluminate precursors and rare-earth dopants such as europium and dysprosium. Modern phosphorescent pigments rely heavily on these inputs, creating structural exposure to geopolitical risk and raw material volatility.

Data from the U.S. Geological Survey confirms that the United States remains fully import-dependent for strontium ore, with no domestic mining activity since 1959. This structural dependency has accelerated long-term offtake agreements with suppliers in Mexico, Spain, and China, particularly following the logistics disruptions and freight volatility experienced during 2024. Pigment manufacturers are increasingly prioritizing security of supply over spot pricing to protect downstream contractual obligations.

Vertical integration is becoming a competitive moat. Leading producers are investing in upstream control of celestite processing and downstream crystallization to ensure purity consistency. This strategy directly addresses rising demand for specification-critical phosphorescent pigments used in electronics, aerospace components, and medical sensors, where trace impurity levels can compromise performance or regulatory acceptance.

As a result, the market value structure is shifting. High-purity, application-specific phosphorescent pigments now command price premiums of 25 to 35% over standard safety-grade materials. This transition reflects a broader reallocation of value from volume-driven safety signage toward specialty applications where performance reliability, certification, and traceability are decisive purchasing criteria.

Zero-Energy Indicative Lighting for Electric Vehicles and Micromobility

The rapid growth of electric vehicles and micromobility platforms is creating a compelling opportunity for phosphorescent pigments as zero-energy illumination solutions. As OEMs seek to maximize battery efficiency and reduce parasitic power losses, passive lighting technologies are gaining strategic importance for both safety and user experience.

Automotive innovation is already laying the groundwork. In late 2024, ultra-thin solar-charging automotive coatings demonstrated the feasibility of multifunctional surface layers. This development opens the door to dual-function systems in which phosphorescent pigments provide orientation lighting around charging ports, door handles, and vehicle perimeters, recharging naturally through ambient light without drawing on battery reserves.

Emergency response considerations further strengthen the opportunity. In 2025, U.S. emergency management authorities highlighted the need for clearer visual identification of battery locations and high-voltage disconnect points during EV fire incidents. Long-afterglow phosphorescent markings offer a reliable solution that remains visible in smoke-filled or power-loss scenarios, positioning these pigments as safety-critical components rather than cosmetic features.

Micromobility adoption is reinforcing demand. Cities across Europe and North America are evaluating passive visibility requirements for e-bikes and e-scooters to reduce nighttime accidents. Integrated phosphorescent wheel rims, frames, and decals provide continuous low-light visibility without increasing vehicle weight or energy consumption, creating a scalable growth channel aligned with urban mobility regulation.

Biocompatible Phosphorescent Pigments for Medical and Wearable Technologies

The medical and wearable device sectors represent one of the highest-value opportunity spaces for phosphorescent pigments, driven by demand for non-toxic, high-visibility materials in diagnostics, surgery, and continuous health monitoring. The market is transitioning toward intelligent pigments that combine optical performance with biocompatibility and regulatory safety.

Near-infrared active phosphorescent coatings are gaining traction in image-guided surgery, where visual clarity under low-light or minimally invasive conditions is critical. Research published in 2025 demonstrates that advanced phosphorescent formulations can enhance instrument visibility during complex procedures, reducing procedural risk and improving surgical precision.

At the materials level, silica-encapsulated strontium aluminate pigments are emerging as a breakthrough. These ceramic-based composites deliver afterglow durations exceeding 1,000 seconds while eliminating the toxicity concerns associated with legacy sulfide-based pigments. Their stability and safety profile make them suitable for in-vitro imaging, diagnostic devices, and research-grade biosensors.

Looking ahead, smart medical wearables represent a disruptive frontier. Prototype reactive medical tattoos and skin-mounted wearables are being developed to provide visual cues for metabolic changes such as glucose fluctuations or pH imbalance. By leveraging non-toxic phosphorescent pigments, these devices enable continuous, non-invasive monitoring, aligning with long-term trends in personalized medicine and chronic disease management.

Phosphorescent Pigments Market Share and Segmentation Insights

Strontium Aluminate Leads Phosphorescent Pigment Demand with High-Brightness Long-Afterglow Performance

Strontium aluminate accounted for 58.60% of the Phosphorescent Pigments Market by chemical type in 2025, reflecting its superior luminescent performance compared with traditional zinc sulfide pigments. These pigments provide significantly higher brightness and extended afterglow durations that can exceed 10 hours, making them suitable for safety signage, industrial coatings, and premium glow-in-the-dark materials. Strontium aluminate pigments are widely used in coatings, plastics, and printing inks that require stable photoluminescent performance. In 2025, co-doped strontium aluminate phosphors incorporating europium and dysprosium are enabling optimized trap depth and afterglow intensity, while particle size engineering and encapsulation technologies improve dispersion, water resistance, and durability in outdoor and industrial applications.

Emergency Signage Drives Phosphorescent Pigment Consumption in Photoluminescent Safety Systems

Emergency signage represented 38.60% of the Phosphorescent Pigments Market by application in 2025, reflecting the widespread use of photoluminescent materials in safety and evacuation systems for commercial and public infrastructure. Glow-in-the-dark pigments are incorporated into exit signs, stairway markings, pathway indicators, and safety labels that provide visibility during power outages or low-light conditions. Building safety regulations across many regions mandate the use of photoluminescent emergency guidance systems in hospitals, airports, high-rise buildings, and public facilities. In 2025, code-driven adoption of photoluminescent egress systems in international building standards continues to support consistent demand for high-performance phosphorescent pigments used in regulatory-compliant safety signage and evacuation infrastructure.

Phosphorescent Pigments Market Competitive Landscape

The global phosphorescent pigments market is shifting toward high-performance strontium aluminate chemistry, replacing zinc sulfide in safety-critical, infrastructure, and precision applications. Competition is shaped by ultra-long afterglow performance, rare-earth doped luminescence, vertical integration, and expansion into smart infrastructure and high-value industrial use cases.

Nemoto Sets Global Benchmark in Strontium Aluminate Pigments with Ultra-Long Afterglow Performance

Nemoto & Co., Ltd. leads phosphorescent pigment innovation through its LumiNova® technology based on strontium aluminate chemistry. These pigments deliver up to 10 times higher brightness and afterglow exceeding 30 hours compared to zinc sulfide alternatives. The Lumistar B-300 and G-300 series targets flexographic printing and plastic injection molding with enhanced weather resistance for architectural applications. Strategic focus during 2025–2026 emphasizes photoluminescent safety markings for disaster prevention, including tsunami and earthquake evacuation systems across Asia-Pacific. The company introduced “earth-friendly” pigments eliminating radioactive substances and improving non-toxic chemical stability. Product development aligns with high-durability, safety-grade phosphorescent materials for infrastructure and consumer applications.

RC Tritec Dominates Luxury and Precision Luminescence with High-Stability Super-LumiNova Pigments

RC Tritec AG specializes in high-precision phosphorescent pigments under the Super-LumiNova® brand, widely used in luxury watchmaking and aerospace instrumentation. The Grade X1 series improves afterglow performance by 60% after two hours of darkness, enhancing low-light legibility. The company maintains strong expertise in color consistency and long-term chemical stability, ensuring decades-long luminescence without degradation. Luminizing Services integrate automated dispensing and 3D-printing technologies for complex micro-component applications. Core demand comes from tier-1 Swiss watch brands and safety-critical aerospace cockpit systems requiring non-electronic illumination. Technical capabilities focus on precision-engineered, high-reliability phosphorescent materials.

DayGlo Expands Industrial Phosphorescent Applications Through Masterbatch Integration and Safety Coatings

DayGlo Color Corp leverages its integration with RPM International to scale phosphorescent pigment adoption across industrial coatings and plastic masterbatches. The BPM Series phosphorescent masterbatch enables direct incorporation into thermoplastics such as LDPE, PP, EVA, and PVC for safety equipment manufacturing. The NightGlo™ NG200 (zinc sulfide) and NGX300 (strontium aluminate) product lines address varying performance needs, including rapid charging under low-intensity light. Expansion into Latin America and Europe targets infrastructure applications such as road markings and tunnel safety systems. The Phantom™ series introduces covert phosphorescent pigments for anti-counterfeiting and brand protection, visible only under specific spectral conditions. Product strategy combines high-visibility color technology with functional phosphorescent performance.

LuminoChem Advances Machine-Readable Phosphorescent Pigments for High-Security and Anti-Counterfeiting Systems

LuminoChem Kft. focuses on advanced phosphorescent and fluorescent markers designed for machine-readable security applications rather than visual luminescence. A 2025 R&D milestone includes development of a closed-loop system combining optical-spectral pigments with dedicated detection hardware. The company specializes in near-infrared (NIR) absorbing materials and organic photoactive markers compatible with offset and gravure printing technologies. These pigments are engineered for forensic-level authentication in banknotes, tax stamps, pharmaceuticals, and high-value electronics. Strategic direction emphasizes instrumental detection and digital verification systems over conventional glow-based applications. Product portfolio supports secure supply chains and anti-counterfeiting technologies.

Zhejiang Minhui Scales Global Supply of Rare-Earth Doped Phosphorescent Pigments for Infrastructure Applications

Zhejiang Minhui Luminous Technology Co., Ltd. operates large-scale production of MH series strontium aluminate phosphorescent pigments, supplying global safety and infrastructure markets. Manufacturing scale supports cost-efficient production of long-afterglow pigments widely used in exit signage, maritime safety systems, and construction applications. The company is optimizing europium and dysprosium dopant ratios to enhance brightness while reducing rare-earth material waste. Vertical integration extends from pigment powders to finished products such as luminous PVC films, rigid boards, and adhesive tapes compliant with IMO and SOLAS standards. Strong presence in Asia supports deployment in smart city projects, including luminous pavements and bicycle paths. Production strategy emphasizes scale, cost efficiency, and infrastructure-grade photoluminescent solutions.

Japan – Technology Stewardship Anchored in Safety and Precision Applications

Japan continues to define the global performance benchmark for phosphorescent pigments through deep materials science capability and application-led regulation. Nemoto & Co., Ltd. has retained its position as the technical reference point for long-afterglow pigments, with its LumiNova® platform expanding in 2025 through the GLL-300 series. These strontium aluminate pigments are engineered for outdoor flexographic printing and spray paints, delivering unlimited excitation cycles and consistent luminance decay profiles under harsh weather exposure. Parallel innovation in late 2025 focused on micro-encapsulation technologies that address the historic hydrolyzation weakness of strontium aluminate, enabling stable deployment in water-based industrial coatings and infrastructure paints.

Demand-side policy is reinforcing this technological lead. Japan’s Ministry of Land, Infrastructure, Transport and Tourism has embedded phosphorescent materials into national disaster preparedness planning, with updated 2026 urban safety guidelines mandating emergency exit signage exceeding 12-hour afterglow persistence in coastal and high-risk zones. Consumer electronics adoption further supports premium-grade demand. In November 2025, Japanese watch and wearable manufacturers integrated ultra-pure LumiStar BG-300M pigments into bezels and interface elements to enable battery-free nighttime visibility. From January 2026 onward, the industry-wide transition to heavy-metal-free, zinc-free formulations aligns phosphorescent pigment portfolios with Japan’s 2030 environmental targets, reinforcing export credibility in regulated markets.

United States – Infrastructure Pilots and Polymer Integration Drive Market Pull

The United States phosphorescent pigments market in 2025 is being shaped by infrastructure experimentation and polymer-centric productization. Federal and state-level road safety initiatives have accelerated pilot deployments of glow-in-the-dark pavement technologies. Mid-2025 trials across select southern municipalities tested phosphorescent-infused lane markings aimed at reducing rural roadway energy consumption by up to 20%, shifting pigments from novelty applications into functional civil engineering materials.

Commercialization momentum is strongest in plastics and composites. In March 2025, Brilliant Group launched the BPM Series phosphorescent masterbatches, offering ready-to-use solutions for LDPE, PP, and PVC systems across automotive interior components and toy manufacturing. Regulatory dynamics are also influencing formulation pathways. As the 3M PFAS exit approaches completion in late 2025, U.S. pigment producers are pivoting toward europium and dysprosium dopant systems that eliminate reliance on fluorinated processing aids. Architectural and leisure construction is another growth vector. Techno Glow Products expanded shipments of ultra-glow 50-micron grades in 2025, supporting demand from architectural glass facades and glow-enhanced pool finishes where uniform particle size and transparency are critical.

India – Policy-Backed Localization and Urban Safety Deployment

India’s phosphorescent pigments industry is transitioning from import dependence toward localized precursor development and infrastructure-driven demand. Under the NITI Aayog Chemical Industry Strategy 2025, targeted incentives are encouraging domestic synthesis of strontium and rare-earth intermediates, with the stated objective of reducing import reliance for phosphorescent masterbatches by 15% by 2026. This policy framework is strengthening backward integration for domestic compounders supplying plastics, coatings, and textile segments.

Urban infrastructure initiatives are translating policy into real-world adoption. The 2025 Smart Cities Mission update highlighted the deployment of phosphorescent smart pavements in cities such as Pune and New Delhi, aimed at improving pedestrian safety in areas with inconsistent lighting. Export-oriented segments are also gaining traction. India’s textile ministry reported a notable rise in photoluminescent yarn exports during Q3 2025, driven by international demand for high-visibility activewear and compliance-driven safety apparel. At the Global Road Infratech Summit 2025, the Ministry of Road Transport and Highways reinforced its preference for recyclable construction materials, explicitly citing photoluminescent additives for national highway projects, signaling sustained public-sector demand.

Germany – Regulation-Led Innovation and Functional Hybridization

Germany’s phosphorescent pigments market is evolving under the combined pressure of regulatory tightening and advanced functional research. The October 2025 update to EU REACH Annex XVII intensified scrutiny of heavy-metal content in specialty pigments, prompting German producers such as Lanxess to pivot toward green luminescence portfolios designed to exceed 2026 toxicity thresholds. This regulatory alignment is pushing innovation beyond compliance into value-added functionality.

R&D institutions are expanding the application envelope. In late 2025, Fraunhofer-linked research programs initiated pilots for hybrid colorants that merge phosphorescent behavior with thermochromic response, targeting smart packaging and temperature-sensitive security labeling. Additive manufacturing is another differentiator. German industrial 3D printing leaders integrated strontium-aluminate-doped resins into production workflows in 2025, enabling glow-in-the-dark aerospace components and low-light machine parts where passive visibility improves operational safety. These developments position Germany as a hub for high-specification, multifunctional phosphorescent materials rather than commodity volumes.

China – Scale Economics and Nano-Enhanced Performance

China’s role in the phosphorescent pigments industry is defined by rapid scale-up and incremental performance enhancement. By December 2025, producers such as Fujian ZhanHua Chemical and Hubei Xingfa had expanded high-purity phosphorus and aluminate processing lines, leveraging shared feedstock infrastructure that also serves battery and specialty coatings markets. This scale advantage supports competitive pricing across standard phosphorescent pigment grades.

Technological differentiation is increasingly achieved through surface engineering. Surveys conducted in late 2025 indicate that more than a quarter of Chinese manufacturers have adopted nanotechnology-based surface treatments, improving pigment brightness by an average of 12% compared with conventional bulk processing. However, supply-side policy remains a critical variable. In October 2025, China’s Ministry of Commerce expanded export licensing requirements for several rare-earth-derived chemicals, tightening availability and influencing global spot prices for high-persistence green and blue-green phosphors. This regulatory overlay is prompting overseas buyers to reassess sourcing strategies while reinforcing China’s leverage in the upstream rare-earth value chain.

Comparative Snapshot – Phosphorescent Pigments by Country

Phosphorescent Pigments Market County Level Snapshot

|

Country

|

Strategic Focus

|

Primary Demand Driver

|

Structural Positioning

|

|

Japan

|

Ultra-high performance and safety compliance

|

Disaster preparedness, electronics

|

Technology benchmark, premium grades

|

|

United States

|

Infrastructure pilots and polymer integration

|

Roads, plastics, architecture

|

Application-led commercialization

|

|

India

|

Localization and urban safety

|

Smart cities, textiles

|

Policy-driven demand expansion

|

|

Germany

|

Regulatory compliance and hybrid R&D

|

Smart packaging, aerospace

|

High-spec, multifunctional innovation

|

|

China

|

Scale and nano-enhanced efficiency

|

Coatings, exports

|

Cost leadership with upstream control

|

Phosphorescent Pigments Market Report Scope

Phosphorescent Pigments Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$384.2 Million

|

|

Market Size (2034)

|

$596 Million

|

|

Market Growth Rate

|

5%

|

|

Segments

|

By Chemical Type (Strontium Aluminate, Zinc Sulfide, Alkaline Earth Silicate, Rare-Earth Doped Phosphors), By Emission Color (Green, Blue-Green, Violet, Red & Orange, Yellow & White), By Application (Paints & Coatings, Plastics, Printing Inks, Textiles, Ceramics & Glass, Emergency Signage)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Nemoto & Co. Ltd., BASF SE, Hexion Inc., Lumiere Technology, Brilliant Group Inc., Techno Glow Products, Yingde Chemical Co. Ltd., Zhongshan Allure Glow, DayGlo Color Corp., GloTech International Ltd., Dainichiseika Color & Chemicals Manufacturing Co. Ltd., Lanxess AG, United Initiators GmbH, RTP Company, Sudarshan Chemical Industries Limited

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Phosphorescent Pigments Market Segmentation

By Chemical Type

- Strontium Aluminate

- Zinc Sulfide

- Alkaline Earth Silicate

- Rare-Earth Doped Phosphors

By Emission Color

- Green

- Blue-Green

- Violet

- Red & Orange

- Yellow & White

By Application

- Paints & Coatings

- Plastics

- Printing Inks

- Textiles

- Ceramics & Glass

- Emergency Signage

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Phosphorescent Pigments Industry

- Nemoto & Co. Ltd.

- BASF SE

- Hexion Inc.

- Lumiere Technology

- Brilliant Group Inc.

- Techno Glow Products

- Yingde Chemical Co. Ltd.

- Zhongshan Allure Glow

- DayGlo Color Corp.

- GloTech International Ltd.

- Dainichiseika Color & Chemicals Manufacturing Co. Ltd.

- Lanxess AG

- United Initiators GmbH

- RTP Company

- Sudarshan Chemical Industries Limited

*- List not Exhaustive