Piperidine Market Size 2025–2034: $123.6 Million to $203.6 Million at 5.7% CAGR Driven by High-Purity Pharma Demand and Advanced Synthesis Technologies

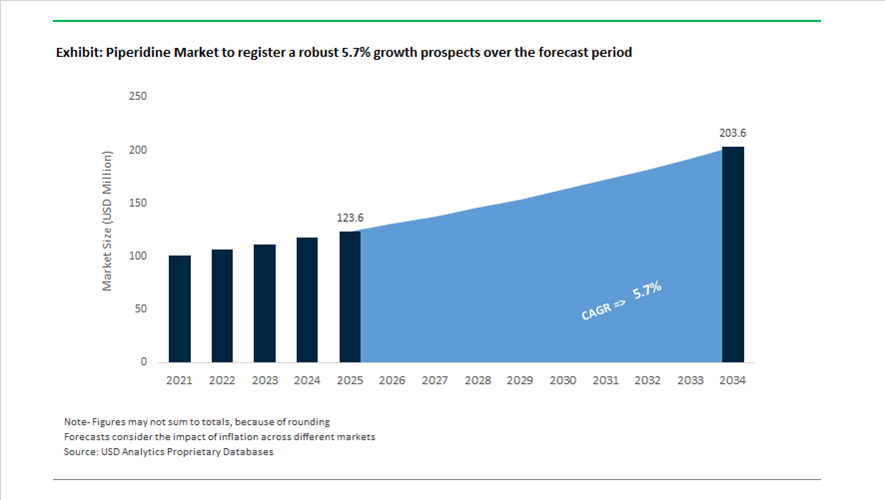

The global piperidine market is projected to grow from $123.6 million in 2025 to $203.6 million by 2034, registering a CAGR of 5.7%. Piperidine, a six-membered heterocyclic amine, is a critical intermediate in pharmaceuticals, agrochemicals, rubber chemicals, and specialty additives. Market expansion is primarily supported by rising demand for high-purity pharmaceutical intermediates, increasing complexity in drug molecule design, and continued innovation in synthetic methodologies. As regulatory frameworks tighten across the U.S., EU, and Asia, manufacturers are prioritizing high-grade piperidine production and process optimization to meet stringent impurity thresholds required for active pharmaceutical ingredient (API) synthesis.

A significant technological breakthrough emerged in December 2024 when researchers from Rice University and Scripps Research published a novel piperidine synthesis route in Science. The method integrates biocatalytic C–H oxidation with radical cross-coupling, enabling rapid construction of complex three-dimensional piperidine scaffolds. This development reduces synthetic steps and improves atom economy, accelerating drug discovery programs that rely heavily on substituted piperidine motifs. The technique is expected to lower production costs for next-generation oncology and CNS therapeutics where structural complexity is critical for receptor selectivity.

Pharmaceutical-grade production capacity is expanding, particularly in Asia. In January 2025, Jubilant Ingrevia commissioned a new human-grade Vitamin B3 facility leveraging its integrated pyridine-piperidine chemistry platform. The plant is expected to reach 65% utilization by 2028, strengthening the company’s position in high-margin nutrition and life science segments. In October 2025, Jubilant announced plans for 18 new product launches during FY2025–2026, emphasizing its Specialty Chemicals and CDMO pipeline. The company reported 8% revenue growth and an 18% increase in profit after tax in Q2 FY26, supported by expanded scientific capabilities and improved contract development win rates in piperidine-based intermediates.

High-purity requirements are reshaping production standards. By early 2025, leading producers confirmed a clear shift toward 99% purity grades, driven by FDA and EMA regulatory expectations for pharmaceutical intermediates. Manufacturers are upgrading fractional distillation systems and implementing tighter impurity profiling protocols to meet compliance benchmarks. This purity-driven differentiation is increasing capital expenditure but enabling premium pricing in regulated markets.

Strategic acquisitions are reinforcing supply security. In September 2024, Merck KGaA completed acquisition of a specialty chemicals manufacturer, expanding its piperidine production footprint and strengthening its life science portfolio. Additionally, broader specialty chemical infrastructure investments—such as BASF’s November 2025 commissioning of a high-performance production line in Nanjing—support the regional ecosystem in which piperidine functions as an intermediate for coatings additives and industrial formulations.

Demand from agrochemicals remains stable. Throughout 2024–2025, companies such as Syngenta and ADAMA introduced new pinoxaden-based herbicide formulations, where pinoxaden is a piperidine derivative. These resistance-management herbicides for cereal crops sustain baseline consumption of technical-grade piperidine in crop protection markets.

Strategic Trends and High-Value Opportunities in the Global Piperidine Market

Strategic Shift Toward High-Purity Piperidine as a Pharmaceutical Building Block

The global piperidine market is undergoing a structural upgrade from bulk heterocyclic amine supply toward high-purity, value-added pharmaceutical intermediates. Piperidine has emerged as a privileged scaffold in medicinal chemistry, featuring in more than 20% of FDA-approved drug molecules. This structural relevance is driving sustained demand for pharmaceutical-grade piperidine and its derivatives, particularly as drug discovery pipelines become more complex and impurity tolerance thresholds tighten.

During 2024–2025, pharmaceutical R&D momentum has been strongest in Central Nervous System and oncology therapeutics, where piperidine-based cores offer superior bioavailability and blood-brain barrier permeability. Industry pipeline analysis indicates that roughly 15% of Phase II and Phase III neurodegenerative drug candidates incorporate piperidine-derived motifs, underlining its importance in late-stage clinical development rather than early exploratory chemistry alone. This shift has materially raised demand for consistent, GMP-compliant supply.

Capacity expansion has followed this demand signal. In June 2024, BASF announced an expansion of high-purity intermediate production at its Ludwigshafen site, explicitly targeting pharmaceutical-grade piperidine derivatives. These investments reflect the reality that even trace-level impurities can destabilize downstream API synthesis, particularly in antiviral and anti-inflammatory drugs. Parallel to this, suppliers such as Vasudha Pharma Chem and Koei Chemical have repositioned their portfolios away from technical-grade volumes toward 99% plus purity building blocks. This transition allows suppliers to capture significantly higher margins while embedding themselves deeper into regulated pharmaceutical supply chains.

Expanding Role of Piperidine Scaffolds in Next-Generation Agrochemicals

Piperidine chemistry is also gaining strategic importance in agrochemical innovation, where the industry is moving away from high-dose legacy actives toward low-application-rate, high-selectivity molecules. Piperidine-based heterocycles are increasingly favored in fungicide and insecticide discovery due to their tunable bioactivity and favorable environmental profiles.

In September 2025, peer-reviewed updates in the Journal of Agricultural and Food Chemistry highlighted that heterocyclic scaffolds such as piperidine and pyrimidine now dominate advanced fungicide research programs. These structures allow precise molecular modification, enabling site-specific pest control and improved resistance management. This trend is particularly relevant as resistance erodes the efficacy of older chemistries across cereals, fruits, and specialty crops.

Strategic portfolio realignment has followed suit. In March 2024, Vertellus completed the acquisition of a specialty chemicals firm to strengthen its position in pyridine and piperidine intermediates. This move reflects a broader industry pattern in which leading agrochemical suppliers seek direct control over advanced heterocycle supply rather than relying on fragmented merchant producers. As regulatory pressure increases on application rates and environmental persistence, piperidine-based actives are positioned as premium components in future crop protection portfolios.

Ultra-High-Purity Piperidine for Semiconductor Lithography and Cleaning Applications

Beyond life sciences, the migration of semiconductor manufacturing toward sub-5 nanometer and emerging 2 nanometer nodes has opened a high-value niche for ultra-high-purity piperidine derivatives. Hindered amines such as 2,2,6,6-tetramethylpiperidine and its lithium salt, LiTMP, are increasingly deployed in advanced lithographic and post-etch processes where molecular precision is critical.

Technical reports published in December 2025 demonstrate that LiTMP is becoming a key reagent for regioselective lithiation in complex heterocycle synthesis used in logic and memory chip fabrication. This chemistry enables highly selective intermediate trapping that conventional reagents cannot achieve, supporting scalable production of advanced semiconductor materials. As fabs push toward tighter geometries, demand for electronics-grade piperidine derivatives with impurity levels measured in parts per billion is rising accordingly.

In parallel, piperidine-derived hindered amines are being adapted for post-etch residue removal and corrosion inhibition. These compounds help protect ultra-fine metal interconnects during wafer cleaning in three-dimensional transistor architectures. While volumes remain modest compared to pharmaceutical demand, margins are materially higher, creating an attractive opportunity for suppliers capable of meeting Grade 5 electronics specifications.

Piperidine-Based Catalysts for Sustainable Polymerization and Green Manufacturing

Sustainability-driven chemistry represents another structurally attractive growth avenue for the piperidine market. TEMPO and related piperidine-based N-oxyl radicals have become essential catalysts in controlled radical polymerization and selective oxidation reactions, particularly in the production of biodegradable and bio-based materials.

Green Chemistry Reviews published in 2025 emphasized the role of TEMPO in electrochemical oxidation processes that eliminate the need for toxic stoichiometric oxidants. These catalytic systems are central to the production of cellulose nanofibers and high-performance polyamides aligned with the EU Green Deal and broader decarbonization mandates. As regulatory frameworks increasingly penalize waste-intensive processes, TEMPO-enabled pathways are moving from laboratory scale into industrial deployment.

Further downstream, mid-2025 studies highlighted the use of TEMPO-oxidized cellulose in microbial fermentation systems for biobutanol production. This application improves fermentation stability and yield, illustrating how piperidine-based catalysts are becoming integral to hybrid chemical-biotechnology manufacturing models. For piperidine producers, this represents a durable opportunity to participate in carbon-neutral value chains with strong policy and investor backing.

Piperidine Market Share and Segmentation Insights

Industrial Grade Piperidine Leads Market Demand in Rubber Chemicals and Agrochemical Intermediates

Industrial grade piperidine accounted for 48.60% of the Piperidine Market by purity grade in 2025, reflecting its extensive use in large-volume chemical manufacturing processes. Industrial grade material is widely used as an intermediate in the production of rubber processing chemicals, agrochemical intermediates, and specialty chemical synthesis where cost efficiency and consistent chemical quality are essential. The global scale of rubber and agrochemical manufacturing continues to support stable demand for piperidine derivatives used in accelerator production and chemical synthesis pathways. In 2025, strong linkage between piperidine demand and rubber chemical production for tire manufacturing continues to influence market consumption patterns as global vehicle production sustains demand for industrial rubber products.

Pharmaceuticals and Biotechnology Sector Drives Piperidine Consumption in API Synthesis

Pharmaceuticals and biotechnology represented 48.60% of the Piperidine Market by end-use industry in 2025, reflecting the importance of piperidine derivatives as key intermediates in active pharmaceutical ingredient synthesis. Piperidine-based structures are widely used in drug development for their versatile chemical reactivity and ability to form complex molecular frameworks used in modern pharmaceutical compounds. The pharmaceutical industry’s focus on advanced therapeutics continues to sustain demand for high-purity piperidine intermediates used in drug manufacturing. In 2025, growth in specialty pharmaceuticals and orphan drug development is increasing demand for customized piperidine derivatives produced by contract development and manufacturing organizations that supply specialized intermediates for small-volume, high-value pharmaceutical synthesis programs.

Piperidine Market Competitive Landscape

The global piperidine market is evolving toward ≥99.5% purity standards, supported by catalytic hydrogenation technologies and rising CDMO partnerships. Competitive dynamics are shaped by vertical integration, pharmaceutical-grade intermediates demand, and scalable production of heterocyclic amines for agrochemicals, APIs, and specialty materials.

Vertellus Expands Integrated Pyridine-Piperidine Portfolio Through Strategic Acquisitions and Specialty Applications

Vertellus (Aurorium) is strengthening its position in the piperidine market through portfolio expansion and vertical integration across pyridine derivatives. The acquisition of IM Chemicals and Chemtrade specialty ingredients enhances control over feedstock and derivative production, reducing exposure to raw material volatility. The company supplies high-purity piperidine and 2,6-lutidine for catalytic applications, pharmaceutical API synthesis, and agrochemical intermediates. Expansion into medical devices and nutraceuticals leverages piperidine-based molecules for antimetastatic and specialty therapeutic applications. Manufacturing operations comply with stringent North American and European regulatory standards, ensuring high-quality output. Strategy focuses on specialty solutions, high-purity intermediates, and diversified end-use markets.

Jubilant Ingrevia Scales CDMO Capabilities with Multi-Product Plant and Expanding Piperidine Derivative Pipeline

Jubilant Ingrevia Limited is transitioning into a CDMO-driven specialty chemical leader with strong focus on piperidine derivatives. The February 2026 groundbreaking of a Multi-Product Plant (MPP) in Gajraula supports increasing demand for complex heterocyclic intermediates. The company maintains a pipeline of approximately 50 products, with 18 launches planned for FY2026, including diketene derivatives utilizing piperidine frameworks. CDMO revenues are projected to grow from ~₹3 billion in FY26 to ~₹12 billion by FY28, driven by specialty chemicals and nutrition segments. Expansion of scientific talent by 50% and a dedicated tech-transfer organization improves execution of complex synthesis projects. Strategy emphasizes high-value CDMO services, advanced intermediates, and pharmaceutical-grade production.

BASF Strengthens High-Purity Piperidine Production with Verbund Integration and Catalytic Hydrogenation Technology

BASF SE leverages its Verbund model to produce high-purity piperidine and intermediates at industrial scale. Capacity expansion at the Ludwigshafen site enhances production of piperidine and 4-piperidone for pharmaceutical and crop protection applications. Advanced catalytic hydrogenation of pyridine, using molybdenum disulfide or noble metal catalysts, enables production of ≥99.5% purity material. Biomass-balanced feedstock integration supports lower carbon footprint for downstream applications in flavors, fragrances, and specialty chemicals. The Verbund system captures and reuses by-products, improving process efficiency and cost optimization. Strategy focuses on sustainable production, high-purity intermediates, and integrated chemical manufacturing.

Koei Chemical Delivers Ultra-High-Purity Piperidine for Precision Pharmaceutical and Electronic Applications

Koei Chemical Co., Ltd. specializes in high-purity nitrogen compounds with strong focus on precision synthesis and specialty amines. The company offers 99.5% purity piperidine with ultra-low moisture content (≤0.1%), meeting zero-defect requirements for pharmaceutical and electronic applications. Growth in its Amines and Pyridine Bases segment reflects demand for aminopiperidine and tetramethylpiperidine used in polymer stabilization. Expansion of custom synthesis services includes gas-phase and high-pressure reaction technologies for complex molecular architectures. Quality assurance systems comply with stringent regulatory standards, including METI specifications. Strategy emphasizes ultra-high purity, custom synthesis, and specialty nitrogen chemistry.

Dr. Reddy’s Integrates Piperidine Supply into API Manufacturing for Chronic Disease Therapeutics

Dr. Reddy’s Laboratories operates as a major downstream consumer and manufacturer of piperidine-based APIs. The company showcased over 250 APIs at CPHI China 2025, highlighting piperidine as a core building block for oncology, cardiology, and pain management drugs. Annual API production exceeds 2,100 metric tons, supported by multi-sourcing strategies for key starting materials to ensure supply stability. Regulatory compliance includes USFDA-approved facilities across more than 80 countries, with strict control of nitrosamine and azido impurities. Dedicated HPAPI facilities support synthesis of highly potent compounds with OEL thresholds as low as 0.1 µg/m³. Strategy focuses on integrated API manufacturing, regulatory excellence, and high-value pharmaceutical applications.

Lianhetech Expands Large-Scale Piperidine Production with China-Plus-One Strategy and Automation Investments

Lianhe Chemical Technology (Lianhetech) provides large-scale technical-grade piperidine for global agrochemical, pharmaceutical, and performance chemical markets. The company operates across crop protection, pharmaceuticals, and engineering services, supplying piperidine as a key intermediate and catalyst. Production capabilities include technical-grade piperidine (98% purity) for rubber and polymer additive applications. Capital investment in automation enhances consistency and reduces manual intervention in heterocyclic amine synthesis. The company is expanding equipment and engineering services to support global partners adopting China-plus-one sourcing strategies. Portfolio includes substituted piperidines and piperidinones for next-generation pharmaceutical compounds. Strategy emphasizes scale, cost efficiency, and global supply chain integration.

India – Policy-Led KSM Localization and CDMO Capacity Alignment

India’s piperidine industry in 2025–2026 is being reshaped by explicit policy intervention aimed at pharmaceutical self-sufficiency. Under PLI Scheme 2.0, nitrogen heterocycles such as piperidine have been elevated to priority KSM status, directly linking incentive eligibility to domestic production volumes. This has materially altered sourcing strategies for API manufacturers seeking to reduce exposure to Chinese intermediates. The introduction of a Minimum Import Price in December 2025 on select piperidine-based intermediates has further strengthened this localization push by curbing aggressive price undercutting, particularly in the low-margin generics segment. Together, these measures are repositioning India from a formulation-heavy market to an upstream-integrated heterocycle producer.

On the supply side, capacity expansion and process innovation are progressing in parallel. Jubilant Ingrevia announced debottlenecking at its Bharuch facility to raise output of pyridine and piperidine derivatives by roughly 15%, targeting long-term CDMO contracts rather than spot sales. Regulatory easing has complemented this expansion, with the withdrawal of select BIS QCOs in December 2025 reducing compliance friction for MSME downstream users. At the technology frontier, breakthroughs from Indian Institute of Chemical Technology on non-noble metal hydrogenation catalysts signal a structural cost reduction pathway, with reported yields approaching 95% at industrial scale.

China – Scale Efficiency, Digitalization, and Transitional Export Momentum

China remains the largest global producer of piperidine and related heterocycles, but its 2025 trajectory reflects a transition from volume dominance toward digitally optimized, sustainability-aligned manufacturing. The MIIT’s 2026 Blueprint for chemical digitalization has created tangible incentives for producers to adopt AI-driven yield optimization and real-time process controls. Leading manufacturers in Jiangsu and Zhejiang have responded by integrating advanced vapor recovery systems, meeting newly mandated 99.9% recovery thresholds for amine distillation units introduced in early 2025.

Despite India’s import protection measures, Chinese exports of nitrogen-containing heterocycles to India surged 50% year-on-year between January and October 2025, as buyers front-loaded procurement ahead of MIP enforcement. This highlights China’s short-term pricing leverage even as downstream markets tighten. At the same time, strategic experimentation is underway. Shanghai Synchem Pharma piloted a bio-based piperidine route using biomass-derived precursors, positioning Chinese suppliers to defend competitiveness under emerging carbon-accounting frameworks in regulated export markets.

United States – Oncology Manufacturing and Supply Chain Security Imperatives

The United States piperidine market is tightly coupled to its small-molecule pharmaceutical pipeline, particularly oncology. In 2025, combined manufacturing investments exceeding USD 45 billion by Eli Lilly and Bristol Myers Squibb underscored the scale of domestic capacity being built for advanced APIs. Piperidine scaffolds are embedded in more than 30% of FDA-approved oncology small molecules, making secure access to this heterocycle a strategic concern rather than a commodity procurement decision.

Regulatory frameworks are reinforcing this prioritization. The FDA’s 2025 supply chain resilience strategy formally classified piperidine and its derivatives as critical chemicals for essential medicines, encouraging reshoring and long-term supplier qualification. Parallel to this, EPA-backed green chemistry grants are accelerating the development of solvent-free amination routes, particularly for agrochemical-grade piperidine derivatives. This combination of security-driven sourcing and process sustainability is redefining supplier selection criteria in the US market.

Germany – High-Purity Heterocycles Anchored in EU Health Sovereignty

Germany’s piperidine industry occupies a high-value niche shaped by regulatory leadership and advanced materials demand. In October 2025, BASF SE announced a strategic realignment of its Performance Chemicals portfolio to reinforce Verbund integration for high-purity heterocycles. This move directly supports the European Union’s 2026 Health Sovereignty agenda, which emphasizes secure access to pharmaceutical building blocks produced under EU regulatory standards.

Innovation-led demand is also emerging beyond pharma. Merck KGaA showcased piperidine-based light stabilizers designed for flexible OLED displays and automotive coatings, expanding the application envelope of this heterocycle. Concurrently, German producers have set the global benchmark in the 2025 REACH substance evaluation for amines, establishing best practices for transport, storage, and worker safety that are increasingly referenced by non-EU regulators.

Japan – Precision Chemistry and Isomer-Specific Differentiation

Japan’s role in the piperidine industry is defined by precision manufacturing and derivative specialization rather than bulk output. In May 2025, Koei Chemical expanded its N-methyl piperidine and piperidone lines to serve the rapidly growing smart agrochemicals market in Southeast Asia, where formulation performance and impurity control command price premiums. This downstream orientation aligns with Japan’s broader specialty chemicals strategy.

Process engineering advancements further differentiate Japanese suppliers. Domestic equipment manufacturers introduced semi-continuous membrane dispersion reactors in 2025, achieving 97.5% selectivity for targeted piperidine isomers. By reducing reliance on energy-intensive distillation, these systems lower operating costs while improving consistency, reinforcing Japan’s competitive edge in high-specification pharmaceutical and agrochemical intermediates.

Comparative Snapshot – Piperidine Industry by Country

Piperidine Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

2025–2026 Focus Area

|

Structural Position

|

|

India

|

API self-sufficiency and import protection

|

KSM localization and CDMO supply

|

Emerging upstream hub

|

|

China

|

Scale and digital efficiency

|

AI-enabled production and sustainability

|

Volume-dominant exporter

|

|

United States

|

Oncology pipeline security

|

Domestic sourcing and green chemistry

|

Security-driven market

|

|

Germany

|

EU health sovereignty and materials innovation

|

High-purity heterocycles

|

Regulatory benchmark

|

|

Japan

|

Precision derivatives and process selectivity

|

Isomer-specific differentiation

|

Specialty supplier

|

Piperidine Market Report Scope

Piperidine Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$123.6 Million

|

|

Market Size (2034)

|

$203.6 Million

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Purity Grade (Pharmaceutical Grade, Industrial Grade, Specialty Intermediate Grade), By Product Derivative (Piperidone, Piperidinol, Pipecolic Acid, Piperidineethanol, Substituted Piperidines), By Application (Pharmaceutical Intermediates, Agrochemical Intermediates, Rubber Chemicals, Chemical Synthesis & Catalysis, Specialty Chemicals), By End-Use Industry (Pharmaceuticals & Biotechnology, Agriculture & Crop Protection, Automotive & Rubber Processing, Electronics & Displays, Research Institutions)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Jubilant Ingrevia Limited, Koei Chemical Co. Ltd., Vertellus, Vasudha Pharma Chem Limited, Jiangsu FOPIA Chemicals Co. Ltd., Zhejiang Huangyan Wanfeng Chemical Co. Ltd., Shanghai Synchem Pharma Co. Ltd., Solvay SA, Loba Chemie Pvt. Ltd., Alfa Aesar, Tokyo Chemical Industry Co. Ltd., Evonik Industries AG, Sichuan Hengkang Technology, Changzhou Aitan Chemical

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Piperidine Market Segmentation

By Purity Grade

- Pharmaceutical Grade

- Industrial Grade

- Specialty Intermediate Grade

By Product Derivative

- Piperidone

- Piperidinol

- Pipecolic Acid

- Piperidineethanol

- Substituted Piperidines

By Application

- Pharmaceutical Intermediates

- Agrochemical Intermediates

- Rubber Chemicals

- Chemical Synthesis & Catalysis

- Specialty Chemicals

By End-Use Industry

- Pharmaceuticals & Biotechnology

- Agriculture & Crop Protection

- Automotive & Rubber Processing

- Electronics & Displays

- Research Institutions

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Piperidine Industry

- BASF SE

- Jubilant Ingrevia Limited

- Koei Chemical Co. Ltd.

- Vertellus

- Vasudha Pharma Chem Limited

- Jiangsu FOPIA Chemicals Co. Ltd.

- Zhejiang Huangyan Wanfeng Chemical Co. Ltd.

- Shanghai Synchem Pharma Co. Ltd.

- Solvay SA

- Loba Chemie Pvt. Ltd.

- Alfa Aesar

- Tokyo Chemical Industry Co. Ltd.

- Evonik Industries AG

- Sichuan Hengkang Technology

- Changzhou Aitan Chemical

*- List not Exhaustive